CAT - Caterpillar: A Surprising Strength You Shouldn't Overlook

2023-06-20 03:40:13 ET

Summary

- Caterpillar's Q1 2023 financial results exceeded Wall Street analysts' expectations, with all core segments showing year-over-year revenue growth.

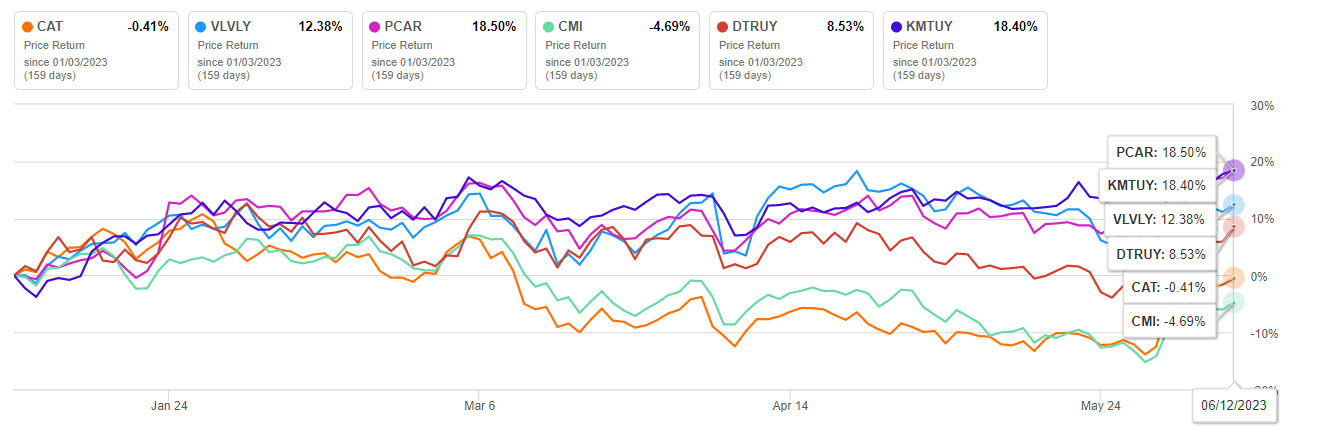

- Despite positive financial results, Caterpillar's share price declined by 0.41% since the beginning of 2023, underperforming compared to main competitors in the industrial sector.

