CRERF - Carrefour Has Its Work Cut Out

2023-09-08 05:26:19 ET

Summary

- Carrefour is positioning itself at the crossroads of technology and retail.

- The company is now fully focused on Europe and Latin America, and it faces challenges in both regions.

- Its financial results revealed a mixed picture. The transformation is still in the early days.

When presenting its strategic plan to 2026 last year, the French company claimed to have "successfully completed its turnaround". Not quite true. There are signs of progress, but the transformation is far from over.

In a quest to become profitable again, Carrefour had to make some painful decisions. A full exit from Asia was an obvious one. The management, however, is staying the course, undeterred by the prospect of low growth in Europe and encouraged by a return to economic normalcy in South America.

Digital strategies - in different business areas, not limited to retail - have taken center stage. In e-commerce, the results are already showing, specifically in home delivery. Data and media is the newest venture with potential.

Carrefour is clearly no longer in denial or idle. The management is putting multiple strategies into action to rework the company. But the burdens they have inherited will keep pulling them back, and the headwinds will make timelines uncertain.

Investors interested in the stock may find it affordable at present, but they should be prepared to temper their expectations.

Hard going

Although a retail pioneer bringing hypermarkets and own-brand products to France, Carrefour has not had it easy. The group stumbled through years of low sales volumes and profit warnings, losing market share to leaner and nimbler rivals. The difficult integration with Promodès post-merger in 1999 could be when its troubles began.

