CAT - Caterpillar: Beware The Dip

2023-09-11 12:51:15 ET

Summary

- Caterpillar has reported impressive financial figures recently with a 22% increase in revenues and a rise in operating profit from 13.8% to 21.3%.

- Despite having a large amount of debt, the company's leverage and coverage ratings are good, and it maintains a mid-A rating.

- The positive pricing environment has supported the company's current value, but a shift in this environment could lead to a significant dip in earnings and stock price.

Introduction

Caterpillar ( CAT ) has posted impressive numbers over the last couple of quarters leading to a rally in the stock price. A dive into the financials however reveals that the current performance is being fueled by an increase in its Return on Capital ((ROC)) due to a favorable pricing environment. The current stock price would imply that the market has priced in this increased level of profitability as a new normal; however, should the ROC revert towards historical levels then a price correction is likely. Caterpillar is a dividend aristocrat, and the stock has a history of increasing in value over the long term and for these reasons I would rate it as a hold. In the short term however, a fall from its current high may be on the cards.

Recent Performance

If you have been following CAT, you won’t have failed to notice that they have been knocking it out of the park recently. In the most recent Q1 conference call , they announced that they were likely to significantly exceed their previous estimates for both revenues and earnings and this was reconfirmed in the Q2 call. As per the company’s own figures , Q2 revenues increased 22% over the prior year with adjusted operating profit increasing from 13.8% to 21.3% on the same comparison. The market has unsurprisingly reacted well to this performance and the stock price has been on a bit of a tear, reaching a record high of $288.65 at the start of August, and at the time of writing is up 19.5% for the YTD with an annualized return of 58.5% for the last twelve months. The company is also a proud dividend aristocrat and flush with cash from its recent performance, it has continued this trend, announcing an 8% increase in the dividend in June of this year which takes its growth to 51% since May of 2019.

Debt

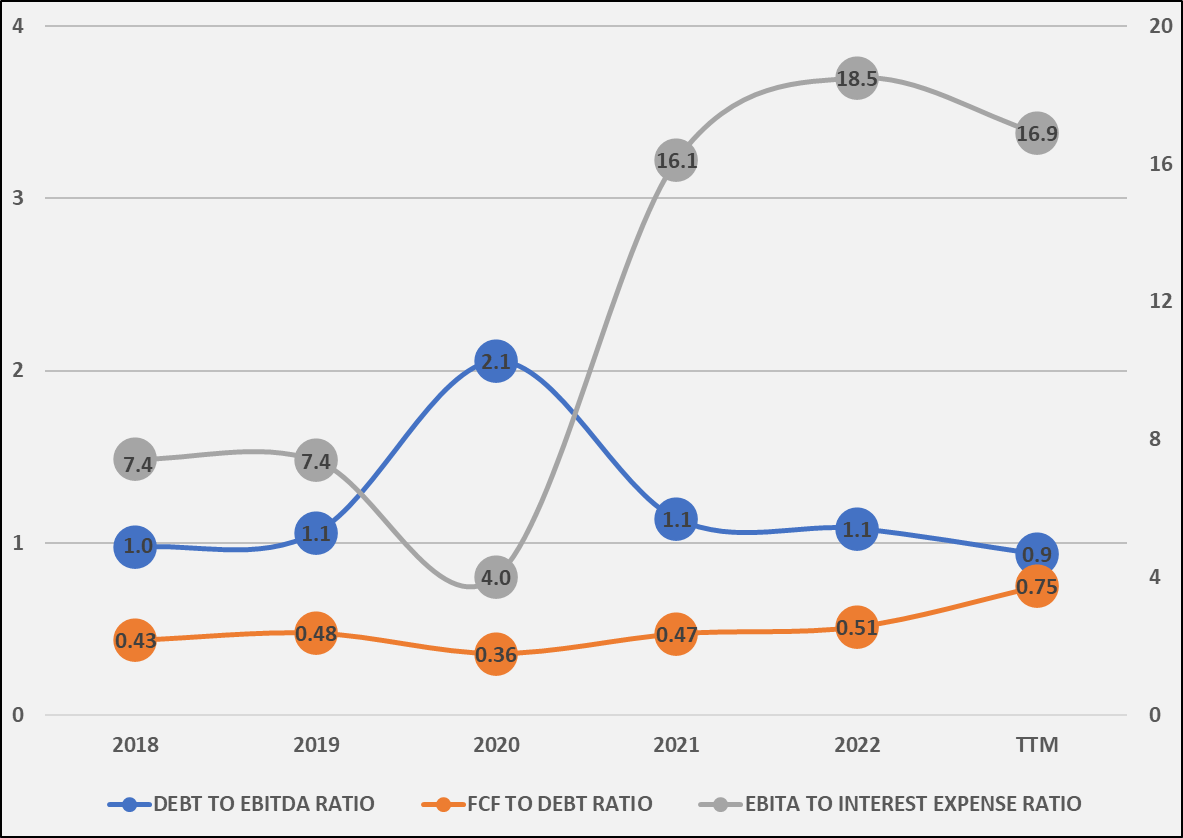

Given the current interest rate environment, when evaluating any company, we need to take a close look at the debt. In absolute terms, CAT has a mountain of it, with total debt currently sitting at $38 billion . The absolute value of your debt is not a problem however as long as you can afford to service it, and Caterpillar is actually in a pretty strong position. The majority of the debt ($28 billion) has been issued by Caterpillar Financial Services Corporation (CFSC), a separate division whose purpose is to provide financing to CAT customers and dealers. Stripping out CFSC, the leverage and coverage metrics are solid with Debt to EBITDA at 0.9, FCF to Debt at 0.9 and EBITA to Interest Expense at 16.9 over the trailing twelve months. These numbers have been improving over the last couple of years and are now in better shape than before COVID.

