CARR - Carrier Gets Growth Boost From Viessman Deal

2023-04-27 14:54:15 ET

Summary

- The planned acquisition of Viessman Climate Solutions gives Carrier more exposure to the fast-growing, government-supported trend of electrifying heating systems in Europe.

- Carrier will become more of a pure-play HVAC company by selling most of its Fire & Security and Refrigeration businesses.

- Carrier is paying a high price, even if planned synergies are delivered, but the recent share price declines make the stock attractive.

Tapping Into A Growth Trend

Carrier Global Corp. (CARR) is making moves to become a pure play HVAC company and tap into fast-growing European electric heating market. Carrier announced plans to acquire the privately-held German company Viessman Climate Solutions for a total of €12 billion in cash and stock. The company also announced the intent to sell most of the Fire & Safety and Refrigeration segments. While Carrier will issue stock and debt to complete the Viessman deal, much of it will be bought back when the sales of the non-HVAC segments are complete. The resulting company will be a climate control leader across all world regions with a high-end brand in Europe, where a secular tailwind is driving conversion of heating systems from fossil fuel to electric.

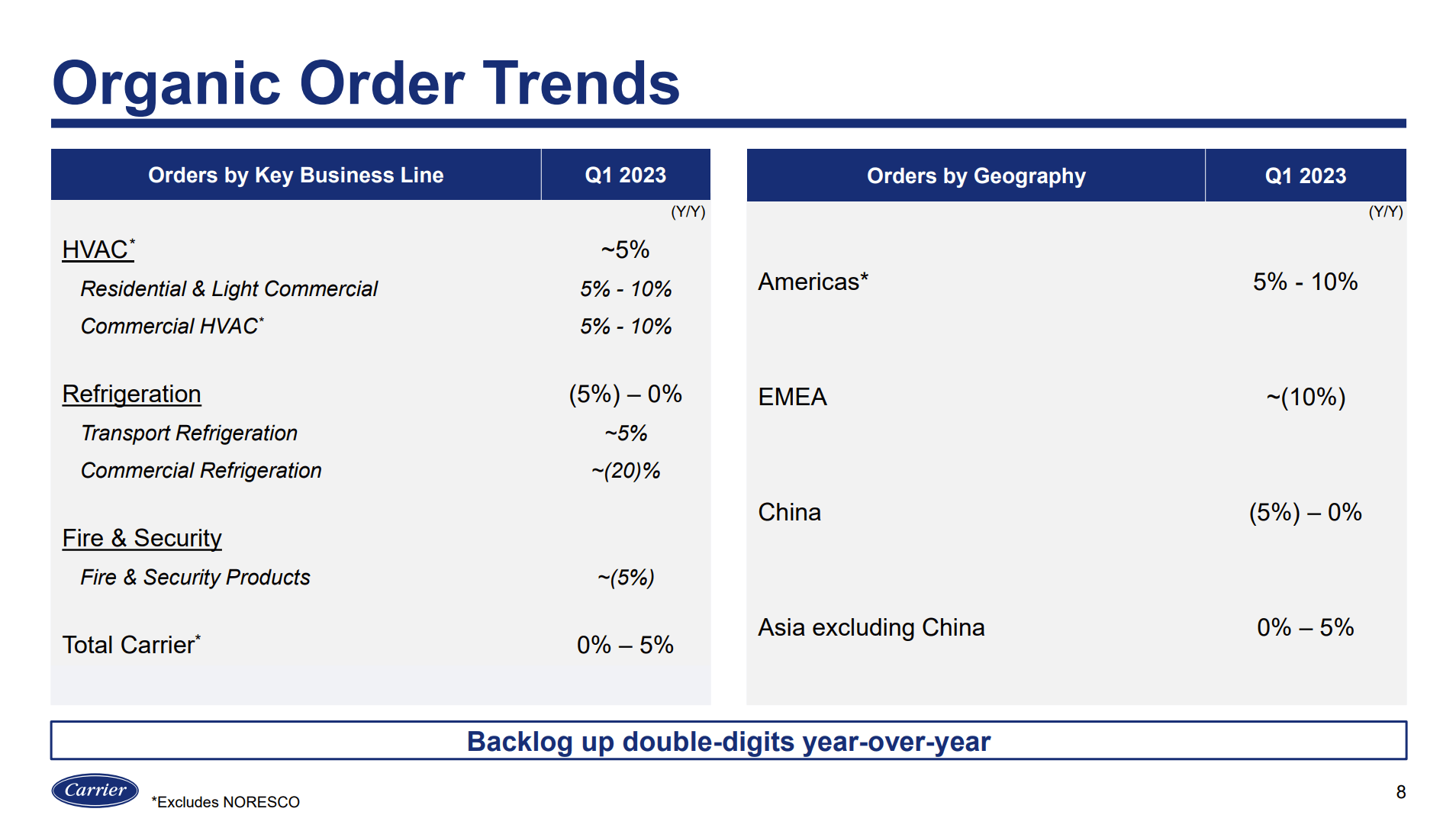

The deal announcement pre-empted Carrier's Q1 2023 earnings report , which was released a day early and basically skimmed over by management on the analyst call to cover the deal. When I last wrote about Carrier in October 2022 , I noted that North American residential HVAC orders were cooling off, but commercial orders were up strongly. The Q1 presentation shows that these orders did indeed turn into sales, as light commercial HVAC sales were up over 30% and large commercial sales were up a double digit percentage. Looking forward, the commercial backlog is still large, suggesting healthy sales for the rest of the year. New orders are now more balanced, with both residential and commercial HVAC orders showing high single-digit growth.

{kind=link}

On the bottom line, Carrier left their 2023 EPS guidance at $2.50 - $2.60 for the year, which is also in line with the $2.52 estimate I noted last October. Overall, there was little in Q1 earnings to change my view of Carrier from what I wrote at the end of last year. It is a steady but cyclical company that can be bought when the price is right, as it was in October and is again after the recent share price drop. The primary reason for this update is to discuss the Viessman deal, which allows Carrier to benefit from the secular trend toward electric heating in Europe.