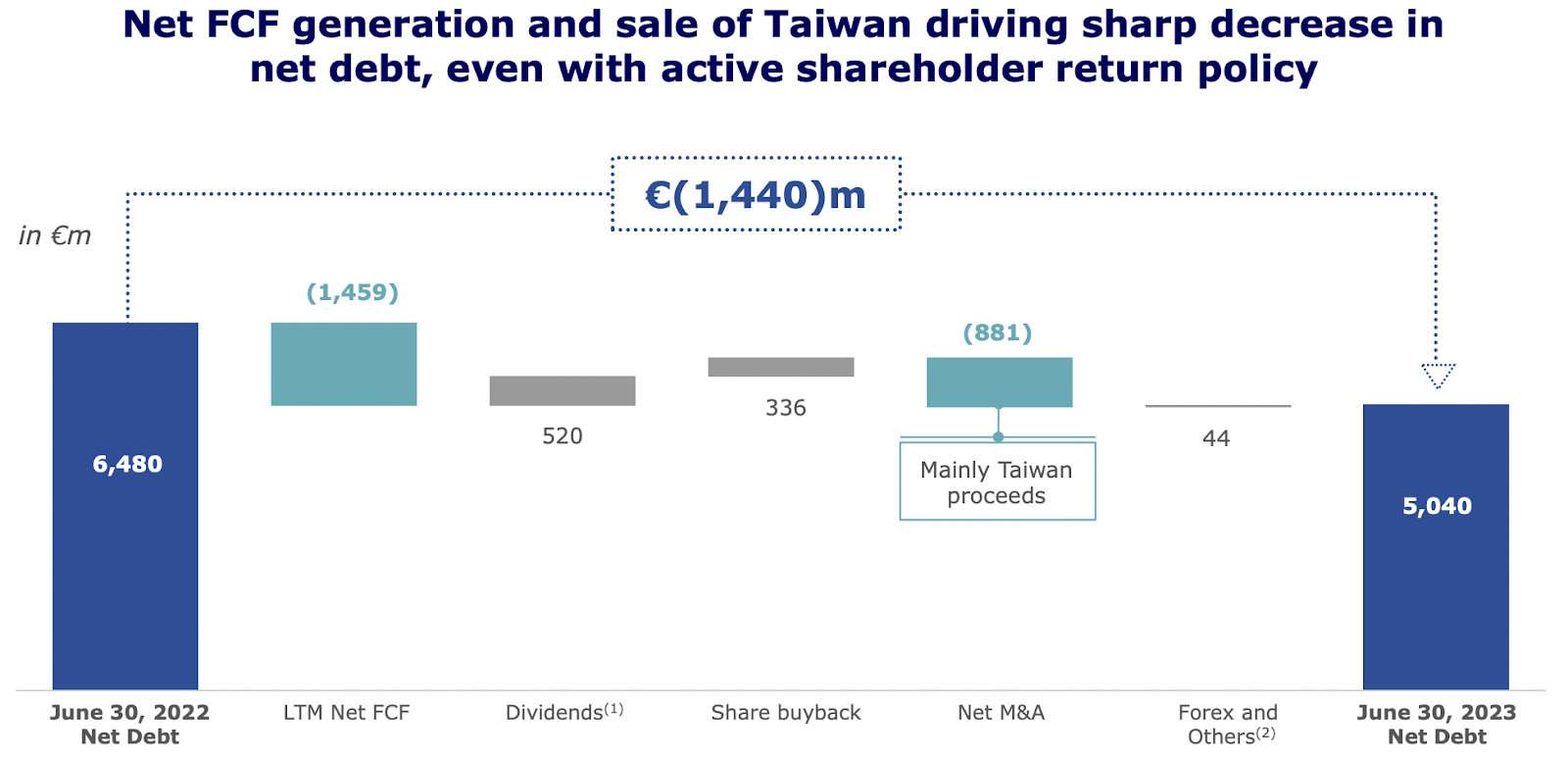

Internationally, the management blundered trying to expand too fast. Overreached and pushed by activist investors, in the end Carrefour had to exit country after country in quick succession. The most painful departure had to be from emerging Asia, especially China. The group completed the pullout from the region with the sale of its Taiwanese business in 2022.

That leaves the company with a large portfolio of mature, low-growth European operations. France contributes 46% of sales and the rest of Europe 28%, which leaves 26% coming from Latin America, the only bright spot where Carrefour has been doing surprisingly well. It has become a staple in Brazil (which the group entered in 1975) as the leading supermarket chain for seven years running. With the recent acquisition of Grupo Big (formerly Walmart's), Carrefour Brasil is the new market leader.

Remodeling

There has long been talk of hypermarkets, Carrefour's original business model, being outdated. But it took the group many decades to start changing: only under CEO Alexandre Bompard, who came in 2017 and is now in his second term , has it gotten serious about paring down large shops as well as digital strategy.

The prime attention is on digital transformation, which Carrefour's Digital Retail 2026 makes apparent. With an investment of €3bn over four years, the group aims to triple its e-commerce gross merchandise value to €10bn. Of course, its 12,000-store network is not going anywhere. So the true focus, as has been the trend in retail, is going omnichannel, combining physical and digital.

This means that Carrefour's unique value proposition - of offering a wide selection of food, clothes and white goods at low prices from a single location - needs to become available online. The first order of business is cementing online operations in key markets of France and Brazil, through leadership in express delivery and quick commerce. Home delivery is currently Carrefour's fastest growing segment.

The other priority is adding low-cost wholesale stores (like the Atacadão chain which has been a driver of growth for the Brazilian subsidiary) as an attempt to adapt to the changing economic and demographic realities; about 200 more will be opened in Brazil by 2026 and France's first is supposed to be launched later this year.

But making money in online retail is notoriously hard, given the already thin margins of grocers - Carrefour's operating margin hovers around 2%. So the company has been looking into additional sources of revenue.

Through Carrefour Links , introduced in 2021, it offers customized artificial intelligence and data analysis services. It attracted over 450 clients within a year and by 2026 is expected to bring extra €200mn in recurring operating income. Earlier in June, the group teamed up with Publicis, an advertising multinational, to form Unlimitail targeting growing retail media markets in Europe and Latin America.

Another fresh opportunity is in real estate, where Carrefour is finally getting a move on. Around the time the media business launched, Carrefour Brasil revealed an intention to carve out its more than 450 assets (with earning power of over $287mn in net operating income). The first to be monetized are five distribution centers and four retail stores that have been newly acquired by Brazil's Barzel Properties and Singaporean sovereign wealth fund GIC, to be leased back under 20-year renewable lease agreements.

