BALY - Casino REITs: Winners Of Blackstone Distress

2023-04-20 10:00:00 ET

Summary

- A success story of the "Modern REIT Era," Casino REITs have been the best-performing property sector since their emergence in the mid-2010s, honing the competitive advantages of the public REIT model.

- Casino REITs were the lone property sector to finish in positive territory in 2022, benefiting from their attractive “inflation-hedging” lease structure, strength in Las Vegas travel demand, and broader institutional acceptance.

- Fittingly, Casino REITs - exemplars in shareholder-friendly governance - have been beneficiaries of distress felt across the darker underbelly of the real estate industry, including Blackstone’s non-traded REIT ("NTR") platform.

- Increasingly desperate to raise capital to meet redemptions - a function of its overstated self-reported NAV valuation - Blackstone's NTR sold its $5.5B stake in two Vegas casinos last December to VICI, and we predict the Bellagio and Cosmopolitan are likely next.

- Access to longer-term fixed-rate capital has proven to be a significant competitive advantage for public REITs. These REITs' impressive track record in capital deployment and shareholder-friendly governance justifies our willingness to “pay up” at moderately elevated multiples.

REIT Rankings: Casino & Gaming

This is an abridged version of the full report and rankings published on Hoya Capital Income Builder Marketplace on April 19th.

{kind=link}

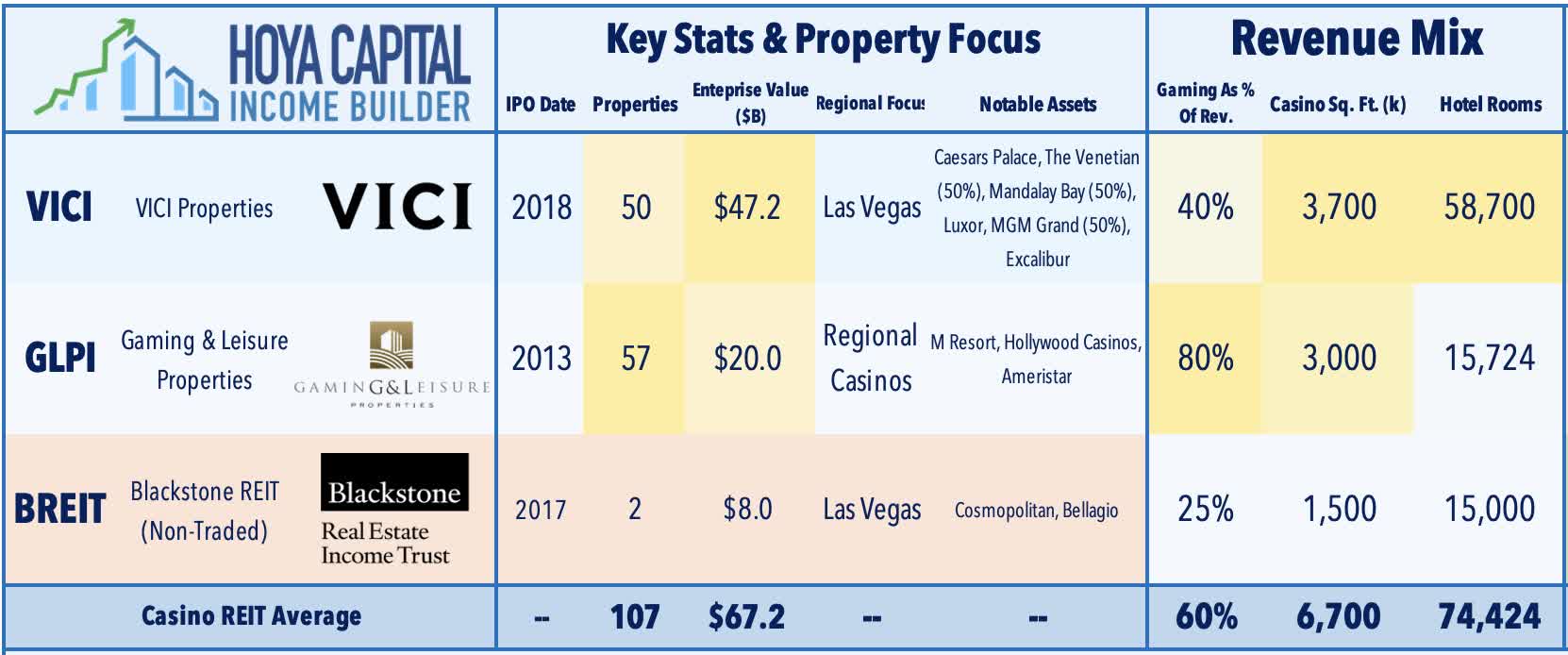

One of several success stories of the "Modern REIT Era" alongside other outperforming entrants, including Single-Family Rentals, Cell Towers, and Data centers, Casino REITs have been the single-best-performing property sector since their emergence in the mid-2010s, honing the competitive advantages of the public REIT model with precision. Within the Hoya Capital Casino REIT Index, we track the two casino REITs: VICI Properties ( VICI ) - which owns a dominant share of the Las Vegas casino market, and G aming and Leisure Properties ( GLPI ) - which owns the largest portfolio of regional casinos. These two casino REITs together account for $46B in market value and own 100 casinos and entertainment facilities across the United States.

{kind=link}

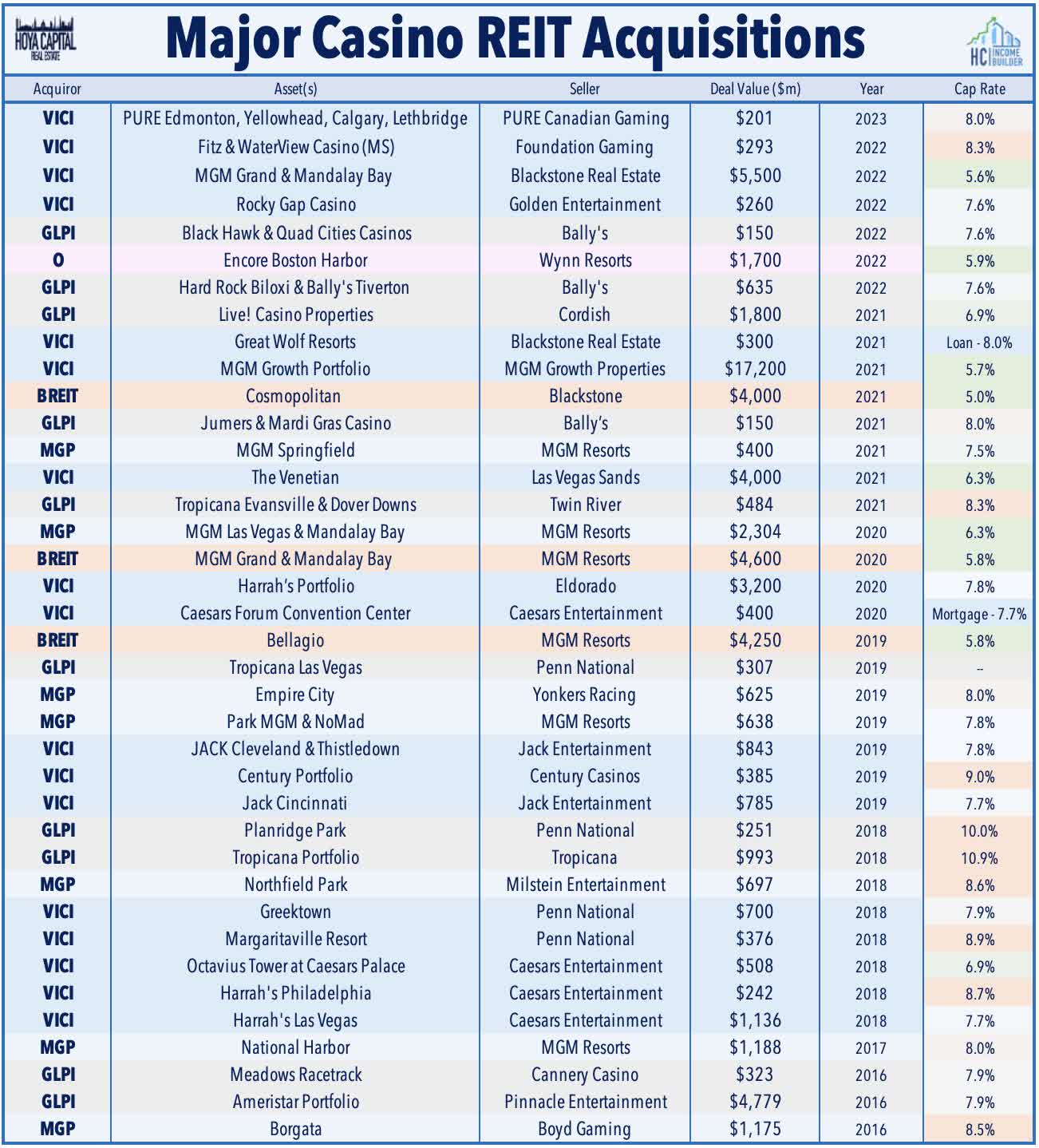

The best-performing property sector last year, Casino REITs have continued their impressive run of performance, benefiting from broader institutional investor acceptance and an upward valuation re-rating, which in turn has given these REITs the capital "firepower" to rapidly consolidate the casino industry. Casino REITs now command a dominant share of the U.S. casino real estate ownership market. These two Casino REITs have acquired roughly $60 billion in assets since the start of 2016, including VICI's acquisition of former REIT MGM Growth Properties and its purchase of The Venetian from Las Vegas Sands in 2021, along with its deals to acquire the MGM Grand and Mandalay Bay from Blackstone ( BX ) in 2022. As we bid farewell to one REIT, another player emerged onto the casino scene last year with Realty Income ( O ) - the largest net lease REIT - acquiring Encore Boston Harbor from Wynn Resorts and indicating that it will be an active player in the casino business.

