RSG - Casella Waste Systems: Still Not A Buy Despite Attractive Growth And Solid Prospects

2023-03-27 06:56:49 ET

Summary

- Casella Waste Systems continues to post attractive sales, profit, and cash flow growth but has failed to keep up with the broader market.

- This is in spite of the fact that it has solid growth prospects moving forward thanks to capacity issues in the regions in which it operates.

- The long-term picture for the company is positive, but shares aren't yet cheap enough to be bullish over.

One industry that I've always found to be particularly interesting is the waste services industry. I can't quite put my finger on it, but I believe it has something to do with the simplicity of the business, combined with the absolute necessity that the service will be needed no matter what the economy looks like. But I digress. One player that I have been intrigued by in this space in recent years is Casella Waste Systems ( CWST ), a regional, vertically integrated solid waste services company with operations centered around the northeastern US. Over the past few months, returns achieved by shareholders have lagged the broader market. This comes even as financial performance reported by the company has been rather robust. Although shares of the company are too pricey for me to consider a 'buy', I am surprised that the stock is not at least keeping pace with the S&P 500. Despite the priciness of the stock, the firm has a rather appealing catalyst that should continue to benefit the business and its shareholders moving forward.

Recent performance is promising

Back in the middle of October of last year, I found myself questioning whether it made sense for investors to buy shares of Casella Waste Systems or not. Fundamentally, the company had been doing well up until that point, with revenue, profits, and cash flows all rising nicely. I believe that, in the long run, the business would do just fine. However, shares were looking a bit pricey. This ultimately led me to rate the business a 'hold' to reflect my view that shares should generate upside or downside that would more or less match the broader market moving forward. Thus far, the firm has fallen short of my expectations. While the S&P 500 is up 6%, shares of this waste services provider have seen upside of only 1.6%.

