CPRX - Catalyst Pharmaceuticals: Fixing Its Misnomer Is No Easy Task

2023-04-19 07:51:25 ET

Summary

- The extent to which FIRDAPSE in the treatment of LEMS can support ongoing growth is a big question mark for Catalyst shareholders.

- The FYCOMPA acquisition comes with more big question marks.

- Although enjoying comfortable liquidity, Catalyst will struggle to live up to high expectations.

This is my fourth Catalyst Pharmaceuticals ( CPRX ) article. In this article I assess both its forward prospects and its challenges.

FIRDAPSE modest growth is proving resilient, with more in sight

FIRDAPSE revenues

FIRDAPSE was FDA approved in 11/2018 for the treatment of Lambert-Eaton myasthenic syndrome (LEMS) in adults. Catalyst's 04/2023 presentation (the " Presentation ") slide 22 excerpt below lists its yearly revenues:

ir.catalystpharmaceuticals.com

{kind=link}

FIRDAPSE revenues advanced slowly during its initial years post-approval and during the pandemic. Its revenues for 2022 advanced over 2021 at an advanced 59% clip. During Catalyst's Q4, 2022 earnings call (the " Call ") CEO McEnany forecast its 2023 revenues in a $245-$255 million range.

Taking the midpoint of $250 million would represent a modest 2023 FIRDAPSE revenue gain over 2022's revenues of ~17%. It would also suggest that the 59% increase from 2021 to 2022 was a bit of an outlier. There are two developments in the wings that could significantly change the FIRDAPSE trajectory, one to the upside, the other down.

Upside growth potential

During the Call, management reported that certain:

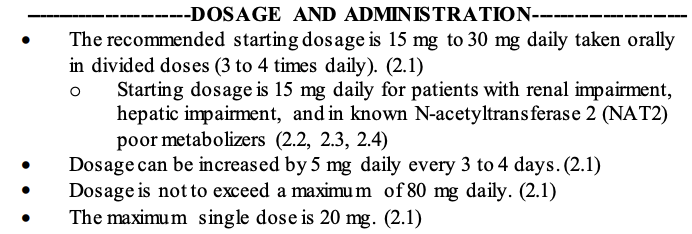

...LEMS patients are already being treated at 100 milligrams daily dosage of FIRDAPSE after their physician worked with the pharmacy and insurance providers to justify the higher dose. Other patients on the current indicated maximum dose of 80 milligrams per day and their physicians have expressed a need to increase the indicated daily dosage to 100 milligrams to optimize therapy and this planned supplement, if approved, will help those patients.

This could be a very big deal. Currently the average daily dose of FIRDAPSE is ~60-61 mg. The current price per patient is ~$375,000. It is dose related. The average price correlates to the average dose.

A widespread increase of the average dose to 100 milligrams would be significant. It is not likely however under FIRDAPSE's current label which reads:

{kind=link}

Catalyst is currently in talks with the FDA to increase this to 100 mg. If all goes as expected it will file an sNDA in Q3 to increase the indicated maximum daily dosage of FIRDAPSE to 100 mg.

Patent clouds

Catalyst's recent share price had an awful ruction earlier this year as shown by the price chart below:

This frigid Arctic air coldcocking Catalyst came in the form of a notice that Teva Pharmaceuticals ( TEVA ) had submitted an FDA application to sell a generic version of FIRDAPSE in the U.S.

Patent law in the United States is inherently complex. I am no expert on the subject. Checking Catalyst's 2022 10-K (the 10-K ) on the subject with its 277 returns for the thread "patent" is headache inducing to the extreme. Three things are clear from the effort:

- In 01/2023 three generic drug manufacturers each submitted an Abbreviated New Drug Application (ANDA) to the FDA for authorization to manufacture or sell a generic version of FIRDAPSE in the United States.

- This filing created a window within which Catalyst could file a lawsuit, thereby triggering a stay precluding FDA from approving any ANDA until May 2026 or entry of judgment holding the patents invalid, unenforceable, or not infringed, whichever occurs first.

- Catalyst timely filed the lawsuit and intends to vigorously protect its rights.

