CASY - Casey's: Fueling The Engine Of Growth

- Casey’s FY 22 set records in revenue, EPS, and new store additions.

- Casey’s continues to capitalize on its offerings such as private brand products and kitchen prepared meals.

- Casey’s has much room for growth as it is currently only in a third of U.S. states, but it can also grow substantially in the white spaces of its current areas.

- I see a target market value of $205.50 with room to upgrade if headwinds subside.

Casey's General Stores, Inc. (CASY) is a fast growing Fortune 500 company, and it is among the nation's largest convenience store chains. I last wrote about Casey’s here at Seeking Alpha back in February. Since then, the company has released its full year FY 22 results. The year brought strong revenue growth and record EPS. My previous market value target was $195.88, and the market has met that target with a current price as of this writing of about $196.00. My new target for a fair market value is $205.50. I continue to see good long-term potential with Casey’s as they expand their business, but I am factoring in significant consideration for possible headwinds here early in their new FY.

{kind=link}

Source for data, information, and images: Casey’s and Seeking Alpha

FY 22 Results and Growth Progress

Casey’s growth strategy was well evidenced during FY 22. Total revenue was over $12.95 billion, or about 49% higher than FY 21 revenue of just over $8.7 billion. This was largely due to Casey’s biggest year yet for acquisitions, but it may seem a bit more impressive when you consider that only Q4 contained revenue from all three of Casey’s FY 22 acquisitions.

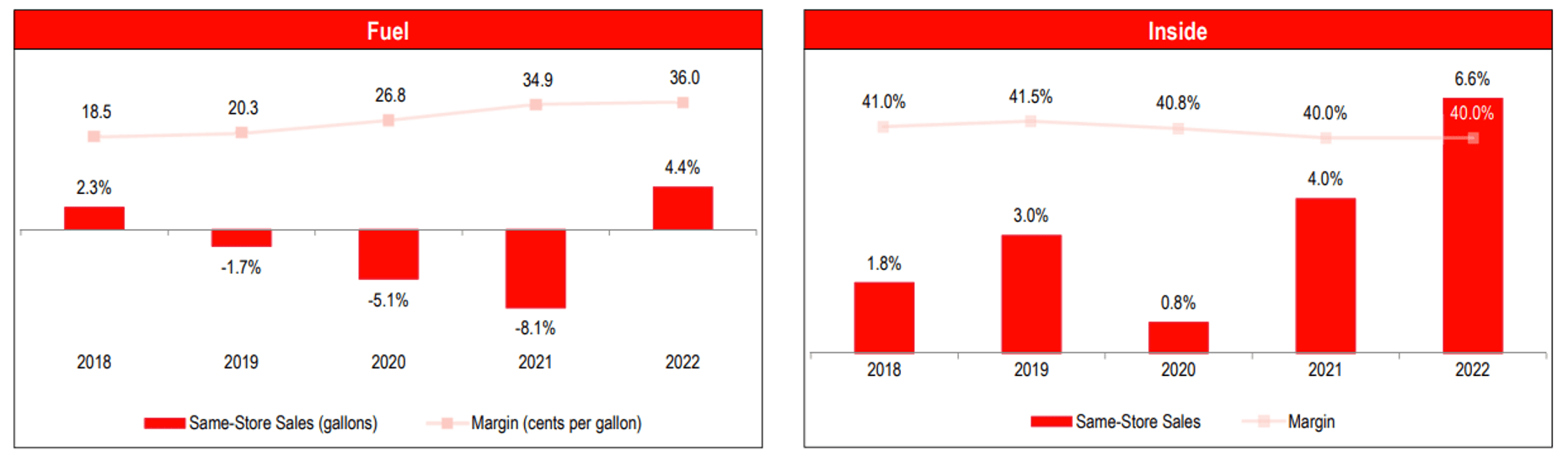

Another contributing factor was achieving a record setting 6.6% increase in same store sales. Casey’s saw strength in fuel sales with good margins, despite unprecedented fuel costs. Inside store sales were also strong with increases in prepared food demand, as well as increased market penetration with Casey’s private label goods.