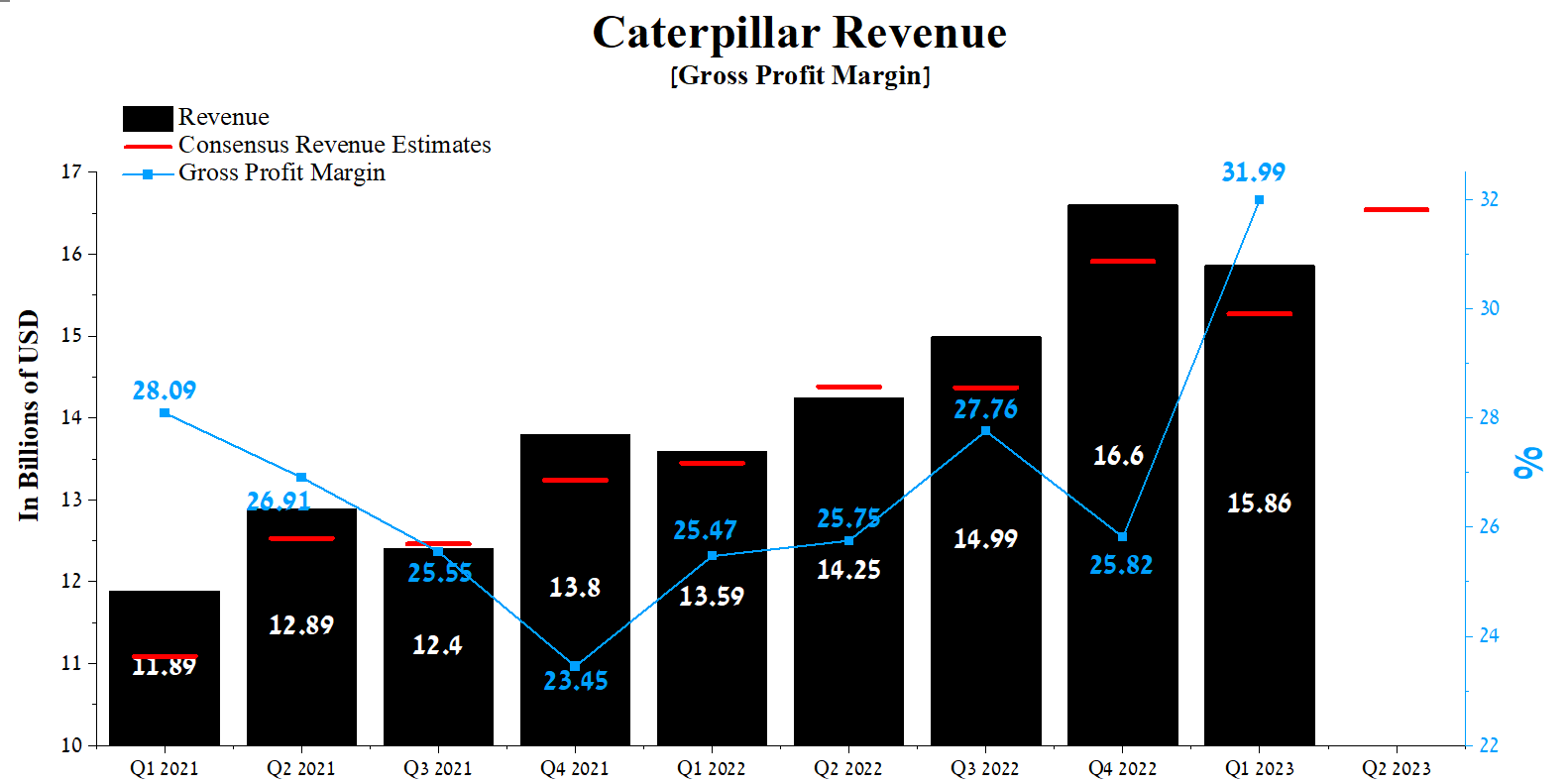

- The company's Q1 2023 revenue was $15.86 billion, a 16.7% increase from the same period in 2022.

- Caterpillar's gross margin was 31.99% in Q1 2023, the highest since the start of the COVID-19 pandemic, despite increased SG&A and R&D spending.

