CARE - Carter Bankshares: A Hidden Gem To Fight Inflationary Headwinds

2023-04-21 06:25:34 ET

Summary

- Carter Bankshares, Inc. is a hidden gem that investors may add to their portfolio.

- There may be a mild recession, but the company can withstand it.

- CARE stock price has been in a downtrend since 4Q 2022.

Carter Bankshares, Inc. (CARE) is a Virginia-based bank holding company. In the past three years, it had dealt with various disruptions, leading to its contraction in 2020. Despite this, the bank proved its resilience as it rebounded and attracted more customers and borrowers. Today, it faces macroeconomic headwinds posing risks to its operations. But the bank remains solid with its sustained revenue growth and margin expansion. Even better, its liquidity remains in excellent shape with its well-diversified loan and investment portfolio. Borrowings are about twenty times higher than in 4Q 2022, but liquid assets are still adequate to cover them. However, the stock price appears divorced from the current fundamentals. It was logical, though, since near-term market prospects are quite pessimistic. Nevertheless, the stock appears to be worth the risk. The downward pattern is an opportunity to buy shares with potential undervaluation.

Company Performance

Carter Bankshares, Inc. operates in a high-interest market environment. Risks are higher as macroeconomic volatility remains high. It may have to be more careful this quarter as The Fed anticipates a mild recession. Despite this, this regional bank shows it can cushion the blow with its most recent performance and financial positioning. It sustained and balanced its growth with margins.

