CPRX - Catalyst Pharmaceuticals: Teva's Patent Challenge Of Firdapse Could Spell The End For This Cash Cow

Summary

- Catalyst has successfully commercialised Firdapse, a therapy for LEMS, earning >$200m from the drug in 2022 likely with a strong profit margin.

- In 2020/2021, Catalyst was able to overturn an FDA ruling granting Jacobus' rival LEMS drug Ruzurgi approval and access to the same market.

- Now the company faces a new challenge - from generics giant Teva, who will attempt to challenge Firdapse's patents.

- It is a less-than-ideal situation for Catalyst despite its previous resilience against the FDA / Jacobus.

- Its rumoured Catalyst is looking at M&A to try to diversify away from its reliance on Firdapse. That could be tricky, but failure to do so may ultimately cost the company.

Investment Overview

Catalyst Pharma ( CPRX ) is a $1.6bn market cap (at the time of writing) Florida based commercial stage biotech that markets and sells a single product - the neuronal potassium channel blocker amifamprdine, under the brand name Firdapse.

When I last covered the company back in November 2019 , I described how Catalyst had acquired the rights to the amifampridine phosphate based treatment in 2012 from BioMarin Pharmaceutical ( BMRN ), which at the time had been awarded Orphan Drug status by the US Food and Drug Agency ("FDA") for the treatment of the potentially fatal autoimmune disease Lambert-Eaton Myasthenic Syndrome ("LEMS"), and how the company won approval from the FDA to market and sell the drug in 2018 in 10mg tablet form under the brand name Firdapse.

I also covered the criticism the company received from the likes of US Senator Bernie Sanders over Firdapse's $375k list price, especially when another company, privately owned Jacobus Pharmaceuticals, had been supplying the drug to patients for free under the brand name Ruzurgi, and the fact that subsequently, ignoring the patents held by Catalyst, the FDA had handed Ruzurgi a pediatric approval, effectively clearing physicians to prescribe Ruzurgi to adults in lieu of Firdapse.

Finally I discussed the fact that Catalyst had opted to take the FDA to court to try to deny Jacobus the rights to sell Ruzurgi, and, pointing out that Catalyst had guided for $72m of Firdapse revenues in 2019, and $130m in 2020, I suggested:

In my view, buying Catalyst at the current price is not much better than a 50/50 gamble, with much riding on the outcome of Catalyst's court case with the FDA.

On the other hand, buy now and should the court case go Catalyst's way, the share price will surely spike. On balance, I do not think that Catalyst will win its case, and will therefore remain neutral to bearish for now, but that is only my opinion.

Long story short, I was wrong. Although the signs initially pointed to Catalyst losing its court battle, with a summary judgment in favour of the FDA and Jacobus upheld by a Magistrate Judge in September 2020, one year later that ruling was overturned after an appeal from Catalyst, and in January 2022, Catalyst reported that:

U.S. Court of Appeals for the 11th Circuit has issued a mandate directing the District Court that heard Catalyst's claim against the FDA to enter summary judgment in favor of Catalyst in its lawsuit against the FDA, thereby vacating the FDA's approval of Ruzurgi

In July, Catalyst settled its patent dispute with Jacobus, agreeing to license the rights to develop and commercialise Ruzurgi in the US and Mexico, purchasing Ruzurgi patents, making a cash payment to Jacobus and agreeing to pay a low single digit royalty on net sales of amifampridine.

By the time Catalyst reported record net revenues of $57.2m in Q322 - up 59% year-on-year, and guided for FY22 revenues of $205m - $210m, whilst reporting a cash position of >$250m, the company's share price had reached an all-time high of $19, for a 5-year gain of >350%.

Catalyst shares passed $21 earlier this month, but now it seems there may be a new threat on the horizon, this time in the form of Teva Pharmaceuticals - an altogether different proposition, being an $11bn market cap generics specialist.

On 23rd January Catalyst announced that it was aware Teva had submitted an Abbreviated New Drug Application ("ANDA") to the FDA "seeking authorization to manufacture, use or sell a generic version of FIRDAPSE® in the United States: and additionally that:

Teva's Notice Letter states that its ANDA contains a Paragraph IV Certification alleging that these patents are not valid, not enforceable, and/or will not be infringed by the commercial manufacture, use or sale of the proposed product described in Teva's ANDA submission.

Catalyst now has 45 days to initiate a patent infringement lawsuit against Teva, which would:

...trigger a stay precluding FDA from approving Teva's ANDA until May 2026 or entry of judgment holding the patents invalid, unenforceable, or not infringed, whichever occurs first.