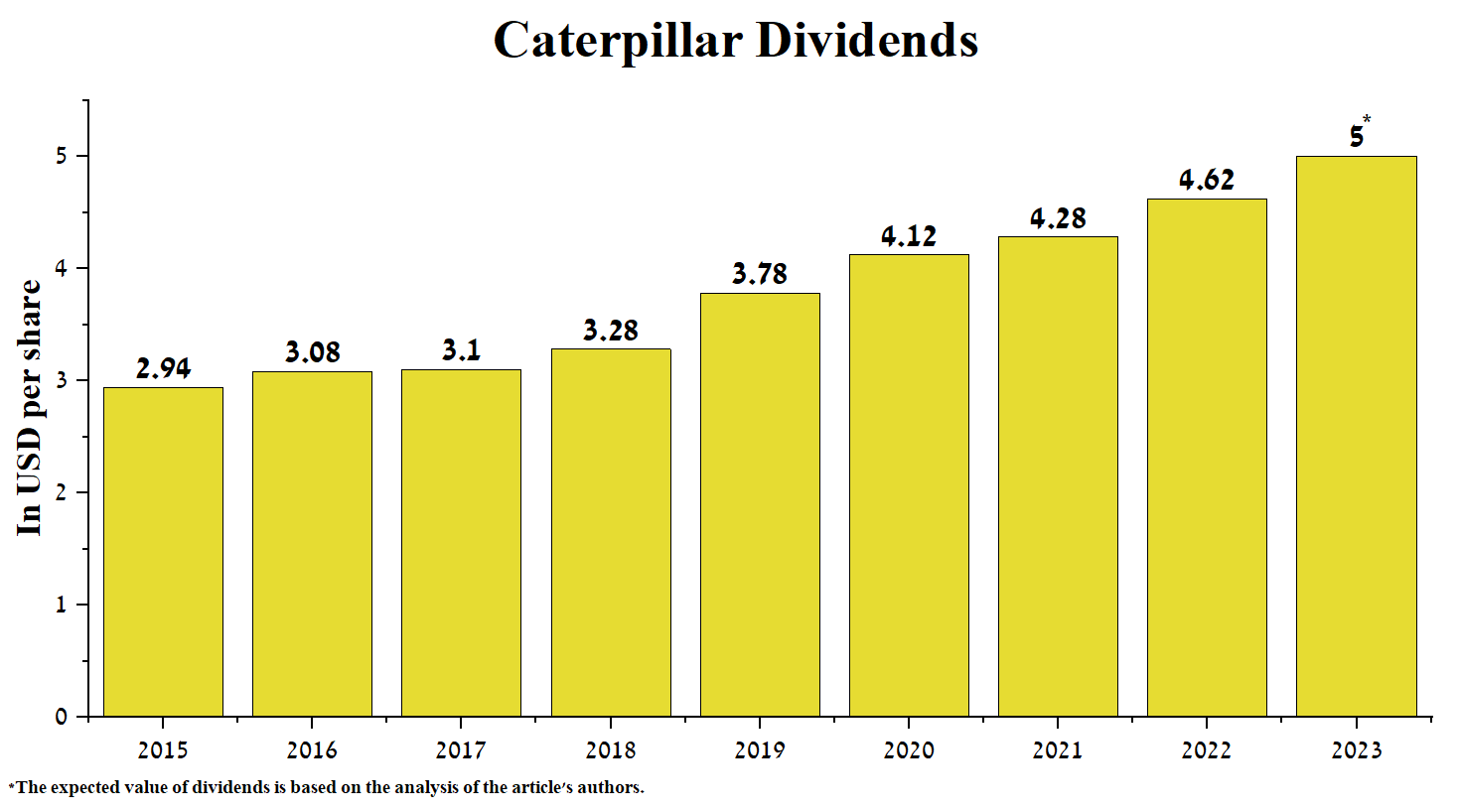

- In addition, with debentures and senior bonds due between 2023 and 2097, we do not expect Caterpillar to have any problems with their redemption, and the company's management will continue to increase dividend payments and pursue an active share buyback program.

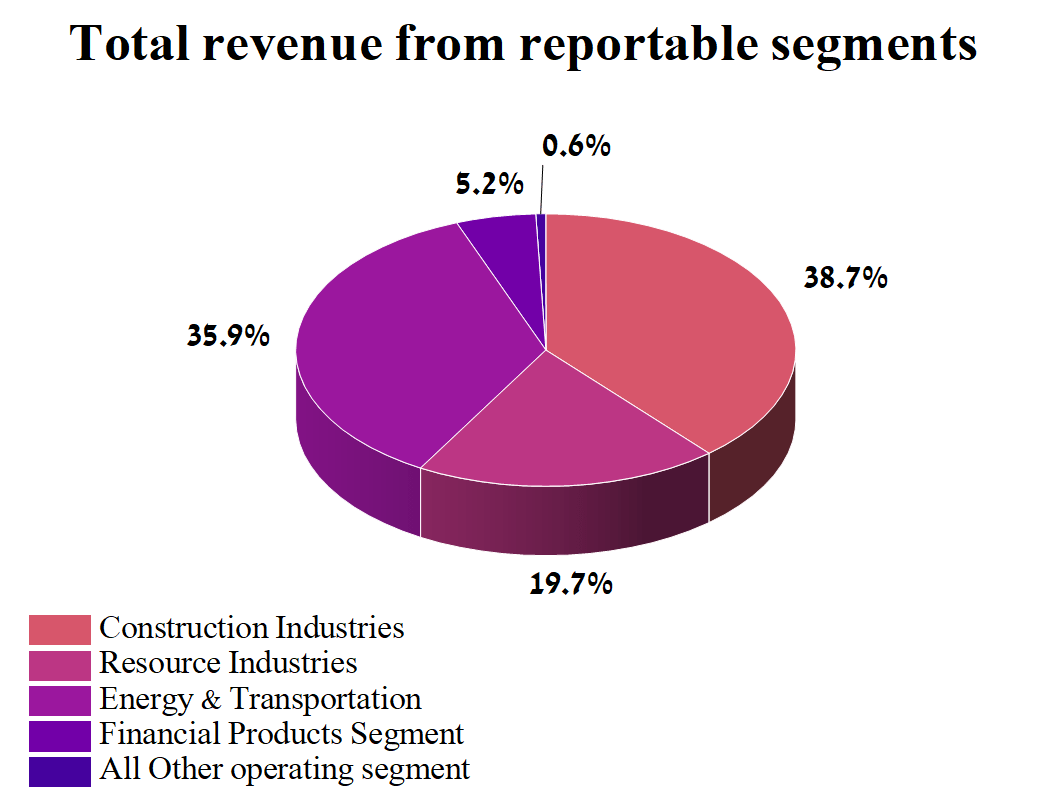

Caterpillar (CAT) is a leading manufacturer of construction and mining equipment, industrial gas turbines, diesel, and natural gas engines, serving customers in 192 countries. The company's activities focus on core segments such as the Construction Industries, Resource Industries, energy, Energy & Transportation, and financial product segment, which provides clients financing.