{kind=link}

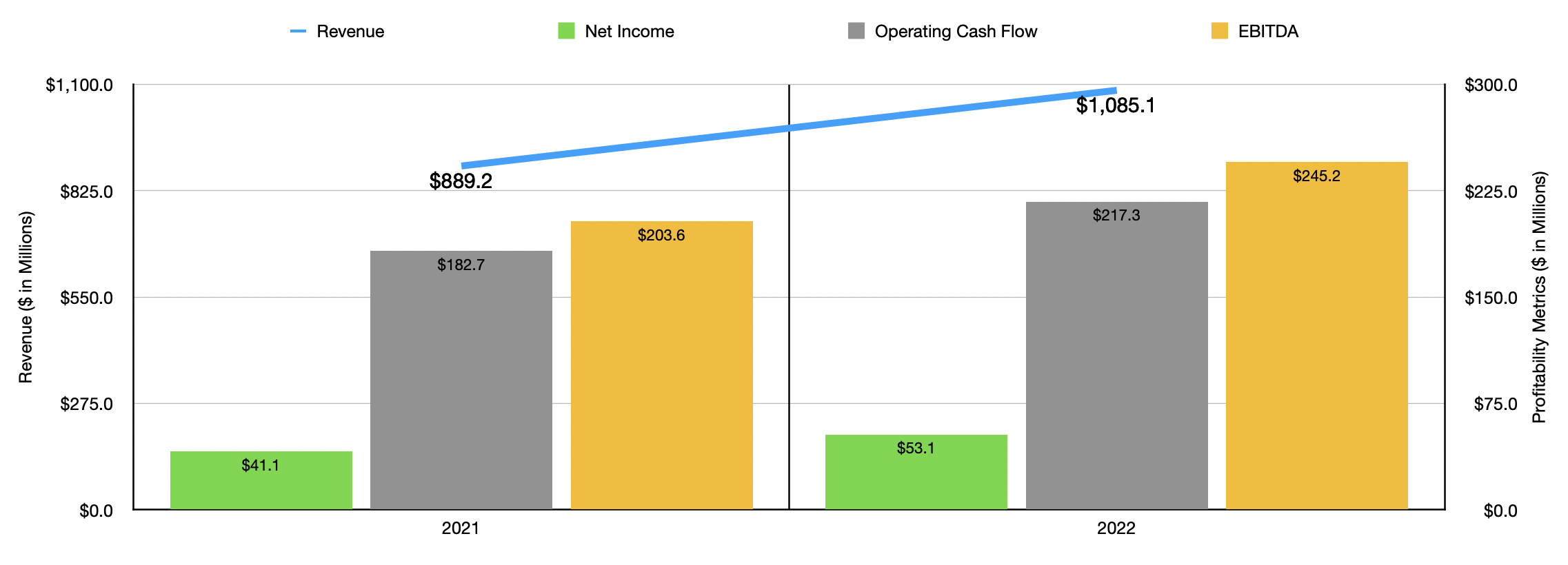

From a purely fundamental perspective, this is a bit perplexing. Financial performance achieved by the company has been quite impressive. For the 2022 fiscal year , for instance, revenue came in at $1.09 billion. That was up 22% compared to the $889.2 million generated in 2021. The greatest growth achieved by the company came from its collection operations. Revenue here spiked 21.9% from $442.7 million to $539.6 million. But other portions of the company also improved nicely. Disposal revenue, for instance, grew 15.7%. Power revenue increased. And processing revenue rose as well. Collectively, these operations make up the solid waste portion of the firm. Acquisition activity accounted for $49.5 million of the $131.1 million in additional revenue this unit received in 2022. Price increases added another $41.7 million in revenue, while surcharges and other fees contributed $32.6 million. The company also benefited from a 27.6% rise in revenue associated with its resource solutions business. On this side of the business, investors benefited to the tune of $42.9 million from acquisition activity and to the tune of $25.9 million from a combination of higher volumes for the firm's customer solutions business, favorable pricing, and increased fees.

