CTRM - Castor Maritime Reports Strong Q4 Results And Completes Tanker Operations Spin-Off

2023-03-08 21:46:51 ET

Summary

- Castor Maritime reports another set of decent quarterly results with weaker dry bulk charter rates largely offset by strong tanker markets.

- Going forward, Castor Maritime's result will mostly depend on movements in dry bulk charter rates which just recently recovered from multi-year lows.

- Shares continue to trade at a massive discount to net asset value ("NAV") due to severe corporate governance issues.

- Tanker operations have been spun off into a new entity with very strong fundamentals named Toro Corp. But similar to other recent spin-offs like Imperial Petroleum, United Maritime and OceanPal, the company is looking to pursue growth at the expense of common shareholders.

- That said, with near-term dilution less likely than previously anticipated and shares trading at a large discount to NAV, I would expect Toro's common shares to rebound once selling pressure from legacy Castor Maritime shareholders starts to abate.

Note:

I have covered Castor Maritime ( CTRM ) previously, so investors should view this as an update to my earlier articles on the company.

Earlier this week, junior Cyprus-based shipping company Castor Maritime completed the previously announced spin-off of the company's tanker operations into a new, Nasdaq-listed entity named Toro Corp. ((TORO)) or "Toro".

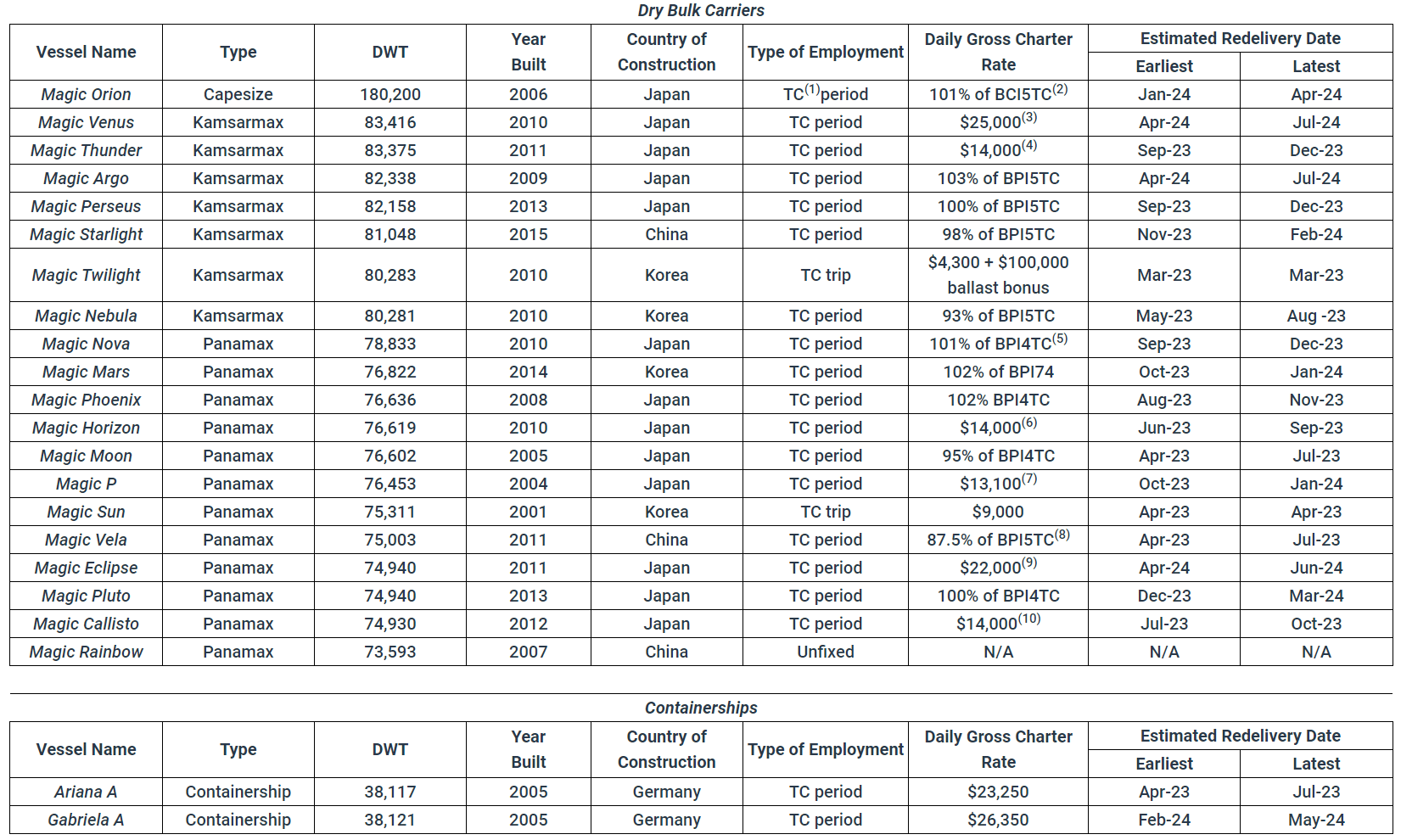

In addition, Castor Maritime reported strong fourth quarter and full-year 2022 results with the tanker segment offsetting recent weakness in dry bulk charter rates.

The company generated an impressive $46.4 million in cash from operating activities in the fourth quarter and $123.8 million for the full year.

Castor Maritime's year-end balance sheet remained in decent shape with zero net debt and $142.3 million in unrestricted cash on hand.