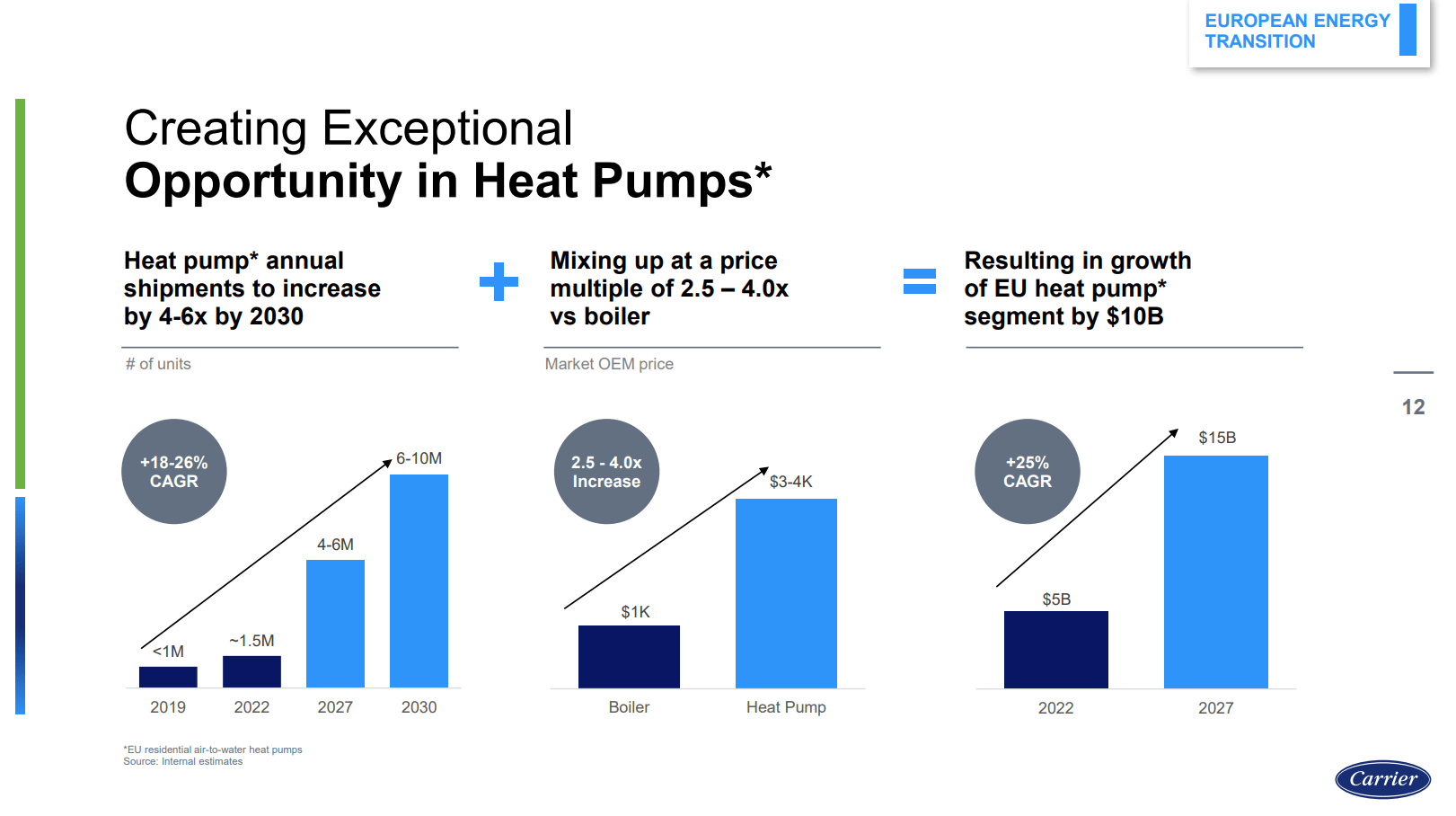

Before 2022, Europe was already at the center of the sustainability movement to combat climate change. Russia's invasion of Ukraine and the resulting spike in natural gas prices brought additional urgency to the electrification effort. The EC plans to add 10 million heat pumps in the next five years with further growth beyond that. 17 European countries have announced or implemented bans on heating systems that use fossil fuel. Carrier expects European heat pump shipments and revenues to grow by about 25% per year through 2030.

{kind=link}

Viessman has been around for 100 years, similar to Carrier, and has been a provider of fossil-fuel based boilers. They have evolved into a provider of high-end heat pumps for both indoor climate control and water heating. Viessman also provides home battery and solar panels so that consumers can have a one-stop solution to fully electrify their home, along with aftermarket service and controls. Heat pumps cost up to 4 times as much as boilers. Installing a full system with batteries and solar panels plus a service contract can generate up to 20x the revenue of a boiler.

