CAT - Caterpillar: 5 Reasons Why You Should Consider Buying This Blue-Chip Aristocrat

2023-11-24 10:00:00 ET

Summary

- Caterpillar is a dividend aristocrat with a strong business model and a long track record of paying out dividends.

- The company has a conservative growth outlook with steady earnings and cash flow growth expected in the next two years.

- Caterpillar has a strong balance sheet and is currently undervalued, making it an attractive investment opportunity.

- The company does expect weaker sales in China and Europe going forward. Additionally, dealer inventory is expected to decrease in the 4th quarter compared to Q4 '22.

- If the economy does fall into a recession, CAT could experience a decline in finances like it did during the GFC.

Introduction

One thing I love doing is researching and finding dividend stocks to buy that are undervalued or at a fair price. It's even better when the stocks are blue-chips trading at reasonable prices. These are stocks to help you sleep well at night because they seem to do all the right things. Grow their cash flows, maintain a strong balance sheet, and operate a business that's going to be around for a very long time.

One stock that comes to mind is Caterpillar Inc. ( CAT ). They are a dividend aristocrat that has been around since the early 1900s. And I think it's safe to say they'll probably be around well after me and those reading this article are gone. These are the type of stocks I prefer to invest in because as I mentioned earlier, they are blue-chip SWANs. In this article, I get into why you should consider holding this blue-chip stock, especially if you love collecting dividends and plan to hold it for a long time.

#1 Strong Business Model & MOAT

So, the question is why Caterpillar? Well for starters the stock is a dividend aristocrat. So that means it has a long track record of paying out dividends. 25 years of a growing dividend is nothing to sneeze at. Yes, there are plenty of aristocrats on the market that pay a growing dividend. But CAT has been crushed in the last 3 months. In August the stock was trading near the $300 level at $286 and recently touched $226 before bouncing back to its current price of $246 at the time of writing.

How many times do we drive to work or anywhere for that matter and see a ton of construction? Or go into a place of business like a mall or our favorite store and see things being renovated? Well, it takes equipment to get that work done and there's a high likelihood that the equipment being used is Caterpillar. The company manufactures and sells construction & mining equipment. They also sell off-highway diesel & natural gas engines, industrial gas turbines, and diesel-electric locomotives. They provide all types of tools, vehicles, and equipment for various jobs.

CAT investor presentation

So, you have to ask yourself? Will businesses always need work done? Companies will always need additional things built, or new businesses whether that is a new hotel or a new home that needs to be constructed. As long as that happens, there will always be a need for equipment to do the job with. So, is that a company you would want to consider investing in? One that's needed and will be for a long time? One that has a strong MOAT like Caterpillar? In my opinion, the answer is yes. But a question an investor should ask themselves is: Can the business continue growing and what does its future growth picture look like?

#2 Conservative Growth Outlook

One may say, Why is conservative growth a reason to choose Caterpillar? I prefer stocks that return double-digits and outperform. Of course, we all would love those but I like businesses that are more conservative. Just a personal preference. Like the story of the hare & the tortoise. Slow and steady wins the race usually. Caterpillar's earnings have grown 9.9% per year over the past 5 years and are forecasted to grow nearly 3% per annum. Like I always say some growth is better than no growth. And although this is expected to be lower than the past 5 years, I'll take the near 3% growth. I prefer businesses that are boring and conservative. A true steady eddy. And CAT is just that. A stock that offers low single-digit growth but continuously performs year after year.

{kind=link}

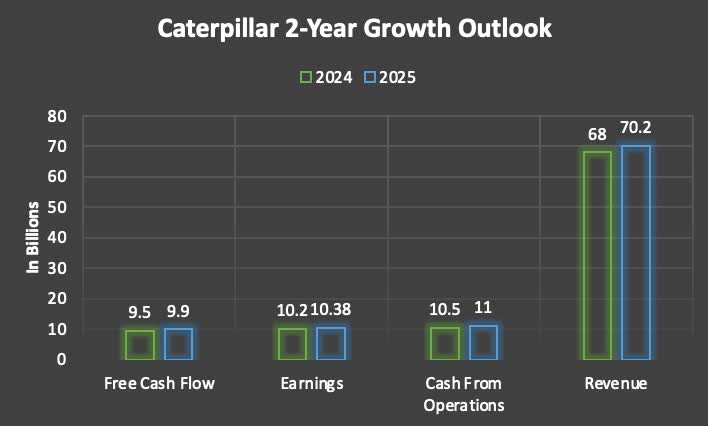

Earnings and revenue are expected to grow the least posting 1.7% and 3.2% while both cash from operations and free cash flow are expected to grow 4.2% and 4.7% respectively over the same period. That's an average of nearly 3.5% growth over the next two years. It's always better to manage expectations than to get overly confident. Due to the macro-economic environment and the looming recession still expected 3 and a half percent growth is good in my opinion.

During the latest earnings management stated they expect full-year 2023 results to be better than anticipated. That's because sales and revenue increased 12%. Adjusted operating profit margin also improved to 20.8%, up year-over-year. They also generated $2.8 billion FCF in the quarter bringing the total to $6.8 billion YTD. They also returned a total of $4.1 billion to shareholders through share repurchases and dividends paid.

CAT investor presentation

This year they've managed to repurchase $2.2 billion worth of shares and paid $1.9 billion in dividends. At quarter end they had a total of 510 million shares outstanding, and they have decreased this by 14.3% in the past 5 years. Free cash flow is also expected to exceed the previous $4 billion-$8 billion target range for the full year.

