CASY - Casey's General Stores: Despite New All Time Highs Still A Buy

2024-01-16 04:48:18 ET

Summary

- Casey's General Stores is the third largest convenience store chain in the US and the fifth largest pizza chain.

- The company's focus on smaller towns allows for cheaper operations and establishes brand loyalty.

- Casey's has experienced strong growth in revenue and EBITDA, driven by its acquisition strategy and private label products.

- While there are some risks related to fuel margins contracting near term, shares look attractive at the current valuation.

Company Overview

As you can probably tell from the name, Casey's General Stores ( CASY ) is an operator of convenience stores. With over 2500 locations across 17 different states, the company is the third largest convenience store chain in the United States and the fifth largest pizza chain in the U.S.

{kind=link}

Investment Thesis

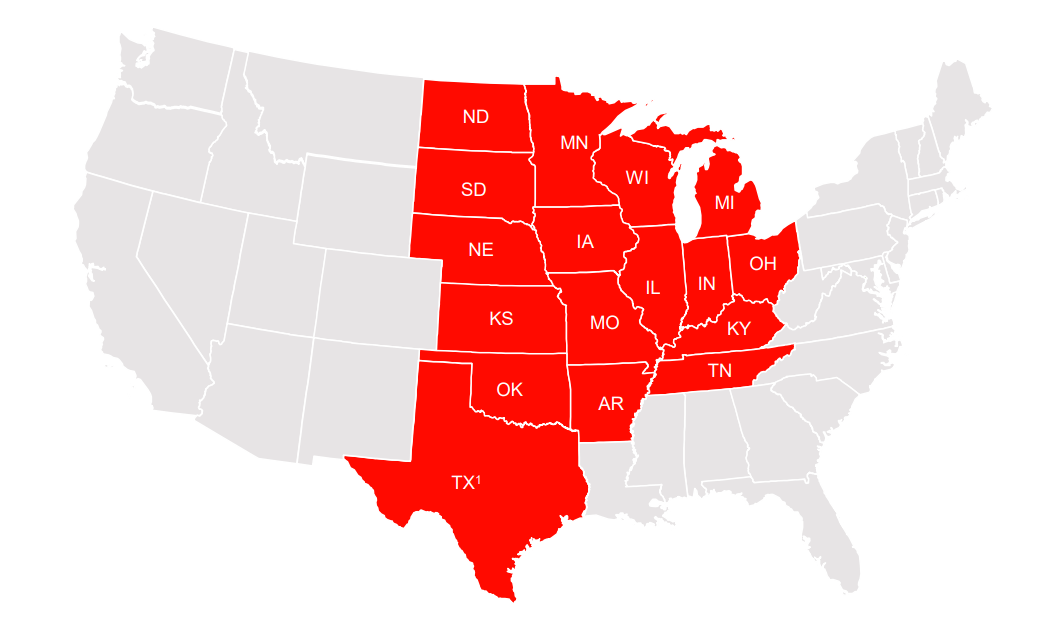

Casey's General Stores is unique in the sense that it operates mostly in the midwestern United States like Ohio, Michigan, Indiana, Wisconsin, Illinois, Minnesota, Iowa, Missouri, North Dakota, South Dakota, Nebraska, and Kansas. Importantly, it primarily serves towns with fewer than 5,000 people. About half of its stores fit that criteria. This is an advantage for the company in that these locations are cheaper to build out as well as acquire and operate.

It also has the advantage that since there's often less retail options, Casey's General Store's becomes a place where customers can buy things outside of what may be conventional items at a convenience store compared to a typical location in an urban area, for example. Operating in smaller towns also has the advantage of being the primary store in the area which leads to familiarity by the residents and customers who live in the community. Being rooted in the communities it serves also establishes brand loyalty and repeat business.

One of the things that first impressed me about Casey's General Stores has been its share price outperformance over time. When looking at the chart below, we can see that the company has returned a 330.5% return for shareholders over the last 10 years, compared to the S&P500's return on 159.7%.