{kind=link}

As effects of the pandemic continue to manifest in so many ways, Casey’s has been able to adapt and see some positive improvements. The company sees a trend of people returning to work and that appears to be steadily increasing. Higher inflation is here but Casey’s says its products are seen as lower cost items and the kind that customers are less likely to give up even when they are trying to stretch their dollars.

Also, Casey’s points out that their company performed well during the recessionary periods of 2008 and 2014. Those times were before the company had private label products and a rewards program, which should serve to help Casey’s in times of tighter margins. And another recent trend has seen customers typically purchasing a bit less fuel on each visit to the store, which affords more opportunities to sell items to customers inside the store, with each additional visit.

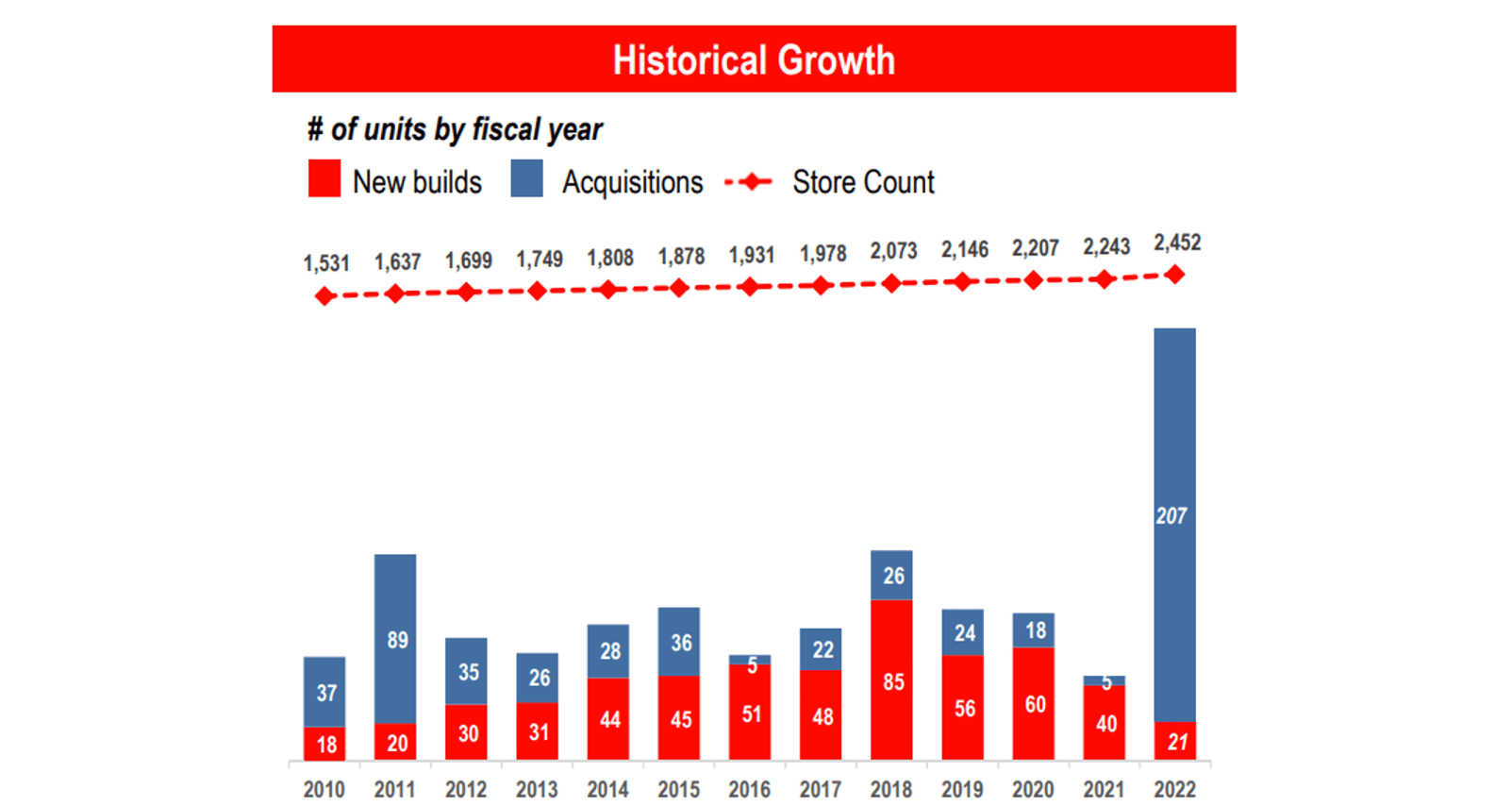

Casey’s apparently saw some excellent opportunities to acquire stores as they closed 3 large acquisitions in FY 22. Together with new builds, the company added 228 new stores in FY 22, which brings the store count to 2,452. This was by far the largest store increase for one year, and most of the mix came from the 3 acquisitions which included 207 stores. The chart below shows historical store growth since 2010.