{kind=link}

Emerging in the mid-2010s, casino REITs had seemingly been flying under the radar over the past several years despite delivering steady and consistent outperformance and high-single-digit FFO growth fueled by this continued wave of accretive acquisitions and industry consolidation. Much like their retail-focused net lease REIT peers, external growth through acquisitions is the modus operandi of the casino REIT sector, and while casino REITs now own more than a third of the total "investment-grade" casinos in the United States, recent deals and management commentary indicate that the acquisition environment remains active and should continue to provide a steady source of FFO growth for the foreseeable future given these REITs' relatively favorable cost of capital and unique competitive positioning. Summing up the consolidation potential, VICI recently commented that it plans to “capitalize on the fact that we have capital when a lot of other people don’t.”

{kind=link}

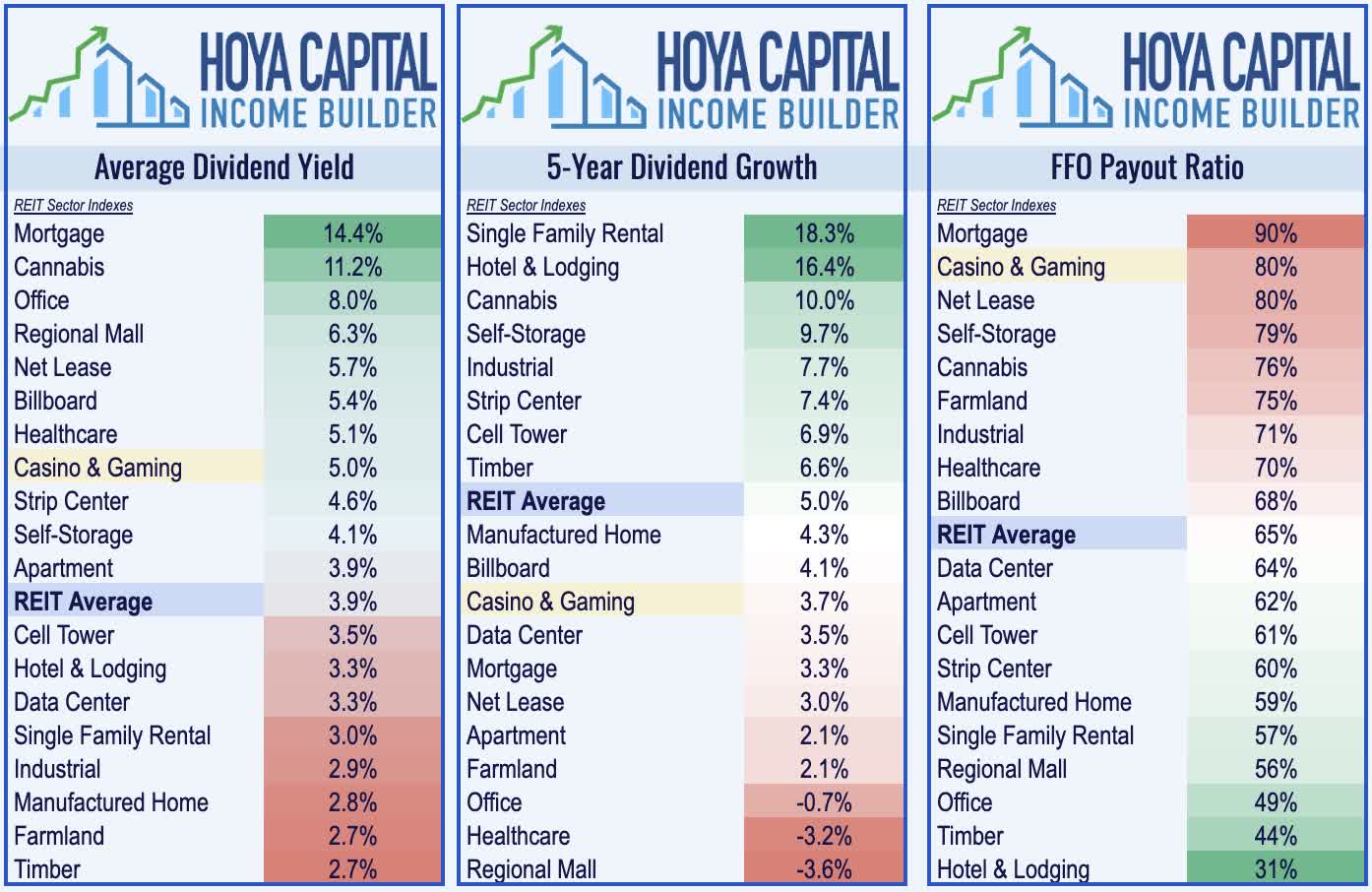

Blending some of the better attributes from each of the net lease, hotel, and healthcare REIT sectors, casino REITs emerged in a fashion similar to many lodging REITs as "spinoffs" designed to separate the capital-intensive real estate business from the operationally-intensive property management business. Casino REITs now own 100 of the roughly 250-300 "investment grade" commercial casinos in the United States, one of the highest concentrations of REIT ownership within any property sector. With an average dividend yield of around 5%, we've long viewed casino REITs as a more compelling - and perhaps "under the radar" - alternative to other seemingly "cheap" sectors facing stiffer secular headwinds. Like their net lease peers, casino REITs are some of the most operationally efficient property sectors, operating with Adjusted NOI margins of nearly 90%, leaving most of the financial risk and capital expenditure responsibilities to their tenants.

