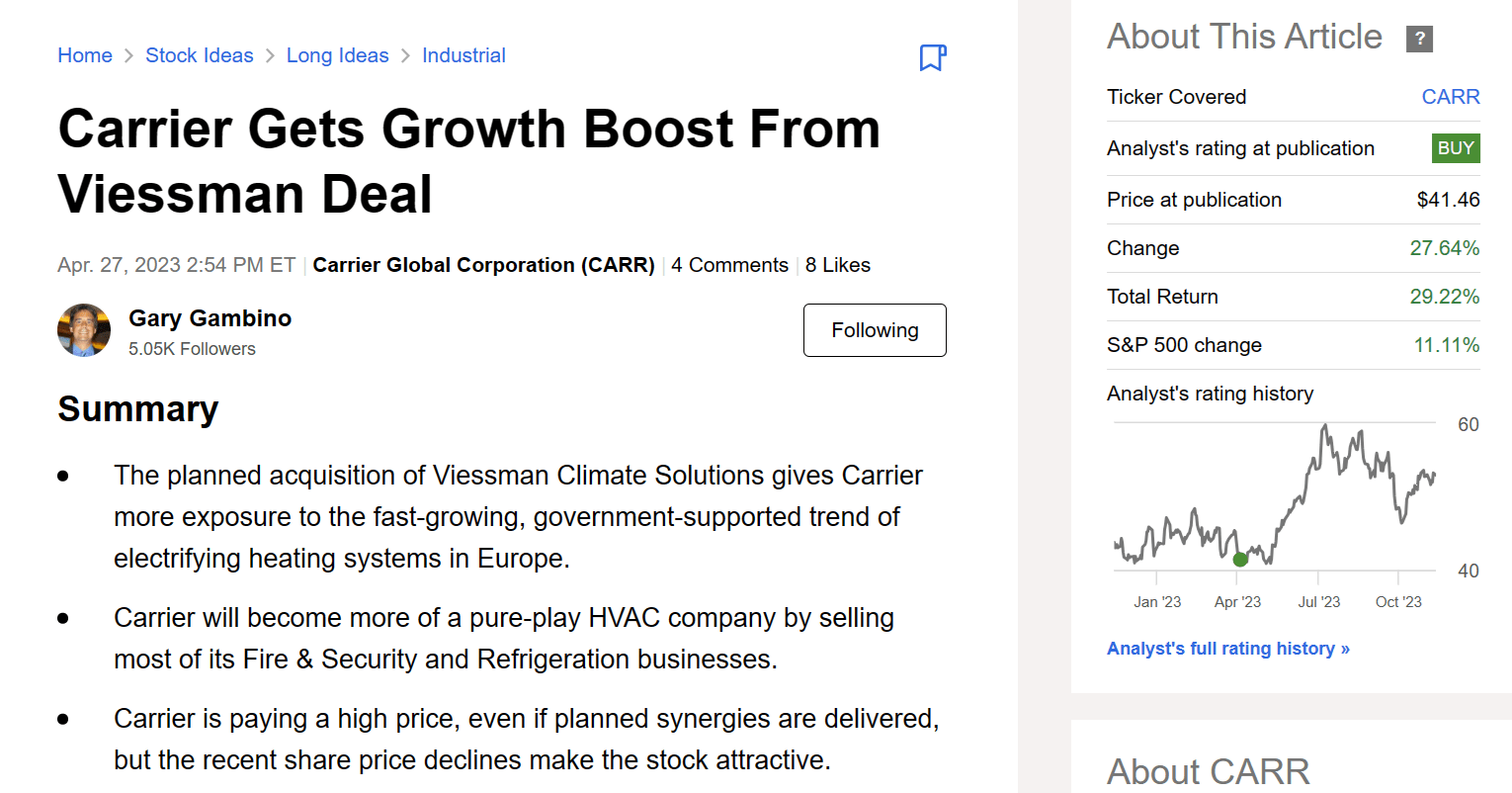

CARR - Carrier: Cool Things Happening In 2024

2023-12-05 03:09:45 ET

Summary

- Carrier Global is on track to acquire Viessmann Climate Solutions and divest its Refrigeration and Fire & Security businesses in 2024.

- The base HVAC business has some earnings volatility due to a switchover to the new refrigerant in the US required by 1/1/2025.

- CARR will grow faster as a pure-play HVAC company, so any share price declines on short-term quarterly earnings concerns would be a buying opportunity.

