CRRFY - Carrefour: Revisiting My Positive Thesis After A 20% Drop

Summary

- Carrefour has, overall, underperformed the market slightly since my last article on the company, which is one of the largest public businesses in all of France.

- While there are challenges ahead, I remain positive on the retailer, and a strong investor in conservative businesses that address fundamental needs. Carrefour is that.

- Here is my updated overall thesis on Carrefour, and why I continue to be "LONG" in this business.

Dear readers/followers,

Remember my article on Carrefour (CRRFY)? This is a stellar company, at least fundamentally, in the European hypermarket segment, and I wrote about it a few months past, going "BULLISH" and buying shares. Since the time, the company has slightly underperformed the broader S&P 500 index. While there are certainly risks to be considered to the stock, the fact is that at its heart, Carrefour is one of the largest businesses on earth, and it's not going anywhere.

And it's improving its fundamentals.

Here is what's happening and what's happened to Carrefour.

Carrefour - Revisiting The business

Now, to those of you initiated to the French company called Carrefour, the company is a supermarket chain. Carrefour sells, in its 12,000+ stores what supermarkets typically sell in stores. It drew its early inspiration from the American hypermarket/supermarket model and brought it to France in 1958. It was the first in Europe to do so, and the first also in producing its own store-brand products, which were packaged just as unexciting as these products tend to be packaged.

Carrefour IR (Carrefour IR)

Fast-forward to 2022, and the company is one Europe's largest retailers, and only behind Walmart in terms of pure size. I went through in my original article how fundamentals are "essentially" solid, with an investment-grade credit rating and a covered dividend of 3-4% at today's prices, and a debt that for the company sector is under control, at below 2.5x to EBITDA.

Like all companies in the segment, Carrefour is adapting to a changing world. Omni-channel retailing is growing in importance, and COVID-19 has shown the importance of things like Click & Collect services, which Carrefour has adopted.

The biggest markets by far for Carrefour are France, Spain, and Brazil. France alone represents 40%+ of the group profit. This means that France is more important than virtually every other market.

While the company has 35 market exposures including Spain, Asian Markets, the Middle East, non-France EU markets including Belgium, Italy, and Eastern Europe as well as African markets, it remains highly dependent on its legacy markets.

Carrefour also isn't just Carrefour - it has plenty of brands under its umbrella, named for the size of the store and what target demographic/customer they're looking at. This creates an interesting situation where a massive-size Carrefour Hypermarket is owned by the same company that also owns your typical picturesque French corner store with hand-written signs for fresh cheese.

Both of them, and everything in between, is Carrefour.

I highlighted the very mixed bag that we've seen in terms of results for the past 10 years. Legacy allowed it to expand internationally, but these expansions have not necessarily been a net positive. Because of extremely low sales contribution from these new segments, the investments and international advantages were quickly overshadowed by slowing growth, margins, and greater omnichannel-based competition in France.

Competitors that focused on legacy-market margins, market share, and efficiencies have generally done better than companies that focused on expanding to x new markets. The company's 2004-2010 focus in conjunction with the financial crisis meant that other discounters had a much freer range of legacy markets than you might have seen in the US. Carrefour was in fact very late in starting to push price/mix actions - not in food, but in other products.

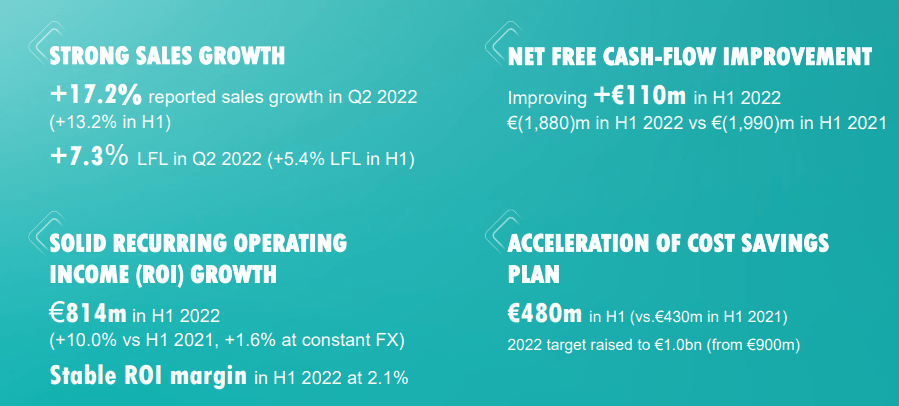

But, the company is in a bout of recovery - and that recovery has been ongoing since I bought my position in the company. The latest results are 2Q22/3Q22, and for this period, we see strong top-line growth for Carrefour.

