QSR - Carrols Restaurant Group: Not The Best Part Of The Fast Food Value Chain

2023-12-30 02:18:09 ET

Summary

- Carrols Restaurant Group is the largest Burger King franchisee in the US, operating ~15% of all Burger Kings.

- Since going public in 2006, Carrols has delivered a total return of 111%, compared to the S&P 500's return of 364%.

- Despite benefiting from the strength of the Burger King brand, Carrols faces challenges related to restrictive franchise agreements.

- Carrols has struggled to generate consistent profits and EPS growth historically, and I expect this to continue.

- I am initiating Carrols with a hold rating, as I believe the franchisor part of the fast food value chain represents a much better investment at current levels.

Carrols Restaurant Group ( TAST ) is the largest Burger King franchisee in the country operating ~15% of all U.S. Burger Kings.

Since becoming a public company in December 2006, TAST has delivered a total return of 111%. Comparably, the S&P 500 has delivered a total return of 364% during the same time period.

While TAST has benefited from the success of the Burger King brand, returns have been limited due to the nature of its position in the value chain.

As a fast food restaurant operator, TAST faces stiff competition from other restaurants and has significant exposure to rising costs which creates substantial margin volatility.

Comparably, a much better part of the fast food value chain includes companies such as Restaurant Brands International Inc ( QSR ) and McDonald's ( MCD ) which mostly license the use of their brands while owning just a small fraction of restaurants operated under their brands.

Market participants are well aware of this dynamic and thus TAST trades at a lower valuation than companies such as QSR or MCD. However, I believe the current discount is warranted and TAST is not highly attractive at current levels.

Largest Burger King Franchisee In The U.S.

TAST is the largest Burger King Franchisee in the U.S. with 1,020 restaurants. The company also operates 60 Popeyes restaurants.

TAST was established in 1960 as a fast-food hamburger company and became the largest BurgerKing franchisee in 1976 by converting 78 Carrols restaurants to BurgerKing franchises. The company has grown through both organic growth and M&A. The company has grown its restaurant count from 547 in 2006 to 1080 today representing a ~4.1% CAGR.

{kind=link}

A Challenging Business Model

The fast-food franchisee business model is challenging. While TAST benefits from being able to use the BurgerKing and Popeyes brands, it faces many other challenges.

One of the biggest challenges that TAST faces is that it is bound by franchise agreements entered into with Burger King, which is owned by Restaurant Brands International ( QSR ).

To open a new restaurant TAST must pay Burger King an initial franchise fee of $50,000 and a $50,000 fee upon renewal. In the event that TAST decides to terminate a franchise agreement, it must pay Burger King the net present value of the royalty stream that would have been realized by Burger King if the agreement had not been terminated. Furthermore, TAST is required to pay Burger King and Popeyes a monthly royalty based on a percentage of sales. Currently , the royalty rate for new Burger King restaurants is 4.5% of sales and the royalty rate for Popeyes restaurants is 5% of sales. TAST is also generally required to contribute 4% of restaurant sales to fund Burger King and Popeyes national and regional advertising campaigns.

These royalty and advertising related payments are very large relative to the net profit margin potential of the business. Historically, TAST has generated an average net profit margin of just 0.50%.

Despite the highly restrictive nature of TAST's franchise agreements, the company does not have exclusive rights to operate Burger King restaurants in any defined territory. In its 10-K, TAST provides additional commentary around this challenge:

Our franchise agreements with BKC and PLK do not give us exclusive rights to operate Burger King restaurants in any defined territory. Although we believe that BKC generally seeks to ensure that newly granted franchises do not materially adversely affect the operations of existing Burger King restaurants, we cannot assure you that franchises granted by BKC to third parties will not adversely affect any Burger King restaurants that we operate.