{kind=link}

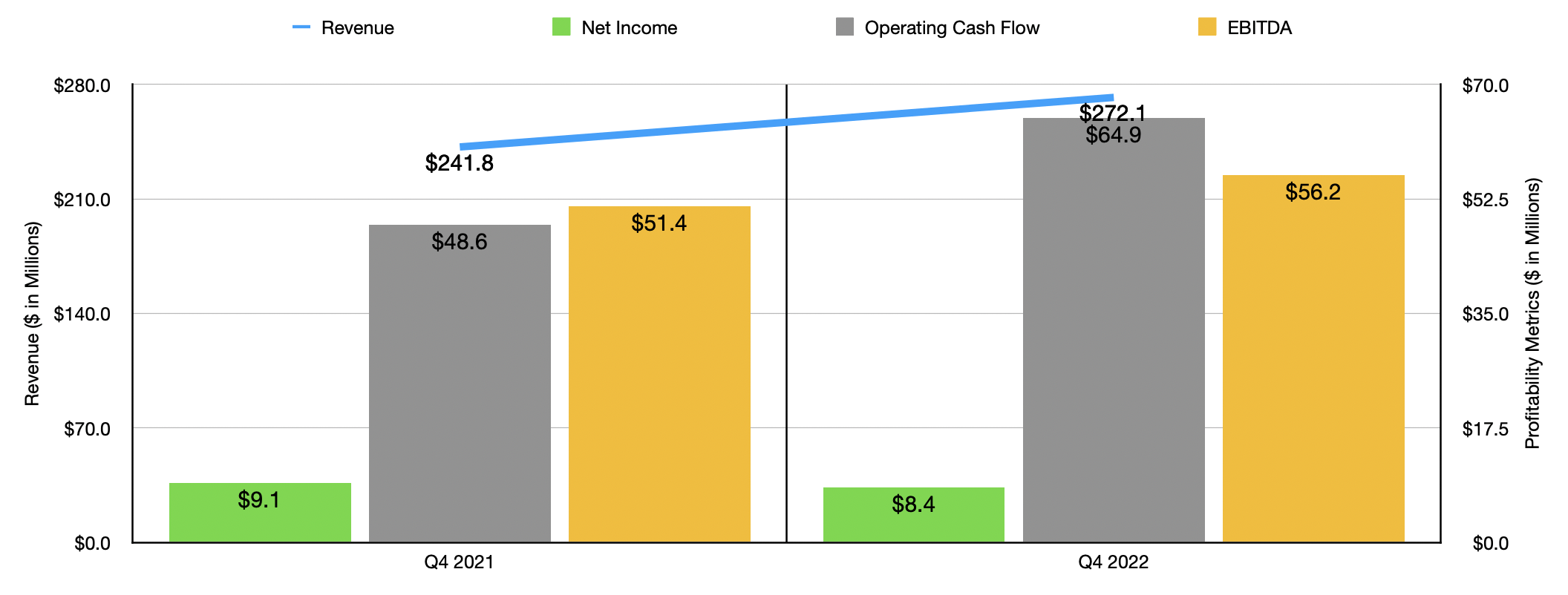

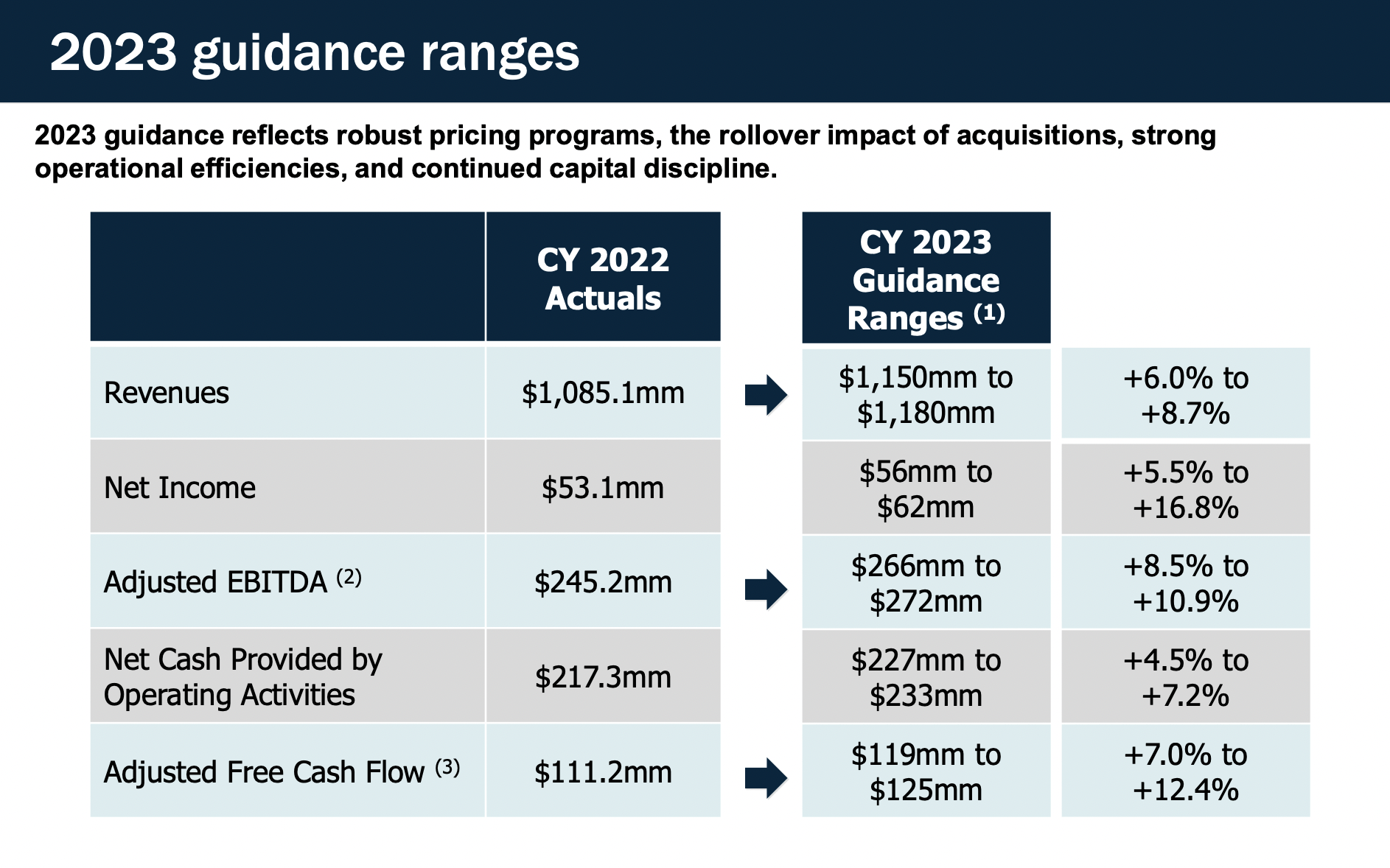

On the bottom line, the company also fared quite well. Net income of $53.1 million beat out the $41.1 million reported one year earlier. Over the same window of time, operating cash flow managed to climb from $182.7 million to $217.3 million. Meanwhile, EBITDA rose from $203.6 million to $245.2 million. As you can see in the chart above, we have not really seen any slowdown in performance improvements as time has gone on. In the fourth quarter of 2022, every one of the metrics I looked at, except for net income, managed to come in stronger than it was one year earlier. And when it comes to 2023, management has some high expectations . They currently expect revenue to total between $1.15 billion and $1.18 billion. At the midpoint, that would represent a 7.4% rise year over year. Management is forecasting net income of between $56 million and $62 million, operating cash flow of between $227 million and $233 million, and EBITDA of between $266 million and $272 million. It's worth noting that the operating cash flow figure should come in strong even in spite of an $11 million hit associated with landfill costs. The revenue increase year over year accounts for $15.5 million in acquired revenue, but has not taken into consideration $30 million in annual revenue that should come from two acquisitions the company has not locked down.

{kind=link}

The future looks solid

The recent past for the company has clearly been positive. In addition to this, 2023 is looking up for the firm. However, I would make the case that financial performance achieved by the company should continue to grow in the years after. This is because the company has not only an impressive operating history, but also a strong catalyst to push growth higher. Driven in part by acquisitions, the firm has seen its revenue climb by about 13% per annum between 2017 and through 2023 if midpoint guidance comes to fruition. This is not to say that organic revenue is not important. For 2024, for instance, as well as the years after, management is forecasting organic revenue growth of between 4.5% and 7%.