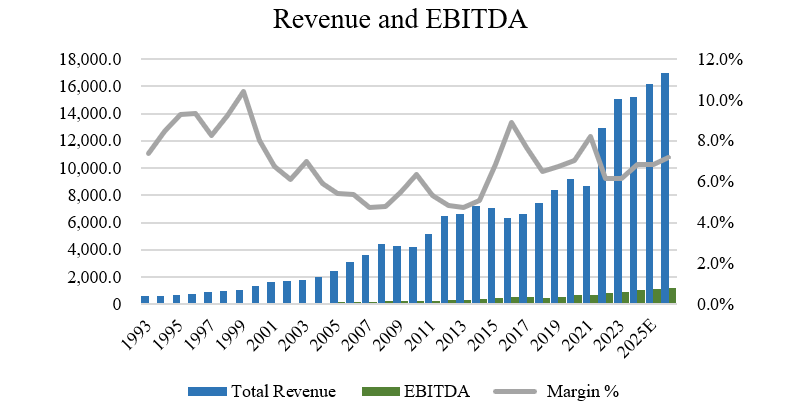

This outperformance has been driven by strong growth in revenue and EBITDA, which have grown at a CAGR of 9.6% and 15.9%, respectively, over the last decade. Over the last 20 years, since 2003, revenue and EBITDA have compounded at 23.0% and 19.7%, illustrating that the company has been able to put up consistent increases in both sales and earnings over the long-term.

Revenue and EBITDA Growth (Author, based on data from S&P Capital IQ)

{kind=link}

In my view, part of the reason for this excellent growth over the last few decades have been directly as a result of the company's acquisition strategy.

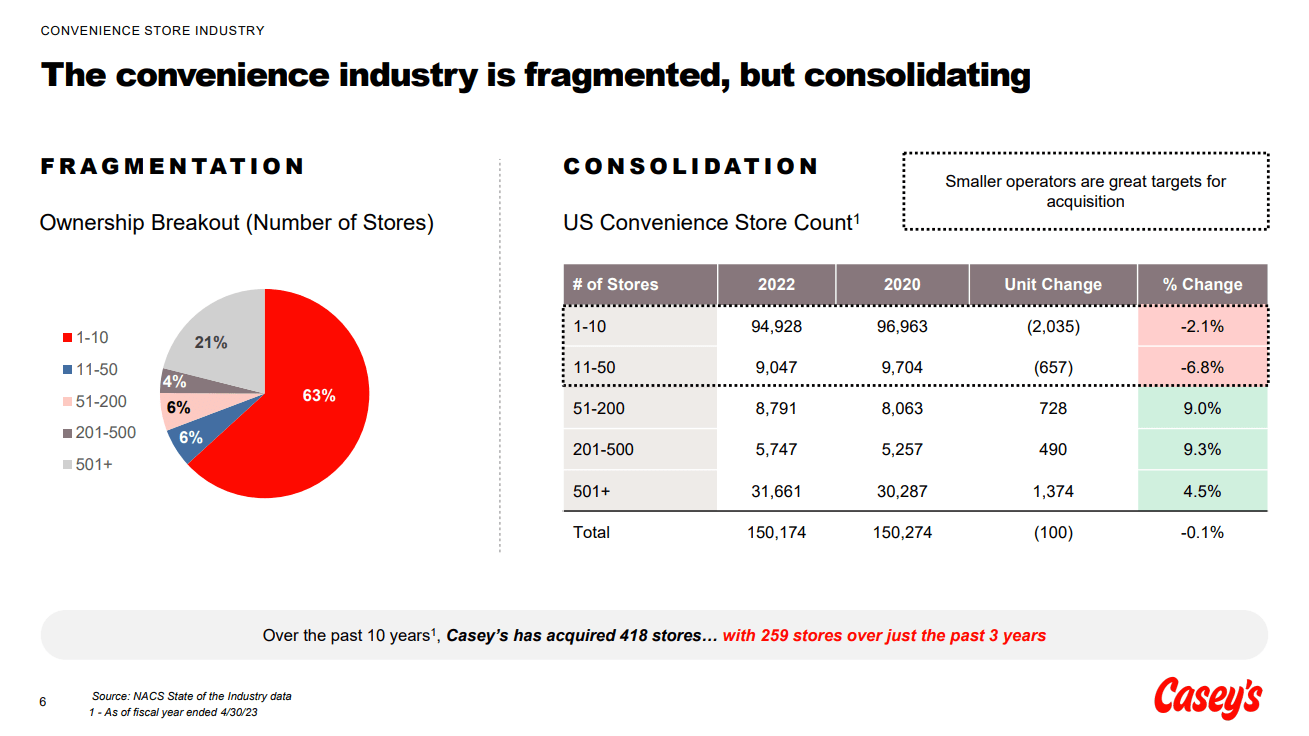

The convenience store industry is a highly fragmented market. There's only a few major players , like 7-Elleven and Alimentation Couche-Tard ( ATD:CA ) who are first and second largest players and have thousands of stores. With consolidation being a major theme in the industry, as larger operators can achieve economies of scale and optimize supply chains, this has made smaller convenience stores very attractive targets to buy. In the last decade, Casey’s has acquired 418 store with 259 of these being acquired in just the last three years.