Financials

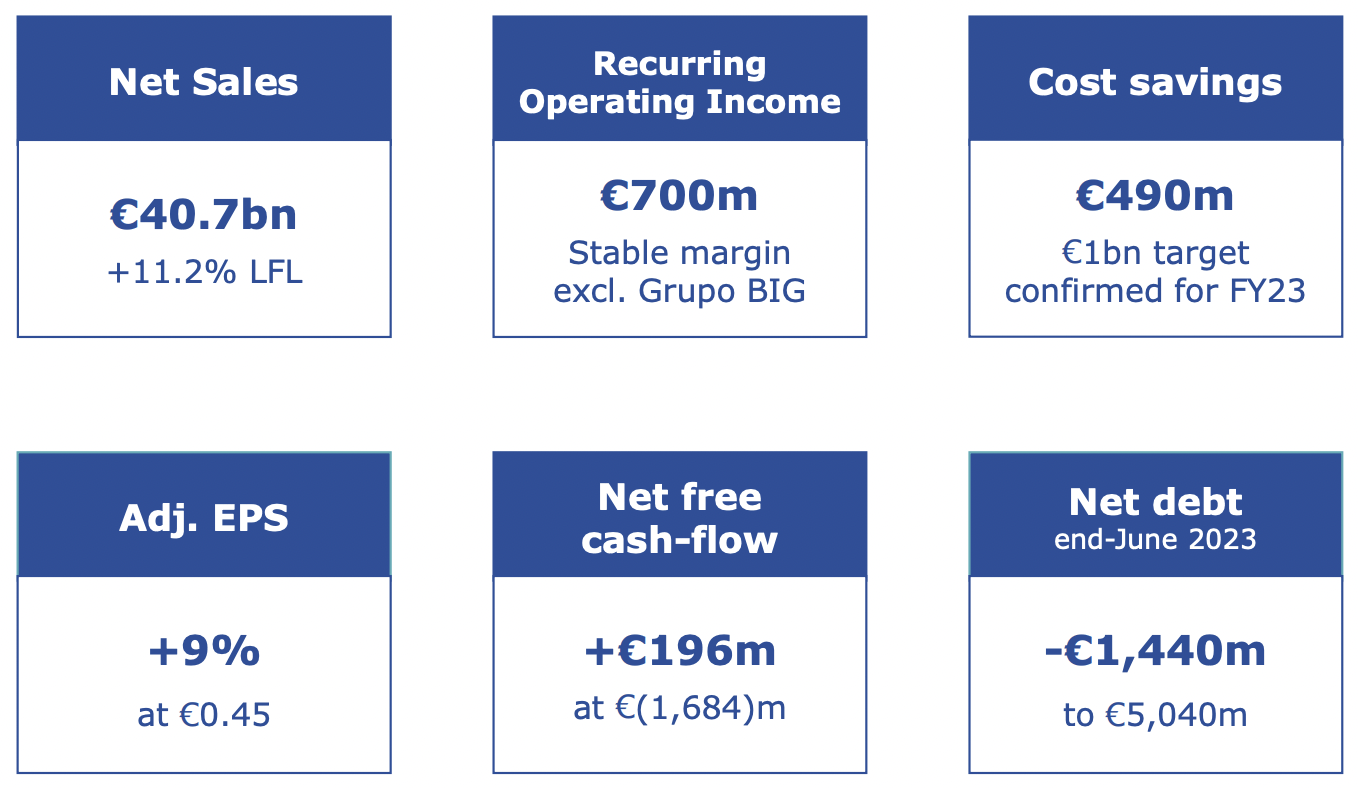

The latest results for the first half of 2023 were encouraging, reflecting the progress on initiatives set out in the 2026 plan. Sales for Q2 were up by 4% and 8% for H1; e-commerce gross merchandise value increased by 20% in both reporting periods.

At the same time, recurring operating income reduced by 9.6%, mostly because of the ongoing integration of Grupo BIG stores in Brazil - although the realized cost synergies of about €99mn, exceeded the negative effect of -€65mn.

Key highlights of H1 2023

{kind=link}

Operating performance was the best in France which added 39% to recurring operating income in H1 thanks to favorable pricing decisions, rising sales of private label products - which are projected to make up 40% of group-wide sales by 2026 - and cost-cutting measures (through, among other things, optimized inventory management). Like-for-like sales grew by 7% driven by food items.

Elsewhere, positive results were reported in Spain (8.5% adjusted gain in sales) and Argentina (122%). Overall, the Latin American segment continues to grow at a brisk pace, averaging a 21% increase in sales (despite lukewarm numbers from Brazil lately) versus 7.7% in Europe. Though recurring operating income for the latter region remained flat, it fell quite dramatically, by 30%, in Latin America (again due to the teething pains post-merger in Brazil).

In the first half of the year, the group managed to cut costs by €490m, as part of the larger plan aiming for €4bn in savings by 2026. Net income received a one-time boost from the capital gain from the disposal of Carrefour Taiwan. Adjusted net income was up by 5% and adjusted EPS by 9%.

Among other financial targets of Carrefour 2026 is a net free cash flow (after financing costs and lease payments) of more than €1.7bn. There has been little headway to that end, with net free cash flow improving by some €300mn in H1 (+€1.5bn in the last 12 months). The overall figure is still very much negative at -€1.7bn, the polar opposite of the desired value.

{kind=link}

For all that, the group stays decently capitalized and tries to control debt. With Baa1 by Moody's and BBB by S&P, it issued its latest bond of €500mn in May 2023 which brought the total portfolio to €7.3bn. Net financial debt was recorded at €5.0bn on 30 June 2023, down from €6.5bn a year ago. Operating cash flow is almost 30% of debt, which is acceptable.

To make its remodeling, organizational and digital initiatives possible, Carrefour bumped up its annual capital expenditure to €2bn. About €687mn was spent in H1 2023. Only superior technology and cost efficiency can ensure the preservation of margins in today's increasingly cutthroat world of omnichannel retail.

