CRRFY - Carrefour: Still Value There In 2023

Summary

- European stocks have outperformed - and that's the reason I'm in positive territory at this time, and only moving upward.

- My position in Carrefour was never huge - but it still did around 16% better than the market, due to the massive undervaluation we saw about 3-4 months back.

- Carrefour is a market leader in some European countries - and despite current challenges, I don't consider the company "overvalued" here.

Dear Readers/followers,

Carrefour ( CRRFY ) isn't exactly the most popular company I cover or follow. I consider it underappreciated, given how popular consumer staples stocks are in other parts of the world like North America. Carrefour is pretty stellar if viewed from a European perspective.

Carrefour Article (Seeking Alpha)

What's even better, the company has been improving its results and fundamentals for several years and is in a great position to outperform the market for 2023 and forward. Now, the valuation is up 20% since my last article - so is there still value in investing here?

That's what we'll look at in this article, and I'll show you my 2023 thesis for the company.

Carrefour - The company has done well

Carrefour is essentially 12,000+ investment-graded stores in Europe and outside of Europe. The fact that Walmart (WMT) is so appreciated as an investment but Carrefour is not, especially with recent improvements, only strengthens the case for Carrefour here. The company is BBB rated, and its latest results give some justification for my positivity here.

Now, there's no doubt that €17.5 is less attractive than €14-€15 - but is it enough to take away the fundamental upside for the company?