Paying For Growth

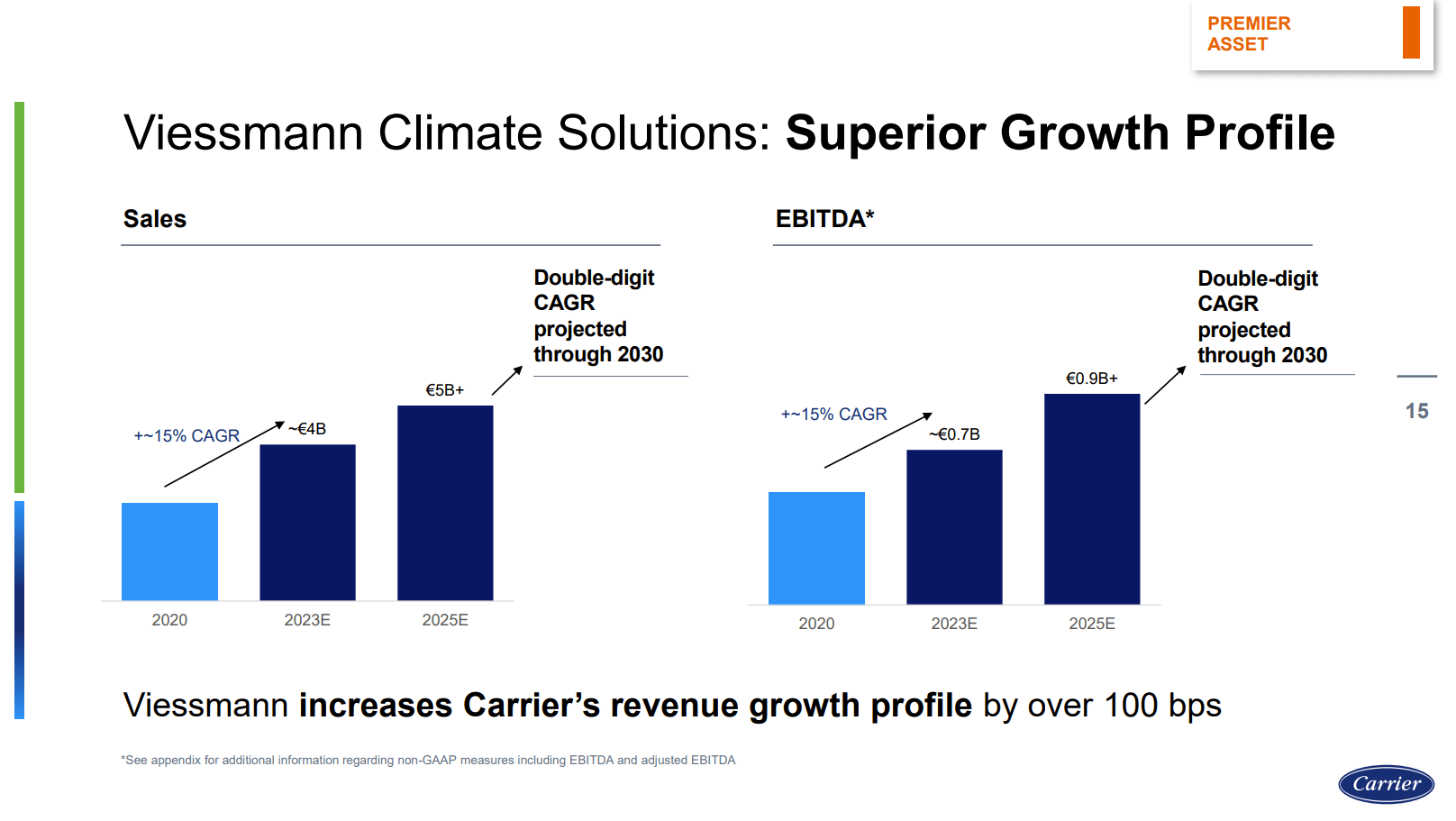

With this fast-growing business, Carrier expects the Viessman acquisition to add 1 percentage point to their long-term EBITDA growth rate. This is not coming cheap, at a total cost of €12 billion ($13.3 billion). Carrier initially will finance this deal by issuing 58.6 million shares of stock ($2.4 billion, 7% of currently outstanding shares) to Viessman's private owners. They will also issue €7 billion in debt ($7.7 billion) with the remainder paid for with cash on hand. In exchange, Carrier gets a business expected to earn €700 million in 2023, growing 15% per year thereafter.