Another challenge for TAST is that is has significant capital requirements. TAST owns 9 restaurant properties and leases 1,078 restaurant properties. Typically the company's leases range from 20 to 40 years. Additionally, TAST is generally responsible for remodeling and upgrading restaurants over-time though Burger King makes certain contributions toward remodeling costs. In recent years, the company's average cost in terms of improvements related to franchise agreement renewals has ranged from $500,000 to $1,200,000 per restaurant.

Finally, TAST also faces challenges due to changes in input costs. Specifically, the cost of labor and food commodity products poses challenges as TAST has limited pricing power due to a highly competitive fast-food marketplace. The impact of rising costs can be seen in the company's performance during 2022 when adjusted EBITDA margins dropped to 3.6% and the company reported a $1.49 loss per share.

The result of all these challenges is that TAST has struggled to generate strong profitability through economic cycles and has delivered an average ROIC of -0.42% since becoming a public company in 2006.

Further proof for the fact that the Burger King franchisee business is challenging can be seen in a number of recent bankruptcy filings by Burger King franchisees. Toms King, an operator of 90 Burger King franchises, filed for bankruptcy in January 2023. Meridian Restaurants Unlimited, an operator of 118 Burger King franchises, filed for bankruptcy in March 2023. Through a bankruptcy process 70 of the locations were sold back to Burger King and other franchisees. Premier Kings, an operator of 172 Burger King franchises, filed for bankruptcy in November 2023.

Strategic Relationship with RBI

TAST has a strategic relationship with Burger King and its parent Restaurant Brands International ( QSR ). Currently, QSR owns Series D preferred stock which is convertible into 9,414,580 shares of common stock which represents ~14.7% of TAST shares outstanding. QSR is entitled to elect two members to TAST's board of directors. Moreover, TAST is also required to get approval from QSR for certain actions including paying a special cash dividend or engaging in any business other than the ownership and operation of Burger King Restaurants.

While QSR's ownership stake in TAST helps to align incentives, it should be noted that incentives are not fully aligned as QSR still benefits more from a dollar of earnings attributable to itself vs TAST. That said, QSR is incentivized to make sure that TAST is able to generate enough cash flow to ensure that restaurants are upgraded and new restaurants are opened.

Ultimately, QSR benefits from a stronger and more vibrant franchise system. Given the fact that TAST is the largest U.S. franchise operator its success matters greatly to QSR. However, QSR is incentivized to drive marginal profits to itself as opposed to TAST. Given this dynamic, I believe QSR is a valuable partner for TAST and has a vested interest in its success but will not take actions that benefit TAST at the expense of its own shareholders.