That said, with the tanker bonanza having been spun off into Toro, Castor Maritime's near-term earnings and cash flows will be impacted quite meaningfully.

While the company's Q1 report will still include a meaningful contribution from the tanker fleet, Castor Maritime's second quarter report will largely depend on movements in dry bulk charter rates which recently have started to recover from multi-year lows marked in February.

Considering the lack of scrubber benefits and given the fact that most of the fleet remains employed under index-linked time charter contracts, absent any major rally in dry bulk charter rates, Q2 results are likely to be materially weaker on a year-over-year basis:

{kind=link}

Company Press Release

Please note also that the company recently acquired two, fairly old feeder-size containerships in an expensive related-party transaction from entities affiliated with the company's CEO. Even when considering the profitable time charters attached to the vessels, I would estimate a premium of up to 20% to prevailing market prices at the time of the purchase in November.

Looking at net asset value ("NAV") per share following the Toro spin-off, CTRM stock continues to trade at a massive 80%+ discount:

Annual Report on Form 20-F / MarineTraffic.com

Clearly, investors are discounting the fact that the company has aggressively pursued growth at the expense of common equity holders in recent years thus resulting in shares being down 98% since listing on Nasdaq four years ago.

With that said, it's time to take a closer look at Toro after the company filed its annual report on Form 20-F in conjunction with the spin-off.

Toro Update

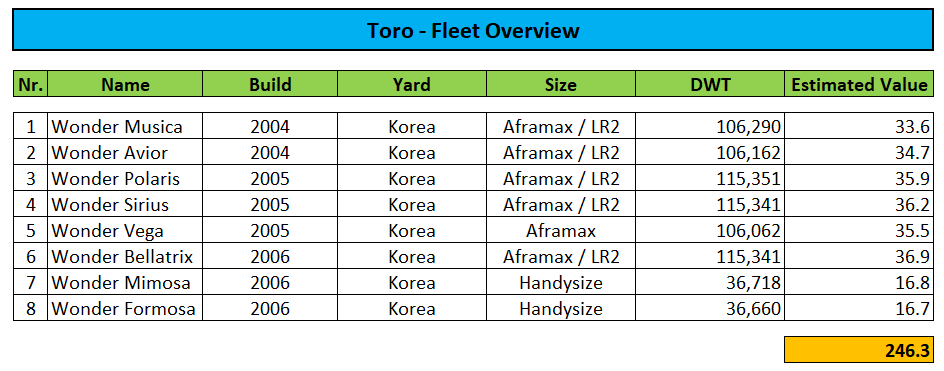

At first glance, Toro appears to be an interesting and highly profitable bet on the red hot tanker markets with decent dividend potential. Moreover, due to recent geopolitical events, the company's fairly old fleet is currently in the sweet spot of buying interest with second hand vessel valuations at all-time highs.