Stock

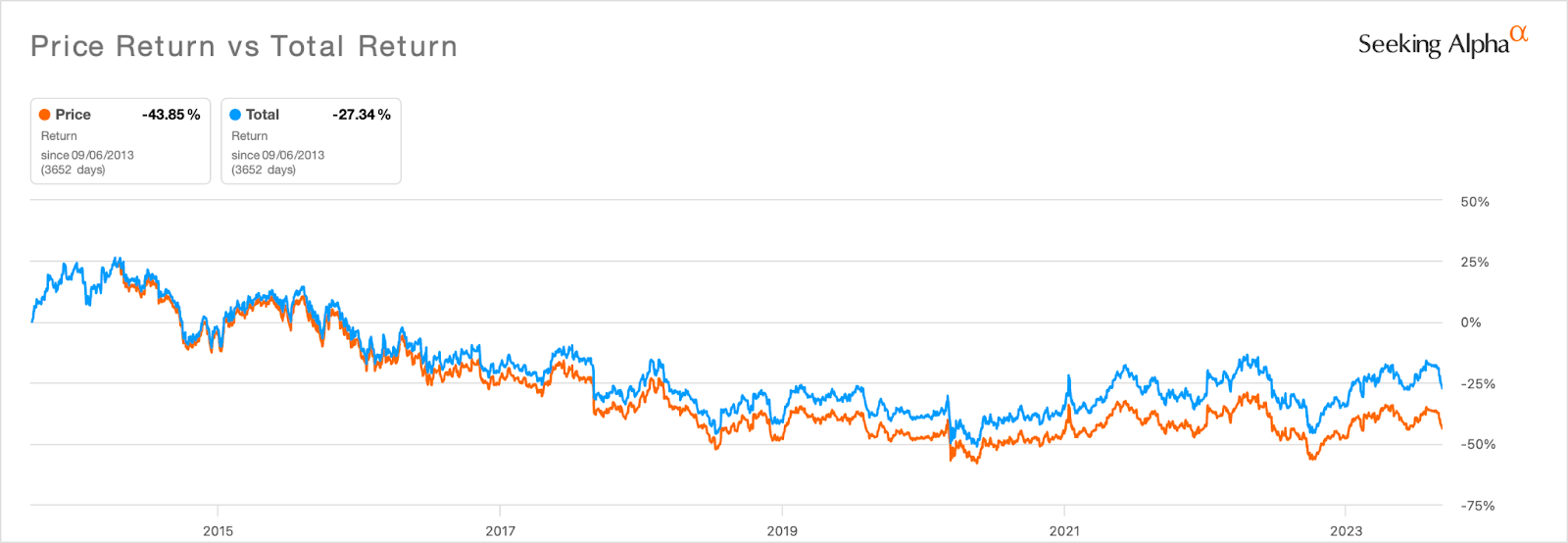

Euronext Paris listed Carrefour (ENXTPA:CA) has been a very modest performer, and only dividends have cushioned the returns. Over the past year, the stock went up by only 2.9% and 6.4% with dividends, more than other French retailers but way below the overall market.

On the other hand, [[CRRFY]] returned 8.2% and 11.8% with dividends (SP500TR: 16.6%).

{kind=link}

Carrefour has been paying dividends for the past decade but in an erratic manner. After reaching an all-time low in 2020, the amount and the yield both have resumed growth. The stock currently generates 3.2% (at a payout ratio of 33%); the yield is expected to go up to almost 5% over the next couple of years.

The company has also been buying back shares since 2021 when its turnaround started bearing fruit. This year it is repurchasing €800mn worth of stock; about half of it was completed to end-July. Notably, capital stock has been further reduced through a cancellation of 26.9mn shares.

Valuation wise, the stock appears cheap with a P/E ((TTM)) of 9.73 versus peers and consumer staples sector. Historically, the ratio is at its lowest since the group returned to profitability at the beginning of 2020.

{kind=link}

Conclusion

Carrefour seems confident. It has reaffirmed its full-year outlook in principal items like recurring operating income and net free cash flow. Shareholders must be pleased with the group promising to continue returning value in successively higher increments. And yet the market is not fully convinced.

Risks in key locations are weighing the company down. Inflation may take time to subside in France compared to the rest of Europe. In Brazil, even with the economy improving, Carrefour has much left to do with Grupo BIG.

Perhaps it is the memory of a similar episode in Carrefour's past - its long-drawn-out fumbling with Promodès at the dawn of the century - that makes investors nervous. If Carrefour Brasil takes longer than expected to get back to form, it will have a major impact on the group's progress to goals to 2026.

Although the incumbent CEO and his team have been a breath of fresh air, it remains to be seen whether their digital offensive and remaking of Carrefour's legacy big stores bring the desired results. Because for investors, they couldn't come soon enough.

For further details see:

Carrefour Has Its Work Cut Out