Highly Levered Balance Sheet

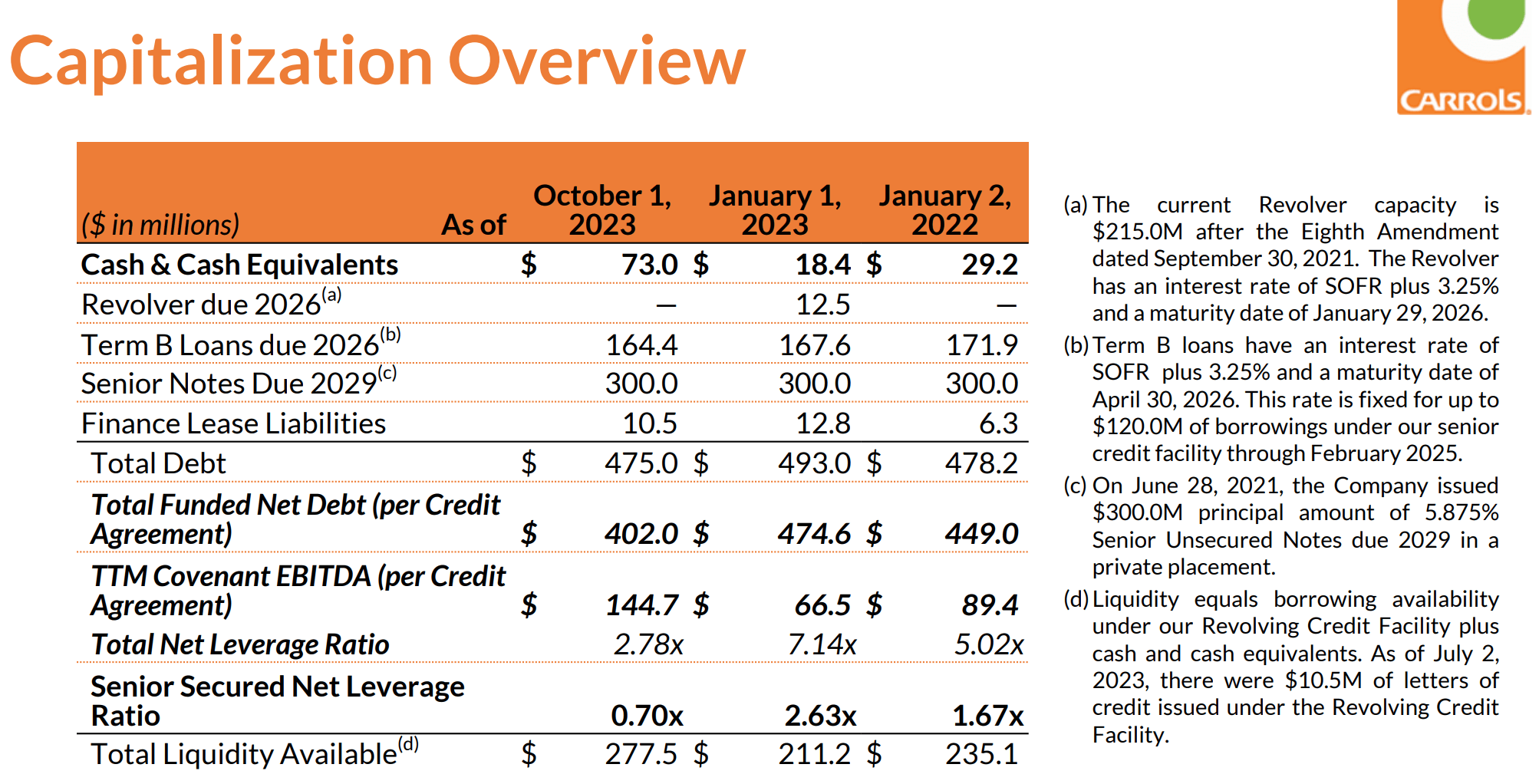

TAST started 2023 with a very high total net leverage ratio of 7.14x. The company made substantial progress during the year to improve covenant EBITDA via margin improvement. As of October 1, 2023 the company's leverage ratio improved to 2.78x.

Despite significant improvement, TAST remains highly levered. I view the company's balance sheet as too highly levered given the volatile nature of earnings and cash flows due to margin variability. TAST recent announced the initiation of a $0.02 per share quarterly dividend. I would have preferred to see the company use this cash toward further reducing its debt load.

TAST faces a potential increase in interest expense upon refinancing the $300 million Senior Notes due 2029. These notes were issued in June 2021 and carry a fixed coupon of 5.875%. At the time, the U.S. 10 year note was yielding ~1.5% and thus the notes were issued at a spread of 4.375%. Today, the U.S. 10 year note is yielding 3.84% and thus a similar spread would imply a funding cost of ~8.2%. However, I believe the company may be able to manage this refinancing risk by using a portion of cash on the balance sheet, revolver capacity, and free cash flow generated in the coming years to reduce this large refinancing risk.

{kind=link}

Fast Food Franchisors Have A Better Business Model

A much better part of the fast food value chain is the position held by companies that own great brands and are focused on franchising such as QSR and McDonald's. A relevant comparison for TAST is Arcos Dorados Holdings ( ARCO ) which operates over 2,140 McDonald's restaurants.