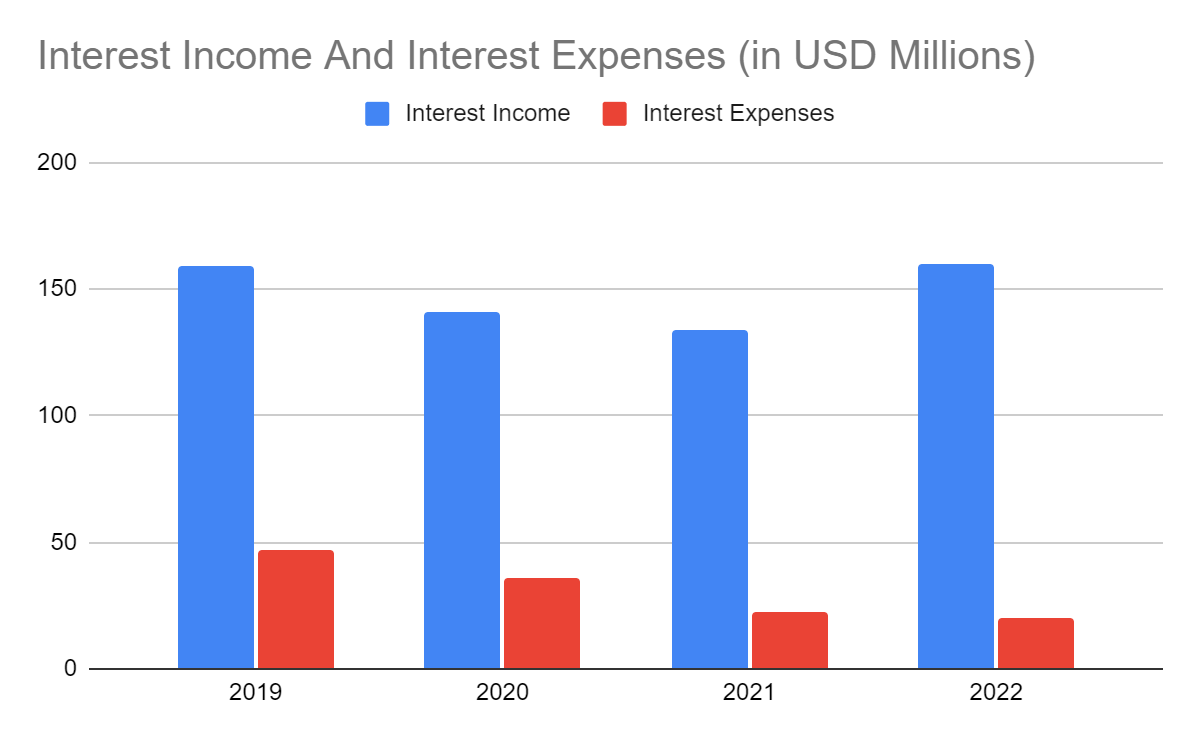

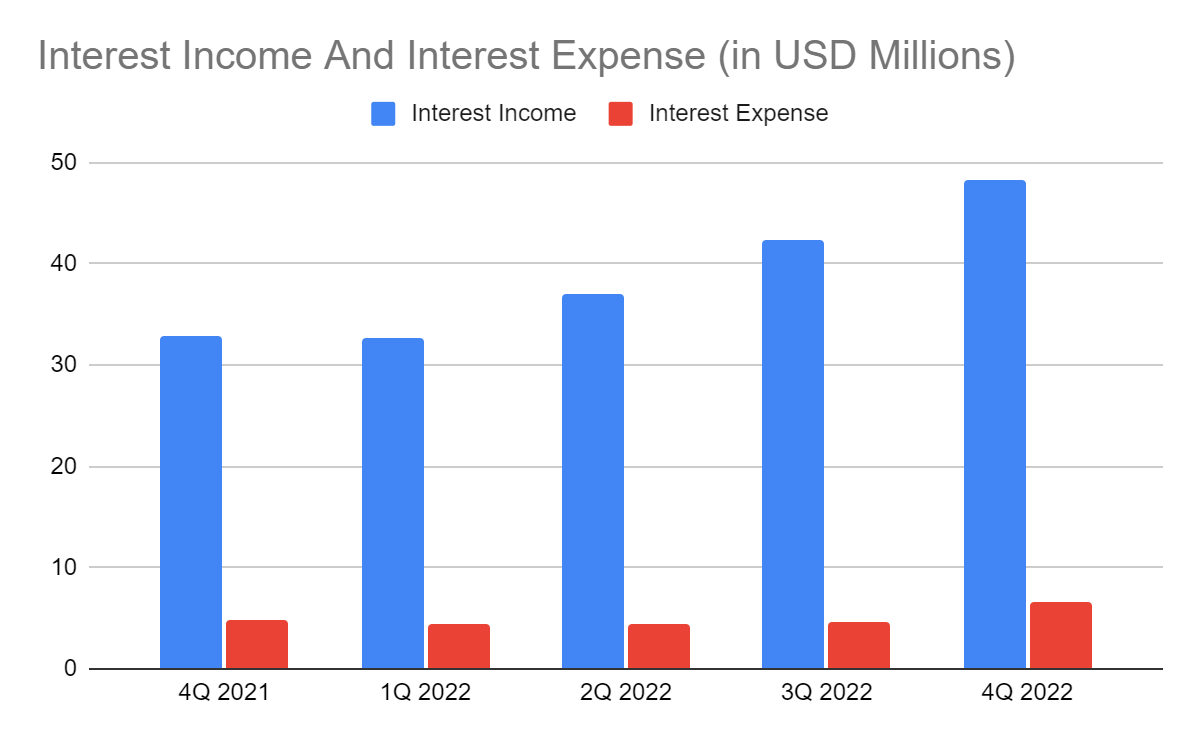

As a bank, its primary sources of operating revenue are loans and investment securities. Given the nature of these assets, revenues come in the form of interest income and yields. The previous year was tough, characterized by skyrocketing prices and interest rates. Yet, CARE managed to stabilize its core operations. Its Interest income amounted to $160.18 million , a 20% year-over-year growth. It also exceeded pre-pandemic levels, showing that higher interest rates worked in its favor. We can see it clearly in its quarterly values, given the uninterrupted increase. In 4Q, it reached $48.22 million, a 46% increase. Indeed, as interest rate hikes persisted, revenue growth sped up. Unlike many other banks that had troubles with loan volume and quality, Carter moved in the opposite direction. We can attribute it to the prudent and active loan repricing of the company. With its strategic loan rates, it was able to attract more borrowers, which led to higher volume and yields. Despite this impeccable trend, CARE remained conservative to minimize defaults and delinquencies. Its NPL to total loans was only 0.21% versus 0.26% in 4Q 2021. So as interest rate hikes intensified, the company became more cautious. Another factor was the prudent diversification of its loans. More than half of its loans belong to its commercial segment. I believe the commercial segment is better than the consumer segment. Borrowers in the commercial segment have a higher capacity to pay loans. Also, collaterals are more secure regarding their fair value. I'm only a bit concerned about its high concentration on CRE loans, given the current changes in the property market. Even so, these loans have better yields and may stay stable despite market worries. We will discuss more of these in the next section.