#3 Strong Balance Sheet

Another metric that makes a stock a blue-chip is a strong balance sheet . At the quarter's end, CAT had $6.5 billion in cash and a very strong interest coverage ratio. Furthermore, they had an additional $4.3 billion in slightly longer-dated liquid marketable securities to improve yields on the cash on the balance sheet. Additionally, in comparison to its peers, it also has one of the lowest Net debt to EBITDA ratios at just 0.47x, well below peers Cummins Inc. ( CMI ) 1.10x, and Deere & Company ( DE ) 1.10x. The company's debt has increased slightly in the last 5 years, but cash & debt have relatively stayed similar. In comparison to its peers, Caterpillar does have a substantially larger debt load which may concern investors due to the current high interest rate environment but a blue-chip with a strong MOAT such as CAT presents no worry.

#4 Undervalued

Currently, CAT trades at a forward P/E OF 12.75x, below the 5-year average of 18x and the sector median of 20x, indicating it could be undervalued. Furthermore, The Goldman Sachs Group, Inc. ( GS ) equity team suggested investors should focus on beaten-down cyclicals as they present an opportunity for capital appreciation. Me, personally, I think the stock is slightly undervalued and like it in the $220-$230 range. But those with a long-term outlook could be getting the stock at a decent price. If you want a larger margin of safety to its price target, I suggest waiting for a pullback like the one earlier this year in May or the end of October.

{kind=link}

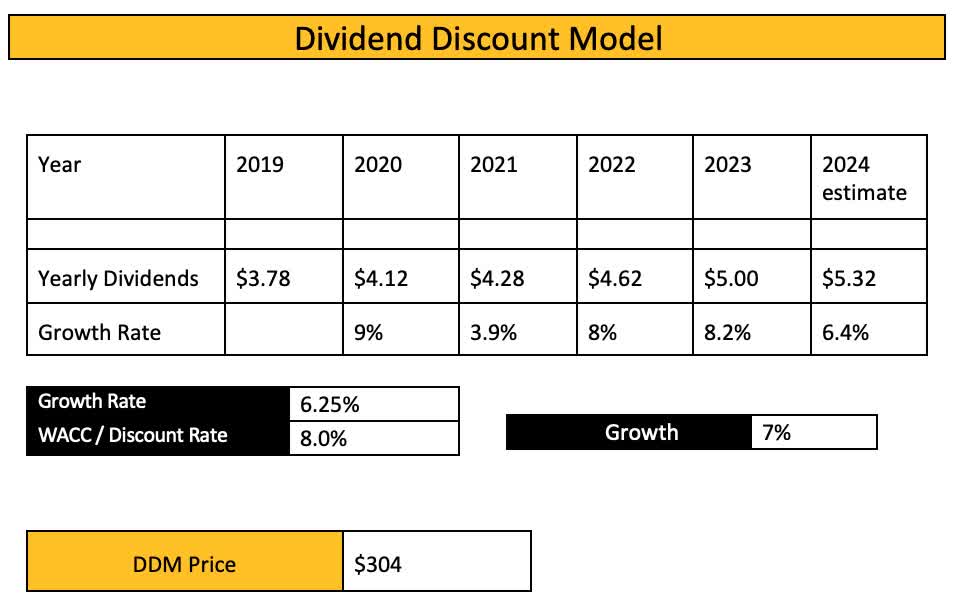

Using the Dividend Discount Model, I have a current price target of $304, roughly $10 higher than the 52-week high. Of course, several factors can affect this going forward. In the past few years CAT has had near double-digit dividend growth and using next year's estimate of $5.32, this gives investors a 23% upside, making it a buy.

{kind=link}

#5 Robust Dividend Growth

Speaking of the company's dividend growth, as you can see from my dividend discount model chart, Caterpillar's dividend growth has been pretty impressive over the past 5 years. Since then, the heavy equipment maker has increased the dividend by over 51% from $0.85 to $1.30. Currently, they have over 32 years of dividend increases and even managed to increase the dividend during the Great Financial Crisis in 2008. Next year's increase is expected to be slightly lower than the last two years, but I think this is still impressive considering the looming recession which is still expected in 2024. With their share repurchases over the years and very low earnings & free cash flow payout ratios, I expect CAT to continue delivering mid to high single-digit increases for the foreseeable future.

Risk Factors

Due to the current macro environment, the company expects sales weakness in China and Europe to continue. China is expected to be well below its typical 5%-10% enterprise value sales. In EAME they expect the region to be down due to continued weakness in Europe but is expected to be offset by strong demand in the Middle East. Furthermore, Latin America's construction activity is expected to be flat vs strong performance in 2022.

The company is also expecting a dealer inventory decrease in the coming quarter this year, versus an increase in the fourth quarter of 2022. Another risk could be a recession that is still expected. Although it is expected to be not as bad as the one in 2007-2009, it is to be noted that CAT did experience headwinds during that time. Caterpillar reported losses and laid off more than 22,000 workers in 2009. If the economy does indeed fall into a recession, unemployment will likely rise, and this could have a potential effect on the business.

Investor Takeaway

Caterpillar is a dividend aristocrat that according to the dividend discount model and dividend yield theory, is currently undervalued. This blue-chip stock offers investors a double-digit upside and is a premier sleep well at night stock. Additionally, they have a strong MOAT and a business that will thrive when the economy settles out and gets back to normal. Although a recession is still expected, I do see Caterpillar being affected by a slowing economy but still offers a safe haven for dividend investors due to its low earnings & FCF payout ratio, and strong balance sheet. Furthermore, the company continues to grow its finances, and this is expected to grow over the next two years due to share repurchases and a strong business model. Due to the 5 factors, I listed above, I think Caterpillar is a buy.

For further details see:

Caterpillar: 5 Reasons Why You Should Consider Buying This Blue-Chip Aristocrat