{kind=link}

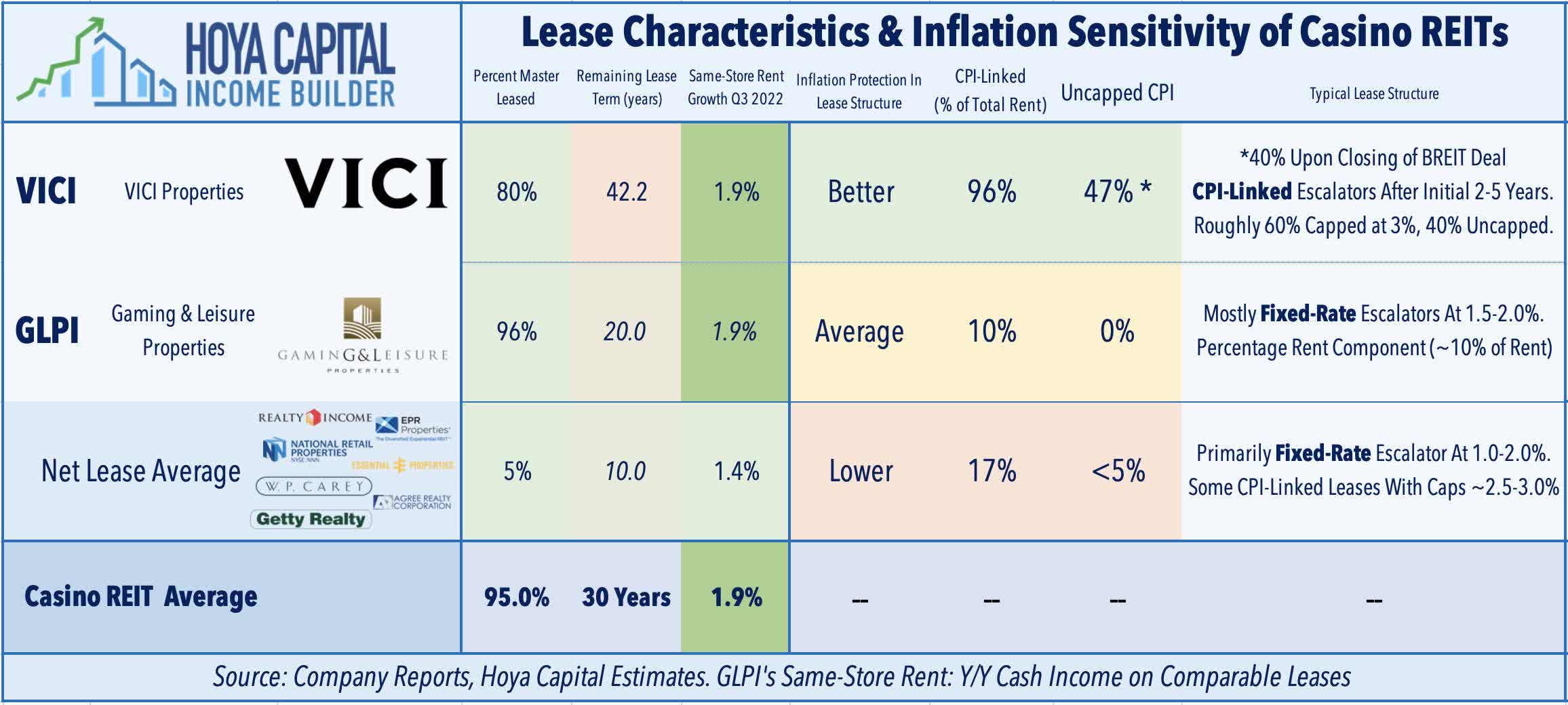

Despite their ultra-long-term triple net lease structures, casino REITs are better protected from inflation than many initially presumed. Inflation sensitivity is driven by several interacting factors, including external growth potential, lease structure, and term, tenant credit quality, and the cyclicality of the underlying property type. VICI Properties boasts inflation-linked escalators on 96% of its leases – and, importantly - 40% of its leases use uncapped CPI for the annual escalation formula. Gaming & Leisure's inflation protection, by comparison, is less direct with few explicit CPI linkages - but most of its leases do include a percentage rent component – roughly 10-15% of its cash rental income – along with the 1.5%-2.0% escalator that is generally tied to rent coverage ratio thresholds - which together result in a pro-cyclical dimension to its cash flow stream.