{kind=link}

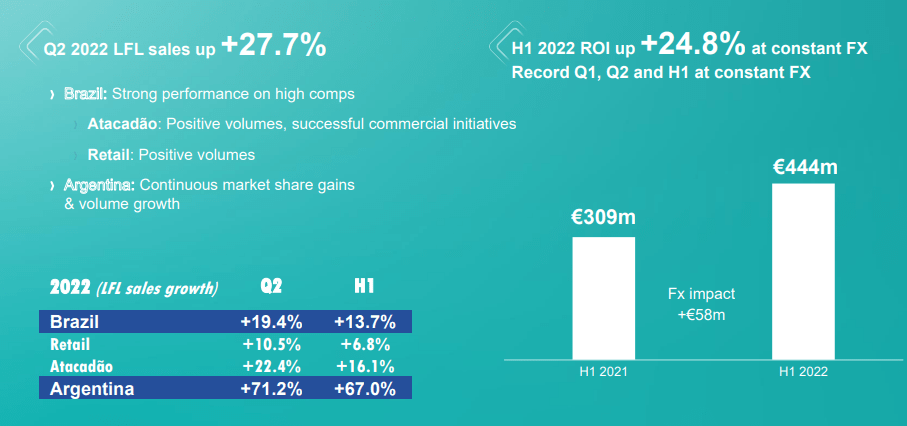

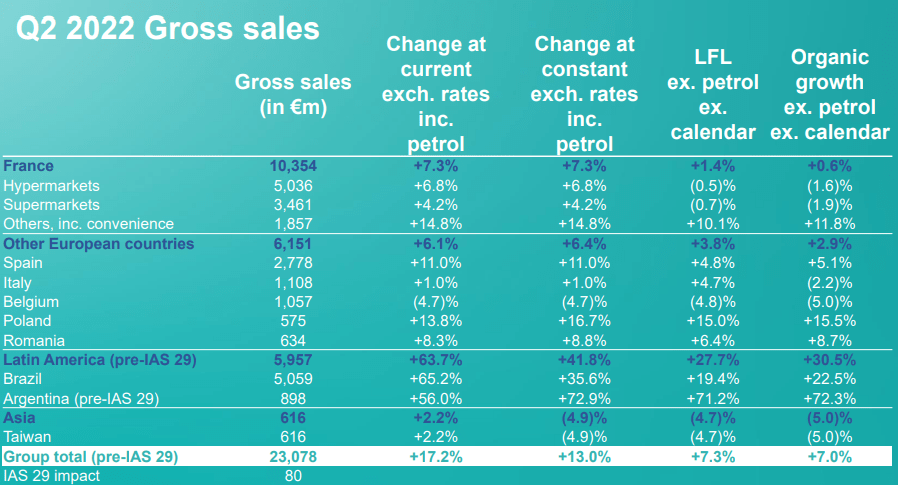

That is 2Q22. The company pushed very impressive LFL sales growth, with additional sales income from petrol, expansion effects, calendar effects, and positive FX. ROI is also improving, and for legacy, Carrefour keeps growing. For Europe as a whole in fact, excluding Belgium, things are extremely good. Belgium is down 6% for 1H22, but the rest is up about the same or in that range. The company's expansion markets are also showing growth, with superb near-20% top-line growth out of Brazil and over 71% in Argentina.

{kind=link}

So, growth upon growth even in expansion geographies. The company did have some issues in COVID-19 geographies - and Carrefour is "done" with Taiwan, and is selling its operations to Uni-Presented at an EV of €2B.

Top-line was up double digits. Bottom-line EPS was also up in 1H22, but only around 3.1%. Expenses were naturally up (interest rates) as well, but overall it was a good half-year with good earnings. Net debt was up due to the inclusion of a Brazilian M&A and some share buybacks - which is a good strategy when the company is bottom-feeding in terms of valuation.