Catalyst's FYCOMPA acquisition complicates and enhances its revenue outlook

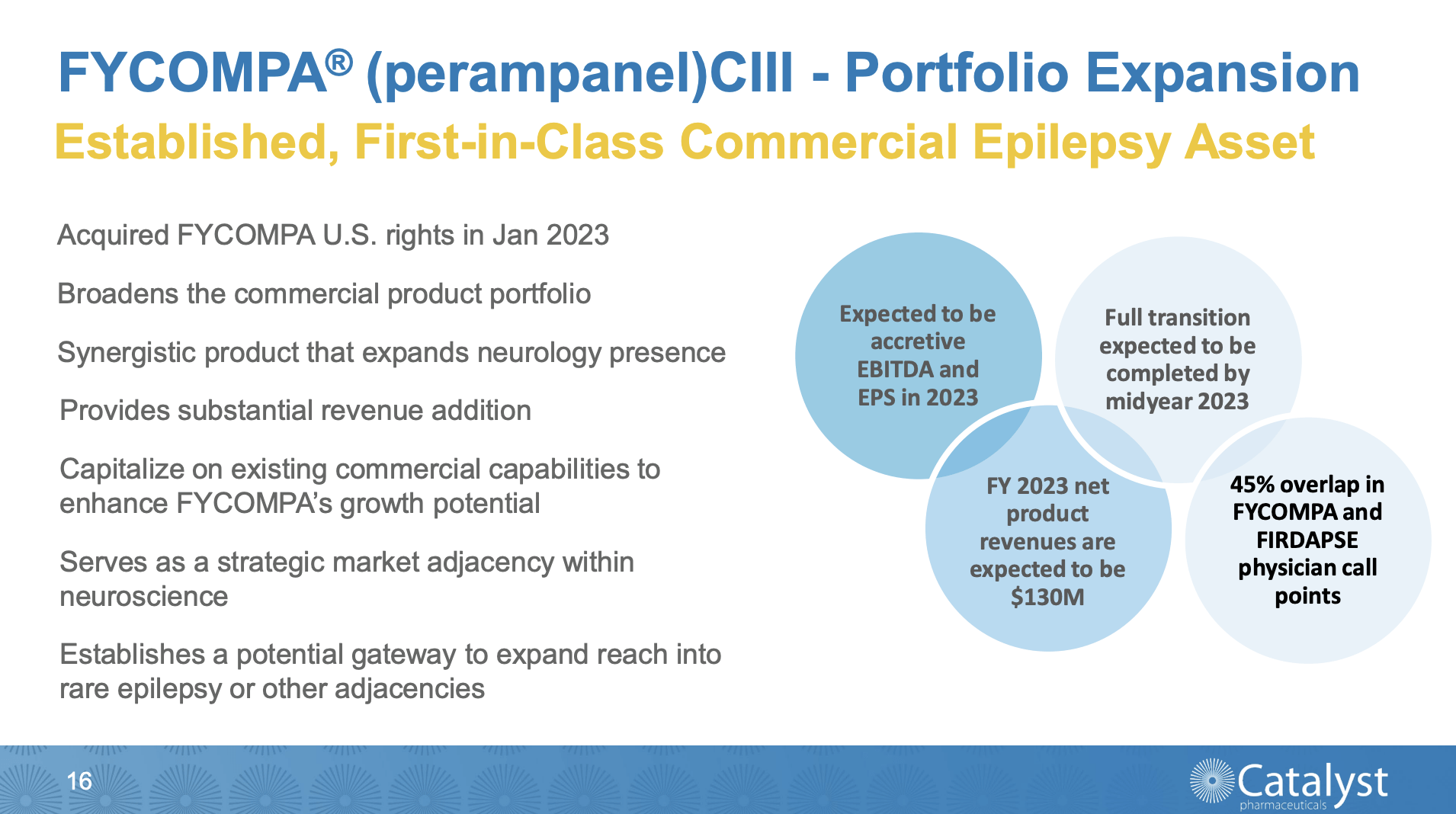

On 12/2022 Catalyst acquired US rights to an old warhorse epilepsy drug FYCOMPA (perampanel) from Eisai's ( OTCPK:ESALY ). Its Presentation slide 16 sets out the rationale for the deal:

{kind=link}

I have long chafed at Catalyst's over-reliance on FIRDAPSE. Now it has a backup revenue generating product. In its 10-K (p. 4-5) Catalyst describes key elements of this deal which closed on 01/24/2023:

- an upfront payment of $160 million in cash

- an additional cash payment of $25 million if a requested patent extension for FYCOMPA is approved

- royalty payments in undisclosed amount after patent protection for FYCOMPA expires, which royalty payments will be reduced upon generic equivalents to FYCOMPA entering the market