Author's elaboration, based on 10-Q

{kind=link}

On April 27, 2023, the company released financial results for the first three months of 2023, which not only beat Wall Street analysts' expectations but demonstrated that Caterpillar's four core segments continue to grow year-over-year in revenue, driven by higher equipment sales to clients. But even so, since the beginning of 2023, Caterpillar's share price has shown a decline of about 0.41%, which is significantly worse than that of such main competitors in the industrial sector as PACCAR ( PCAR ), Komatsu ( KMTUY ) and AB Volvo ( VLVLY ).

Author's elaboration, based on Seeking Alpha

{kind=link}

We initiate our coverage of Caterpillar with an "outperform" rating for the next 12 months.

Caterpillar's Financial Position

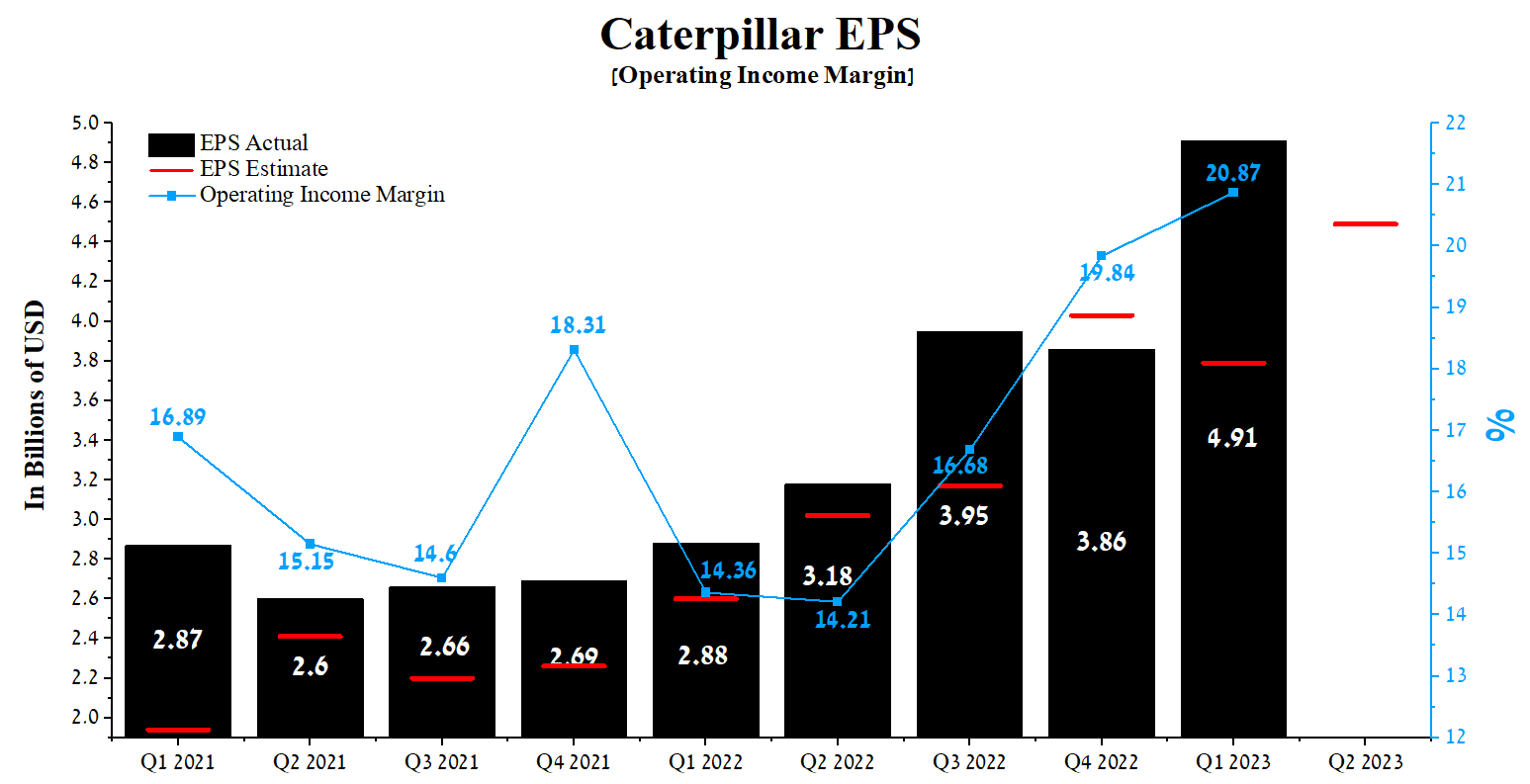

Caterpillar's revenue for the first three months of 2023 was $15.86 billion, down 4.5% from the previous quarter and up 16.7% from the first quarter of 2022. At the same time, Caterpillar's actual revenue has beaten analyst consensus estimates in seven of the last nine quarters, indicating that Wall Street has underestimated its successful performance during the current favorable period for the industry.

Author's elaboration, based on Seeking Alpha

{kind=link}

The Construction Industries segment's revenue was $6,746 million in the first three months of 2023, up 10.3% year-on-year, driven by a better price realization and reduced supply chain pressure following the end of the COVID-19 pandemic. Sales in North America were a key contributor to the segment's revenue growth, driven by higher sales volumes due to increased dealer inventories, anticipating higher demand for the company's products as macroeconomic conditions improve in the region.