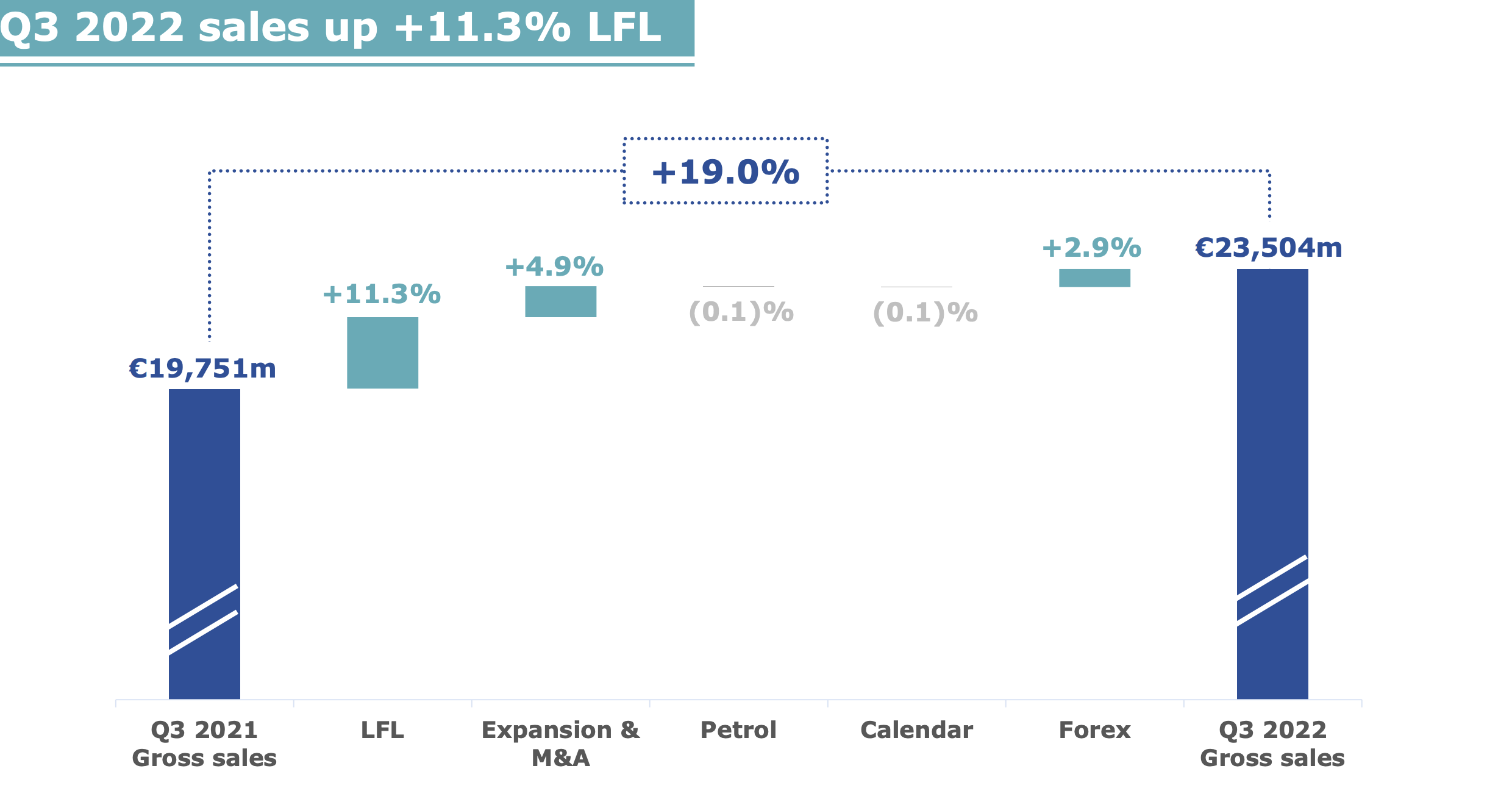

3Q22 results is the latest set of results that we do have, and this mostly confirms the market challenges that are currently impacting the world. I'm talking about:

- Inflation

- Supply Chain Challenges

- Geopolitical volatility

However, the company saw good performance based on:

- Shopping patterns changed, but sales remained resilient, growing double digits at 11.3% YoY.

- Market share gains in all geographies

- Private-label and company-label sales are up and make the case for value that most consumers are looking for here.

- 38% YoY growth in company E-Commerce.

- Smooth integration of recent M&A's.

So, all in all, Carrefour is firing on all cylinders despite some challenges.