{kind=link}

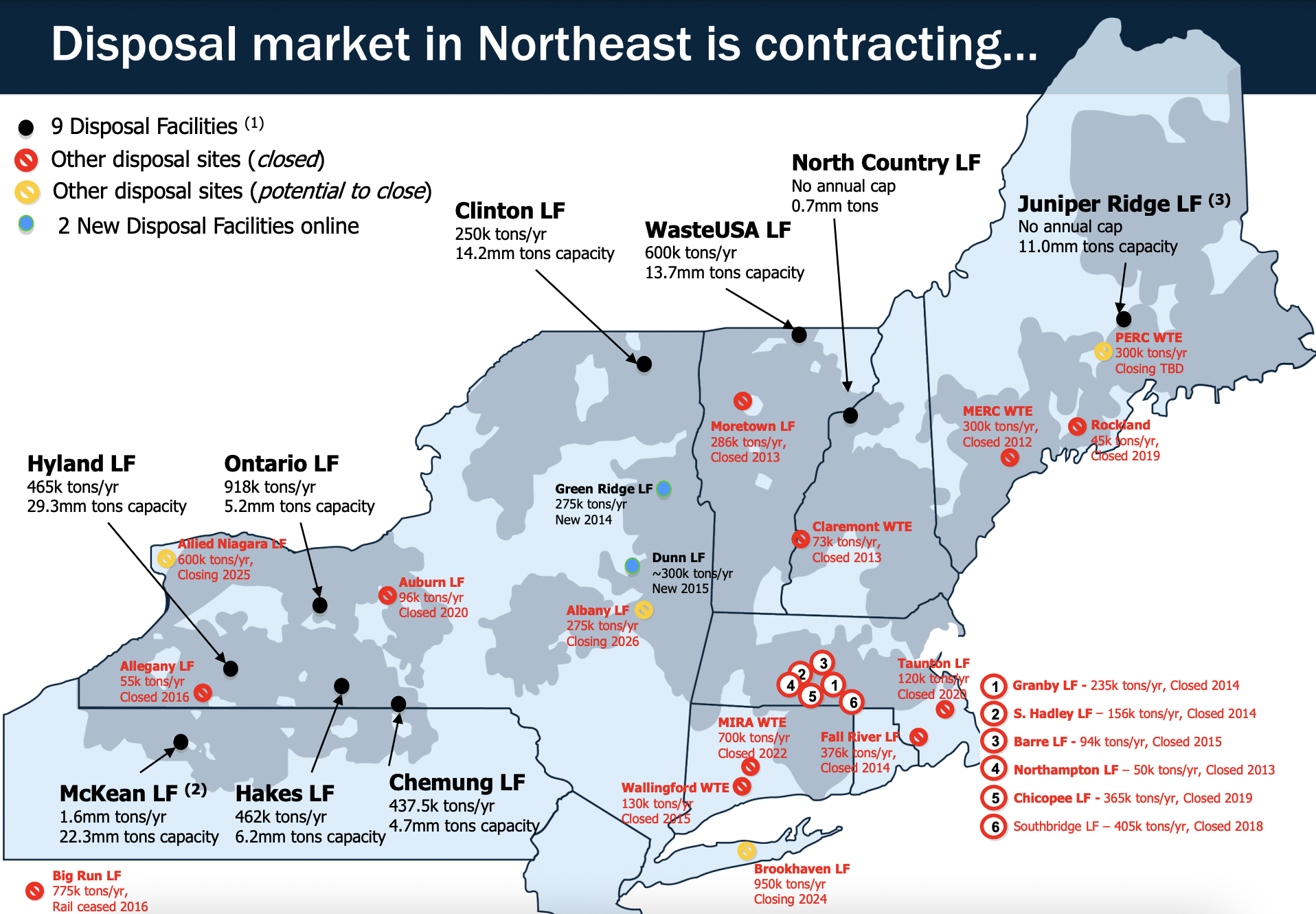

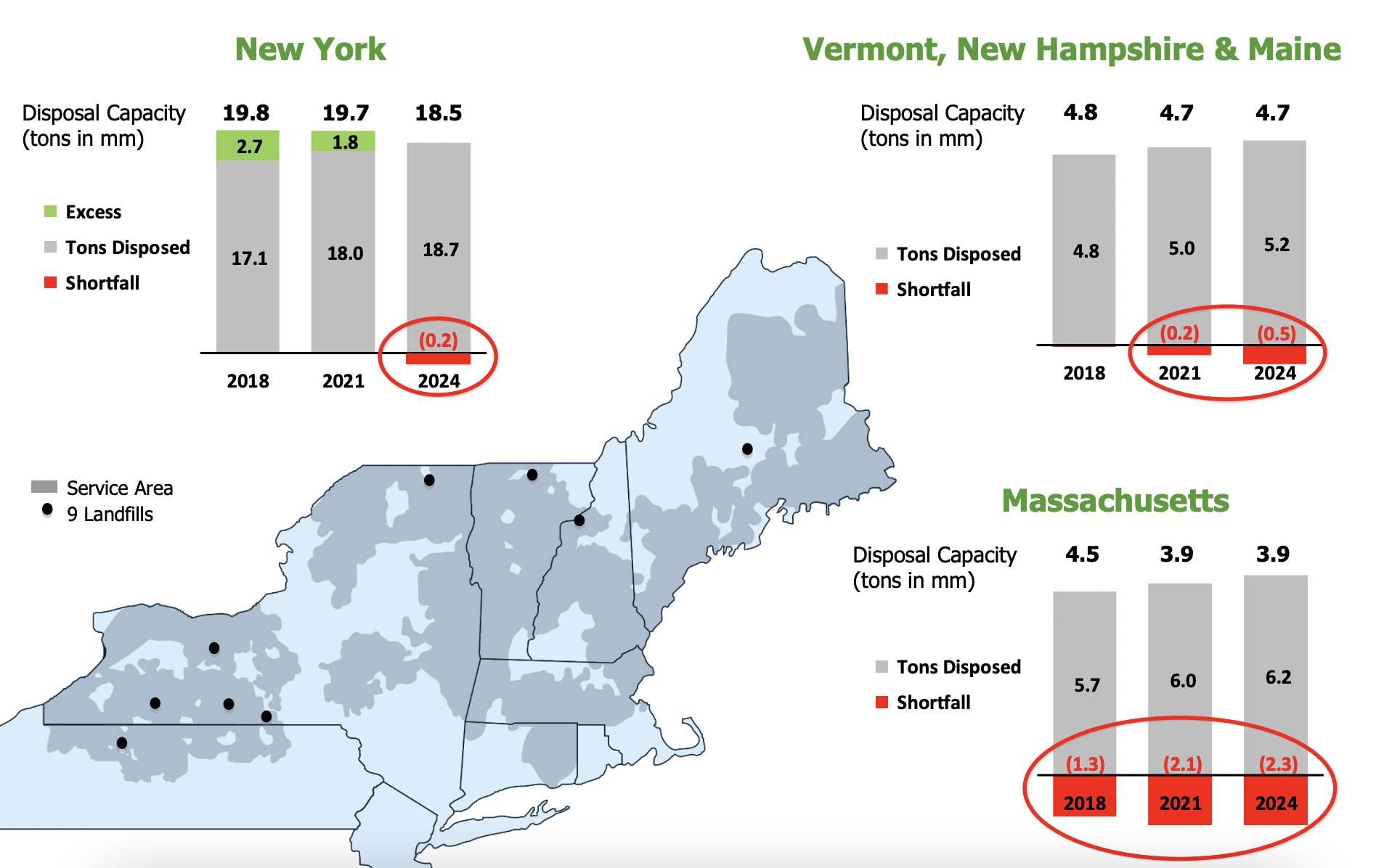

According to the management team at Casella Waste Systems, the waste disposal market in the northeastern portion of the US is contracting. Even though a couple of new disposal facilities have come online, multiple other ones have closed. This has created a shortfall and disposal capacity in many key areas. In New York, for instance, that number for 2024 is estimated to be 0.2 million tons. Between Vermont, New Hampshire, and Maine, that number should climb to 0.5 million tons. But the real pain will be in Massachusetts which, by 2024, will have a shortfall of 2.3 million tons. This should, naturally, allow the companies that do have capacity to charge more for their services.

{kind=link}

That's part of the reason why, in 2022, collection pricing for the company grew by 7% compared to the 3.1% to 5.3% range seen between 2017 and 2021. This