CRRFY - Carrefour: Strong Sales Growth And Attractive P/E Ratio

Summary

- Carrefour has seen impressive sales growth in the fourth quarter.

- Growth in e-commerce sales was particularly strong.

- I take a bullish view on Carrefour stock.

Investment Thesis: I take a bullish view on Carrefour SA owing to strong sales growth and an attractive P/E ratio.

In a previous article back in November, I made the argument that while Carrefour SA ( CRRFY ) has seen encouraging sales growth - an accompanying rise in the cost of sales could mean that growth in the short-term remains modest.

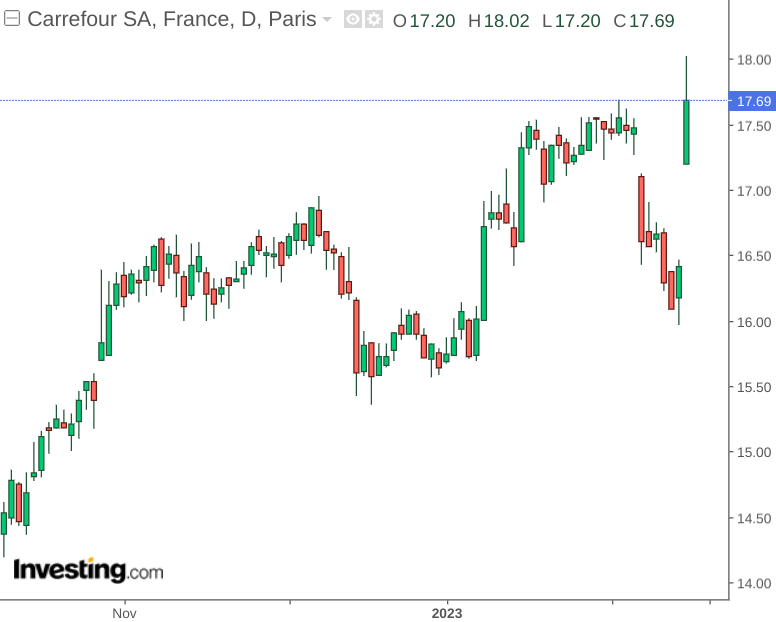

However, growth has in fact been particularly impressive, with the stock up by over 17% since my last article:

{kind=link}

The purpose of this article is to investigate the main drivers behind recent growth, and whether we can expect the stock to continue appreciating from here.