Overall, both 1H22 and 3Q22 confirm the stance that Carrefour is an efficient and well-adjusted cash-minting machine. It has strong commercial momentum, a good market position, excellent cost discipline, and is likely to increase efficiency even further going forward. The company is expecting net free cash flow of over €1B now, with a cost-saving target increased to €1B as well for the higher end. Gross sales development especially is a joy to behold.

{kind=link}

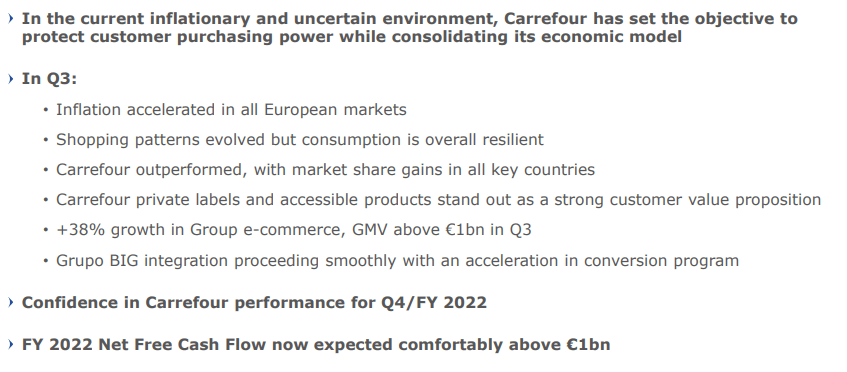

3Q22 results confirm the upside we see in 1H22. Sales increased by 19% or 11% on an LFL basis, with continued market gains in all geographies. Results are also ahead in an inflationary context, and the company outperformed the market as a whole in legacy markets like France. The company's e-commerce is growing strong, with a near-40% YoY growth in 3Q22. Basically, insofar as 3Q22 goes, it confirmed the upside and the FY22 targets set by the company in 1H22.

{kind=link}

It remains a fundamentally sound retailer/discounter in both food and department store sales with market-leading legacy positions in several core markets. Its focus, due to the sales exposure, needs to be on France, but the secondary markets of Spain, Brazil, and China also contribute. It has a decent yield in terms of dividends, but a bit of a problematic position in e-commerce, where due to management, it essentially missed 5-8 years of growth when it could have been the first mover in many of its important markets. There is no crying over spilled milk, and we do need to be forward-looking, but keep in mind that this company hasn't been the first mover all that often.

Carrefour changed in early 2020-2021, after several quarters and 2020 of operational improvement and restoration of a proper dividend.

Following a sharp drop, Carrefour became an M&A target. The first out to offer to buy the company was Canadian-based operator Alimentation Couche-Tard (ANCUF), at a 30% share price premium which at the time was "okay", as the company to my mind was trading below fair value. (At least to anyone not giving credence to DCF analysis or book value premiums). But French companies do not make easy takeover targets, due to the national pride in businesses. It's not actually that rare for the government to step in here and stop them on the basis of "national safety".

Let's look at the current valuation for this great business.

