CAT - Caterpillar: A Good Value Opportunity

2023-06-27 05:05:09 ET

Summary

- Caterpillar stock is an attractive investment option due to its upside potential, solid dividend yield, and rich history of dividend growth.

- The company demonstrates strong financial performance amid the current economic turmoil, with expanding profitability metrics and a healthy balance sheet.

- Risks to consider include global economic trends, geopolitical and economic factors, and exchange rate fluctuations.

Investment thesis

My first Caterpillar ( CAT ) stock coverage stock did not age well, though I have a long-term mindset about the company. The stock substantially underperformed the broad market over the past three months, and I see this recent weakness as a good investment opportunity. According to my analysis, the company demonstrates stellar financial performance even amid the current economic turmoil, and the stock looks very attractively valued. Therefore, I reiterate "Buy" for CAT stock.

Recent developments

The company released its latest quarterly earnings on April 27 , confidently beating consensus estimates in revenue and EPS. Revenue increased about 17% YoY, solid amid the challenging environment. It is essential to mention that the bottom line improved significantly, with a 70% YoY growth.

Seeking Alpha

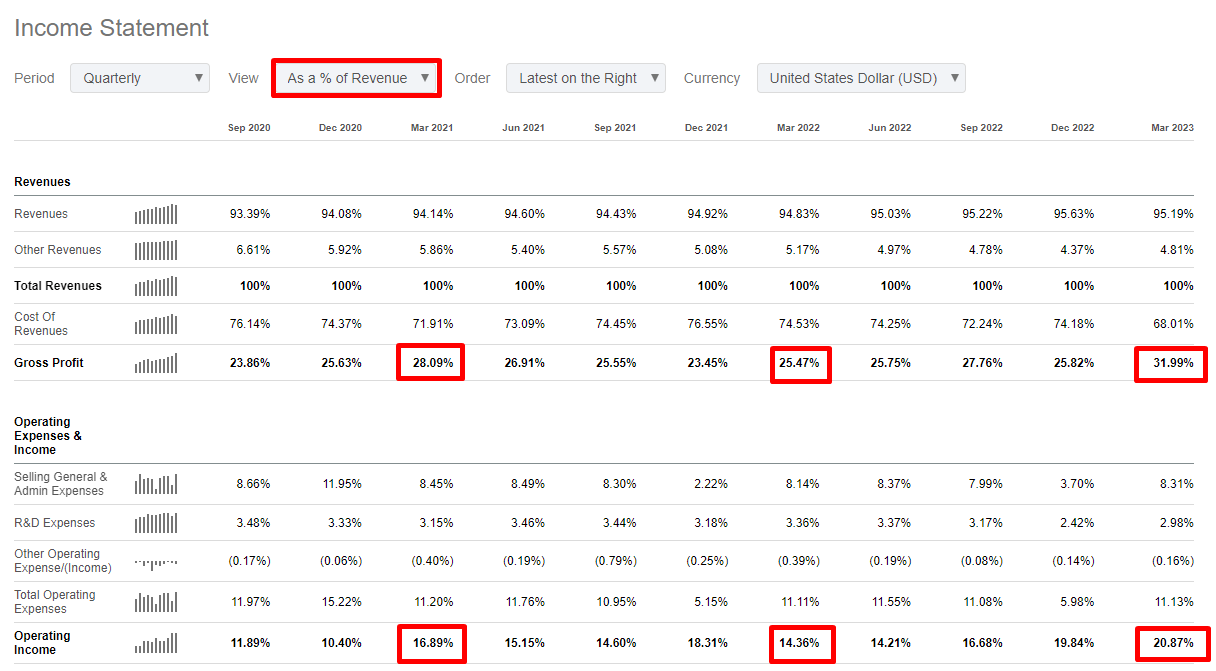

Sales growth demonstrates solid momentum with the ninth consecutive quarter with a double-digit YoY growth. I like that the company is expanding its profitability ratios, which is a high-quality sign in the current challenging environment of high inflation. It is also important to mention that current profitability ratios are even better than Q1 of 2021, when the macro environment was much more friendly than now.

{kind=link}

The Construction Industries [about 40% of the total Q1 sales] segment demonstrated a 10% increase driven by improved pricing that was partially offset by lower sales volume. I like that the segment's operating margin improved significantly, demonstrating about nine percentage points expansion. The increase in sales was mainly due to the strength in North America. In the Resource Industries segment [about 21% of the total Q1 sales], revenue demonstrated an impressive 21% growth. The increase was fueled by the higher prices as well as rising volume. This segment also demonstrated a comparable operating margin expansion. Last but not least, the Energy & Transportation segment also saw a solid 24% YoY increase in sales. Sales improved in all four subsegments - Oil & Gas, Industrial, Transportation, and Power Generation. The operating margin also significantly improved here. Substantially improved profitability metrics are a very bullish sign for me. It means that the management is succeeding in keeping an eye on costs.

On June 14, the company increased its quarterly dividend by 8%, which signals the management's confidence in the near term.

I agree that the company's future is bright because I see significant tailwinds for the company. First, Caterpillar will likely benefit from the near-term tailwinds of the U.S. infrastructure spending plans. Second, the overall increased demand for new roads in emerging markets due to urbanization is also a sizeable secular headwind.