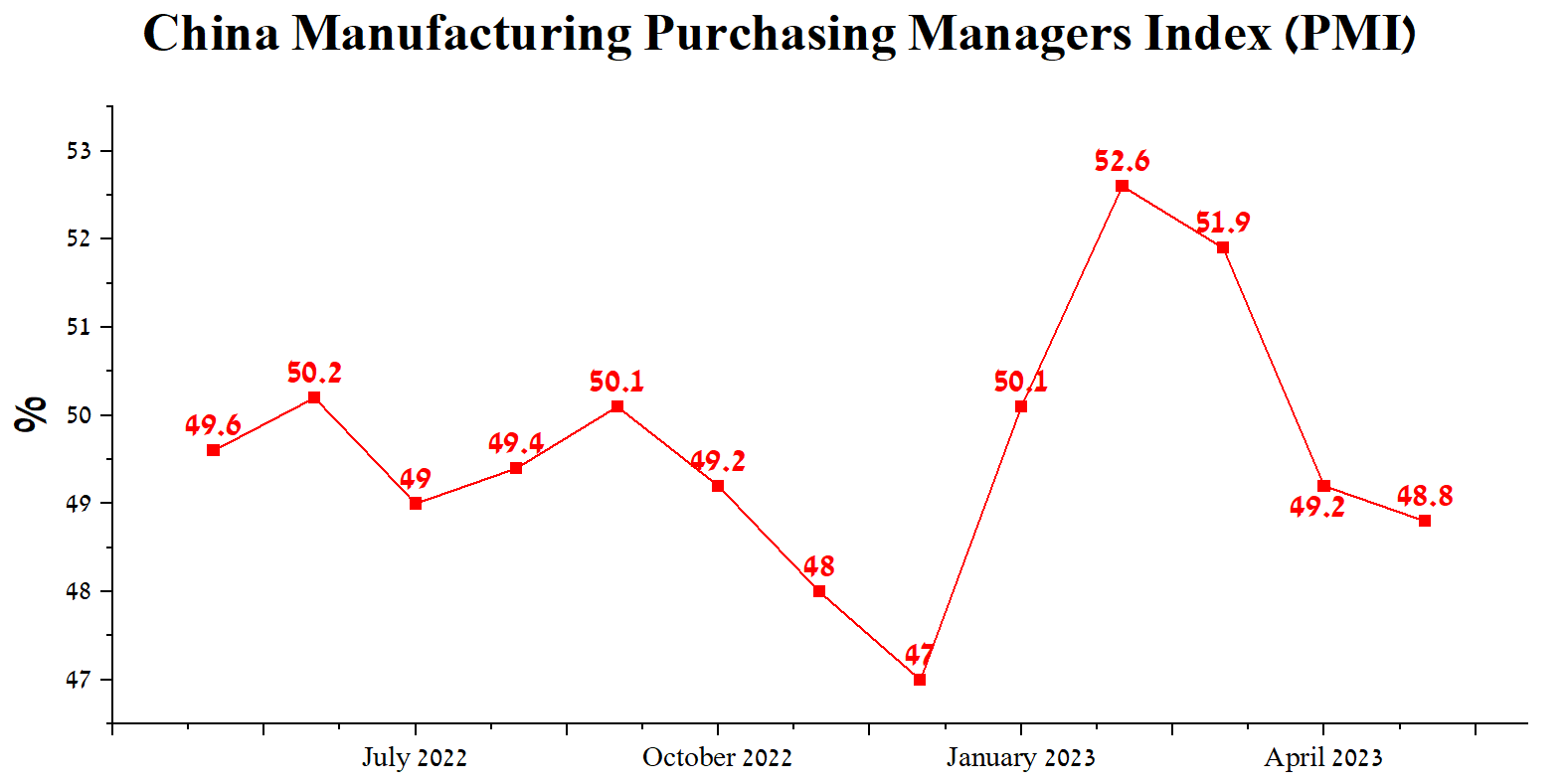

But at the same time, the slow recovery of factory activity in China continues to affect the construction activity in the country negatively. So, in May, the PMI of the manufacturing industry in China amounted to 48.8%, continuing the downward trend that began in February 2023.

Author's elaboration, based on the National Bureau of Statistics of China

{kind=link}

At the same time, the Energy & Transportation segment's revenue of $6,254 million in 1Q 2023 continued to grow year-on-year despite the strengthening of the Chinese yuan and the euro against the US dollar. In addition, we believe the Ukrainian-Russian conflict will positively impact this segment's financial position, which will keep demand for reciprocating engines and Caterpillar's gas compression engines strong. One of the main reasons for this is the construction of LNG terminals and the active modernization of refineries by the countries of the European Union to reduce the consumption of Russian fossil fuels and improve their energy security in the run-up to winter.

Caterpillar's revenue for Q2 2023 is expected to be $16.12-17.27 billion, up 8.3% from analysts' expectations for Q1 2022. We believe that most of the revenue growth will come from various factors. One is the positive impact of the Inflation Reduction Act approved by President Biden in mid-August 2022 and a bill aimed at over $1 trillion in U.S. infrastructure improvement and modernization, passed in November 2021 .

So, in the second quarter of 2022, one can observe an increase in the volume of construction of non-residential premises in the United States. Moreover, the Asia-Pacific region continues to increase public spending on infrastructure. Overall, we expect lower natural gas prices in Europe to play a significant role in recovering economic activity relative to 2022, eventually boosting construction volumes.

Also, thanks to two years of high freight rates that have led to record profits in the shipping industry, there will be an increased need to modernize aging fleets and purchase new ships powered by Caterpillar's generator sets and diesel engines.

Caterpillar's gross margin was 31.99% in Q1 2023, the highest since the start of the COVID-19 pandemic, despite increased SG&A and R&D spending. Moreover, this financial indicator is not only higher than that of the industrial sector but also that of such major competitors as Cummins ( CMI ), Daimler Truck Holding ( DTRUY ), and AB Volvo, which is another factor that attracts investors to choose Caterpillar as a long-term investment.

We forecast that Caterpillar's gross margin will reach 33.6% by 2023 and grow to 35.2% by 2024, driven by increased sales in the company's key business segments and reduced inflation in the US, Japan, the European Union, and China.

Caterpillar's operating income margin in Q1 2023 was 20.87%, a significant increase from the previous year and the previous quarter. The company's earnings per share ((EPS)) for the first three months of 2023 was $4.91, up 27.2% quarter-on-quarter, and last but not least, it continued to beat analyst consensus estimates in recent quarters.

Moreover, Caterpillar's Q2 EPS is expected to be in the $3.75-$5.09 range, up 18.5% from the Q1 2023 consensus estimate. Caterpillar's Non-GAAP P/E [TTM] of 15.43x is 7.61% less than the sector's average and 14.18% less than the average over the past five years. On the other hand, P/E Non-GAAP [FWD] is 13.69x, which is one of the factors indicating that the company is undervalued during the current period of global economic recovery and an increase in construction volumes.