{kind=link}

Like Casey's General Stores, while both 7-Elleven and Couche-Tard have put up fantastic growth in store count over the years, part of the reason I like the way Casey's is strategically positioned is due to the fact that they are now focusing more on convenience stores and less on fuel. As selling fuel is a lower margin business, Casey's focuses less on fuel with around 75% of inside transactions not including fuel.

One thing that seems to be true for Casey's is that higher fuel margins look like they might be here to stay. On the company's earnings call for the quarter, we did see same-store gallons flat with fuel margins clocking in at $0.423 per gallon, so it seems like Casey's is still benefitting off of higher margins despite natural gas, ethanol, and overall fuel prices coming down over the last year. While I don't have a view on where margins go from here or if they contract, especially given the cyclical nature of commodities, it's still important to note as the company is benefitting from higher free cash flows on this front in the short-term. If we did see higher fuel margins over the medium and long-term, then I would see this as gravy on top.

Another key differentiator I view as important is the company's private label. As is true for major grocery chains, private label is important for convenience stores like Casey's as they provide a value alternative for guests and also help to build brand loyalty. With around 350 SKUs at Casey's being margin accretive, it has about 120 SKUs that are unique to Casey’s.

From the company's most recent quarter , we can also see this has been a source of growth for the company. On the earnings call, management discussed how private label continues to outperform. For example, in potato chips, despite national brands growing nicely by 10% with 2% positive unit growth, private label is completely blowing it out of the water with 38% growth (33% unit growth).

What I think this highlights is two things. The first is that private label is doing extremely well, providing customers with a value alternative that they can't get elsewhere. The second point, and perhaps more importantly in my view, is that there isn't so much of a risk of cannibalization of sales from one product to another. This is very important to note because in many cases the private label products are manufactured by the companies who also manufacture the national brands products. So there isn't a risk of a national brand pulling product away from Casey's because the private label outperforms national brands growth. The national brands benefit either way.

Finally, an exciting part of the business growth here that I don't think the market is paying attention to is the delivery capabilities Casey's will have going forward. With ordering food online becoming increasingly popular as a result of the rise of DoorDash ( DASH ) and Uber Eats ( UBER ), Casey's is now offering delivery in about 10% of stores (around 250 stores).

With around 80% of guests agreeing “Casey’s is a good value for the money", I wouldn't be surprised to see deliveries act as a source for organic growth going forward. If they're successful in the 10% of stores they're in now, it wouldn't be far-fetched to think that they could easily up that number pretty quickly. Right now, delivery is a mix of the delivery is being done themselves with the rest being third-party companies, so Casey's doesn't see labor issues with respect to getting drivers. Using third-party companies is also great as Casey's pay per delivery which doesn't require a company-employed driver to be waiting around for the next delivery.

Valuation

Based on the 9 sell-side analysts with one-year target prices on Casey's General Stores stock, the average target price is $302.56, with a high estimate of $340.00 and a low estimate of $263.00. From the current price to the average price this implies about 5.5% upside potential one-year out. This suggests analysts are moderately optimistic on the company's near-term outlook.

Even with the new 52-week highs Casey's General Stores stock is making, the company's valuation seems very reasonable at 11.8x EV/EBITDA. With the historical valuation range being between 8.3x EBITDA and 13.8x EBITDA, the valuation is slightly on the high side but by no means is it an egregious valuation. Price to earnings also looks reasonable at around 22.2x earnings, compared with the overall market (S&P 500) PE ratio at around 26.0x earnings. For a company that has grown faster than the overall market, the lower valuation provides some comfort.