Catalysts shares nosedived from $21, to $16 on the news - a fall of nearly 25%, but is this the beginning of the end of Catalyst's monopolistic control of Firdapse and the LEMS market, or can the biotech successfully fight off this generic competitor?

Firdapse - Background To Market Opportunity

{kind=link}

Although Catalyst has come under significant criticism over its pricing of Firdapse, in the company's defence, as Chief Commercial Officer Jeffrey del Carmen told analysts on the company's Q322 earnings call:

Patients enrolled in Catalyst Pathways, including those who are covered by Medicare and accessing foundation assistance, had an average co-pay of less than $2 per month.

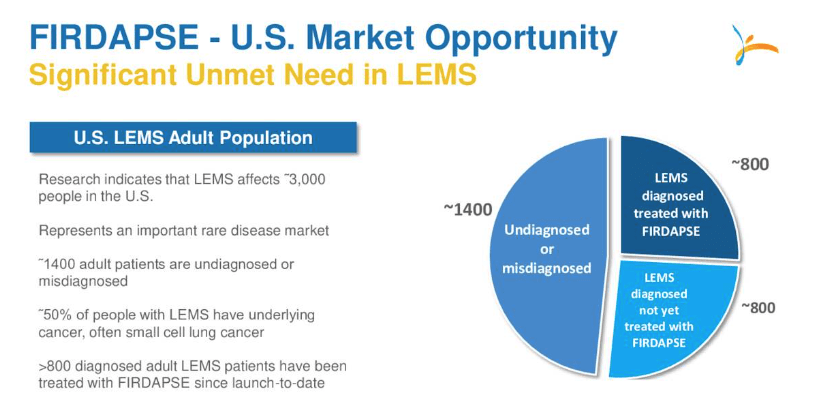

Catalyst is also committed to supporting all patients with LEMS, which has resulted in the submission of a supplementaryNDA ("sNDA") to the FDA to expand the label into pediatric patients, and the targeting of patients who have a co-morbidity of small cell lung cancer - ~50% of all patients.

The company is additionally seeking out patients who may be undiagnosed or misdiagnosed, and attempting to "shorten the diagnostic journey for LEMS patients" through voltage-gated calcium channel antibody tests.

That's not necessarily to say that Catalyst management is not motivated by profits - it was reported in September that co-founder and President Patrick McEnany had sold shares worth $15.8m in two separate transactions, while Chief Operating Officer and Chief Scientific Officer Steven Miller, sold ~653.8K CPRX shares for a total value of ~$1.8M.

Catalyst has undoubtedly become a very profitable company, delivering operating income of $32m, $41m and $52m in 2019, 2020, and 2021, whilst rewarding shareholders with triple digit share price gains.

Clearly, however, Catalyst believed that it had sufficient patent protection in place to continue to drive significant profits from Firdapse for many more years, driven by the drug's market exclusivity and its own ability to find new patients who could benefit from the drug.

Teva - A Different Proposition With The Resources To Win A Legal Battle

Catalyst may have been able to deal with privately owned Jacobus by making a small cash payment and offering a small royalty on net sales, but it seems unlikely that this approach will work with Teva, an experienced marketer and seller of generic drugs that picks its targets carefully.

It seems almost inevitable that Catalyst will "trigger a stay" and drag Teva into the courts, as this will substantially delay Teva's entry into the market, even if the outcome of the dispute is not in Catalysts' favour, perhaps until 2026.

An interesting point is how hard Teva would fight any court battle however. For example, last November, Eli Lilly was ordered to pay Teva $176m as a result of Lilly's infringing three patents covering Teva's migraine prevention drug Ajovy. Granted, in this case the situation is the other way around, but the point is that Teva is a very large Pharmaceutical company, generating revenues of nearly $16bn in 2021, and operating income of >$3bn, and fighting likely hundreds of lawsuits with triple-digit millions on the line.

In short, Teva may simply be testing the water, so to speak, with Firdapse, and may back away if the process of filing its ANDA proves too complex or the rewards of marketing and selling a Firdapse look too meager.

For a small biotech, Catalyst is making a lot of money out of marketing and selling Firdapse, but a generic version of the drug would probably do well to earn even 25% of the amount that Firdapse will make in 2022 thanks to its high price point and exclusivity. From Teva's perspective, it may not be worthwhile to fight Catalyst in court - after all, whilst Jacobus may have been a small company, it should also be noted that Catalyst took on the FDA itself and won.

Besides The Stay, How Does Catalyst Respond?