{kind=link}

Benefiting From Blackstone's Distress

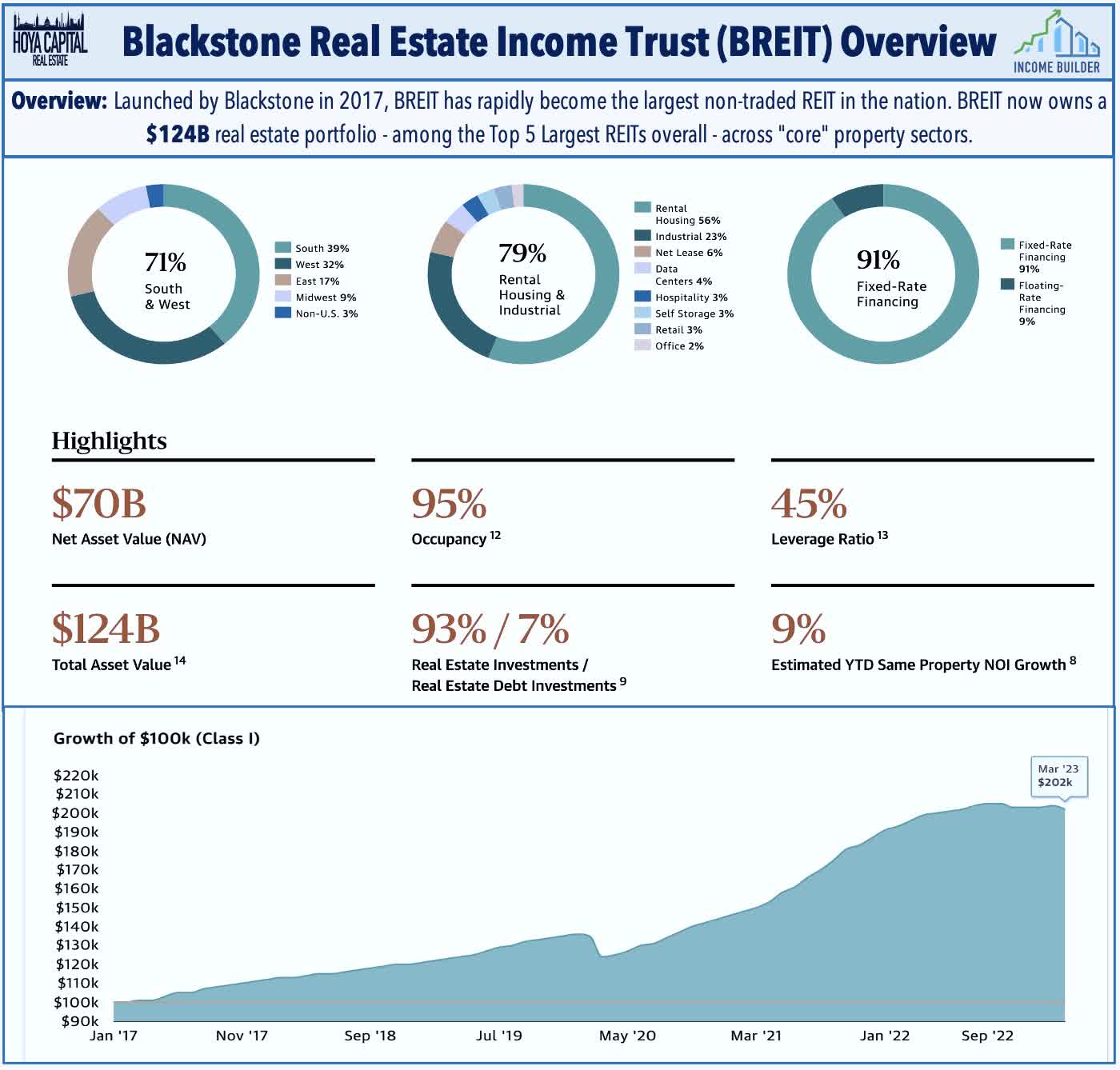

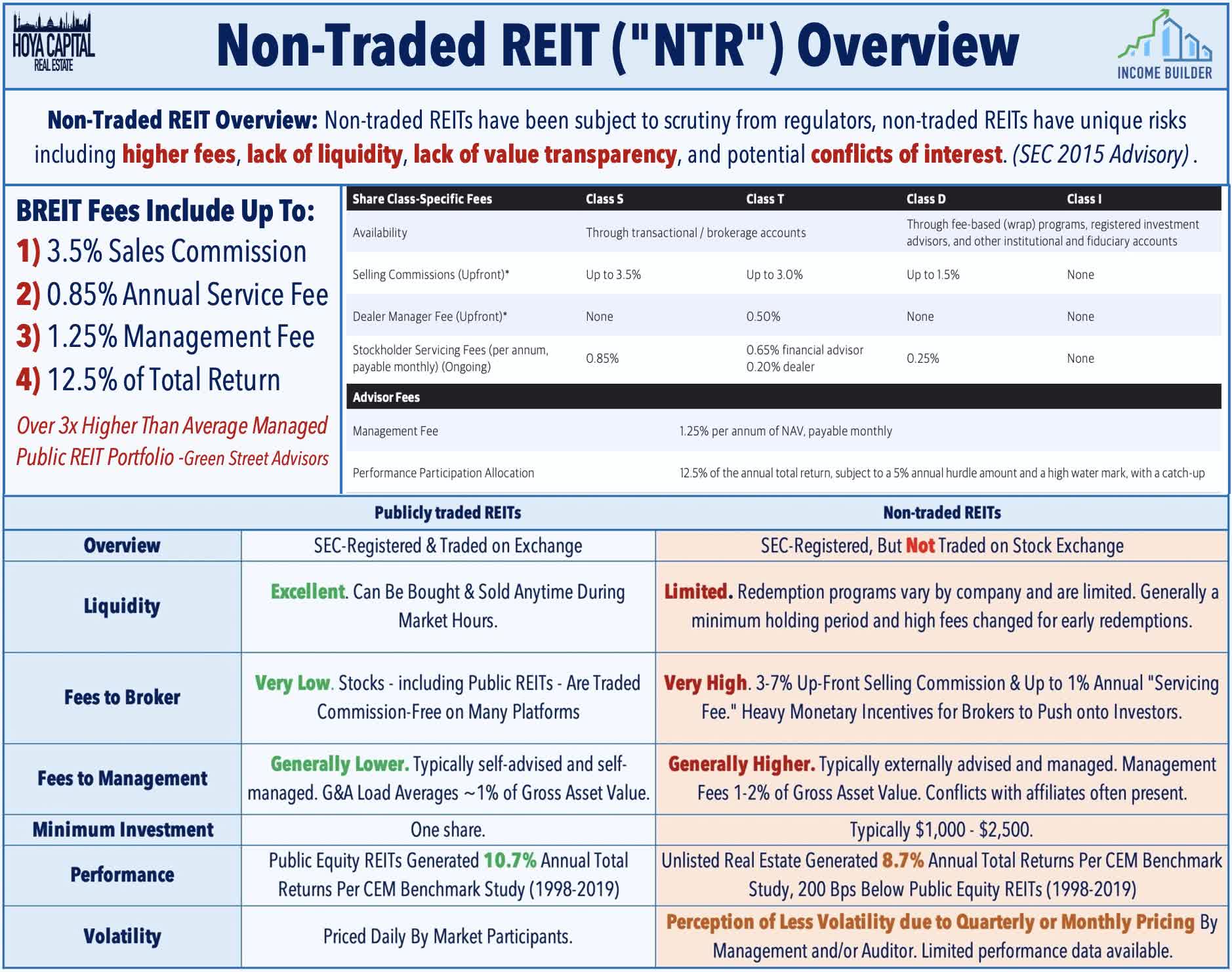

Fittingly, Casino REITs - exemplars in shareholder-friendly governance - have been beneficiaries of recent distress felt across the darker underbelly of the real estate industry, including Blackstone’s non-traded REIT ("NTR") platform colloquially as BREIT , which has been forced to limit investor redemptions after facing a wave of requests that exceeded its liquidity thresholds. BREIT fulfilled just 15% of withdrawal requests in March, down from 35% in February and 25% in January. BREIT - which internally determines its Net Asset Value ("NAV") monthly, which is the rate at which sales are sold or redeemed - claims to have generated a positive 8.4% net return in 2022 during which time publicly-traded equity REITs were lower by 26% and private market commercial real estate valuations declined 13.2%, per estimates from Green Street Advisors. The Chilton REIT Team published a must-read report earlier this month, which estimated that BREIT's actual NAV "is approximately 55% lower than BREIT’s stated NAV as of December 31, 2022." Naturally, investors have seized on the opportunity to redeem shares at these premium NAV valuations, and outflows are likely to continue until this valuation gap narrows.

{kind=link}

Chilton refers to the NTR valuation process as "mark to magic" - a play on the "mark to market" fair value accounting methodology and concludes that "BREIT would be trading at 65% to 75% less than its current price if it were public today." The report also highlights that BREIT's investors pay relatively exorbitant fees compared to those incurred through public REIT investments, noting that BREIT paid Blackstone over $1.5B in fees in 2022, which equates to 1.1% of gross assets, which is more than double that of average public REIT. We've discussed the risks of NTR space across many reports over the past half-decade and continue to watch the area for signs of increased stress given their typically-high leverage and sensitivity to investor fund flows - which we expect will become an area that's "ripe for picking" for public REITs. Starwood, KKR, and Ares also run sizable NTR platforms that have also been forced to limit investor redemptions in recent months.

{kind=link}

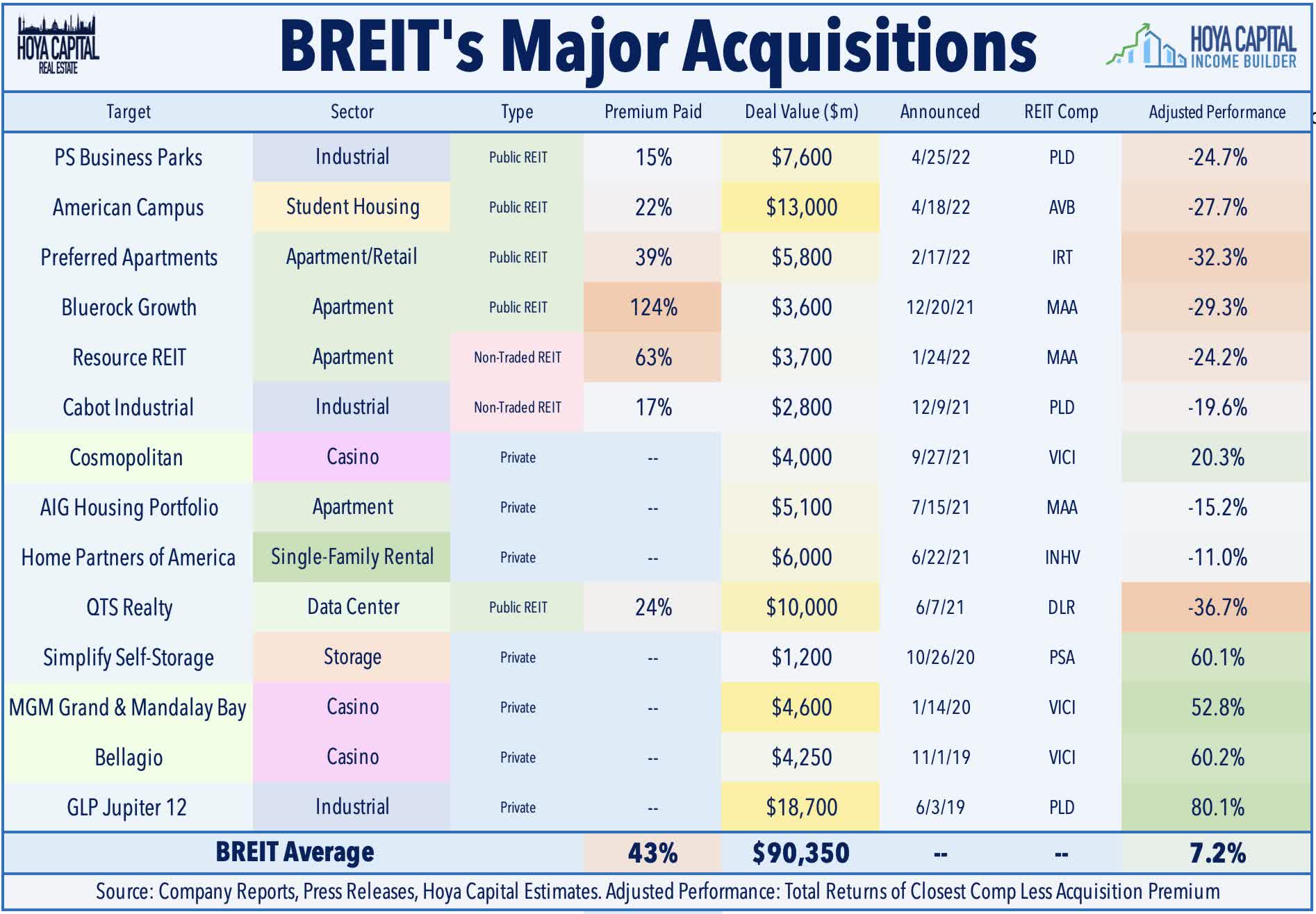

Seeking to raise capital to meet redemptions and keep the music playing, BREIT has quickly pivoted from buyer to seller – spawning its aforementioned deal with VICI at favorable terms for the Casino REIT – and we believe BREIT’s interest in the Cosmopolitan and the Bellagio are among the most likely assets that BREIT sells next. In arriving at this conclusion, we compiled statistics on all of BREIT's major portfolio acquisitions since its inception and examined the performance of the closest comparable public REIT for each of the 14 deals. The analysis revealed that BREIT paid an average premium of 43% on its deals for publicly-listed companies and that 9 of the 14 deals are currently "in the red" based on public market comparable pricing. Given that BREIT is unlikely to sell assets at a loss versus the original purchase price, we believe that the four most likely asset sales are its ~$4.25B stake in the Bellagio, its ~$4B state in the Cosmopolitan, its ~$1B Simply Self-Storage portfolio, or its Jupiter 12 industrial portfolio acquired as one of its first large-scale purchase.