should also help grow the demand for the company's resource solutions, thereby allowing it to grow revenue and experience higher margins. For its recycling activities, for instance, the company reported an EBITDA margin of 24.5% in 2022. With the exception of the 2021 fiscal year when that number came in at 29.7%, it was the highest on record. For context, between 2014 and 2020, the margin averaged about 15.1% per year.

{kind=link}

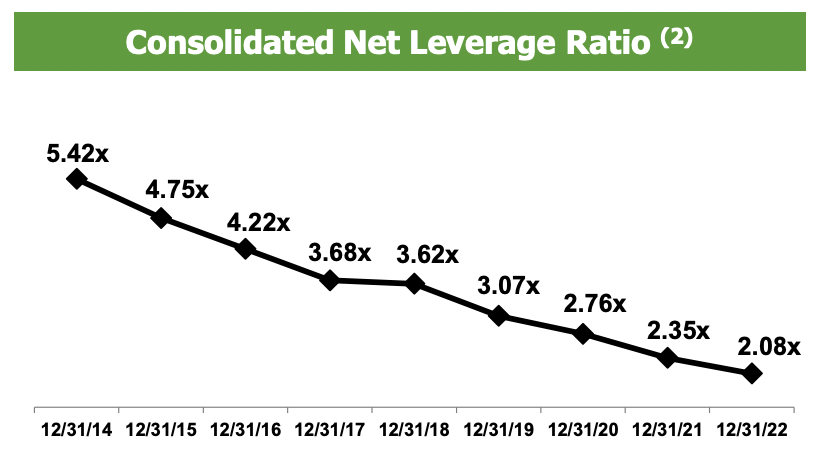

To capitalize on this, the company is targeting various acquisitions. Even after acquiring 14 different properties in 2022 to generate annualized revenue of $51 million, the business claims to have a pipeline totaling $500 million or more in revenue opportunities that it could acquire throughout the northeast. And with the company having a net leverage ratio of 2.08, down from 5.42 back in 2014, it has a tremendous amount of capacity to make acquisitions happen.