{kind=link}

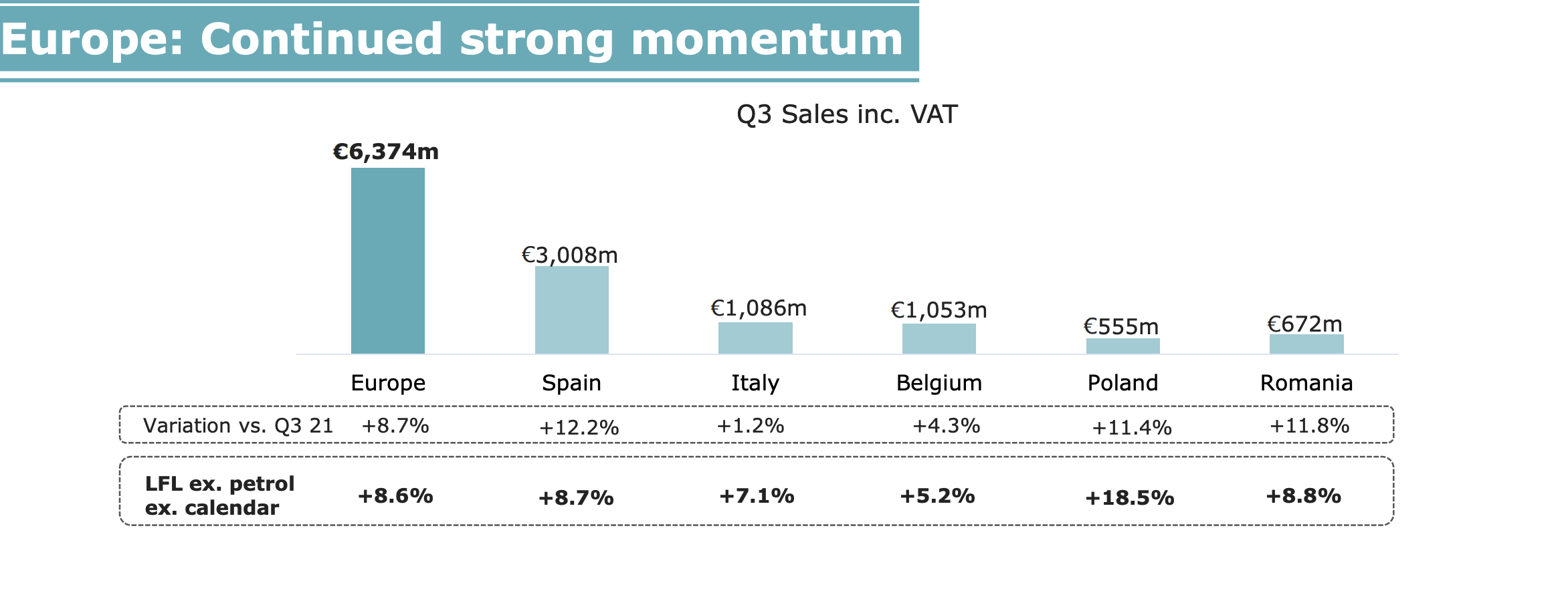

Even taking away FX and expansion, the company is doing well on the top line. In France alone, the company saw growth in all segments - Hyper, Supermarkets, and other formats, with other formats even without petrol up 10.8% YoY. on a Europe-wide basis, the company's sales are also showing strong trends.

{kind=link}

The company's growth market is LATAM though, and Brazil was up 41.4%, and Argentina was up 91.3% (though from a very low level). Carrefour is growing in all markets and across all segments. Carrefour partnered with renewable energy companies to reduce its climate footprint and also does have some other plans to increase its ESG appeal. My view on this is similar to the recently-published stance from Home Depot ( HD ) execs/co-founders, that companies should focus on strategies that impact the bottom line, and stay away from strategies that do not.

Omni-Channel retailing, while changing and going through major developments, is not going anywhere, and Carrefour is a world leader in this segment, because Walmart does not really operate outside of North America, while Carrefour has operations not only in France and other European nations, but is moving into growth markets.

The company has given us some strategic plans for 2026, that we can follow and use to track company performance, knowing when it's potentially time to sell off Carrefour, and when its time to buy the company. The company expects that it will become more of a private-label company, with the company's private labels growing to represent 40% of Carrefour sales in less than 3.5 years. The company also means to push CapEx with expansion into Brazil, focusing on launching and managing more than 470 Atacadao stores, up 200 from now, and launching the brand Atacadao in France as well.

The company, similar to businesses like Lidl, is moving heavier into the agri sector, with pushes into both sustainable agriculture, but expanding operations and offerings here.

The company is also getting serious about its climate goals - for the 100 suppliers that are on the top of the company's volume list, they have given the option to work with the 1.5 degree (an ESG goal) trajectory at 2026 at the latest - otherwise Carrefour will delist them from being able to supply the company with product.

Aside from that, we're going to see cost savings from ongoing reorganization, saving upwards of €4B until then, as well as some ventures I'm less than thrilled about.

Carrefour is moving into retail media, partnering with Publicis (PUBGY) to drive a JV that aims to bring Europe and LATAM to the same scale and connectivity in terms of Retail Media.

By combining Publicis’ advanced technologies, ‘CitrusAd powered by Epsilon’, with Carrefour Links’ retail media knowledge and expertise, this new venture will build a comprehensive media player that addresses the entire Retail Media value chain. It will span technology for inventory creation and data sharing for merchants to the full commercialization of media and data solutions for advertisers, backed directly by merchant transactions, across Continental Europe, Brazil and Argentina.

This joint venture has the ambition to rally multiple new retailers, to build an unparalleled network of inventories and accelerate the development of retail media in Europe and Latin America. Its ultimate goal is for any company with direct customer touchpoints and first party data to join the platform, in order to monetize their assets and partner with advertisers to build more efficient marketing strategies, and boost their business.