{kind=link}

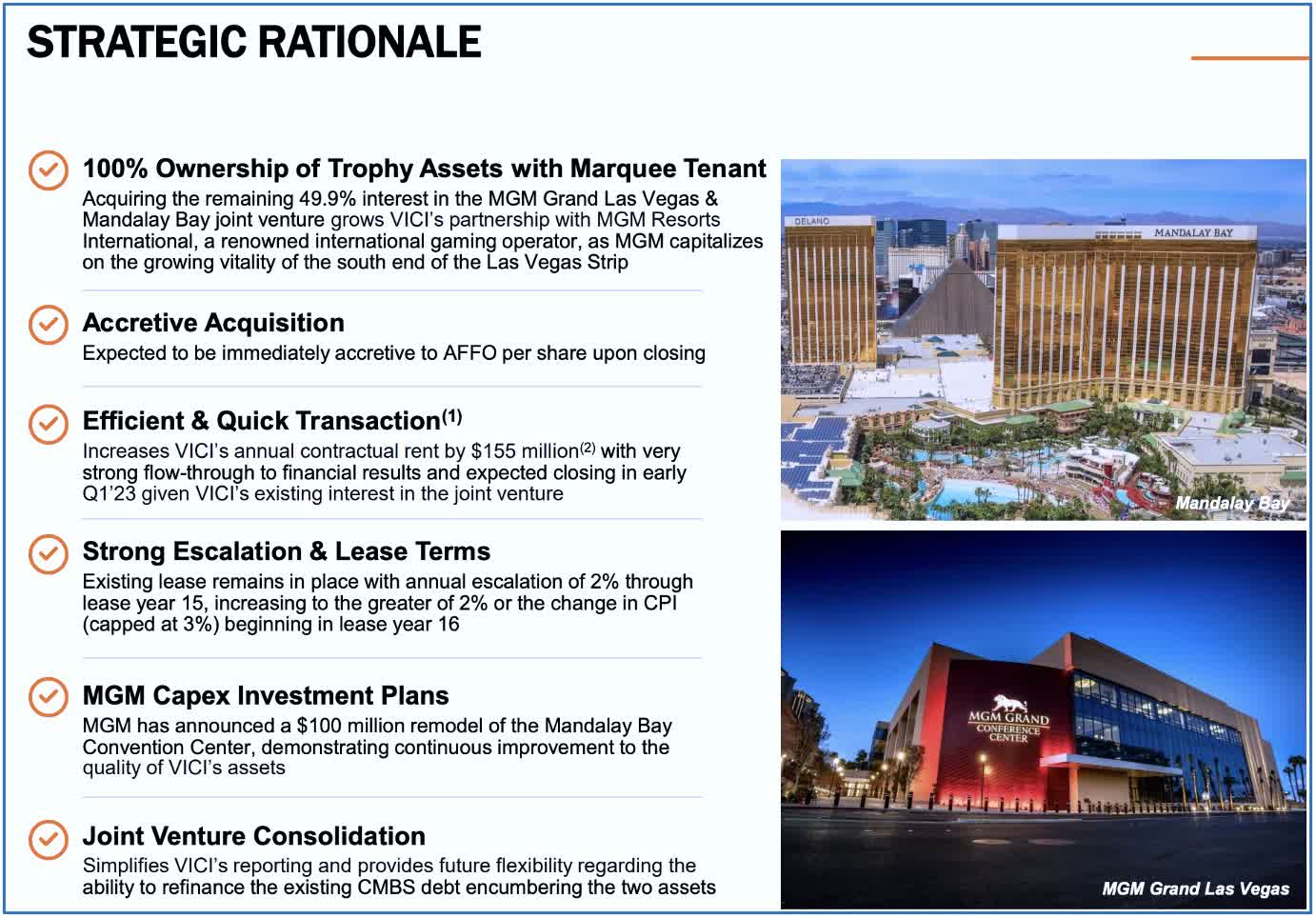

Of course, BREIT already sold one of its 5 profitable acquisitions in a $5.5B deal to sell its 49.9% share in the MGM Grand Las Vegas and the Mandalay Bay Resort to VICI Properties , which closed in January. Blackstone received $1.27B in cash, while VICI will assume Blackstone's share of roughly $3B in debt, which underscores the large debt load of BREIT. VICI - which will now own 100% of the properties - intends funded the deal with cash on hand and proceeds from existing forward equity sale agreements. The transaction - which has an implied cap rate of 5.6% - is expected to be immediately accretive to VICI's AFFO/share this year and will generate annual rent of $310M next year and escalate at a fixed 2.0% rate through 2035 and up to 3.0% thereafter. Notably, VICI Properties CEO Ed Pitoniak commented to CNBC that Blackstone approached VICI and that the deal "came together quickly."

{kind=link}

Casino REIT Portfolio & History

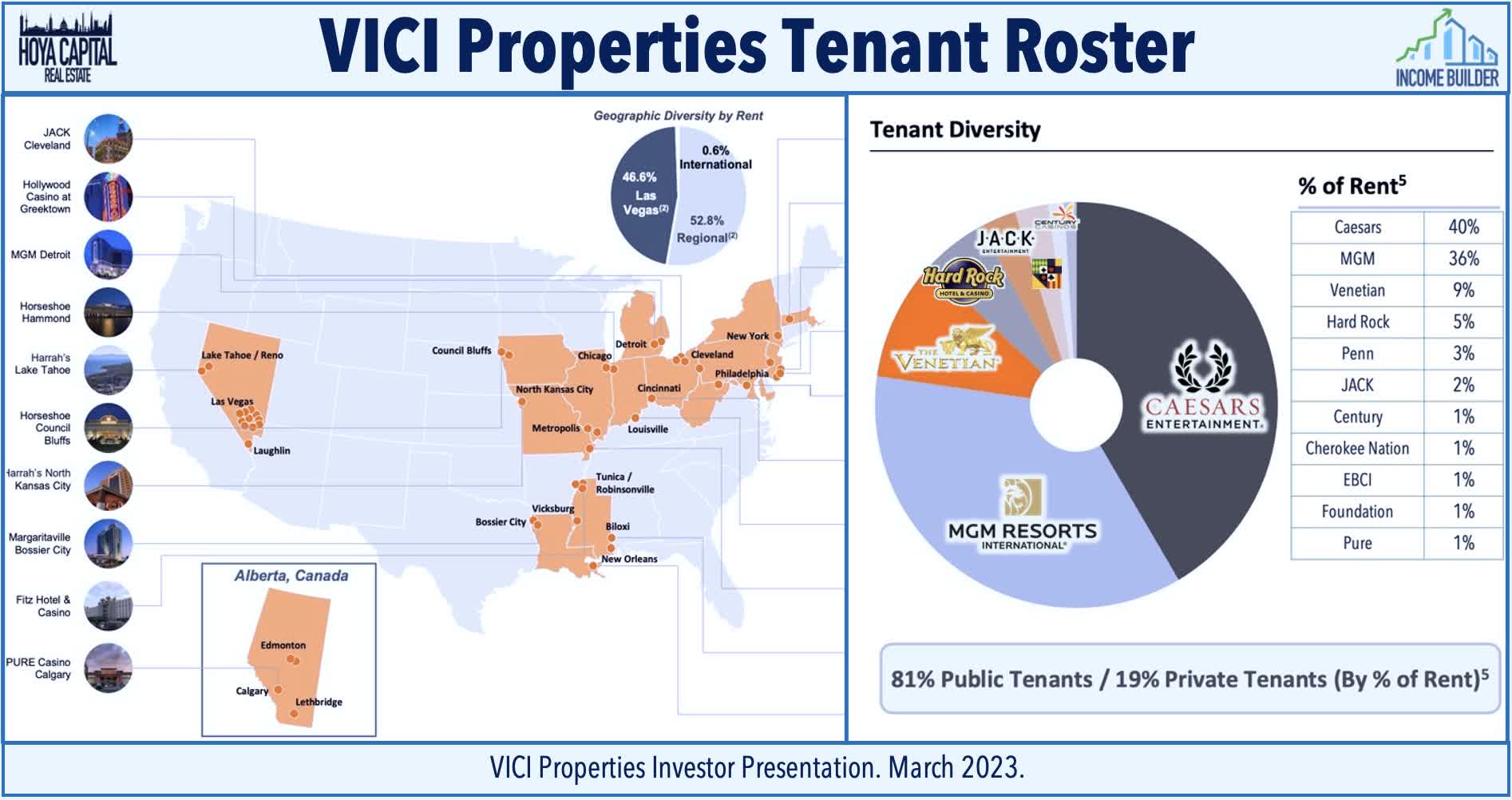

The deal is among the largest in VICI's history - which emerged as a "spin out" from Caesars Entertainment ( CZR ) in 2018 and has seen its market capitalization swell by 5x since its IPO. The new "King of Vegas," VICI now owns 50 properties across 15 states which include 59k hotel rooms - a portfolio that includes 3 of the 5 largest hotels in the country. Its recent combination with MGM Growth Properties further diversifies VICI's tenant concentration and geographical scope, lowering its largest tenant exposure - Caesars - from nearly 80% at the end of 2020 to just 40% following the closing of the MGP deal and the $4B acquisition of The Venetian from Las Vegas Sands earlier this year. The MGM Growth Properties portfolio - which was initially spun out in 2016 by MGM Resorts (MGM) owned 15 destination casinos including Mandalay Bay and the MGM Grand Las Vegas.