{kind=link}

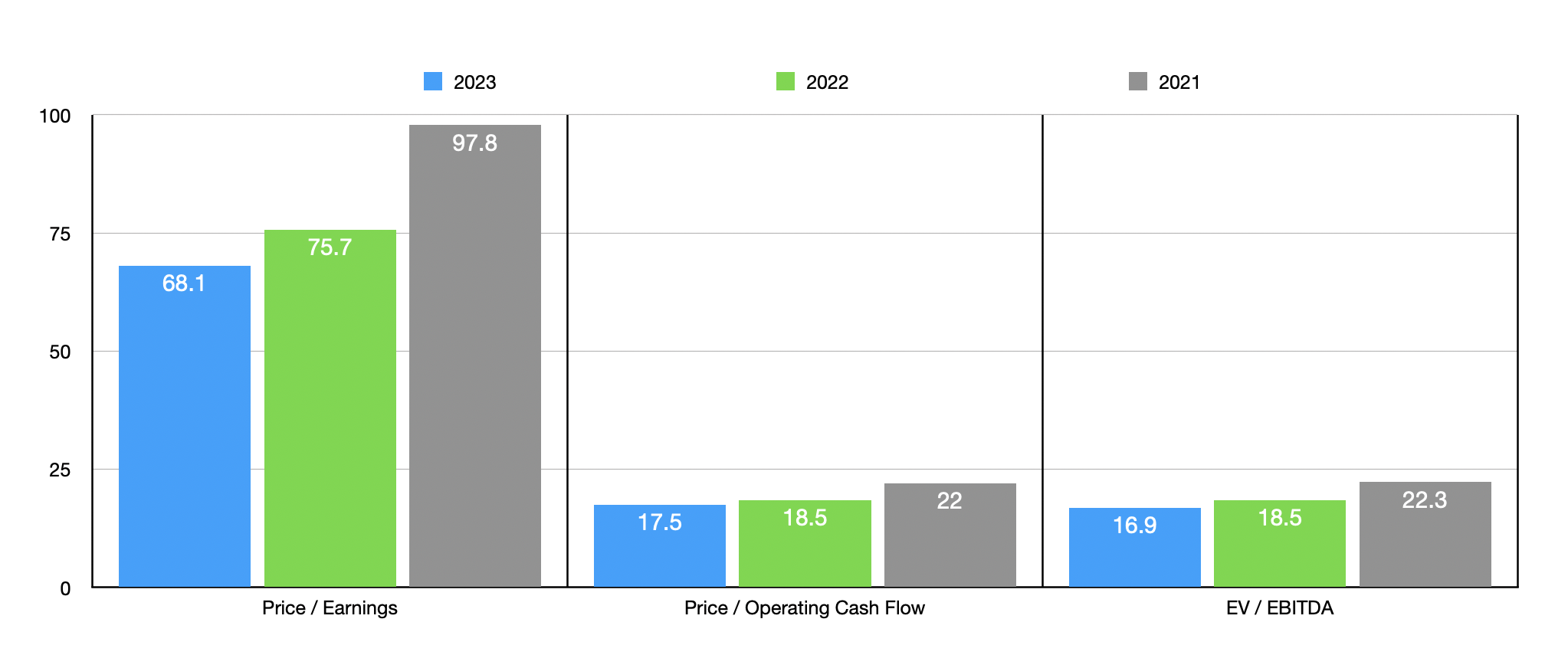

Of course, the price that investors pay is important. Growth is great, but it's only worth so much. Taking the estimates for the 2023 fiscal year and also using data from both 2021 and 2022, I created the chart above. In it, you can see the pricing for the company. As part of my analysis, I also created the table below, which shows how shares are priced compared to five similar businesses. On a price-to-earnings basis, these companies ranged from a low of 15 to a high of 66.9. Using our 2022 figures, I calculated that Casella Waste Systems is the most expensive of the group. Using the price to operating cash flow approach, the range was between 11.4 and 67.1. Two of the five firms were cheaper than our target. And when it comes to the EV to EBITDA approach, we get a range of between 9.1 and 38.7. In this case, four of the five firms were cheaper than our prospect.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Casella Waste Systems |

| 75.7 |

| 18.5 |

| 18.5 |

| Stericycle ( SRCL ) |

| 66.9 |

| 18.8 |

| 13.5 |

| ABM Industries Incorporated ( ABM ) |

| 15.0 |

| 67.1 |

| 9.5 |

| Clean Harbors ( CLH ) |

| 17.3 |

| 11.4 |

| 9.1 |

| Montrose Environmental Group ( MEG ) |

| N/A |

| 48.8 |

| 38.7 |

| Republic Services ( RSG ) |

| 27.7 |

| 12.9 |

| 14.2 |

Takeaway

Operationally speaking, Casella Waste Systems seems to be in really solid shape. The company's recent financial performance has been positive and the firm has an attractive growth catalyst to benefit from. However, the stock does not come cheap. Shares do look a bit pricey, especially from an earnings perspective. The stock is also trading near the high end of the scale relative to similar firms. Due to these factors, I still believe that the company warrants a 'hold' rating at this time.

For further details see:

Casella Waste Systems: Still Not A Buy Despite Attractive Growth And Solid Prospects