Performance

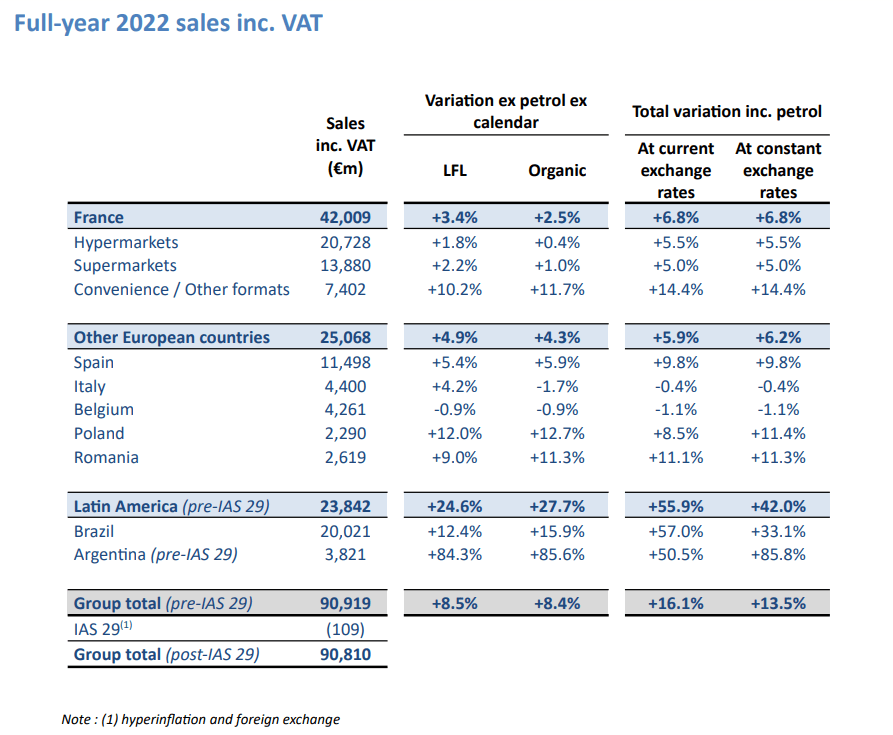

When looking at full-year 2022 results for Carrefour, we can see that overall sales growth has up by 16.1% at current exchange rates, and 8.5% on a like-for-like basis.

Carrefour SA: Q4 2022 sales and FY 2022 results

{kind=link}

Moreover, we can see that while like-for-like sales were up by 3.4% across the French market for the year as a whole, LFL sales for Q4 in particular were up by 5.6% - which was driven by solid food sales of 7% over the period:

Carrefour SA: Q4 2022 sales and FY 2022 results

Given that we have seen Q4 sales growth across France outpace that of the year as a whole - this could be an indication that inflationary pressures are having less of an effect on sales demand and further growth in quarterly LFL sales across the region would be highly encouraging.

More broadly, e-commerce growth continued to represent a significant win for Carrefour as a whole - with 2022 recording an increase in Carrefour's GMV by 26% to €4.2 billion, which was substantially more than that of 11% 2021 - a significant driver of growth having come from a doubling of e-commerce sales in Brazil.

From a balance sheet standpoint, we can see that while the quick ratio still remains significantly below 1 - the ratio has increased to 0.60 since June. This indicates that the company's capacity to meet its current liabilities using existing liquid assets is improving, and further growth in this ratio would be encouraging:

| December 2019 |

| June 2022 |

| December 2022 |

| Current Assets |

| 18875 |

| 19586 |

| 22243 |

| Inventories |

| 5867 |

| 7227 |

| 6893 |

| Current Liabilities |

| 23061 |

| 24417 |

| 25712 |

| Quick Ratio |

| 0.56 |

| 0.51 |

| 0.60 |

Source: Figures sourced from Carrefour SA Q4 2022 sales and FY 2022 results. Figures provided in € millions, except the quick ratio. Quick ratio calculated by author as current assets less inventories all over current liabilities.

At the same time, we have seen a marginal increase in the long-term borrowings to total assets ratio:

| December 2021 |

| December 2022 |

| Long-term borrowings |

| 5491 |

| 6912 |

| Total assets |

| 47668 |

| 56551 |

| Long-term borrowings to total assets ratio |

| 11.52% |

| 12.22% |

Source: Figures sourced from Carrefour SA Q4 2022 sales and FY 2022 results. Figures provided in € millions, except the long-term borrowings to total assets ratio. Ratio calculated by author.

My overall view on the above results is that Carrefour SA has continued to show strong growth in spite of inflationary pressures - with e-commerce growth continuing to remain particularly strong.

I had previously pointed out that the past three years have shown a trend of the P/E ratio falling back towards 2020 levels while earnings per share continues to grow overall.

ycharts.com

This trend appears to be continuing, so I still take the view that Carrefour has further potential upside from here, particularly taking recent sales performance into consideration.

Looking Forward

Going forward, the main risk for Carrefour at this time is if inflationary pressures or the broader macroeconomic situation becomes particularly acute and we see a slowdown in consumer demand.

However, there is little evidence to suggest that this will be the case - given the strong sales growth we saw in the latter half of 2022. Moreover, given that solid food sales was a significant driver of growth in the French market - sales of such essential goods will continue to see demand even if recessionary conditions worsen.

From this standpoint, I take the view that Carrefour can continue to see upside from here.

Conclusion

To conclude, Carrefour SA has seen resilient sales growth in spite of an inflationary environment. Given the company's recent performance, as well as an attractive P/E ratio - I take a bullish view on Carrefour SA.

For further details see:

Carrefour: Strong Sales Growth And Attractive P/E Ratio