Carrefour Valuation

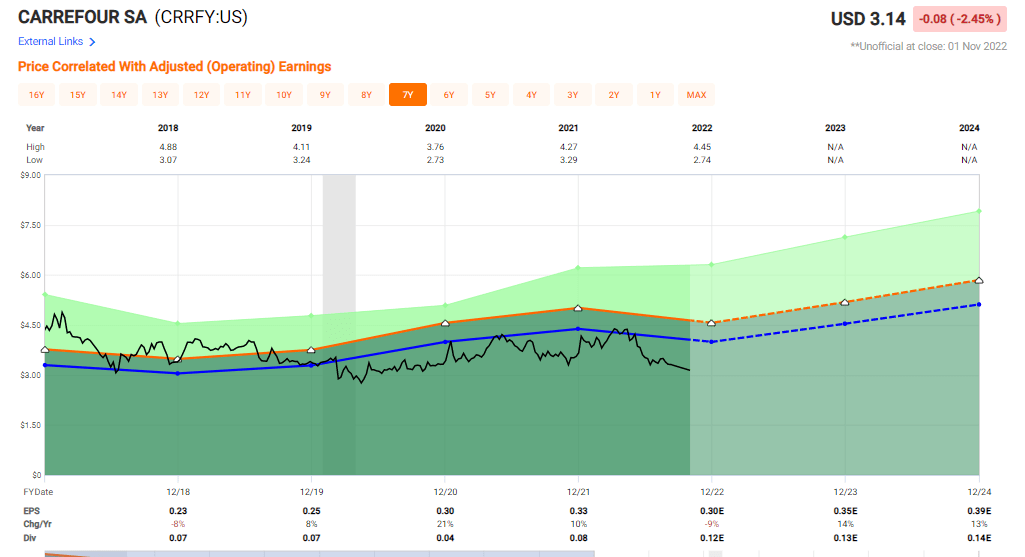

Valuation for Carrefour remains very appealing. In light of the 2019-2021 operational improvements that show no signs of stopping in 2022 despite an extremely problematic macro, I view these latest years as a turning point for a downward trajectory of over a decade, disappointing shareholders with poor returns as well as dividends.

The company has finally normalized the dividend. The expected dividend for 2021-2022, payable in 2022-2023 is ~€0.57/share, indicating a forward yield of 3.5%. (Source: S&P Global)

This is impressive for a grocer/supermarket like Carrefour. It becomes clear, when looking at company estimates, that the market believes the bad years to be over, followed by strong, stable growth or just stability for the next few years. There are far worse places to be invested in (take any of the hundred tech "growth" businesses that are down 70% YTD and more).

Carrefour Forecast (S&P Global/TIKR)

So, with that picture the one that we're looking at here, this makes the current valuation for the company somewhat illogical. European peers include Ahold Delhaize (ADRNY), Sainsbury (JSAIY), Casino Guichard-Perrachon (CGUIF), Axfood (AXFOY), Colruyt (CUYTY) and Tesco (TSCDY). International peers include Walmart ( WMT ). A peer average for these companies comes in at high P/Es of above 14-15X, though a lot of that is coming from US averages, with locals like Casino and Colruyt trading below 7X P/E at this time. Carrefour, meanwhile, has dropped to a normalized P/E of 9.7x, which is low even for its mean of closer to 11x.

Current analyst targets would suggest that there is at least a ~25% upside to the company - and that is considering an average target of just north of €20/share for the native, with 11 out of 16 following analysts considering the company a "BUY" at this time.

I continue to give Carrefour DCF estimates of €22 on the very low side and around €27.5 on the high side. Even with the most conservative cash flow growth rates, with some of the highest-scenario CapEx/sales ratios and pressured variables, you're still ending up at an indicative DCF that's potentially higher than what Auchan offered a year back now.

So - on a P/E, DCF, EV/EBITDA, and book value basis, Carrefour is trading at a discount to most of its peers. That's what forms my continued fundamental upside view for this company here.

Even when we view the ADR, we can see that the company's valuation trend is going in the exact trajectory we want for a good investment. Estimates are up, valuation is down.

{kind=link}

It is therefore easy for me to point out and say, that this company has an annualized upside on a 12-13x P/E normalization in 2024E, of no less than 30% per year, or almost 80% until the year-end of 2024E.

That is the thesis I am investing in, from a high level, and that is why I consider Carrefour to be a solid "BUY" at this particular time.

My PT for the company is no less than €22 - higher than most analysts here. But I refuse to go lower without a good reason, and I currently see no good reason to do so when the company continues to outperform.

Thesis

My thesis for Carrefour is as follows:

- Carrefour is one of the stronger and the largest hypermarket/supermarket chain in all of Europe. The company has gone from performing poorly since the financial crisis, to performing quite well in 2022 and is expected to continue to do so moving forward.

- At a reasonable or cheap valuation, Carrefour deserves a place on a person's "BUY" list.

- At this valuation, I believe the time is ripe to do just that - and I'm adding more Carrefour.

- My PT is €22/share, and this one is a "BUY".

Remember, I'm all about:

Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

For further details see:

Carrefour: Revisiting My Positive Thesis After A 20% Drop