Interest Income And Interest Expense (MarketWatch)

{kind=link}

Interest Income And Interest Expense (MarketWatch)

{kind=link}

Investment securities are also impressive despite the decrease in their fair value. They only comprised 14% of the total loans. Even so, their yields were noticeable, increasing by 59%. Like its loan portfolio, investment securities were also well-diversified. Over 30% of them are government-backed securities, which are more suitable in a high-interest environment. They also have better yields during inflation than other securities.

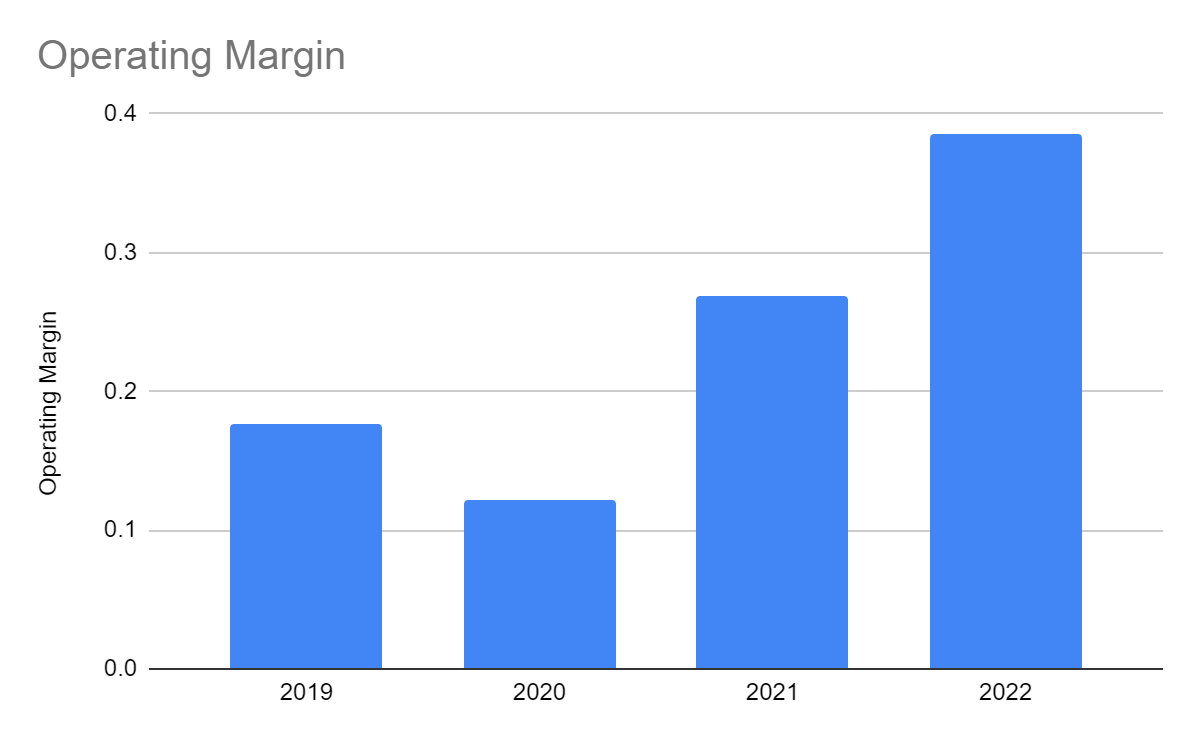

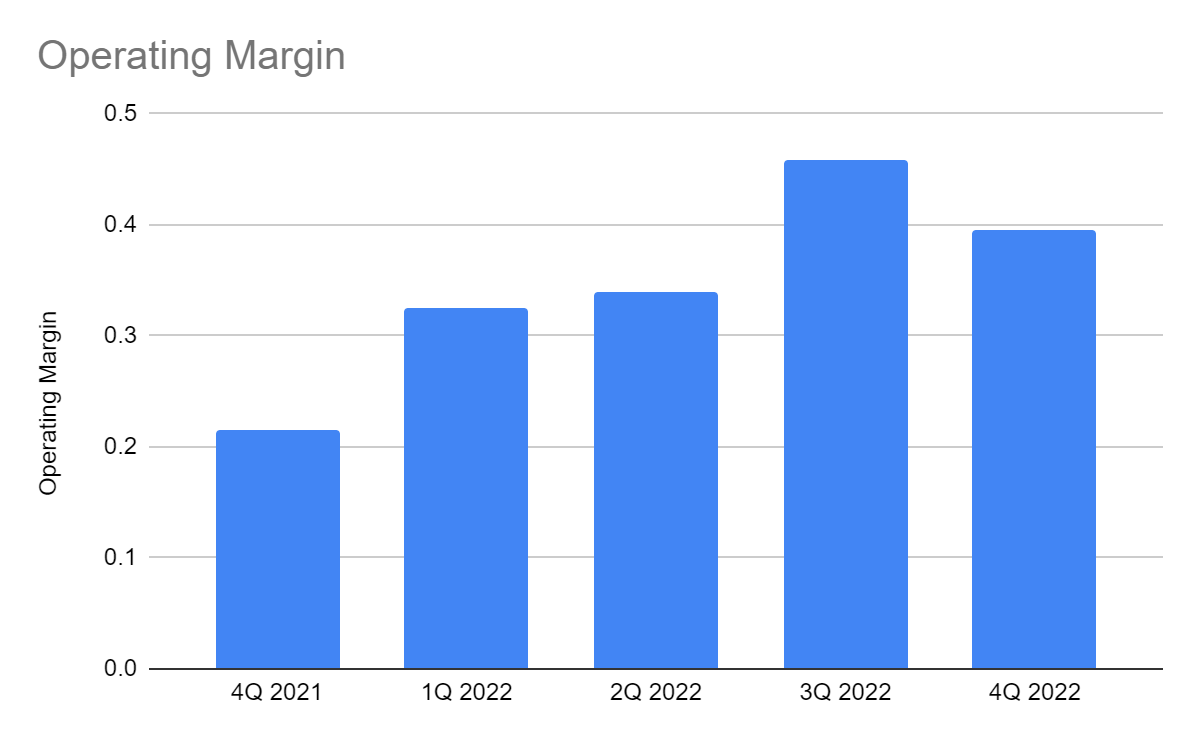

More importantly, Carter remained an efficient company. It also knew how to maintain its performance and financial positioning. Its pricing strategy also applied to deposits. Although inflows decreased, its move worked to stabilize deposit yields. In turn, interest expenses remained manageable even during the interest rate hike peak in the second half. Meanwhile, its non-interest segment was still stable. Non-interest income had a slight decrease in 4Q, which we can attribute to lower deposit volumes. Non-interest expenses were flat amidst the rising prices. In turn, the operating margin reached 38% versus 27% in 2021. In 4Q, it reached 40% versus 22% in 4Q 2021. We can infer that the company took advantage of the situation while ensuring the stability of its costs and expenses. It was able to balance growth and margins.

Operating Margin (MarketWatch)

{kind=link}

Operating Margin (MarketWatch)

{kind=link}