{kind=link}

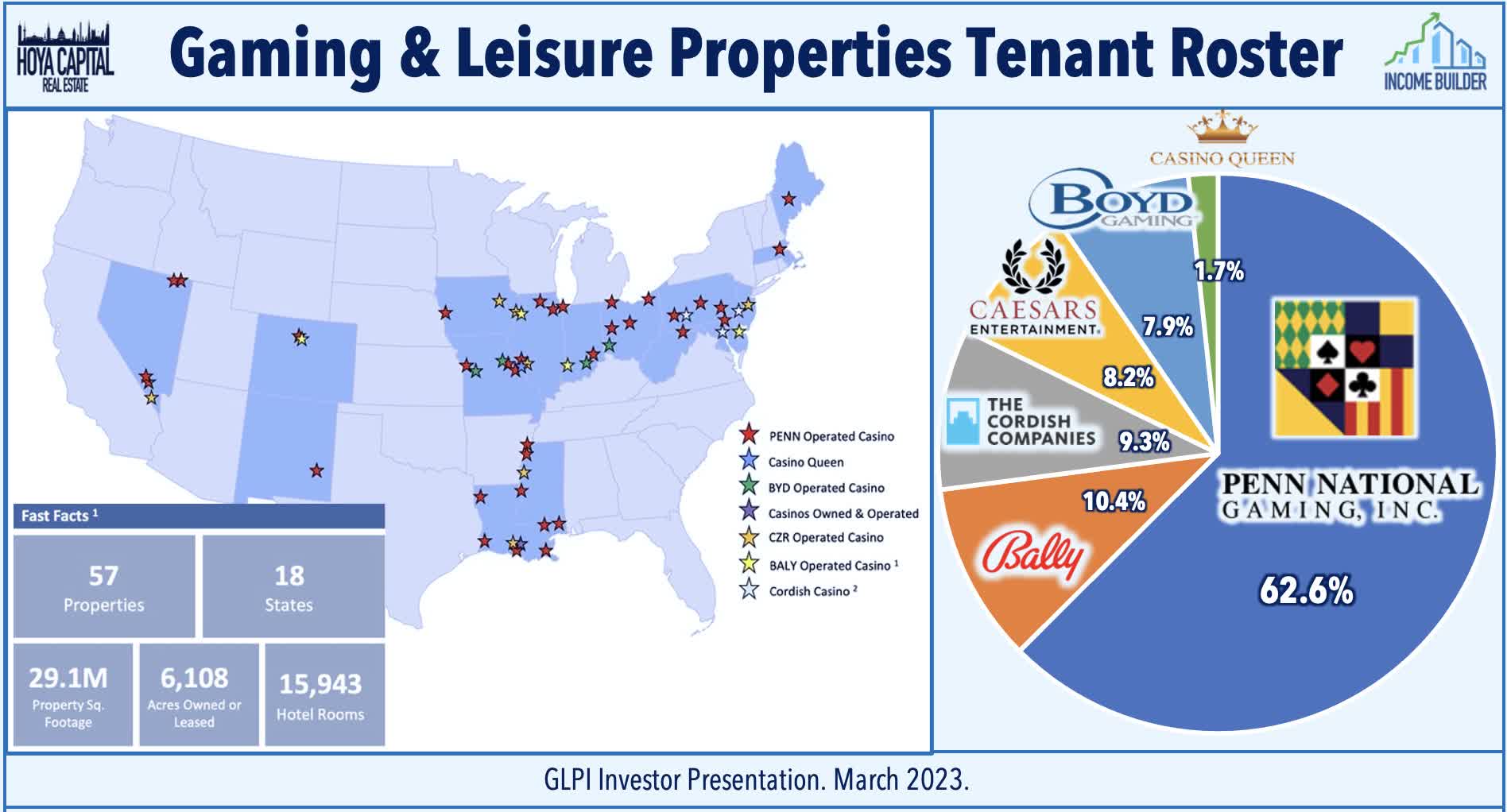

GLPI - which was spun out from PENN Entertainment ( PENN ) in 2013 - has also been an active and successful consolidator of regional casino assets, growing its market capitalization by nearly 4x since 2016. GLPI was also a bidder for MGP, but commented that the valuation "did not pencil for us" conceding that "it's a better deal for [VICI] than it would have been for us." GLPI did score a win in late 2021 with a major $1.8B acquisition of the Live! casinos in Maryland, Philadelphia, and Pittsburgh from Cordish Companies. Acquired at a 6.9% cap rate, the acquisition is GLIP's largest since 2016 and helps to diversify its tenant base further. GLPI now owns 57 properties across 18 U.S. states - primarily focused on regional casinos, which rely more heavily on gaming revenues compared to their Las Vegas peers which see a higher share of revenues from non-gaming hospitality and convention activity.

{kind=link}

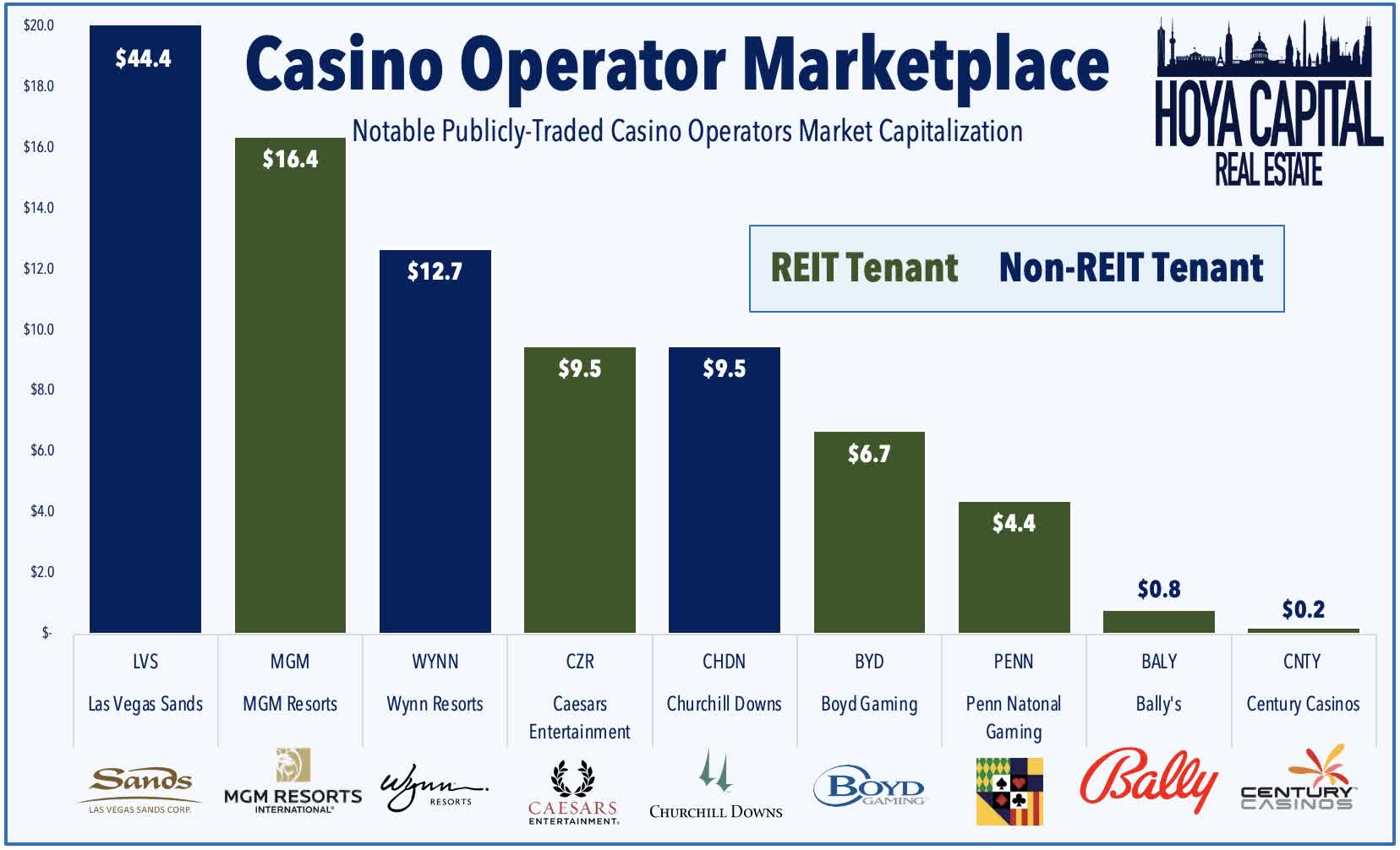

In addition to the aforementioned operators, other major casino operators include Las Vegas Sands ( LVS ), Wynn Resorts ( WYNN ), Churchill Downs ( CHDN ), Boyd Gaming ( BYD ), Bally's ( BALY ), and Century Casinos ( CNTY ) - most of which still retain ownership some or most of their real estate assets that could be potential future sale-leaseback opportunities for casino REITs. Among the few Las Vegas casinos that are not owned by REITs, the Wynn Las Vegas and Wynn Encore are likely among the most likely to eventually fall into these REITs' hands, particularly after Wynn's $1.7B sale of Encore Boston Harbor to Realty Income last year. International expansion has also long been a potential avenue discussed in casino REIT earnings commentary, and we got a small taste of this with VICI's recent $201M deal to acquire four casinos in Canada from PURE Canadian Gaming, a transaction that is expected to be immediately accretive to FFO upon closing.