( Source : Carrefour/Publicis)

To be clear, I think this is a bad idea, for the company to leave its core markets in such a way, and I will be impairing the company's valuation accordingly for this push. I won't argue that there is a booming retail media market in both the EU and LATAM, but I don't think Carrefour should be part of trying to address it, especially when it contains the creation of a "media player" as described. There is a reason why these LATAM markets are relatively fragmented and why there hasn't been much success in addressing this. Carrefour's own retail media network, Carrefour Links, is doing relatively well in Europe because it already serves 300 brand partners, but I'd rather have seen the company try to slowly push this to market, as opposed to partnering and trying to do a push like this. Operating margins in these industries are already razor-thin - anything above 2.5% is great, and Carrefour is at 3% as of LTM. This might hamper that, and even a 10 bps impact would leave a bad taste in my mouth here.

So - moving to company valuation.

Carrefour Valuation - less attractive, the upside is still there, but I'm impairing the company.

My previous PT for Carrefour was at around €22/share, which was higher than overall market averages. I usually don't change PTs in the face of positive results (not downward at least), but given the company's ESG pushes and media pushes, I feel that the fair thing to do here is discount the company to make sure that potential negative results or failures in these respects do not harm investor returns and fair values.

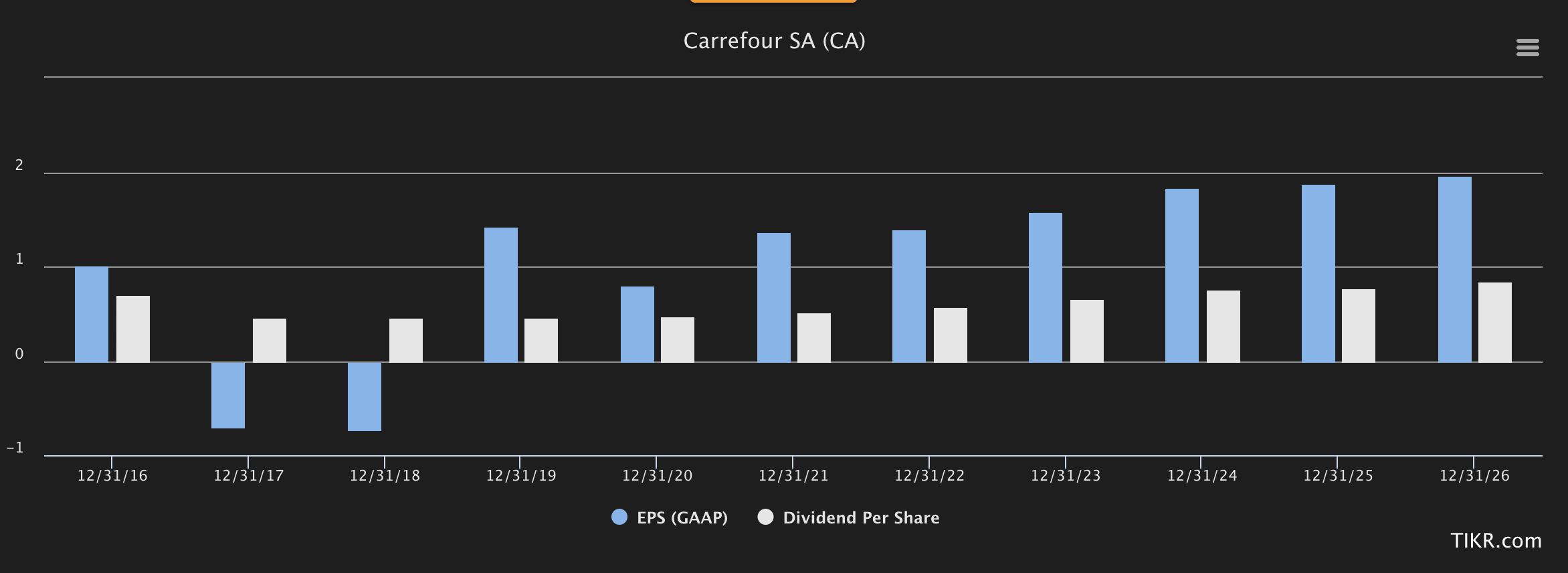

The company's valuation was very appealing, and the overall trajectory of earnings, on a forecasted basis, is actually still intact. With dividend normalization now done, and the yield still above 3% normalized, this is a better investment than I consider Walmart to be.

It becomes clear, when looking at company estimates, that the market believes the bad years to be over, followed by strong, stable growth or just stability for the next few years. There are far worse places to be invested in (take any of the hundred tech "growth" businesses that are down 70% YTD and more).

{kind=link}

Overall, Carrefour has great forecasts, and despite some of the impairments I'm going to be doing, it still shouldn't be trading as cheap as it currently is. European peers include Ahold Delhaize ( OTCQX:ADRNY ), Sainsbury ( OTCQX:JSAIY ), Casino Guichard-Perrachon ( OTCPK:CGUIF ), Axfood ( OTCPK:AXFOY ), Colruyt ( OTCPK:CUYTY ) and Tesco ( OTCPK:TSCDY ). International peers include Walmart. A peer average for these companies comes in at high P/Es of above 14-15X, though a lot of that is coming from US averages, with locals like Casino and Colruyt usually below 8x. I own several of these businesses in my core portfolio, and Carrefour, aside from Ahold Delhaize, is the biggest position here.