Big Changes Ahead

When I last reviewed Carrier Global Corp. ( CARR ) in April 2023, the company had just announced its plans to transform into a pure-play HVAC company by acquiring Viessmann Climate Solutions and divesting its Refrigeration and Fire & Security businesses. Viessmann is a well-established German manufacturer of residential HVAC products that has been shifting its focus from boilers to heat pumps in recent years. Viessmann also sells residential solar panels and battery systems for an integrated green solution. This turned out to be a good buying opportunity for Carrier stock. Although it traded near the low for the year around $41 for a month, it then rallied to a high around $60 by the end of July, a gain of over 46%. Since then, it has pulled back to around $53, which is still a 29% gain from my last Buy rating.

{kind=link}

Since then, we have had more clarity on the Viessman deal close and the exit from the Refrigeration and Fire & Safety businesses. Within the existing business, the company has been guided to higher margins in 2023 and expects a stabilization of the North American residential HVAC business driven by changing EPA regulations on refrigerants. These developments support a continued Buy rating for Carrier for the long term, although noise around quarterly results could create even better entry points.

Viessmann Deal Close

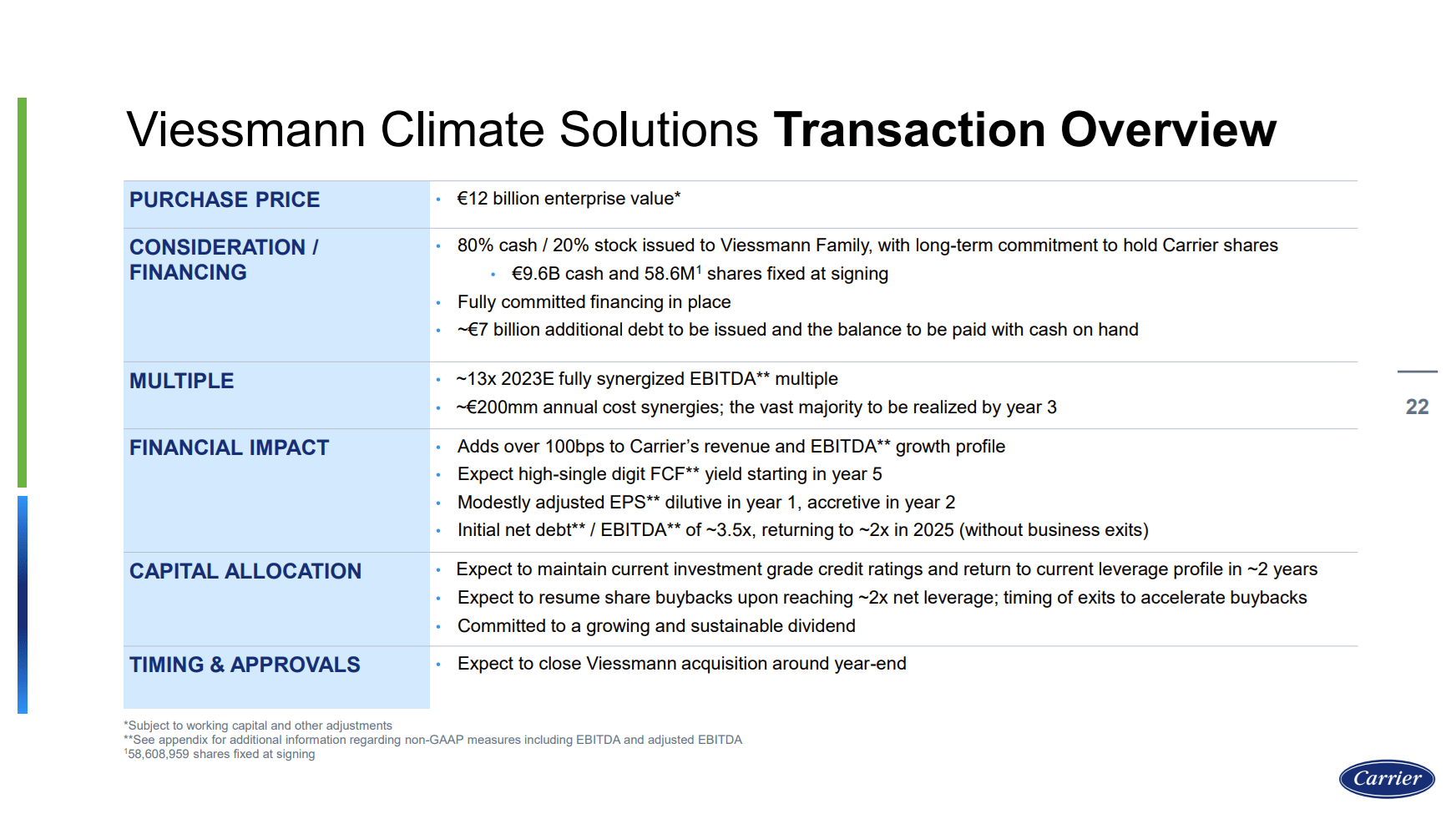

Carrier stated in their Q3 results that the Viessmann deal is on track to close in the first week of January 2024. You can refer to my earlier article or to the deal announcement presentation for more details, but Carrier is paying around €12.3 billion ($13.3 billion) for Viessman, €9.6 billion in cash plus 58.6 million shares of Carrier stock. Viessman earns about €0.7 billion per year in EBITDA. While