{kind=link}

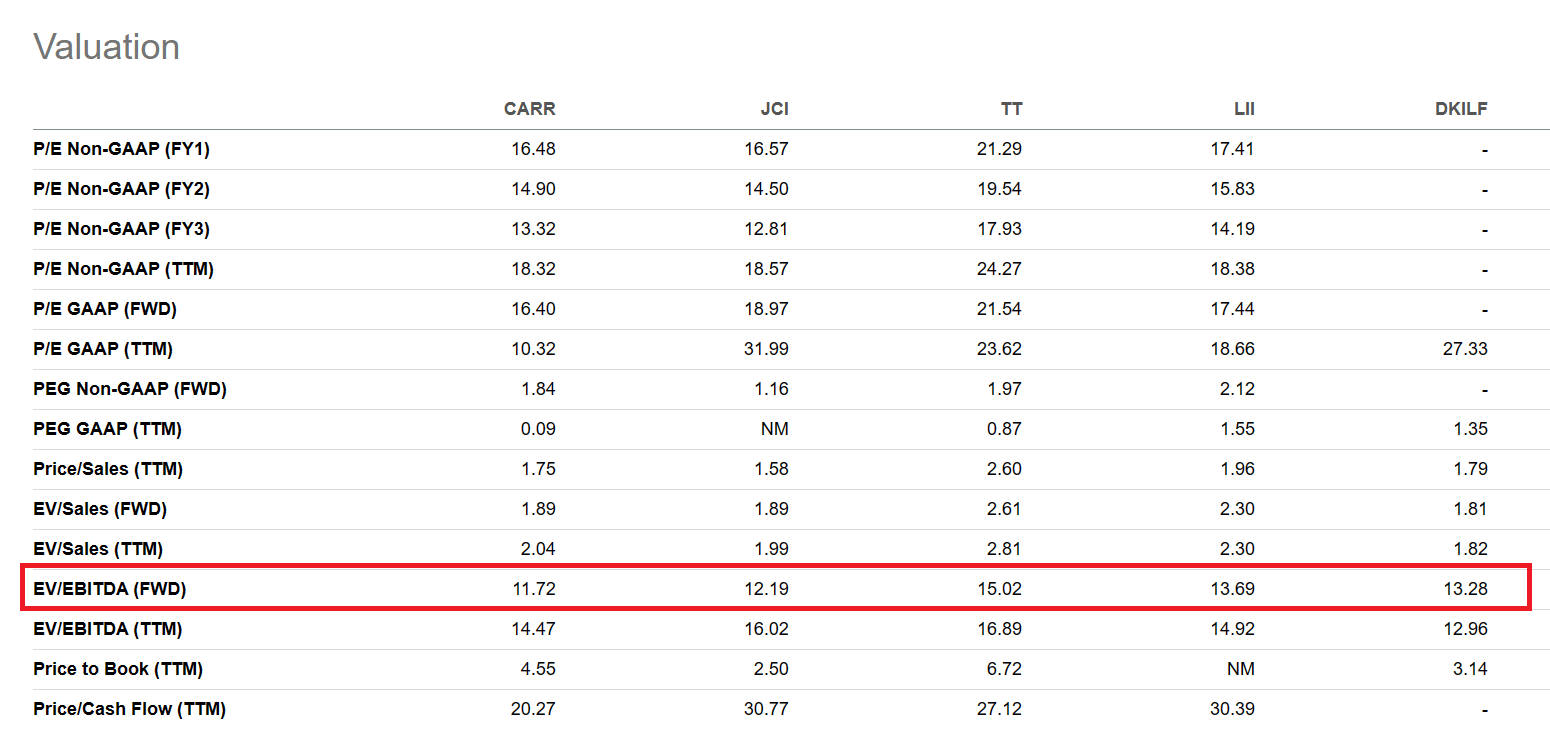

This is very expensive, with an EBITDA multiple of 12/0.7 = 17 times. However, Carrier expects €200 million per year of cost synergies, mostly from reducing materials sourcing costs. This takes us to the 12/0.9 = 13 times multiple cited in the news release. This is more expensive than existing Carrier overall, but in-line with competitors like Lennox ( LII ) and Daikin ( DKILF ), and a bit cheaper than Trane ( TT ).

Seeking Alpha Peer Comparison Page

{kind=link}

No revenue synergies are included in the €200 million estimate but could provide additional value. These would include using Viessman's sales channels to sell Carrier branded products as well as adopting Viessman's technology and selling their products outside of Europe.

