CRRFY - Carrefour SA Q3: Sales Growth Remains Resilient But Further Earnings Growth Needed

2023-11-03 14:42:44 ET

Summary

- Carrefour SA has shown resiliency in sales growth despite price deflation, but earnings need to rise to justify further upside.

- Like-for-like sales were up 9% in the most recent quarter, driven by food sales and hypermarkets.

- Price deflation and a slowdown in Brazil pose risks, but there is cautious optimism for strong sales growth in Latin America.

Investment Thesis: I take the view that Carrefour SA has shown resiliency in sales growth given price deflation, but earnings need to rise to justify further upside.

In a previous article back in September, I made the argument that Carrefour SA ( CRRFY ) has the potential for long-term upside, but a slowdown in Brazilian growth as well as price deflation are potential risk factors in the short to medium-term.

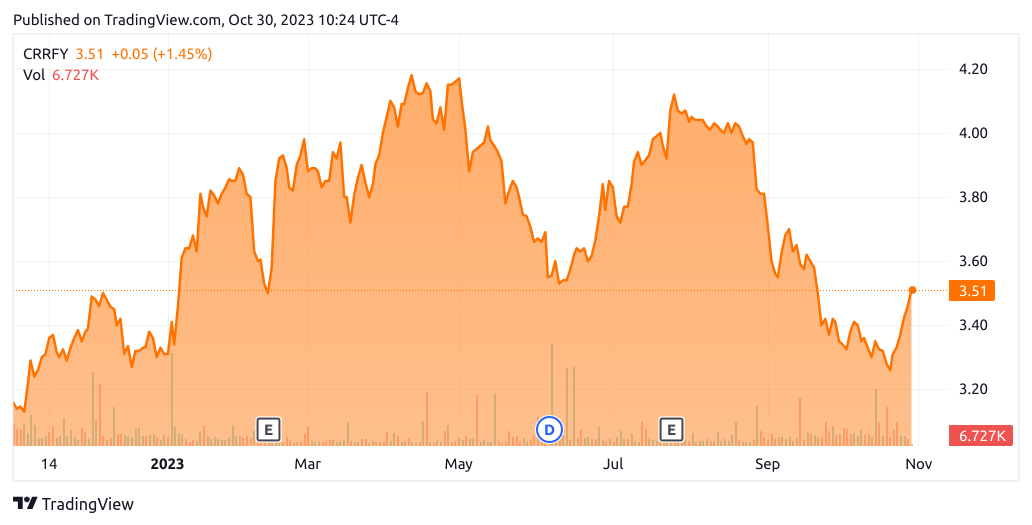

Since then, the stock has descended slightly to a price of $3.51 at the time of writing:

{kind=link}

The purpose of this article is to assess whether Carrefour SA has the ability to see a rebound in growth from here taking recent performance into consideration.

Performance

When looking at the most recent Q3 2023 earnings results (released on October 25, 2023) for Carrefour SA, we can see that like-for-like sales were up by 9%. At 4.3%, growth across the French market slowed down from 7.3% for Q2 2023 . Growth in this quarter was driven mainly by food sales, and hypermarkets showed the best performance among all segments.

Carrefour SA Press Release: Third-quarter 2023 sales

{kind=link}

Additionally, when we look at like-for-like sales for the most recent quarter - we can see that it came in at 9% for Q3 2023 - down from that of 11.3% for Q3 2022.

Figures sourced from historical Carrefour SA quarterly earnings reports. Heatmap generated by author using Python's seaborn library.

I had previously pointed out the risk that Carrefour could see pressure on like-for-like sales going forward. Specifically, with inflation starting to level off and like-for-like sales growth having been driven largely by price rather than volume, price deflation could lead to a situation where volume drops as customers start to delay purchases in anticipation of further price decreases.

With that being said, while Carrefour acknowledges that while inflation has been slowing in Q3 - commercial momentum remains solid with a strong increase in sales of private labels which exceeded 35% of food sales in addition to growth in e-commerce GMV, up by 31% in Q3 2023.

While food deflation was more pronounced in Brazil - which saw a slowdown of over four points as compared to Q2 2023, Atacadão continued to show strong performance given a strong ramp-up of stores converted from Grupo BIG, with a continued synergy target of at least R$2.0bn by 2025.

