CASY - Casey's General Stores: Growth Ahead But At Fair Value

2023-07-29 04:33:49 ET

Summary

- Casey's General Stores has experienced significant growth in revenue and free cash flow over the past five years.

- The company's expansion of store locations has contributed to its revenue and cash flow growth.

- Casey's strong brand and private label products have driven profitability, but the outlook for 2024 is challenging due to increased operating expenses and potential labor market pressures.

Intro

Casey's General Stores, Inc. (CASY) and its subsidiaries operate convenience stores under the names Casey's and Casey's General Stores. These stores offer a wide range of products, including freshly prepared foods like pizza, donuts, and sandwiches, as well as beverages, tobacco, health and beauty aids, automotive products, and other non-food items. They also provide self-service motor fuel, including gasoline and diesel, along with various other products such as soft drinks, snacks, ice cream, and pet supplies.

In this analysis, we will closely evaluate CASY financial performance and growth prospects. We'll delve into the company's revenue, profitability, and cash flow generation capabilities. By gaining insights into these essential aspects, investors can make a more informed assessment of CASY's potential as a favorable investment in the current market.

Growth

Over the last five years, CASY has experienced significant growth in both revenue and free cash flow. From 2019 to 2023, the company's revenue increased by 61.38%, with a compounded annual growth rate ((CAGR)) of 10.05%.

Data by Stock Analysis

Similarly, the free cash flow saw substantial growth, rising by 199.68% over the same period, with a CAGR of 24.55%. These positive trends indicate a strong performance for CASY and demonstrate its ability to generate increasing revenue and cash flow over time.

Data by Stock Analysis

CASY's remarkable revenue and free cash flow growth can be directly attributed to its rapid store expansion over the years. In 2017, the company operated 1,978 stores, but since then, it has aggressively expanded its footprint and currently boasts an impressive store count of 2,521. This substantial increase in the number of stores has significantly bolstered CASY's revenue generation, as it allowed the company to tap into new markets, reach a broader customer base, and drive higher sales volumes.

Moreover, the expanding store network has also contributed to improved operational efficiencies, cost optimization, and economies of scale, resulting in a robust increase in free cash flow. CASY's strategic emphasis on store growth has proven to be a pivotal driver of its financial success, solidifying its position as a thriving and dynamic player in the retail industry.

Profitability

CASY's consistently high return on equity (ROE) with a remarkable ten-year average of 18.53% is a testament to the company's adept management and efficient capital utilization. This impressive performance indicates that CASY has been effectively generating substantial profits in relation to shareholders' equity, showcasing its ability to create value and deliver strong returns to its investors over the long term.

Data by Stock Analysis

This outstanding record of profitability can be attributed to CASY's strong brand. The power of Casey's brand is exemplified through their private label product offering. With over 250 Casey's-branded items, these products have achieved a 5% share of Casey's Grocery and General Merchandise category.

CASY's does have an ambitious goal of achieving 10% which it is making strong progress towards. We believe CASY's will achieve this goal, because their Casey's-branded products stand out for their exceptional quality and value, making them a compelling choice, particularly amidst the challenges of inflationary times.

Outlook

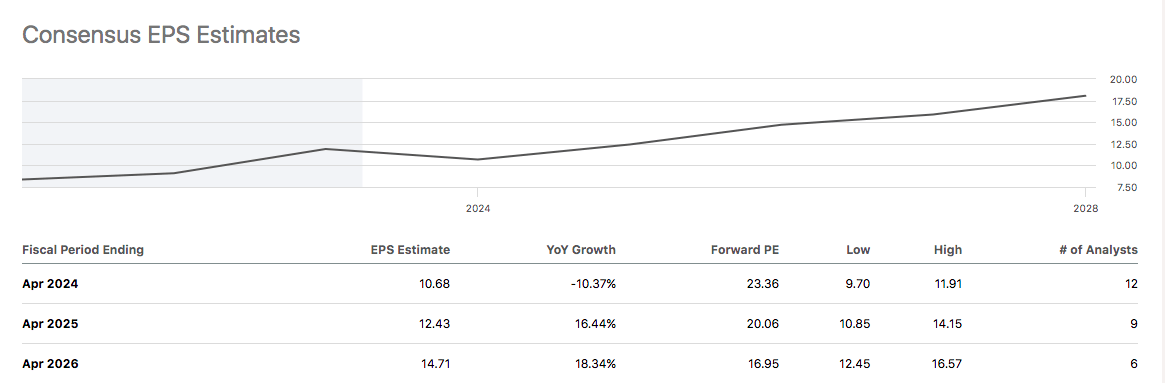

CASY's outlook for 2024 appears to be gloomy, with projected earnings per share ((EPS)) estimate of $10.74 indicates a worrisome decline of 9.84% compared to the previous year. Similarly, the revenue estimate of $14.8 billion for April 2024 reflects a discouraging YoY growth rate of -1.63%. These figures can be attributed to management guiding a 5-7% increase in operating expenses next year.