Author's elaboration, based on Seeking Alpha

{kind=link}

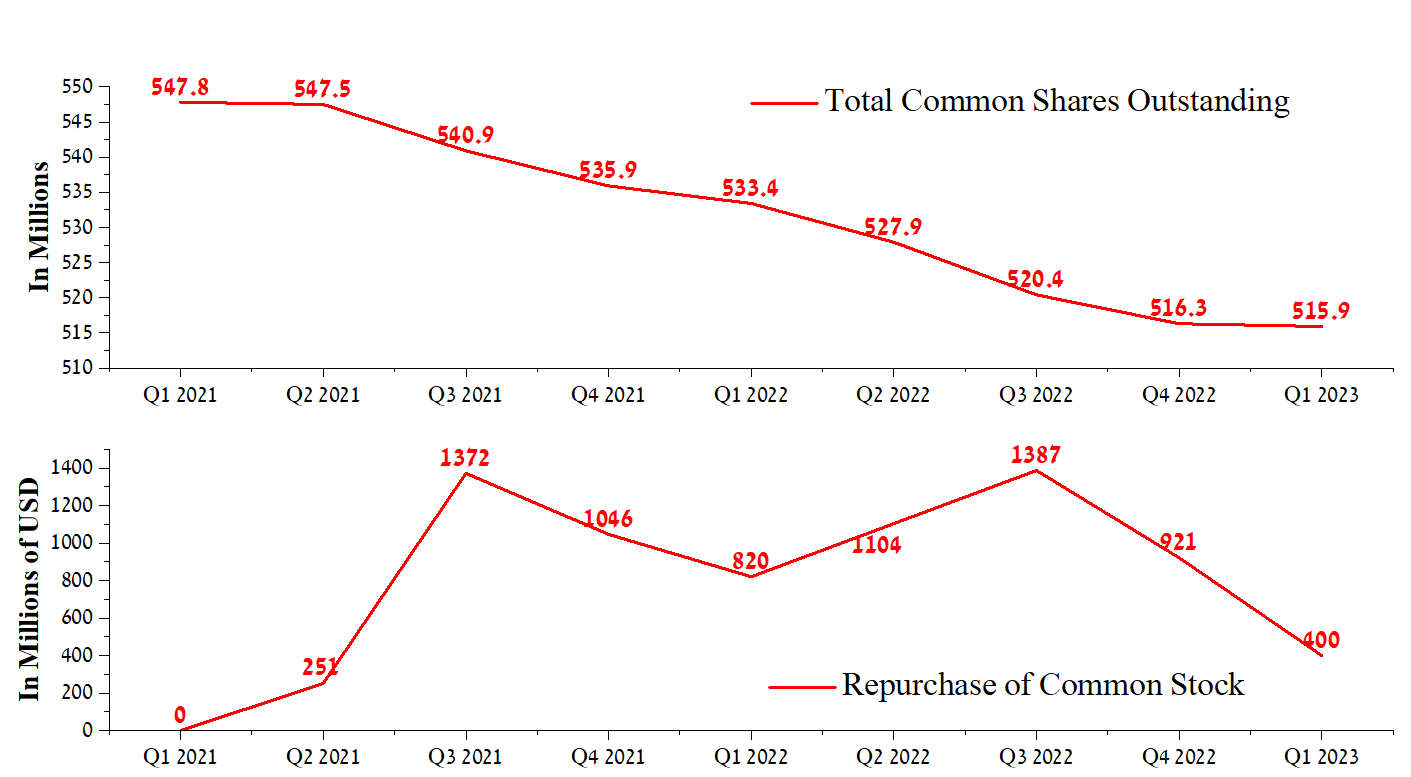

In addition to improving the margins of Caterpillar's segments, beating EPS is also related to the share repurchase program. For the first quarter of 2023, Caterpillar bought back its shares for about $400 million, while Jim Umpleby is still authorized to buy back Caterpillar shares for $12.4 billion . We estimate that this will keep the company's share price in an upward direction even if the S&P 500 ( SPY ) price corrects due to the decline in AI hype in the media.