As shown by the chart below, MCD and QSR have experienced better profit margins and far less volatility than franchisees such as TAST and ARCO. Furthermore, MCD and QSR have experienced better average ROIC's compared to TAST and ARCO. Superior financial performance by MCD and QSR has led to better shareholder returns as well.

The reason for this is that MCD and QSR are primarily in the business of licensing their brands and growing their restaurant count. This means they are much less exposed to challenges such as rising labor costs and economic challenges which can lead to short-term drops in revenue for restaurant operators.

TAST's Relative Valuation Is Not Highly Attractive

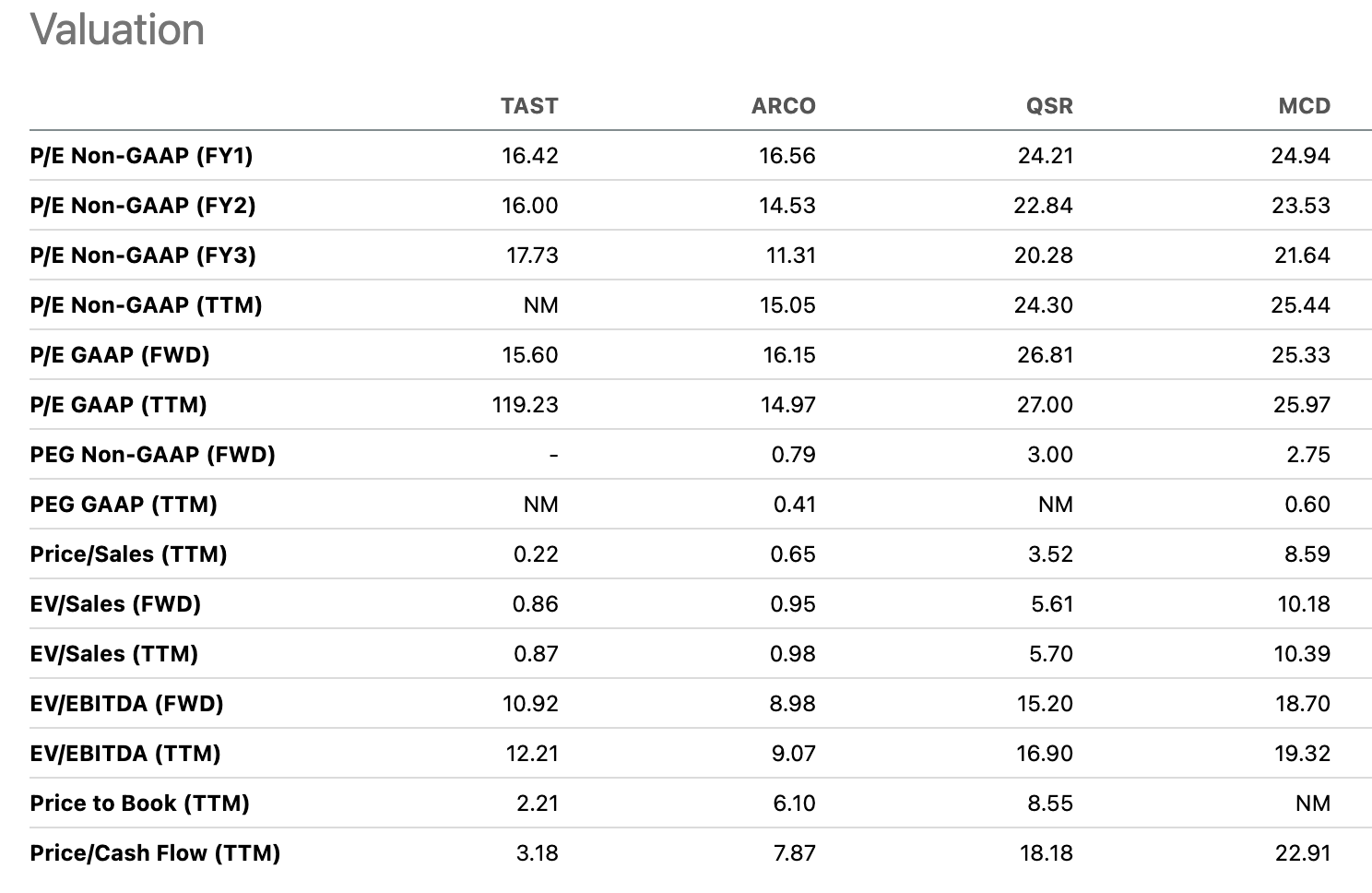

Currently, TAST is trading at 16x consensus FY 2024 EPS and 17.7x consensus FY 2025 EPS. Comparably, ARCO trades at 14.5x FY 2024 consensus EPS and 11.3x FY 2025 consensus EPS. ARCO is a faster growth story given its exposure to emerging markets in Latin America and the Caribbean. ARCO is expected to grow FY 2024 and FY 2025 EPS at 14% and 28.4% respectively. Thus, I do not view TAST as highly attractive vs its franchisee peer ARCO.

QSR and MCD trade at 20.3x and 21.6x consensus FY 2025 earnings respectively. I view these companies as much more attractive on a relative basis given their superior business model which leads to lower earnings volatility and more predictable growth.

QSR is expected to grow EPS by 6%, 12.6%, 16.1%, and 14% for FY 2024, FY 2025, FY 2026, and FY 2027 respectively. While long-term EPS growth estimates are not currently available, I do not think TAST will be able to grow at this level based on historical performance.

TAST has struggled to grow earnings historically and has experienced high earnings volatility. I see no reason for this to change going forward. Comparably, QSR and MCD have shown earnings growth and steady profitability historically.

TAST has experienced significant multiple expansion over the past two years while QSR and MCD have not. Thus, I believe TAST is unattractive vs QSR and MCD on a relative valuation basic compared to historical norms.

{kind=link}

Possible Upside Catalysts