{kind=link}

While the increased acquisition activity versus new store builds in FY 22 may appear to be a departure from the previous growth plan, it is consistent with Casey’s long-term strategy to focus on whichever option may be the best for any given year. Casey’s continues to pursue new store growth opportunities, but they have recently found that sourcing items such as new equipment has been difficult, while some opportunities arose in acquisition targets. Casey’s believes that their strategy keeps them from overpaying in either method of store growth. For FY 23, the company expects to return to a more typical store growth rate and add about 80 new store units. They are currently projecting a more even mix, or about half new stores and half in acquisitions.

The new stores and large acquisitions require some capital investment, but Casey’s notes its strong free cash flow position of $462 million at the end of FY 22 as evidence that they are positioned well to move forward while preserving their balance sheet. In turn, recent new additions are said to fit well with the Joplin, Missouri distribution center that was added in May of 2021. The proximity of the center will help Casey’s manage costs and the new acquisitions are helping to provide synergies such as a realized $15 million in run rate from the Bucky’s acquisition.

{kind=link}

Casey’s also expects to see positive benefits to gross margin in FY 23 as they continue to add kitchens to the newly acquired stores. In addition, they recently added 700 stores that can deliver beer and hard seltzers with pizza orders.

Casey’s reward program is now 5 million members strong with the addition of 1.3 million members just in the last FY. Likewise, the company has rolled out a new subscription program for their 200-plus car washes, joining the new popular trend for that type of service.

Casey’s private brand program now contains over 250 items with 23 new items introduced in Q4 22 and another 20 items were planned for Q1 23. The company’s private bands are popular as Casey’s informed that a recent private label candy bar was outperforming several popular national brands. Private brands can offer value to customers in times of high inflation and provide better margins for the owner of the brand. Casey’s private brands were capturing about 5% of their grocery and general merchandise category by the end of FY 22. Casey’s expects its private brand goods to capture 6% of that market this year, with a long-term goal of reaching 10% of those sales over the next few years.

Private Label Products (Casey's)