{kind=link}

Casino REIT Earnings Analysis

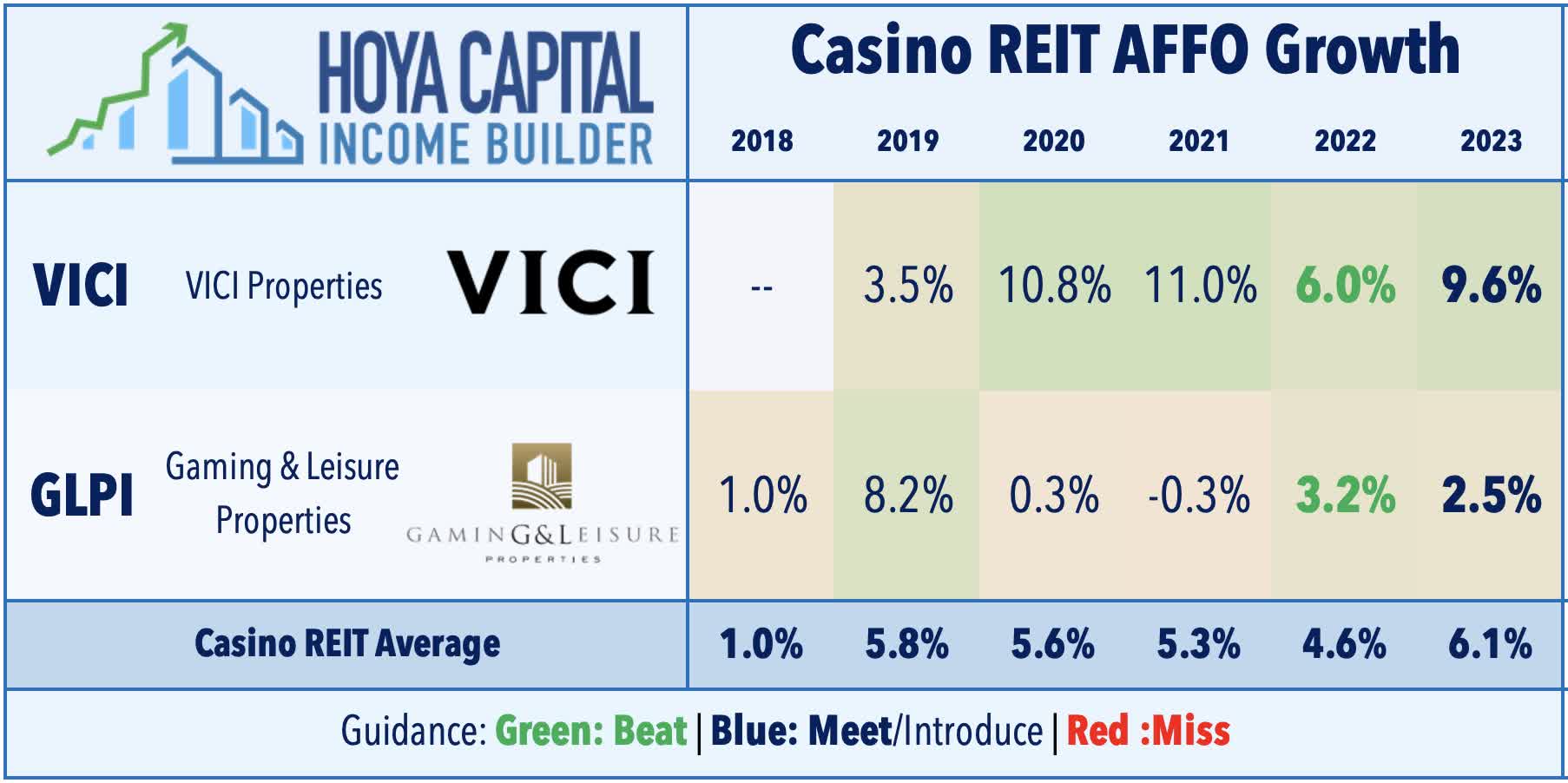

The positive momentum for casino REITs has carried into 2023 following a pair of solid earnings results last month. As discussed in our REIT Earnings Recap , VICI reported the stronger results of the two alongside an upbeat outlook for 2023, noting that its full-year FFO rose 6.0% in 2022 - 80 basis points above its prior growth outlook - and sees FFO growth of 9.6% in 2023 driven by CPI-linked rent escalations and by several recent large acquisitions discussed above. GLPI reported slightly better-than-expected results and concurrently hiked its dividend by 2% to $0.72 alongside a $0.25/share special dividend. GLPI recorded full-year FFO growth of 3.2% in 2022 - 60 basis points above its prior guidance - and sees FFO growth of 2.5% in 2023.

{kind=link}

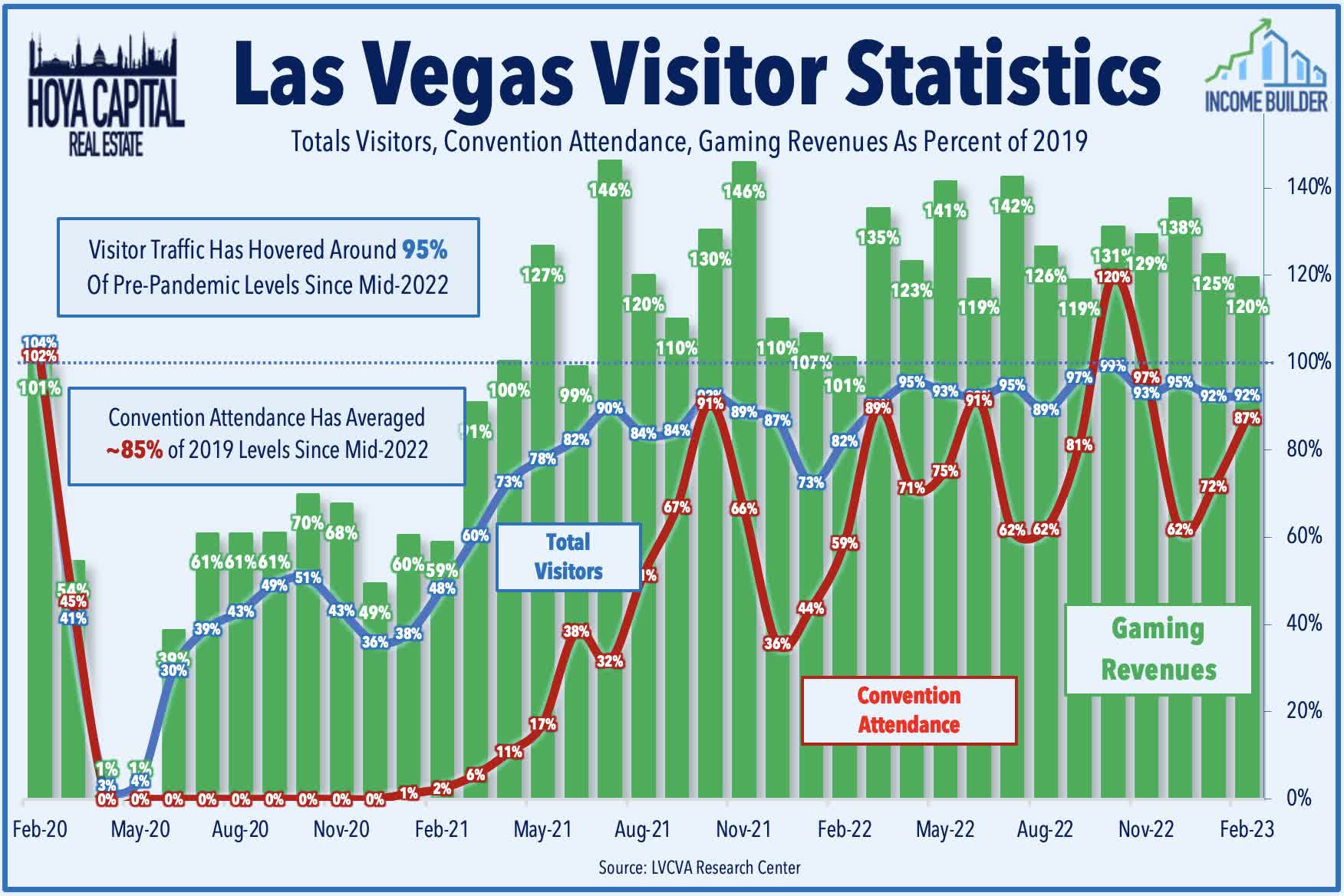

Importantly, Las Vegas has been a relative outperformer among domestic travel destinations throughout the pandemic and the early post-pandemic recovery. The Las Vegas Convention and Visitor Authority reported that total visitor traffic to Las Vegas returned to pre-pandemic record-highs last October and has hovered around 95% of pre-pandemic levels over the subsequent five months. Critically, convention attendance briefly exceeded pre-pandemic levels last year for the first time, and has averaged around 85% of pre-pandemic levels since mid-2022. Regional casinos recorded Gross Gaming Revenues that were 14% above 2019-levels while Vegas casinos recorded GGRs that were 31% higher than 2019 – gains that have importantly come alongside – not in spite of - the growing popularity of iGaming and sports betting.