One possible upside catalyst for TAST would be if QSR decides to acquire TAST in order to gain complete control. I view this as highly unlikely as ~100% of QSR's system-wide restaurants are franchised. However, it is possible that the company decides to change strategies at some point in the future. Controlling more of the value chain would better allow QSR to manage the Burger King customer experience.

Another potential upside catalyst for TAST would be if the Burger King brand were to gain share vs other players such as McDonald's or Wendys. Burger King has lost market share in recent years to McDonald's and other players. In late 2022, QSR announced a "Reclaim the Flame" plan to accelerate growth in the U.S. and drive franchisee profitability. The plan includes investments of $400 million in key areas such as advertising and digital investments through FY 2024. Despite these turnaround efforts, Burger King continues to underperform McDonald's. During Q3 2023, Burger King reported comparable year-over-year sales growth of 7.2% which missed analyst expectations of 8.7% growth. Comparably, McDonald's reported comparable year-over-year sales growth of 8.8%.

While further improvement in Burger King sales is possible, I believe significant market share gains may be difficult to achieve given the challenging competitive marketplace.

Conclusion

I do not believe that TAST represents the most attractive way to gain exposure to the fast-food restaurant business. While TAST benefits from the strength of the Burger King brand, the company faces challenges related to the fact that it is bound by franchise agreements with Burger King. TAST is highly exposed to changes in inputs costs and revenue given its narrow margins.

TAST has struggled to generate earnings growth historically and I do not see this changing going forward. The company has made significant operational improvements over the past year which have led to margin improvement.

TAST is currently trading at a valuation which is high relative to franchisee peer ARCO. TAST trades at only a marginal discount to restaurant franchisors such as QSR and MCD. I believe this discount is fully warranted and investors looking to gain exposure to the fast food business value chain would be better served investing in these companies instead of TAST.

I am initiating TAST with a hold rating and would consider downgrading the company to sell if its valuation increases moderately from current levels.

For further details see:

Carrols Restaurant Group: Not The Best Part Of The Fast Food Value Chain