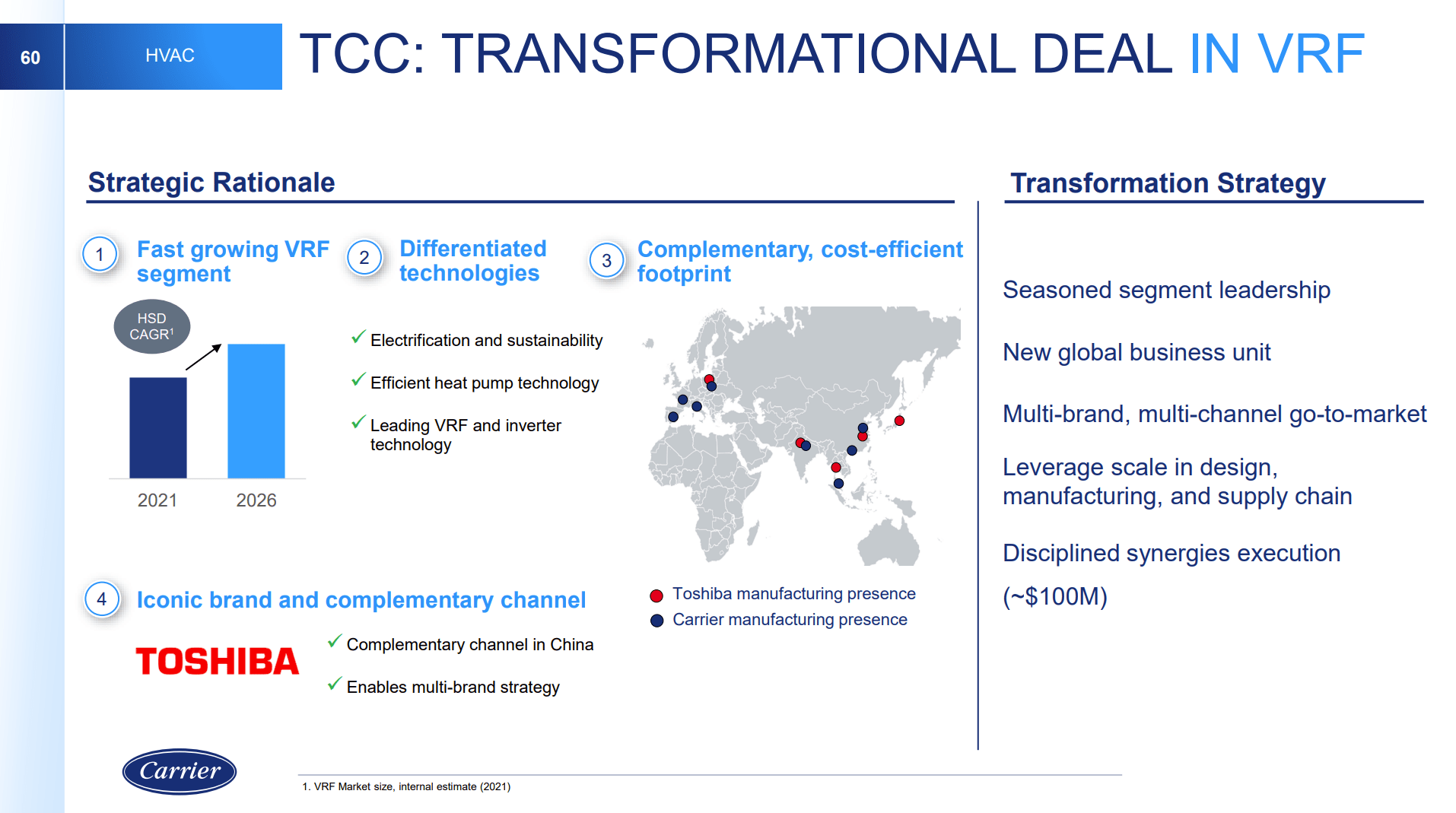

Carrier is not new to successful inorganic growth. Last year, they completed the buyout of Toshiba's ( TOSBF ) stake in the Toshiba Carrier joint venture, following the purchase of Guangdong Giwee Group in 2021. Both of these deals provided cost synergies by optimizing manufacturing facilities in Asia. In the case of Toshiba Carrier, Carrier paid $900 million for an incremental $90 million annual profit and now believe they can exceed $100 million of cost synergies. Further, both Asian acquisitions bring expertise in heat pumps with Variable Refrigerant Flow technology which Carrier can incorporate into its products worldwide. Carrier was already discussing expanding Toshiba sales in Europe prior to the Viessman deal.

{kind=link}

The Viessman deal brings similar opportunities to optimize the manufacturing footprint in Europe. If Carrier is able to deliver $100 million in synergies on the $900 million Toshiba buyout, $200 million from the much larger Viessman acquisition seems plausible.