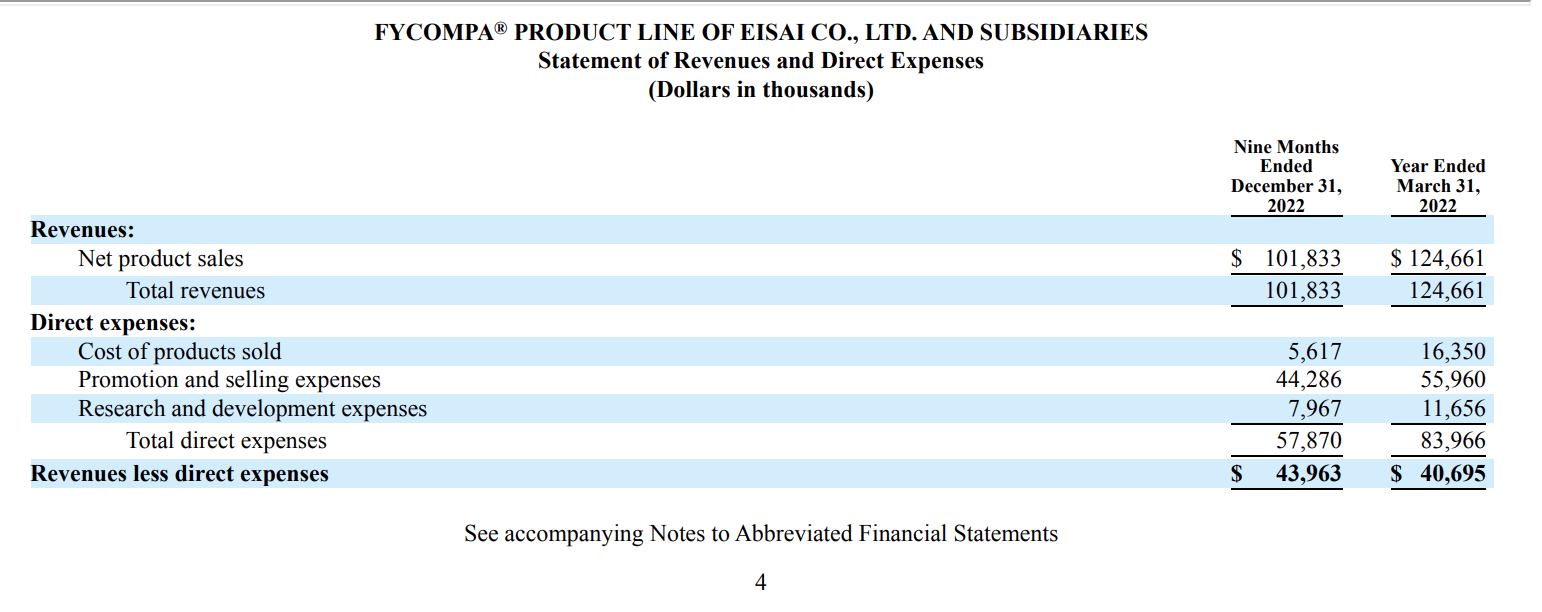

FYCOMPA has patent exclusivity until at least 05/2025 (10-K p.17) with possible extension to 06/2026. During the call Catalyst advised that it expected $130 million in 2023 FYCOMPA revenues roughly in line with its production in 2022 as shown by Catalyst's SEC filing below:

{kind=link}

This deal is a bit of a head scratcher. Catalyst paid $160 million in cash for an asset generating ~$40.6 million in revenues less direct expenses annually. Its patent only extends for two more full years. Will Catalyst ever earn its $160 million back?

Catalyst's future will likely continue to show comfortable earnings but little growth

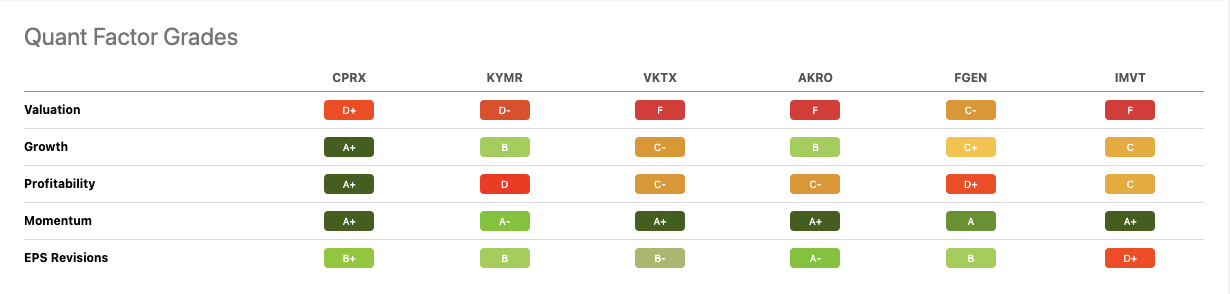

Catalyst fits in nicely with its Seeking Alpha peers . Its market cap and its enterprise value are unremarkable. In terms of comparable 04/18/2023 quant factor grades, things get more interesting:

{kind=link}

Here the peers are truly comparable in terms of valuation, momentum and EPS revisions. The important grades for growth and profitability are where Catalyst stands out.

It is hard to quarrel with Catalyst's A+ for profitability. Management has done a tremendous job with FIRDAPSE taking profits as they come. It has been able to do this because it has virtually no pipeline outside of FIRDAPSE, keeping its R&D expenses broadly in check.

As for growth, its FIRDAPSE is showing modest growth only expected this year. I do not consider any growth attributed to FYCOMPA as true apples to apples growth, particularly since its expected 2023 revenues are roughly in line with 2022.

Conclusion

This upcoming year will be interesting for Catalyst as it inboards FYCOMPA. Investors should keep their expectations in check. Based on its Q4, 2022 performance and its announced expectations, there is little reason for optimism.

During the Call, management bruited the possibility of more deals being imminent. However, judging by FYCOMPA, a new deal may not be reason to celebrate.

For further details see:

Catalyst Pharmaceuticals: Fixing Its Misnomer Is No Easy Task