This year, the company may face the same challenges. It may be more visible in the first half since the economy is still adjusting to inflation and interest rate changes. It may be riskier as the mild recession continues to raise pessimism among investors and borrowers. Also, it can discourage borrowers and investors, which can affect its loan volume and investment yields. So right now, the bank must not let its guard down.

On a lighter note, we can see the efforts of policymakers paying off. It may take some time for these to fully stabilize inflation and interest rates. But the gradual improvement in the macroeconomic indicators may materialize. To that end, it will be easier for banks to manage their earning-asset portfolio. We will discuss this aspect in the next section.

How Carter Bankshares, Inc. May Remain Solid This Year

So many concerns are surrounding the banking industry. And Carter Bankshares, Inc. is no exception. The risks are evident and may intensify as The Fed warned of a mild recession. For instance, interest rate hikes persist, given the conservative approach of The Fed to stabilize inflation. This factor is a concern since the continued interest rate hikes can make the cost of deposits and borrowings higher. In turn, interest expense may continue to increase. It may also lower loan volume and loan quality. Although Carter ensures its solid management of loans and deposits, there may come a point where it will be challenging to sustain their growth. Likewise, the cooling of residential and commercial property sales can affect mortgages. It is a concern for the company since CRE loans comprise a substantial portion of the total loans. It can lead to lower CRE loan yields.