The deal is expected to be slightly dilutive to Carrier's earnings in 2024 due to about $150 million of integration costs and investments needed to deliver the cost synergies. The merger will be accretive in 2025 and beyond. By the end of 2025, Carrier expects to get back down to a net debt/EBITDA leverage of 2x after temporarily going up to 3.5x at the close of the deal. This plan does not count on the sales of Fire & Security and Refrigeration which would enable the company to pay off debt and resume share buybacks sooner.

Valuing The Non-Core Businesses

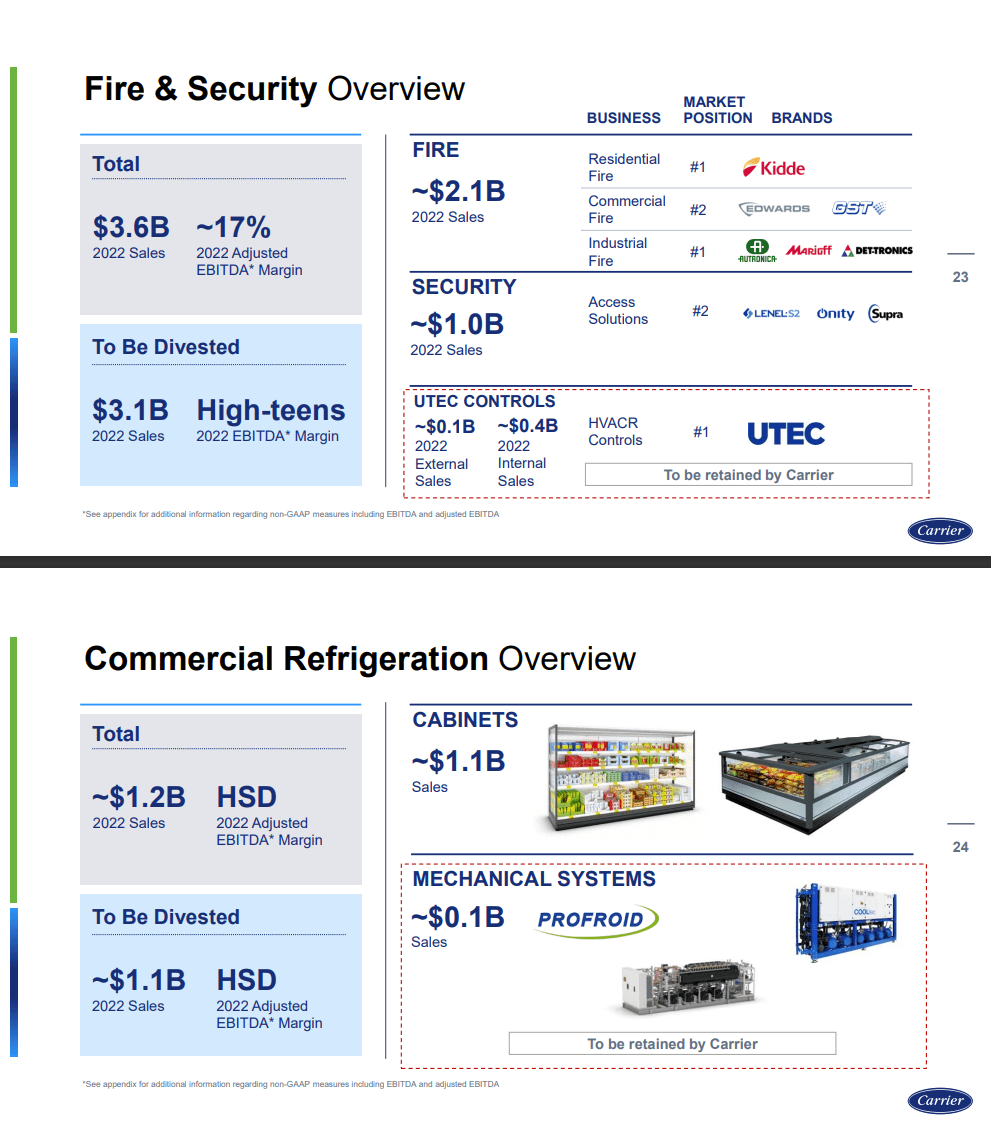

Carrier is planning to sell most of the Fire & Security business which had $3.1 billion of sales in 2022 at a "high teens" EBITDA margin, as well as most of the Refrigeration business which had $1.1 billion in sales at a "high single digit" margin. If we assume 18% margin for Fire & Security and 8% for Refrigeration, Carrier is selling a total of $650 million/year worth of EBITDA. This is less than Viessman's annual EBITDA of €700 million ($770 million) before any synergies, and Viessman's earnings are expected to grow faster than the businesses being sold.