During the latest Bernstein's Annual Strategic Conference, Jim Umpleby, the CEO, underlined the importance of operational excellence over the recent years, which enabled the company to demonstrate expanding margins. I like the management's strong commitment to delivering more shareholder value, and the stellar dividend consistency of the company gives me a high level of conviction that CAT will continue improving its profitability metrics.

The strong growth momentum is still in place. I think so because consensus estimates forecast about $16.5 billion in revenue for the upcoming quarter's earnings, which is 16% higher YoY. The adjusted EPS is also expected to improve significantly from $3.18 to $4.54. The upcoming quarter's earnings are expected to be announced on August 2.

The balance sheet is in good shape, with more than $6 billion in cash and sound liquidity metrics, even if we deduct inventory.

Valuation update

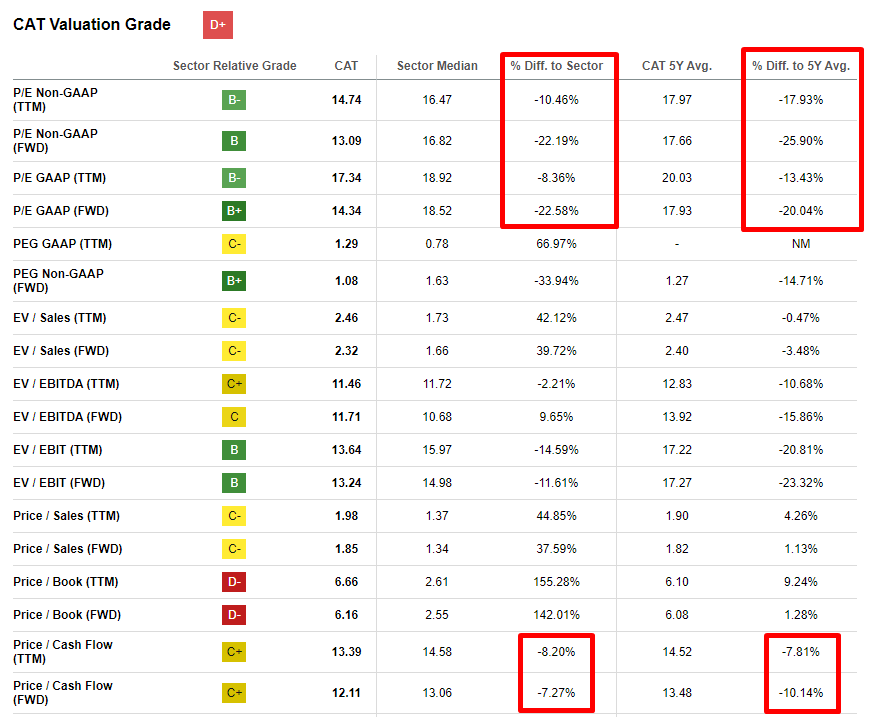

The stock significantly underperformed the broad market year-to-date with an almost flat dynamic. CAT has a relatively low "D+" grade from Seeking Alpha Quant . This is mainly due to high price-to-book ratios. On the other hand, multiples related to earnings and FCF are lower than both the sector median and 5-year averages. To me, this indicates undervaluation.

{kind=link}

Please also let me conduct a dividend discount model [DDM] analysis to cross-check the multiples analysis outcome. I use a 9% WACC, which is close to the suggestion from valueinvesting.io . I use the FY 2024 consensus estimate for the current dividend consensus estimate, which is $5.23. I expect dividend growth to be at 7%, which aligns with the CAT's last 3-year dividend CAGR.

Author's calculations

With all the assumptions incorporated into the DDM formula, we see that the stock is about 10% undervalued with a fair share price of about $262.

Overall, both valuation approaches suggest that the stock is attractively valued. It is also important to mention that the stock offers investors a decent 2.2% forward dividend yield and a history of 29 consecutive years of dividend growth.

Risks update

Investing in Caterpillar stock is not without risks. The company is exposed to various operational and financial risks that could impact its performance.

Caterpillar's performance is closely linked to global economic trends. Weakness in the construction and mining industries, which are sensitive to economic cycles, can adversely affect the demand for Caterpillar's products and services. Following the Great Recession, the recovery was driven by increased commodity demand, which prompted mining companies to ramp up production to meet emerging market demand. However, going forward, fixed asset investment growth in China, a major consumer of these commodities, is expected to be below historical levels.

A significant portion of the company's revenue is generated globally. Therefore, CAT is exposed to risks related to its global operations. One of the main risks is the potential impact of geopolitical and economic factors. Political instability, changes in government policies, and regulatory changes in various countries can significantly adversely affect Caterpillar's operations. Restrictions on international trade, tariffs, and trade barriers can disrupt supply chains and increase costs for the company, which may affect its earnings. Exchange rate fluctuations also pose a risk to Caterpillar's financial performance. An appreciation of the U.S. dollar against other currencies may reduce the value of foreign revenues when translated back into dollars, which may affect the company's profitability.

Bottom line

Overall, I think Caterpillar stock is an attractive option, given its upside potential, solid dividend yield, and rich history of dividend growth. The company demonstrates solid financial performance even under the current harsh environment. Profitability metrics are expanding, and the balance sheet is in good shape. Therefore, I reiterate the "Buy" rating for CAT stock.

For further details see:

Caterpillar: A Good Value Opportunity