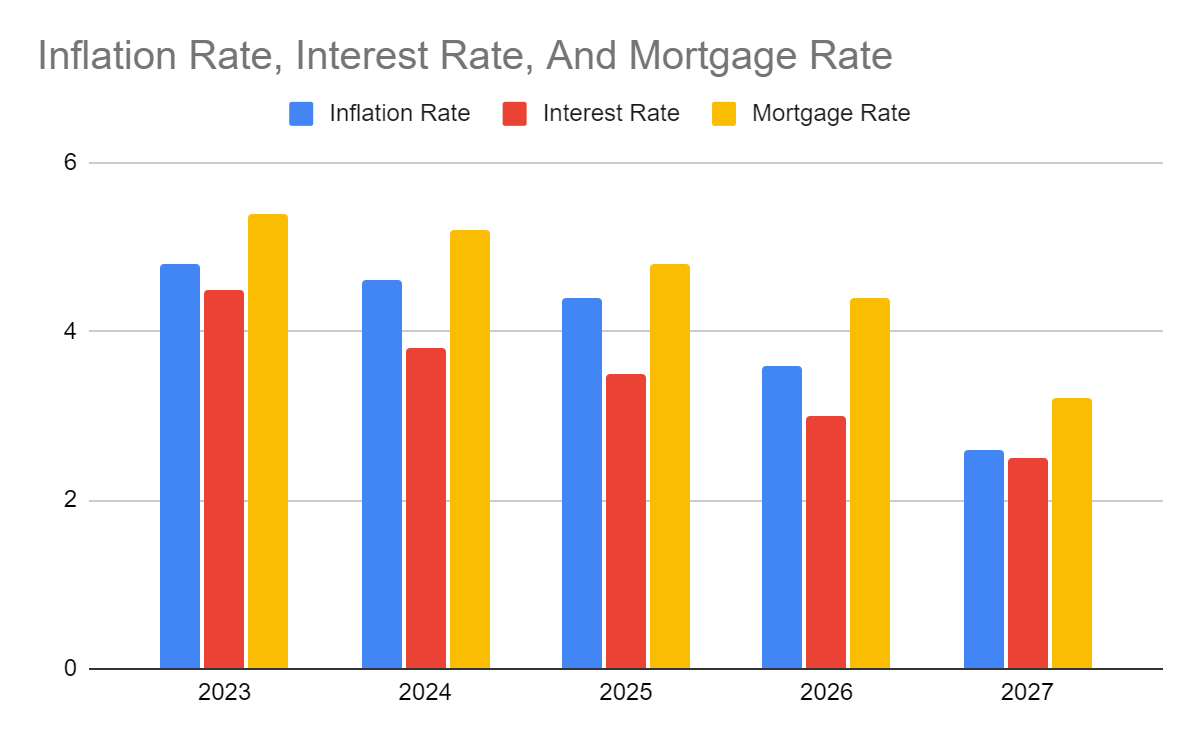

Despite all these, the company can cushion the blow . There are opportunities in the market Carter can seize. We will start with the external forces. Inflation is one of the primary macroeconomic indicators that directly impact interest rates. And now that inflation has relaxed, The Fed may start to ease the monetary policy. Inflation is only 5%, 45% lower than its 2022 peak and 17% lower than last month. Indeed, the strategy of The Fed was effective. With regard to interest rates, it may still increase since it may take more time for it to adjust to inflation. Note that the Fed must continue to stabilize inflation. It can be a reason for the mild recession since higher interest rates can affects the level of borrowings and investments in the economy. On the other hand, we can expect interest rate increments to cool down. In fact, it has already started last Fed board meeting. The most recent increment of 25 bps was way lower than the 75 bps increase in the previous four quarters. The increment downtrend may continue while inflation decreases. It is why I believe Carter can withstand the unfavorable impact of the mild recession should it take place.

Even better, we already saw in its operations its prudent loan and deposit repricing and loan and investment diversification. There is still adequate flexibility so it can adjust loan and deposit rates to stabilize yields and costs. And although the risk of defaults and delinquencies may increase, the fact that it has a high concentration on commercial loans can ensure security.

The same pattern may apply to mortgage rates as interest rates and home sales cool down. The risk focuses on the market crash, but we can disagree with it due to several reasons. Again, it is a crucial factor since CRE loans comprise the majority of loans in Carter. But the important thing is that, the real estate market can slow down price decreases to avoid or minimize market crash potential. First, property shortages remain high. It is more evident in the residential segment, still short of 6.5 million houses. Second, many property builders are still careful, which we have seen over the past decade. Third, the skyrocketing home prices were driven by the massive demand increase, not by material and labor costs.