{kind=link}

Valuation

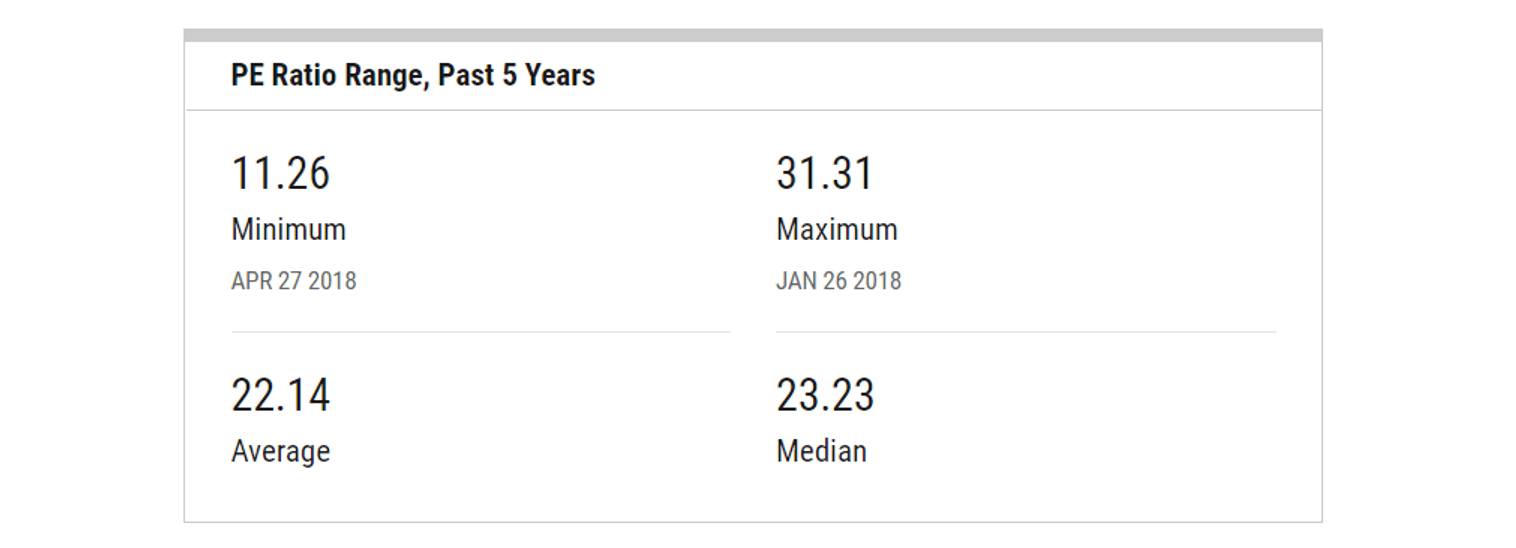

In my last article , my target value for Casey’s was $195.88. I used the then 5-year average P/E, per YCharts of 22.31 and applied it with my guess for FY 22 EPS of $8.78. At the time, Casey’s stock was trading in the market at about $186.00. As of today’s writing, Casey’s stock is trading at about $196.00. That is a significant move-up, but maybe more impressive when considering that many stocks, including typically good performers, are currently trading lower over the first half of this year.