Author's elaboration, based on Seeking Alpha

{kind=link}

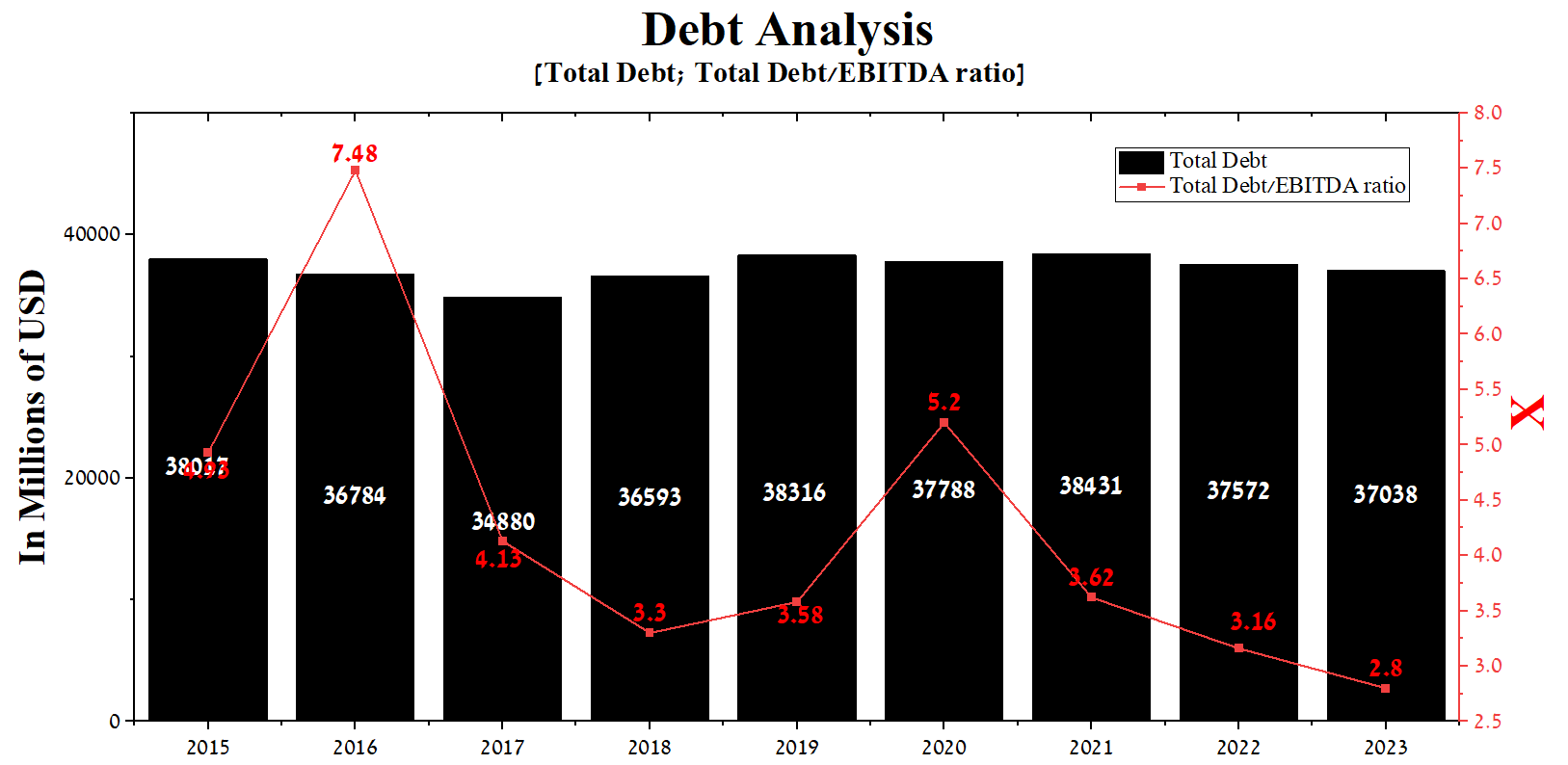

At the end of the first quarter of 2023, Caterpillar's total debt was about $37.04 billion, down slightly from 2021. But more importantly, thanks to the growth in the company's EBITDA in recent years, the total debt/EBITDA ratio has dropped from 3.62x to a record low of 2.8x for Caterpillar.

Author's elaboration, based on Seeking Alpha

{kind=link}

In addition, with debentures and senior bonds due between 2023 and 2097, we do not expect Caterpillar to have any problems with their redemption, and the company's management will continue to increase dividend payments and pursue an active share buyback program.

{kind=link}

Conclusion

Caterpillar is a leading manufacturer of construction and mining equipment, industrial gas turbines, diesel, and natural gas engines, serving customers in 192 countries.

With the recovery of the global economy, easing supply chain pressures, and the positive impact of the Inflation Reduction Act approved by President Biden in 2022 and the trillion-dollar infrastructure investment bill passed in November 2021, we expect this to lead to growth in revenue and net profit in such vital segments as the Energy & Transportation, Construction Industries, and Resource Industries.

Despite the geopolitical tensions caused by the conflict between Ukraine and Russia, tense relations between China and the United States, including over Taiwan, and the strengthening of the US dollar, Caterpillar's management has not only paid dividends for more than twenty-eight years in a row, but also increased them, and thereby this increases confidence in the CEO of Caterpillar in his ability to manage the company effectively.

However, due to the declining AI hype in the media, we expect the S&P 500 to drop to $4292-$4300, eventually leading to a short-term correction in Caterpillar's share price to $235-236 per share in the next few weeks.

We initiate our coverage of Caterpillar with an "outperform" rating for the next 12 months.

For further details see:

Caterpillar: A Surprising Strength You Shouldn't Overlook