When comparing Casey's General Stores to its peers, like Alimentation Couche-Tard, Murphy USA ( MUSA ), Arko Corp. ( ARKO ) and Parkland Corp. ( PKI:CA ), these companies have EV/EBITDA ratios of 11.1x, 9.4x, 8.0x, and 7.6x, respectively, so Casey's General Stores is above the peer group at 11.8x. With a better 10-year growth CAGR in revenue of 9.6%, nearly double that of the peer group, the valuation seems justified.

With fiscal 2024 EBITDA growth guidance in the 8% to 10% range, I expect the company can likely maintain its growth rates, at least in the near term. Furthermore, a great balance sheet and strong free cash flow should also allow for share repurchases in the near future.

Risks

When it comes to risks, one of the ones to consider would be Casey's General Stores' growth by acquisition strategy not working out in the future. However, the company has had a track record of successfully integrating acquisitions and the balance sheet looks well-positioned to finance the company's future growth. With Net Debt to EBITDA of 1.6x and a Debt to Equity Ratio of 0.57x, the company has modest leverage and has capacity to take on additional debt to fund its M&A strategy. It's also noteworthy to point out that these ratios are the lowest they've ever been in the last ten years.

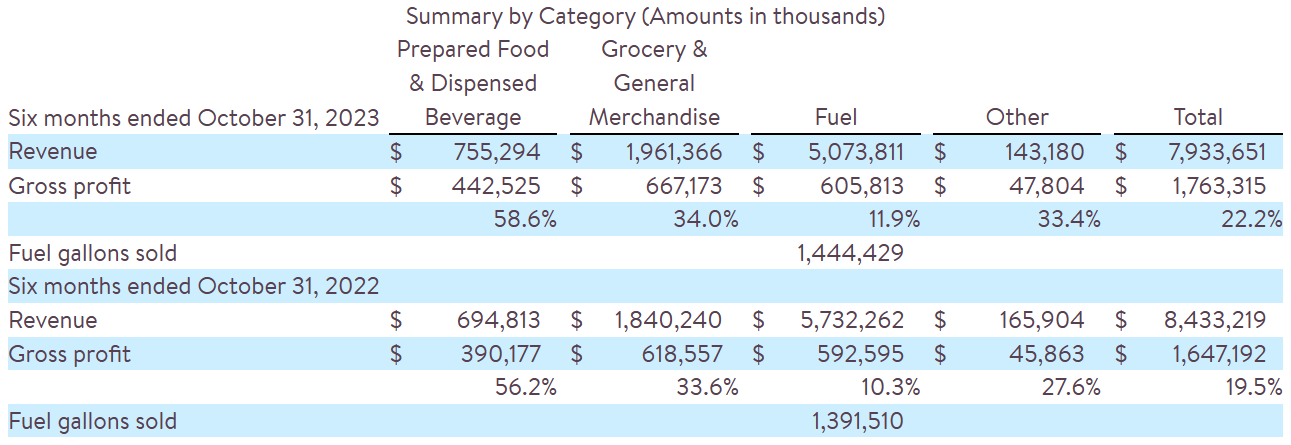

Another key risk to monitor would be the revenues derived from fuel sales. As shown by the graph below, a fairly large portion of the company's revenues come from fuel sales and is the second largest contributor by segment to gross profit. We've mentioned that fuel margins are slightly elevated compared to historical levels (and have remained that way for a while now) but if margins were to decline as a result of unforeseen movements in the price of fuel, then that could hurt Casey's profitability.

{kind=link}

Finally, with more EV vehicles making up a larger percentage of cars on the road, this leaves Casey exposed to risks as fuel consumption from cars on the road may drop in the future. While Casey's might be less exposed to this risk as they operate in the midwestern United States and focus on communities where they can be the primary convenience store in the town, this is still a risk to consider. In addition, while Casey's could start to offer charging stations for EVs at their locations, they've shown no indication to do so on the last few earnings calls or in their investor presentation.

Conclusion

In summary, I think Casey's General Stores could be a great defensive name to add to your portfolio if you're looking for steady growth. The company has proven itself to be a disciplined consolidator in the convenience store space with strong growth in sales and EBITDA over the last few decades. Trading above the peer group and at a slight premium to its historical average, I think the valuation is still pretty fair when we consider the company's growth prospects going forward and that the company's balance sheet has never looked better. For these reasons, I rate shares as a 'buy'.

For further details see:

Casey's General Stores: Despite New All Time Highs, Still A Buy