Similarly, CASY's operating expenses increased 8.1% in fiscal 2023, highlighting an alarming trend. Factors such as new stores (3%), same-store operations (2%), credit card fees (1%), and variable incentive compensation (1%) contributed to the increase. Employee expenses remained flat despite wage rate increases due to a 2% reduction in same-store labor hours. Wages and related costs constitute the majority of all operating expenses.

With more than 43,000 employees scattered across 2500+ stores, three distribution centers, a fleet of 340 grocery and fuel trucks, we believe CASY's largest risk is its exposure to the labor markets. The company incurs labor costs for employee wages, overtime pay, and statutory benefits, etc. Any significant increase in wages, overtime pay, or mandated benefits, such as healthcare or paid time off, would lead to higher labor costs which could significantly impact the business. An example of this would be recent state-mandated minimum wage hikes, combined with labor market shortages and wage pressures, all of which have notably increased the company's operating expenses, impacting its overall profitability.

Amidst the challenges posed by the labor market across various sectors, CASY is proactively addressing the issue by investing in the attraction and retention of its team members. The company has undertaken several recruitment and development initiatives to bolster its workforce. For instance, Casey's organized 'Here For Good' hiring events throughout all its stores, aiming to attract new candidates and fill positions, particularly in preparation for the busy summer season. Additionally, the company introduced retention incentives in specific areas, such as for truck drivers, to ensure operational efficiency, timely deliveries, and well-stocked stores.

One of the company's strategies for returning to growth will be investing in digital technologies. CASY has prioritized enhancing the guest experience by investing in digital capabilities, fostering a modern and digitally-enabled environment. With over 65 percent of pizza orders now received through web or mobile app platforms, the company demonstrated its commitment to convenience and accessibility for customers.

Moreover, the expansion of online ordering options extended beyond pizza, enabling guests to order over 500 grocery and snack items online. Additionally, the company expanded third-party delivery services and maintained curbside service, further solidifying its dedication to providing a seamless and convenient experience for all its guests.

We believe CASY has several key factors working in its favor for future growth. The company possesses a robust brand, an ambitious store growth strategy, and continuous investments in its people and technology. These factors are expected to drive the business forward for years to come. Analysts also share this optimistic outlook, predicting substantial growth for CASY throughout 2025 and 2026.

{kind=link}

Valuation

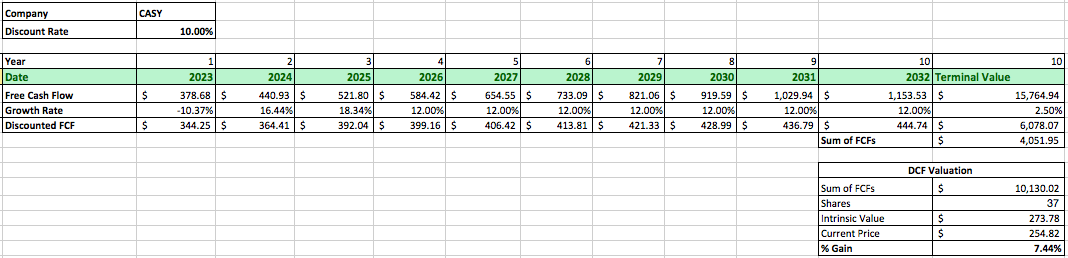

To determine CASY's intrinsic value, we will utilize the discounted cash flow ((DCF)) analysis. Starting with CASY's initial free cash flow of $422.49 million, we'll apply an initial growth rate of -10.37% for 2023, followed by growth rates of 16.44% for 2024 and 18.34% for 2025, based on the average analyst estimates of CASY's revenue growth over the next few years.

For the subsequent period, we usually use the average of the revenue and free cash flow compounded annual growth rate over the past ten years however in the case of CASY their historical growth rate is 26.97% which we don't believe is possible for the company to maintain. Therefore, we will cap the growth rate at 12% and use this growth rate for years 4 to 10.

Using a discount rate of 10%, based on the average return of the market with dividends reinvested, and a conservative perpetual growth rate of 2.5%, we calculate CASY's intrinsic value to be $273.78 million. This suggests that CASY might be currently priced at fair value, presenting investors with neither a potential return nor loss compared to the company's current market price.

{kind=link}

Takeaway

Over the past few years, CASY has demonstrated substantial growth in revenue and free cash flow, attributed to an aggressive store expansion strategy and a strong brand. However, the outlook for 2024 appears challenging, with projected declines in EPS and revenue, primarily due to increased operating expenses and potential labor market pressures.

Despite the potential risks associated with labor costs, CASY is actively investing in recruitment and retention initiatives to address the challenge. Additionally, the company is embracing digital technologies to enhance the customer experience, positioning itself for future growth.

Considering the discounted cash flow analysis, CASY's current valuation suggests it may be priced at fair value. For the time being, investors might consider holding the stock, but careful monitoring of labor market conditions and operating expenses is advisable to assess the company's future performance.

For further details see:

Casey's General Stores: Growth Ahead But At Fair Value