According to MarineTraffic, the company's small tanker fleet with an average age of 17.5 years is currently valued at almost $250 million, more than double its aggregate purchase price of approximately $100 million last year:

{kind=link}

Annual Report on Form 20-F / MarineTraffic.com

Over the past six months, Toro has generated a whopping $37.5 million in cash from operating activities thus increasing cash on hand to $42.5 million and resulting in a net cash position of close to $30 million.

Unfortunately, disclosures made in Toro's annual report on form 20-F clearly show the company's intent to pursue growth at the expense of common shareholders, very similar to former parent Castor Maritime and other recent spin-offs like Imperial Petroleum ( IMPP , IMPPP ), OceanPal ( OP ) and United Maritime ( USEA ):

Toro has an authorized share capital of 3,900,000,000 common shares that it may issue without further shareholder approval. Our growth strategy may require the issuance of a substantial amount of additional shares. Based on market conditions, we may also opportunistically seek to issue equity securities, including additional common shares.

(...)

On November 14, 2022, Castor, in its capacity as our sole shareholder, authorized our Board to effect one or more reverse stock splits of our common shares issued and outstanding at the time of the reverse stock split at a cumulative exchange ratio of between one-for-two and one-for-five hundred shares.

That said, this is actually an improvement from earlier filings (emphasis added by author):

Toro has an authorized share capital of 3,900,000,000 common shares that it may issue without further shareholder approval. Our growth strategy may require the issuance of a substantial amount of additional shares. Based on market conditions, we may also opportunistically seek to issue equity securities, including additional common shares, shortly following the Spin Off.

With more than $40 million in cash on hand and decent cash flow generation, Toro won't have to raise capital anytime soon and given record-high second hand tanker prices, the company simply lacks opportunities to expand its tanker fleet in the near-term.

At this point, I would expect management to wait for a more opportune time to raise growth capital, particularly with shares currently changing hands at an approximately 75% discount to estimated NAV:

Annual Report on Form 20-F / MarineTraffic.com

Please note that Castor Maritime has been compensated with $140 million in 1% Series A Fixed Rate Cumulative Perpetual Convertible Preferred Shares:

The Series A Preferred Shares are convertible, in whole or in part, at their holder’s option, to common shares at any time and from time to time from and after the third anniversary of their issue date and prior to the seventh anniversary of such date. Subject to certain adjustments, the “Conversion Price” for any conversion of the Series A Preferred Shares shall be the lower of (i) 150% of the VWAP of our common shares over the five consecutive trading day period commencing on and including the Distribution Date, and (ii) the VWAP of our common shares over the 10 consecutive trading day period expiring on the trading day immediately prior to the date of delivery of written notice of the conversion; provided, that, in no event shall the Conversion Price be less than $2.50.

But with the conversion option not being exercisable before March 7, 2026, Toro is not likely to be re-merged into Castor Maritime anytime soon.

That said, similar to Castor Maritime, CEO Petros Panagiotidis retains full control of Toro by the means of supervoting Series B Preferred Shares.

Bottom Line

Both Castor Maritime and Toro are fundamentally strong companies but severe corporate governance issues and fears of near-term dilution have resulted in shares trading at very large discounts to estimated net asset value.

That said, considering Toro's low number of outstanding shares and with risk for immediate dilution apparently much lower than previously suspected by me, I have decided to enter a small trading position in the company's common shares with the intent of averaging down on potential further weakness.

Assuming no near-term dilution, I would expect the current selling pressure from legacy Castor Maritime shareholders to abate as soon as next week thus potentially setting the stock up for a rebound.

Please note that this idea is solely suited for highly-speculative investors and traders while long-term investors should continue to avoid both companies.

For further details see:

Castor Maritime Reports Strong Q4 Results And Completes Tanker Operations Spin-Off