Analysts have already given some impairments to the company's targets. From my latest analyst average of €20/share, it's now down to around €19.5. I don't view that impairment as enough for the risks the company is taking in terms of its ESG and new Media pushes. While I hope they work out, I'm not going to allow for exuberance in any of the companies I follow or cover here on Seeking Alpha.

The current range of valuation from analysts is 14 analysts - of which 7 are at a "BUY", and only 1 at "SELL" - between €16.5 and €23/share. A fairly tight range, all things considered. I would go ahead to impair my previous target of around €22 to around €20.5 - note that I say that the impairment of half a euro wasn't enough, not that I view that analysts are being positive enough here. I still believe Carrefour can rise at least 15% from today's native of €17.35 - but I'm more negative on the impairment and analyst changes than others here, which is why I'm lowering my target more.

It's one of the dangers of a big business doing well. When there is stability and when earnings continue to flow in, the company starts asking "Well, what are we going to do with this massive pile of cash that we have on our books?"

And then they start making mistakes.

Like Fortum buying (and later shelling away) Uniper. Like Scandinavian Telco's suddenly deciding that geopolitically unstable geographies would make for great growth markets, despite the risks. Like telcos across the world moving into content creation of all things, which might sound ancillary, but in my mind, is anything but (due to the operational nature of the spending and income in these segments).

I hope we're not seeing Carrefour doing a similar mistake here. I realize that having excess cash on the sheet is in itself actually a problem, but I would reinvest in different ways, being the risk-averse sort of investor that I am.

Anyway - moving to the thesis here.

Thesis

- Carrefour is one of the stronger and the largest hypermarket/supermarket chain in all of Europe. The company has gone from performing poorly since the financial crisis to performing quite well in 2022 and is expected to continue to do so moving forward into 2023 and beyond.

- At a reasonable or cheap valuation, Carrefour deserves a place on a person's "BUY" list. The company is showing some worrying signals with regard to the use of cash and starting of JVs/media, but for now, I'm just impairing the company's target and moving it lower, despite good results.

- My PT is €20.5/share, and this one is a "BUY".

Remember, I'm all about:

Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

I would still call Carrefour cheap, but if it moves above €18.5, that's no longer the case. Still, it's a "BUY" here.

For further details see:

Carrefour: Still Value There In 2023