{kind=link}

Casino REIT Performance & Fundamentals

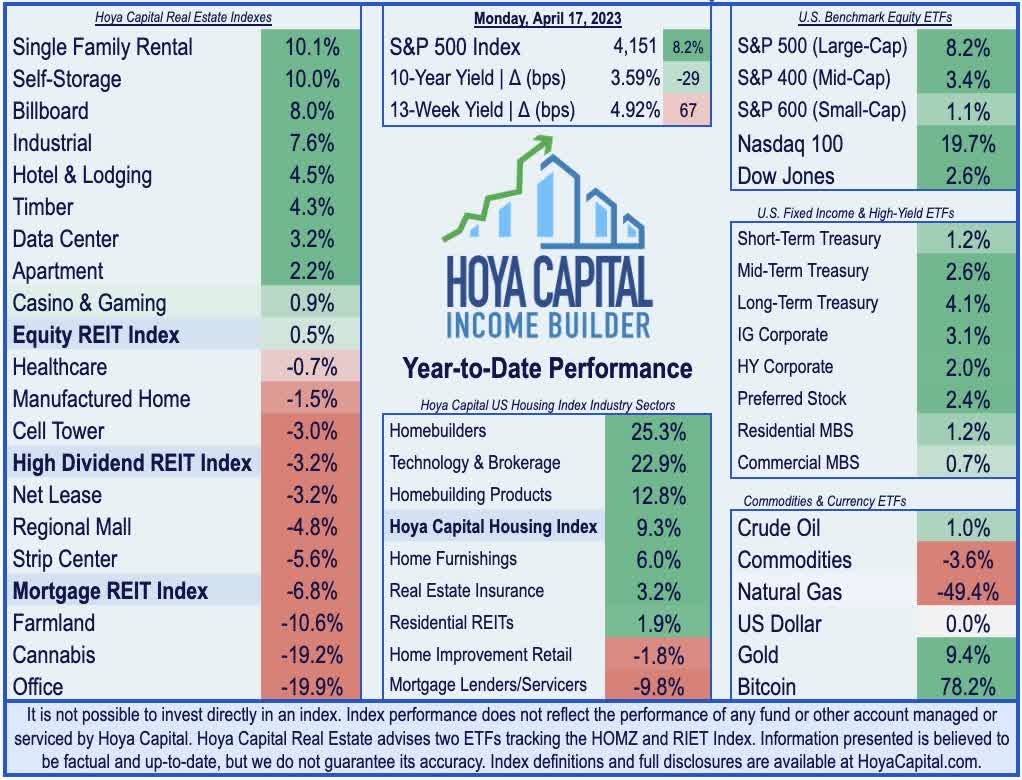

Casino REITs were slammed during the early onset of the outbreak amid the stifling economic lockdown that forced the majority of properties across the country to close temporarily. Casino REITs plunged roughly 60% between late February and early March 2020 on fears that their tenant base was destined for significant financial hardship, but mounted a furious comeback in the back half of 2020 and have continued that strong performance all the way into 2023. Casino REITs were the single-best-performing property sectors last year - and the lone REIT sector in positive territory - and are again higher by 0.9% this year compared to the 0.5% advance from the broad-based Vanguard Real Estate ETF ( VNQ ) and the 8.2% gain from the S&P 500 ( SPY ).

{kind=link}

As we've projected for the past several years, casino REITs have indeed benefited from an upward "re-rating" from investors as the sector has matured and as the business model - and economic "moat" around these REITs - has become better understood. As noted above, Casino REITs are now trading at multiples that are actually slightly above their similarly-sized net lease REIT peers with a Price/FFO multiple of roughly 14x. Critically, unlike their hotel REIT peers which have been among the worst-performing REIT sectors since the start of the pandemic, casino REITs' ultra long-term (15-50 year) triple-net master lease structure leaves most of the financial and operational risk - both on the upside and the downside - to their tenants. As a result, casino REITs have delivered some of the strongest 5-year returns in the REIT sector.

{kind=link}

Casino REIT Dividend Yields & Valuations

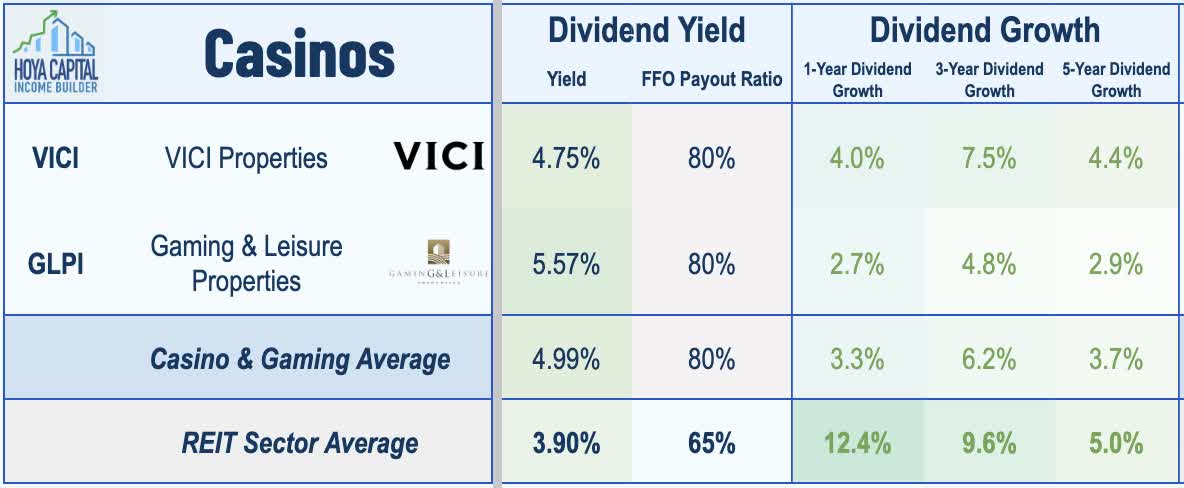

Casino REITs pay an average yield of 5.0%, well above the REIT market-cap-weighted average of 3.9%. Unlike some other higher-yielding property sectors, the long-term secular outlook for casino gaming appears relatively stronger, underscored by the above-average 5-year dividend growth rate of roughly 4% achieved by these casino REITs. In contrast to their hotel REIT peers, perfect rent collection allowed casino REITs to maintain dividends at-or-near previous levels last year, and both REITs boosted their dividends in 2021 and 2022.

{kind=link}

At the company level, GLPI pays the highest dividend yield at 5.57% after raising its payouts three times in 2022. After having reduced its dividend in 2020, the most recent increase to $0.72/share brought its dividend rate back above its pre-pandemic peak of $0.70/share. VICI , meanwhile, pays a yield of 4.75% after boosting its quarterly dividend last quarter by 8% to $0.39/share, as it has in every year since its IPO.

{kind=link}

Takeaway: Playing Offense As Peers Fold

A success story of the "Modern REIT Era," Casino REITs have been the best-performing property sector since their emergence in the mid-2010s, honing the competitive advantages of the public REIT model. Casino REITs were the lone property sector to finish in positive-territory in 2022, benefiting from their attractive “inflation-hedging” lease structure, strength in Las Vegas travel demand, and broader institutional investor acceptance. Fittingly, Casino REITs - exemplars in shareholder-friendly governance - have been beneficiaries of distress felt across the darker underbelly of the real estate industry, including Blackstone’s non-traded REIT ("NTR") platform. Access to longer-term fixed-rate capital has proven to be a significant competitive advantage for public REITs and these casinos REITs' impressive track record in capital deployment and shareholder-friendly governance justifies our willingness to “pay up” at moderately elevated multiples.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

Casino REITs: Winners Of Blackstone Distress