the deal looks expensive based on this level of earnings, Carrier also expects to achieve €0.2 billion per year of cost savings based on economies of scale in materials sourcing as well as eliminating redundant manufacturing locations and management functions. Notably, these synergies do not assume any revenue enhancements such as expanding Carrier products into Viessmann's sales channels and broadening Viessmann sales beyond Europe. It is reasonable to expect some revenue synergies, which would be upside to the €0.9 billion per year benefit estimate.

On the financing side, Carrier has now issued most of the debt needed to fund the cash portion of deal. The remaining amount will come from cash on hand. While this will initially push net debt/EBITDA leverage to around 3.5, they expect leverage to get back down to 2.0 by the end of 2025 not including cash proceeds from the sales of the Refrigeration and Fire & Security businesses. Around half of the new debt recently issued matures in 2025, demonstrating Carrier's confidence in cash generation.

{kind=link}

The Viessmann deal is not without risk, however. Since the merger announcement, Germany has seen lower demand for heat pumps as both government subsidies and the cost of natural gas have come down. Additionally, there are concerns that the grid is insufficient to support all the heat pumps and EV chargers needed to meet electrification goals, and permitting delays are limiting the needed grid investments. This could lead to rationing of electricity needed for this equipment or limiting usage times to off-peak hours. Mitigating these risks is the fact that Viessmann and Carrier both continue to sell conventional gas boilers and furnaces. Viessmann also sells residential solar panels and battery systems which can help get around the grid limitations.