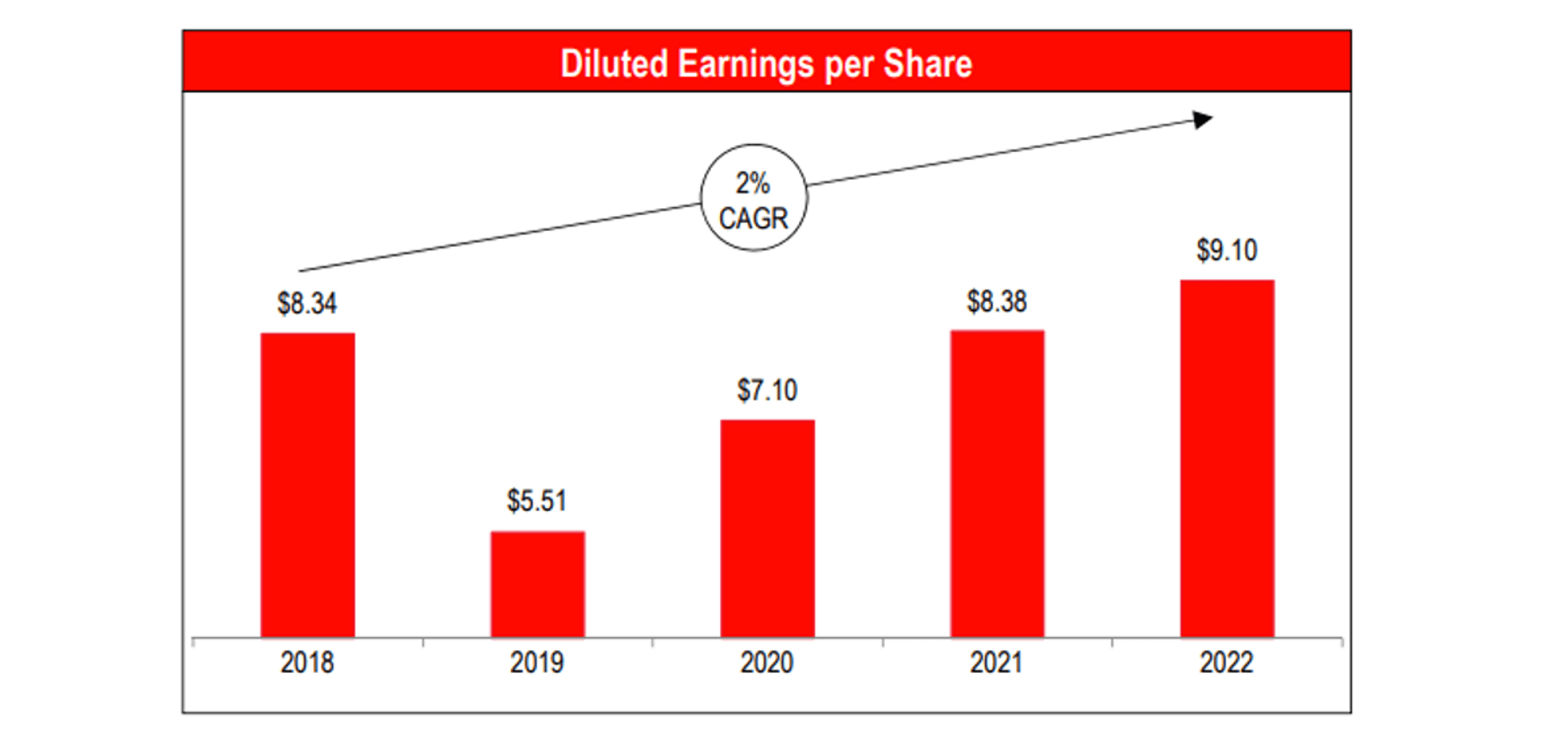

As I mentioned, Casey’s reported an all-time high diluted EPS for FY 22 at $9.10, and that was a bit higher than my guess of $8.78. Also, when I apply the same metrics, I see the current 5-year average P/E from YCharts at 22.14, which is a minor drop from before.

{kind=link}

That would yield an expected market value of $201.47, based on the updated information. But looking into FY 23 there are a few factors to consider. Casey’s expects same store sales to increase 4% to 6%, which is about the same as last year. They expect inside margins to be around 40% and fuel sales to stay flat or grow by 2%. Total operating expenses are expected to increase 9% to 10%. Labor issues are becoming less of a problem, but wage inflation has increased costs. FY 22 EPS was boosted by a one-time tax benefit that set the effective tax rate at 17.8%. For FY 23 the tax rate is expected to be in the 24% to 26% range.

When you combine all these factors with a degree of uncertainty on the prices of goods including fuel, it adds up to some significant possible headwinds that should be considered in guessing on an EPS for FY 23, but it should also be noted that Casey’s expects to see $20 to $25 million saved in the year from synergies gained with the new stores.

I think that until more data becomes available, it may be safer to use a longer-term trend for EPS growth, as seen on the chart below.

{kind=link}

With this information, and early in Casey’s new FY, I will apply a factor of 2% for my guess at EPS growth over the coming year, and I’ll set a fair market target for Casey’s at $205.50. (1.02 x 201.47)

For now, I believe this allows credit for a company that is in rapid growth, while considering current market conditions. Once the Q1 data is available, and with more data that follows, it may be easier to get a better idea whether the target is conservative or optimistic.

Risks

The company provides a full list of risks in its annual filing. I recommend reading that in its entirety, but I will add a few notes.

The most obvious, and perhaps biggest risk for many companies today is the current geopolitical environment. All risks, including market or world events, can lead to share values that do not reflect the thesis of the article.

Casey’s is growing fast, but was last year’s extraordinary pace too fast? It’s a good question, but I expect that the market environment may have led to some good opportunities that a company like Casey’s may have found too good to pass on. Also, the total stores added last year is (a bit) less than 10% of the total and that leaves a lot of established business available to smooth out start-up expenses for the new. In addition, Casey’s new stores are located to take advantage of its newest distribution center, and that should provide substantial cost reduction benefits in supplying those new stores.

I will re-mention from my prior article, that for a longer-term investor, I would give some thought about the macroeconomic environment. Specifically, I am referring to the industry wide transformation from fuels to electric vehicle charging. I think some caution there has merit.

To start, EV charging could mean less stops at a convenience store as perhaps significant charging occurs at home or at other locations. The fuel stop is the life blood and typical primary draw to attract customers. A paramount transition may come, so investors should remain cognizant of the situation.

Having said, we are still likely several years from this perhaps inevitable event. Also, convenience stores, including Casey's are already beginning to offer EV charging services. I expect that eventually customers will pay a fee for the charging that could possibly provide a means for convenience stores to earn more revenue than they do from fuel, in theory.

{kind=link}

Another thought on this is that currently EV charging takes longer than fueling, which may create more of a draw for a customer to come inside the store and buy things or grab a meal while they wait.