Inflation Rate, Interest Rate, And Mortgage Rate (Author Estimation)

{kind=link}

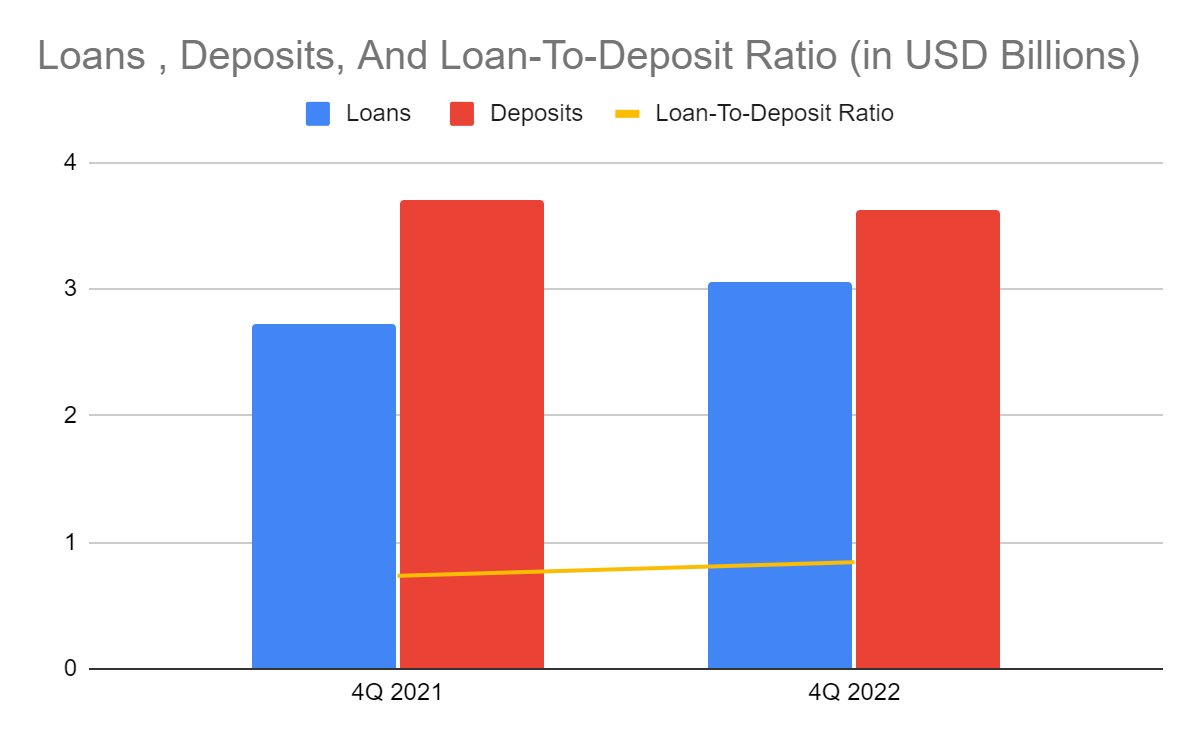

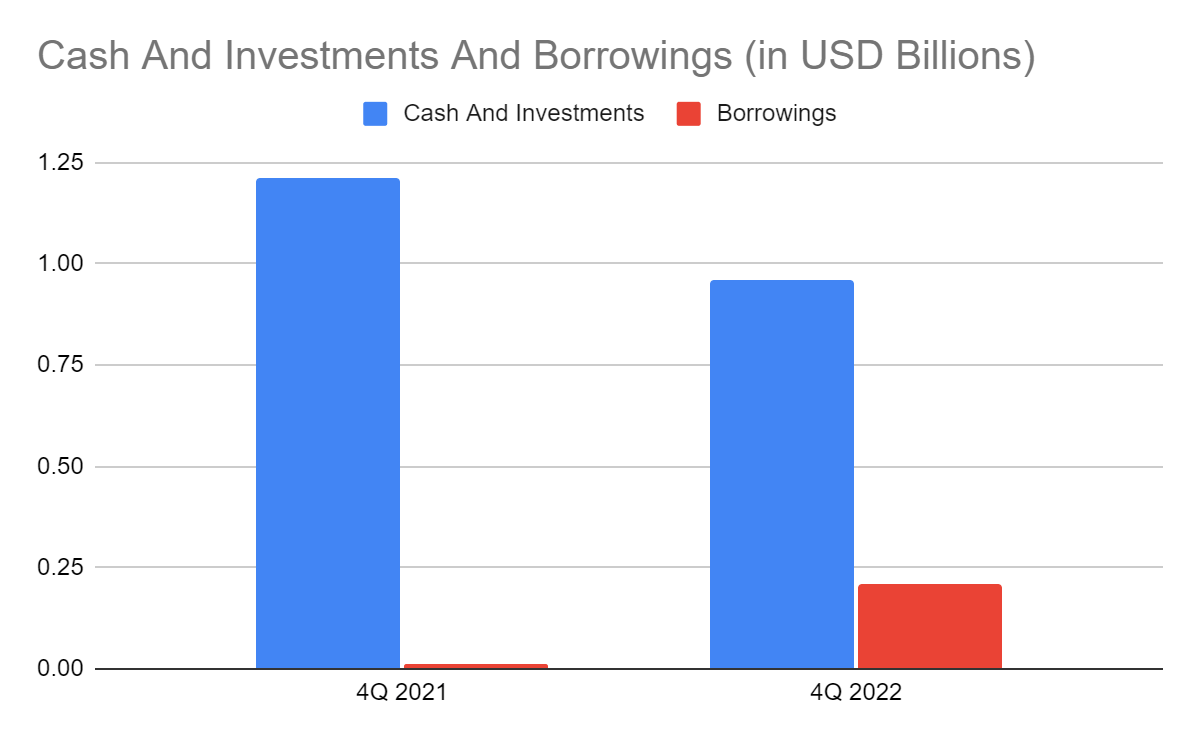

Furthermore, Carter maintains a solid financial positioning. This aspect allows it to sustain its operating capacity while sustaining growth and margins. Its loan and deposits are stable with the loan-to-deposit ratio of 84%. It is still within the average ratio of 80-90%. As such, the company has enough reserves to lend and invest without fearing defaults and delinquencies. Meanwhile, cash has more than doubled in a short period. The combined value of cash and investments comprises 24% of the total assets, making CARE a very liquid company. Borrowings are also another concern, especially since interest rates are higher. But liquid assets are still more than four times higher than borrowings. So, CARE still has enough reserves to sustain its capital returns in the form of share repurchases. This aspect shows that CARE maintains the balance between viability, liquidity, and sustainability.

Loans, Deposits, And Loan-To-Deposit Ratio (Carter 4Q Financial Release)

{kind=link}

Cash And Investments And Borrowings (Carter 4Q Financial Release)

{kind=link}

Stock Price Assessment