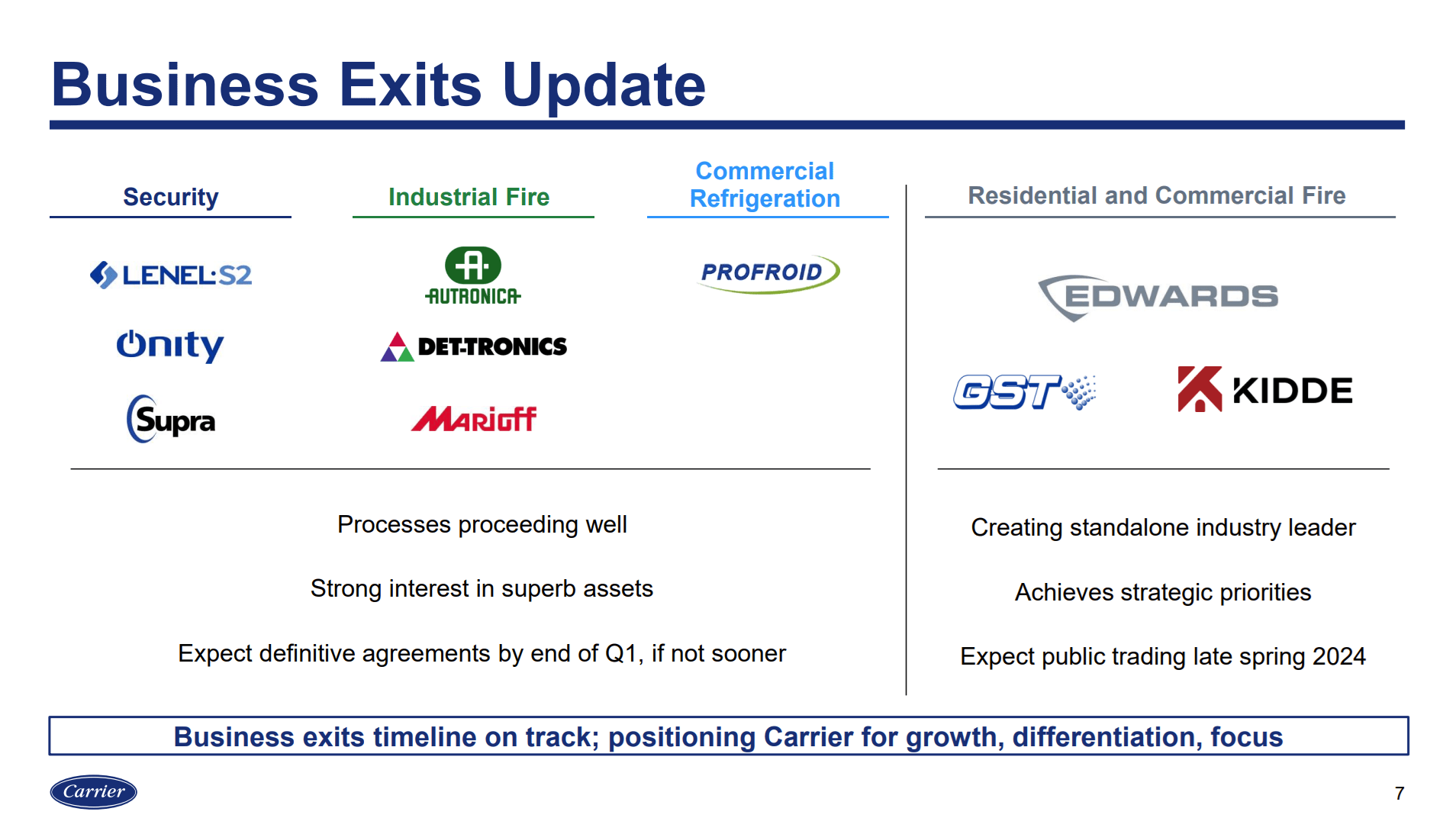

Refrigeration and Fire & Safety Sales

Carrier noted on the last earnings call as well as at a recent investor conference that there is a high level of interest in the company's refrigeration, security, and industrial fire businesses. They expect sales agreements to be completed by the end of Q1 2024 at the latest. That leaves the residential and commercial fire business. While there is still some interest from buyers, the discussion at the investor conference leaves the impression that the price may not be right. In this case, Carrier is looking at a possible spinoff or split of this business in 2Q 2024.

{kind=link}

In my last article, using the sales and EBITDA margin estimates provided by the company in the Viessmann deal announcement, and applying an EBITDA multiple of 13, I estimated the value of the divested businesses at $8.45 billion. Based on the latest information assuming a spinoff of residential and commercial fire, I would expect CARR shareholders to get spinoff shares worth about $1.65 billion, or around $1.93 per CARR share. That would leave $6.8 billion to pay down debt or buy back shares issued in the Viessmann deal. Compared to my last article, it would take Carrier closer to 3 years, rather than 2 years of free cash flow to fully return the capital issued in the Viessmann deal.

Base Business Update

The good news from the 3Q results is that Carrier increased its 2023 operating margin forecast by 0.5% in the HVAC business, to 16.5% from 16% previously. This was driven by an easing of supply chain constraints and the ability to maintain price increases as materials inflation cools. This takes the margin forecast for the overall company to the top end of the previously stated 14.0% - 14.5% range. The resulting EPS forecast is up $0.10 at the midpoint to $2.70 and the company expects to exceed its free cash flow target of $1.9 billion. Carrier also stated that Viessmann, while not yet part of the company, is still on track to hit the €4 billion sales and €0.7 EBITDA targets stated at the time of the deal announcement.