Final Thoughts

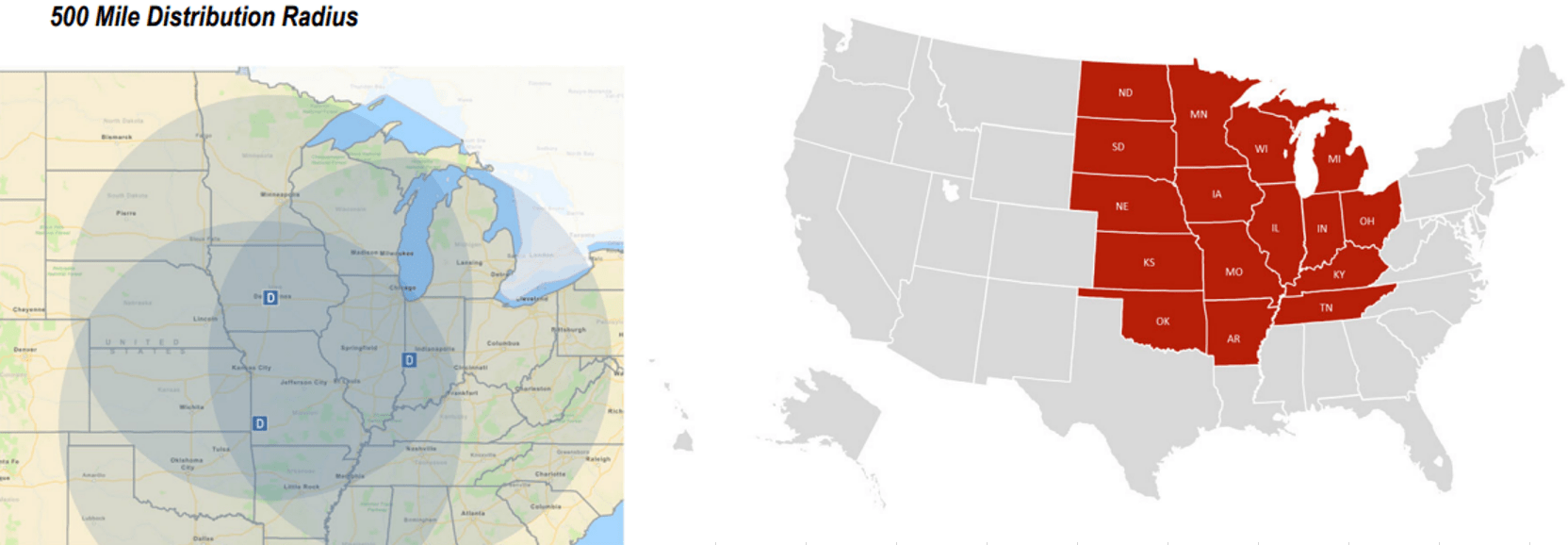

Investors may often lament that they “missed out” on a great opportunity to invest in a company before its growth rate and stock price matured. You can’t say Casey’s is just getting started, but they have lots of room to grow both within the 16 states where they already exist and in the 32 remaining contiguous U.S. states. In the longer-term Casey’s has ample opportunity to grow its business, and thus brings the opportunity for the share price to continue to follow that trend.

And if only you see Casey’s as just 2,400 plus “quick-stops” you may not see them in the same vision as they do. The experience may start with the automobile, but it appears that Casey’s sees its stores as not only as a fuel and EV charging center but as a car wash center, a general store that includes a growing assortment of private label products, and a restaurant as well that comes complete with online ordering. Then throw in a credit card service to go with all that. Their visions beyond simply being a “quick-stop” may explain why their footprint is growing so rapidly.

Casey’s still has $400 million available in its share re-purchase program, but no repurchase were made in the fourth quarter. Perhaps the opportunities to invest were seen as the best use of capital. However, the company did prepay $168 million in debt, and they raised the dividend again at their June meeting. The dividend amount was set at $.38 a share, marking the 23 rd consecutive yearly increase. As Casey’s grows it continues to reward its shareholders.

{kind=link}

Doesn’t everyone want a little more piece of the pie?

For further details see:

Casey's: Fueling The Engine Of Growth