A cynic might believe that knowledge of the Teva ANDA submission was what drove management to sell their shares back in November, and what is driving them to expand the business. On the Q322 earnings call, Steven Miller told analysts:

On the long-term strategy front, we have been accelerating our efforts with our business development initiatives. And we are in advanced stages of due diligence, and we're making substantial progress in evaluating strategic opportunities.

If Catalyst is looking to branch out from being a one-product company and target - and according to some sources, it plans to "acquire the rights to market an epilepsy drug in the first quarter of 2023, potentially generating around $136 million in sales per year" - then now is likely as good a time as any.

With that said, however, it took Catalyst six years and nearly $100m in operating losses to bring Firdapse to market, which speaks to the reality that finding and launching commercially successful drugs is an extremely tough business.

Winners like Firdapse are rare, which is why it must be doubly frustrating to face a challenge from a company as large, experienced and well-resourced as Teva Pharmaceuticals is.

Steven Miller also told analysts on the Q322 earnings call that:

Finally, we're planning to seek through a supplementary NDA to increase the indicated maximum dose of Firdapse from 80 milligrams per day to 100 milligrams per day. A number of Firdapse patients are already being treated at this dose after their physician worked with the pharmacy and insurance providers to justify the higher dose.

Other patients on the current indicated maximum dose of 80 milligrams per day and their physicians have expressed the need to increase the indicated daily dosage to 100 milligrams, and this - and supplement if approved will help to optimize the treatment of those patients.

A well-known strategy for extending the patent protection for a drug is to try to create more patents covering e.g. the dosing regime, method of administration, or the chemistry, manufacturing and controls ("CMC"), often referred to as creating a "patent thicket", thereby extending patent protection for several more years.

I am not sure if a higher dose regime would necessarily extend the patent protection for Firdapse, but it is important to stress that although Catalyst may be a David to Teva's Goliath, it does have a number of stones it can catapult in Teva's direction.

Conclusion - Catalyst's Serene Progress With Firdapse Has Been Checked By Teva - This Will Weigh On The Share Price But Don't Rule David Out Of This Fight

Back in late 2019 I incorrectly surmised that Catalyst would struggle to win its legal disputes with the FDA and with Jacobus, but the company didn't just win them, it ended up taking Ruzurgi out of Jacobus' hands and switching Ruzurgi patients over to Firdapse.

This has resulted in a phenomenally profitable business, albeit one with substantial single asset risk. There's no doubt that Catalyst has the funds to put up a fight against Teva, and that Teva may decide it does not have the stomach for this fight and ultimately decide to allocate its R&D / legal dispute resources elsewhere.

What makes me concerned for Catalyst and its share price however is that Teva is far from the only generic drug developer that could decide to test the strength of Firdapse's patents. To name a few other companies, there is Viatris ( VTRS ), Organon ( OGN ), Sun Pharmaceuticals, Novartis' ( NVS ) Sandoz division, Cipla, Dr. Reddy's ( RDY ), Amgen ( AMGN ), Hikma, and several others' besides.

Catalyst may be able to resist the challenge from a single generic drug maker, and it may be able to resist the challenge of several such companies for a couple of years by taking them to court, but eventually - by 2026, certainly - it will have to move on from Firdapse as its main source of revenue.

That ought to present an interesting challenge for Catalyst and perhaps ultimately reveal whether this is a business focused purely on extracting the maximum amount of revenues possible from Firdapse, or a company that can show it is capable of strategic M&A, new drug development, and securing new drug approvals to complement the success of Firdapse.

The company's current valuation of $1.6bn is nearly 8x forecast 2022 revenues, and based on net income of ~40m in 2021, current price to earnings ratio is ~40x. These are not especially attractive ratios, so although there may be many more Firdapse patients to try to uncover and supply with the drug, Catalyst may have to face up to the cold reality that by 2026, Firdapse revenues will have already peaked.

Perhaps management can find a way to grow revenues >$500m per annum in the meantime, and keep its valuation buoyant, but I think the Teva situation may be threatening enough to drive the share price lower than it is today, and to force investors to ask themselves how low it may go.

Perhaps a share price <$10 could represent a buying opportunity, based on management's successful overturning of the FDA / Jacobus rulings. It would take a brave investor to bet on Catalyst long term based on the promise of Firdapse alone, however. It may be time to see what other profitable drugs management may be able to acquire using its >$250m pile of cash.

For further details see:

Catalyst Pharmaceuticals: Teva's Patent Challenge Of Firdapse Could Spell The End For This Cash Cow