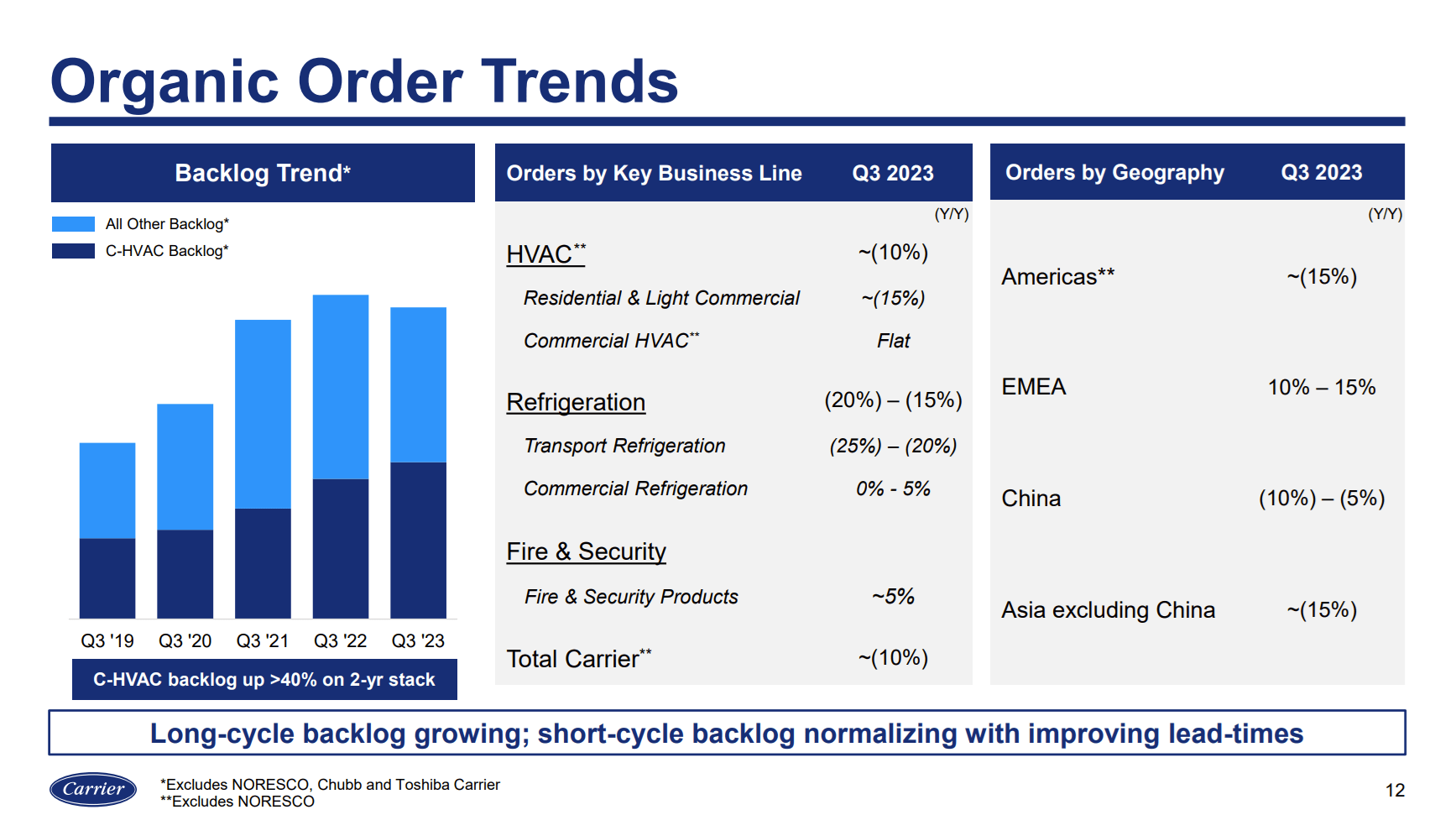

The not so good news is the big drop-off in new orders compared to my last article. In Q1, orders were up 0%-5% for the company overall, while as of 3Q, they are about 10% lower. The big drag is in residential and light commercial HVAC, where orders are now down 15%. Transport refrigeration orders have also slowed considerably, while commercial refrigeration and fire & security orders have strengthened - good timing for selling these businesses. Geographically, orders slowed in North America and Asia but picked up in the Europe, Middle East, and Africa region - also good timing for the European-focused Viessmann acquisition.

{kind=link}

While the drop in residential HVAC orders may look concerning, there are a couple of special circumstances to note. First, the company is up against strong comps from last year and is now seeing some effects from a slower housing market due to higher interest rates. Second is the upcoming phaseout of hydrofluorocarbon (HFC) refrigerants in the US effective 1/1/2025. The most common refrigerant currently used in HVAC systems is R-410A, which for chemistry enthusiasts is a mixture of two HFCs: difluoromethane (CH2F2, or R-32) and pentafluoroethane (CHF2CF3, or R-125). New HVAC systems installed after 1/1/2025 must use non-HFC refrigerants, the most common of which are in a class known as A2L such as R-454B. While there was originally some ambiguity about whether the 1/1/2025 date referred to the manufacturing or installation date, the latest interpretation from the EPA appears to require the new refrigerant in all new installs starting on 1/1/2025. That means that distributors will have to start stocking up on the new units in 2024 ahead of the deadline. That also may help explain the order slowdown as distributors need to destock the old R-410A units in 2024.