The stock price of Carter Bankshares, Inc. has been in a downtrend for a few months. The slow-moving pattern appears divorced from the fundamentals. At $13.45, the stock price is 24% lower than last year's value. Despite this, one may still see it as an opportunity to buy shares at a discount. The rebound may be reasonable since the company has recently authorized repurchasing one million shares. Aside from that, its PTBV Ratio shows that the stock price reflects the intrinsic value of the company. With the current TBVPS of 13.72 and the current and average PTBV of 0.99x and 1.04x, the target price will be $14.88. While their difference is narrow, the stock price shows quite cheap. Likewise, the PE Ratio of 6.47x and the EPS forecast of NASDAQ at $2.31 gives a target price of $14.93. To assess the stock price better, we will use the DCF Model.

FCFF $47,000,000

Cash $89,230,000

Borrowings $205,020,000

Perpetual Growth Rate 4.2%

WACC 9%

Common Shares Outstanding 23,957,000

Stock Price $13.45

Derived Value $18.98

The derived value also shows that the stock is undervalued. There may be a 41% upside in the next 12-18 months. So, investors may add this stock to their watchlist.

Bottomline

Carter Bankshares, Inc. is a solid bank that strategically uses the current macroeconomic trends to its advantage. It continues to balance growth and viability with sustainability. It has impressive liquidity levels, allowing it to cover its operating capacity and capital returns. Also, the stock price is undervalued. The recommendation is that Carter Bankshares, Inc. is a buy.

For further details see:

Carter Bankshares: A Hidden Gem To Fight Inflationary Headwinds