My Perspective

As regards my take on the above results and the implications for the growth trajectory of the stock going forward, the fact that Carrefour is continuing to show strong growth in like-for-like sales despite signs of price inflation is encouraging - in spite of a slight slowdown from that of Q3 2022.

Going forward, I take the view that if Carrefour can continue to demonstrate sales growth in spite of deflationary pressures, then the stock could stand to see further upside from here. In particular, I take the view that the Brazilian market is set to remain resilient - given that performance has been strong in spite of food deflation, with strong performance from the Atacadão brand. In this regard, I continue to take the view that we will see strong sales growth in Brazil going forward - which in turn would be expected to lift sales growth across the Latin American region more generally.

As for the French market, I also take the view that e-commerce is set to continue seeing significant growth - with e-commerce GMV having already seen 16% growth in Q3 2023. In spite of sales growth having largely been driven by price up until now, I take the view that continued growth in e-commerce can be expected to result in an overall boost to volume growth going forward.

I had previously pointed out that with the P/E ratio trailing near a 10-year low as well as earnings per share remaining near a 10-year-high, further earnings growth would have the potential to push the stock higher over the longer-term.

ycharts.com

With that being said, we can see that earnings growth has been plateauing of late, in spite of continued growth in like-for-like sales. Given that the P/E ratio has largely been weakening over the past two years - I take the view that a ratio of 10x to 15x would be more reasonable given the range seen in 2021 and 2022.

With earnings per share of $0.356, I estimate that fair value for the stock within this range would like between $3.50 (10 * 0.356) and $5.34 (15 * 0.356) . Given a current price of $3.51, I take the view that the stock is trading within its fair value range - but the stock could see upside past the $5 mark if we see continued growth in sales and earnings.

From this standpoint, I continue to maintain a cautious view on Carrefour SA in the short to medium-term. While continued growth in LFL sales is no doubt encouraging, this needs to ultimately translate into earnings growth to justify further upside in the stock.

Risks

In terms of the potential risks to Carrefour SA at this time, while growth in like-for-like sales has continued in spite of price deflation - the same still remains a risk to the company.

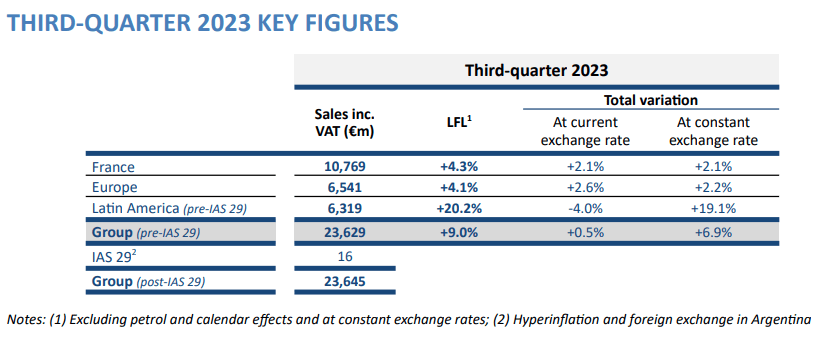

In particular, we have seen that food deflation in Brazil has been more acute, with like-for-like sales down by 3.7% in Q3 2023. Moreover, we have seen that growth across the Brazilian market has been quite important for overall sales growth in Latin America. When comparing to Europe (not including France) - Latin America accounted for almost the same percentage of overall sales and like-for-like sales growth was up by 20.2%, with growth of 19.1% at constant exchange rates.

Should we see a situation where a slowdown in Brazil affects the overall Latin American market, then this could be concerning for Carrefour. With that being said, Brazil has been showing signs of a slowing in food price decreases - with the country's overall inflation rate accelerating.

In this regard, I am cautiously optimistic that Carrefour can continue to see strong sales growth across the Latin American market more broadly.

Conclusion

To conclude, Carrefour SA has seen sales growth remain resilient in spite of price deflation. With that being said, I continue to take the view that this needs to translate into solid earnings growth to justify upside going forward. In this regard, I continue to rate Carrefour SA as a hold at this time.

For further details see:

Carrefour SA Q3: Sales Growth Remains Resilient, But Further Earnings Growth Needed