While this transition creates some volatility in orders, it should be a net positive for Carrier. The discussion on the last earnings call suggests flattish unit sales in 2024, however Carrier expects price increases of 15% - 20% in the next two years. This includes typical twice-yearly price increases as well as passing along the higher cost associated with the new refrigerant. As one of the larger companies in the industry, Carrier expects to have an easier time complying with the transition than smaller competitors. As mentioned by the CEO on the earnings call:

So net-net, EPA ruling more 454-B sooner is overall good, a bit more uncertainty as we navigate this with our partners, but I don't think there's going to be a company more prepared to deal and address with the switchover.

With the acquisition and sales of businesses, there are a lot of moving parts to sort through to estimate overall forward EPS for Carrier. Analyst consensus is for just under 6% growth in 2024, followed by 8%-9% annual growth each the following three years.

Valuation

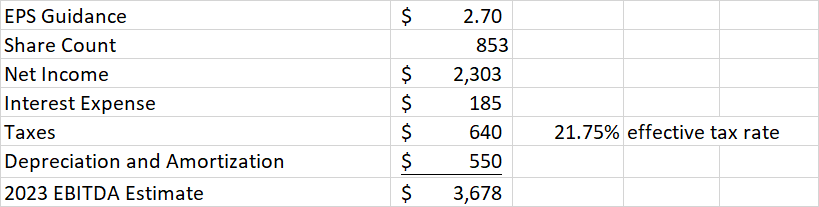

Using company guidance data from the 3Q earnings presentation, I increased Carrier's 2023 EBITDA estimate to $3.678 billion from $3.550 billion in my previous article.

{kind=link}

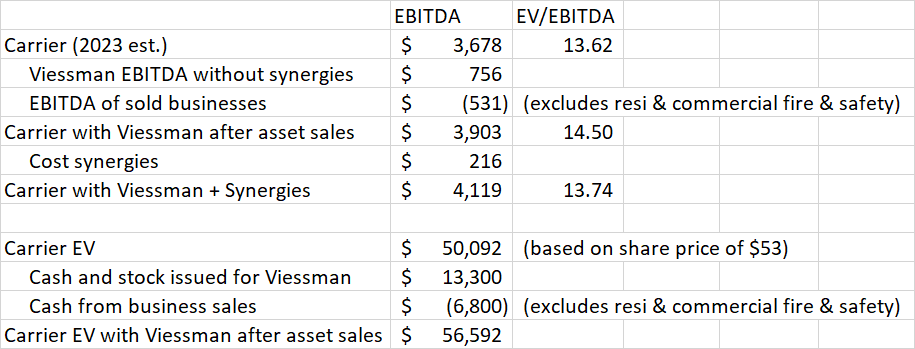

After the large increase in share price since my last article, EV/EBITDA has increased to 13.6 from 11.3 despite the higher EBITDA estimate. In calculating the impact of the Viessmann deal and asset sales, I now use an exchange rate of $1.08/€, down from $1.10 previously. I also now assume the company spins off rather than sells Residential and Commercial Fire & Safety.

{kind=link}

Most peer companies have also seen their share prices rise in the last 7 months, especially Lennox ( LII ) and Trane ( TT ). However, these two competitors have also seen the highest upward revision of their EBITDA growth rates as indicated on the Seeking Alpha peer comparison page. Post-Viessmann, Carrier now looks more expensive than Johnson Controls ( JCI ) and Daikin ( DKILF ), in line with Lennox, and cheaper than Trane. I should note that I am assuming the Viessmann deal increases Carrier's growth potential by 1 percentage point per year based on language in the deal announcement presentation of "over 100 bps". Actual growth could be higher if the merged company can achieve revenue synergies in addition to the cost synergies already accounted for in these calculations. In that case, Carrier would be more deserving of its valuation alongside Lennox and Trane.

{kind=link}

Conclusion

Carrier share price has enjoyed a considerable increase since the initial skepticism hit after announcing the deal to acquire Viessmann. While no longer clearly the cheapest of its peers, it is still a good play on the electrification of HVAC. Revenue synergies from the merger not assumed in the stated deal benefits could provide upside to earnings.

In the year ahead, as Carrier integrates Viessmann and sells off the refrigeration and fire & safety businesses, quarterly earnings could be volatile. Another source of volatility is the phaseout of R-410 refrigerant and replacement with R-454B. Destocking the old units at the start of 2024 and ordering new ones in the second half could cause earnings to be more back-end loaded. If shares get hit because the market focuses on these short-term issues, it would present a buying opportunity.

For further details see:

Carrier: Cool Things Happening In 2024