{kind=link}

To value these businesses, we can go back to Carrier's 2021 sale of the Chubb business from the Fire & Safety segment. Chubb generated $2.2 billion in sales in 2021 at an EBITDA margin of 9% for EBITDA around $200 million. Carrier realized a net sales price of $2.6 billion for this business, resulting in an EBITDA multiple of 13. On the analyst call following the Viessman deal announcement, management stated these assets should get a higher multiple than Chubb. Using the 13 multiple, however, the remaining Fire & Security and Refrigeration businesses would be worth 0.65 * 13 = $8.45 billion. This would cover the buyback of $2.4 billion worth of stock and about $6 billion in debt. That would leave an additional $1.7 billion of gross debt outstanding above the current amount of $8.8 billion. Carrier currently generates about $1.3 billion per year of free cash flow after dividends, so this debt could be paid down in less than two years.

Company Valuation

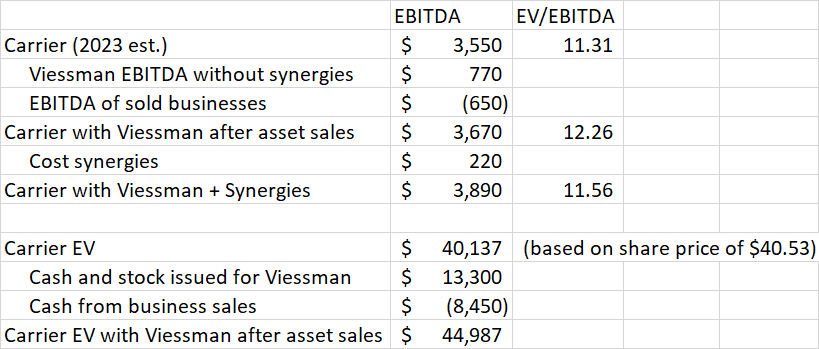

At an 11.3 EV/EBITDA multiple, Carrier is cheaper than the peers shown in the valuation table earlier in this article. (I updated the EV of Carrier based on the share price decline on the day of the deal announcement.) Following the deal and business sales, I estimate EV/EBITDA would increase to 12.3 with no cost synergies or 11.6 with planned cost synergies.

{kind=link}

These values are still cheaper than peers. The lower valuation is justified as Carrier's expected EBITDA growth is the lowest of the group. If we divide the EV/EBITDA multiple by the growth rate (similar to a PEG ratio), we see that Carrier is the most expensive relative to growth. Following the deal and the higher growth, Carrier looks cheaper than Lennox and about in line with Trane when normalized to the growth rate.

{kind=link}

(Growth estimates from Seeking Alpha Peer Comparison page)

Conclusion

The market has beaten up Carrier's share price by over 10% since rumors of the Viessman deal first surfaced . The deal will be dilutive in the first year and increase Carrier's leverage. Considering the government-driven push to electrify heating in Europe however, Carrier should be able to increase its growth rate with this deal. Selling the slower-growing Fire & Security and Refrigeration businesses will enable the company to buy back stock and most of the debt issued in the deal. Shortly thereafter, growing free cash flow should allow the company to pay off the remaining new debt.

The repositioned new pure-play HVAC company looks to be valued in-line with peers when normalized to expected growth rate. Upside exists from the potential for Carrier and Viessman to share technology and cross sell their brands worldwide. The recent share price pullback and announced deal make Carrier a great way to play the ongoing trend of electrification in the HVAC market.

For further details see:

Carrier Gets Growth Boost From Viessman Deal