As it operates as a Captive Finance Company making loans secured on assets, the CFSC debt is a different animal to that of the parent and requires different metrics to evaluate it. The company provides some guidance however, reporting that CFSC is required by its creditors to meet certain covenants, the principal two being a leverage ratio of less than 10 and an interest coverage ratio of not less than 1.15 to 1. As per the last quarterly report, these metrics were sitting at 7.02 and 1.96 to 1 respectively indicating that leverage and coverage are within the acceptable range. The ratings agencies would seem to agree that CAT debt is of high quality with all three majors rating both CAT and CFSC in the mid A range with Fitch recently having upgraded both to A+.

{kind=link}

CAT Leverage and Coverage Metric (Authors Own Calculations)

Growth Drivers

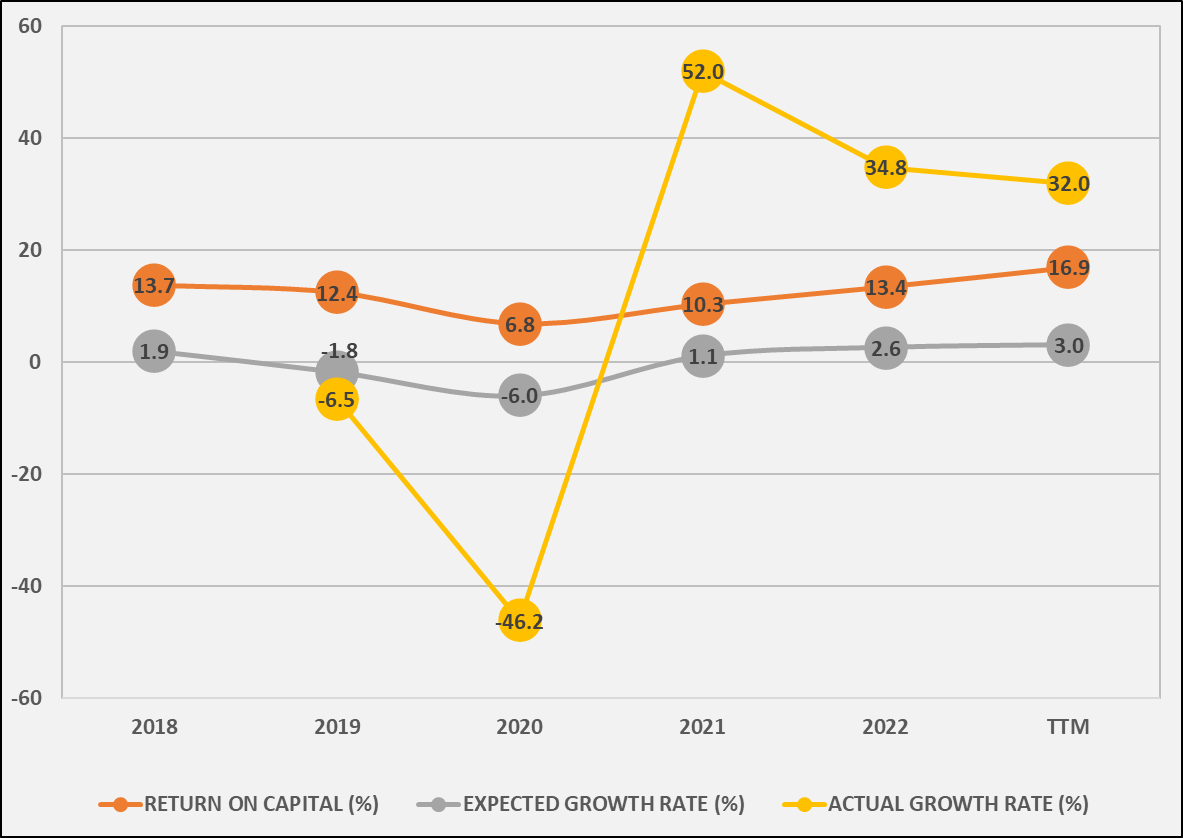

In the Q2 conference call , the company stated that they are currently benefiting from positive pricing tailwinds as well as increases in sales volumes as price increases have outpaced cost inflation. These favorable market conditions have resulted in CAT’s adjusted Return on Capital 1 (ROC) increasing to 16.9% in the TTM as compared to 13.4% for FY2022 and the pre-Covid level of 13.7%. If the ROC is steady, the expected growth rate should be according to the following equation:

Expected EBIT Growth Equation (Authors Reference)

What this equation tells us is that your expected growth in EBIT is a function of your Return on Capital (ROC) and your Re-investment Rate (RIR). If we apply this equation to CAT’s last 12 months (adjusted) ROC of 16.9% and (adjusted) RIR of 18% then EBIT should be growing at 3%, however the actual growth rate is over thirty. The additional growth is a result of the favorable pricing environment which currently enables the company to charge a premium for their products. This has fueled an increase in ROC over a relatively short period, providing an additional boost to Operating Profit growth without any significant change in other fundamentals 2 .

{kind=link}

CAT Groth and Profitability Metrics (Authors Own Calculations)

Outlook

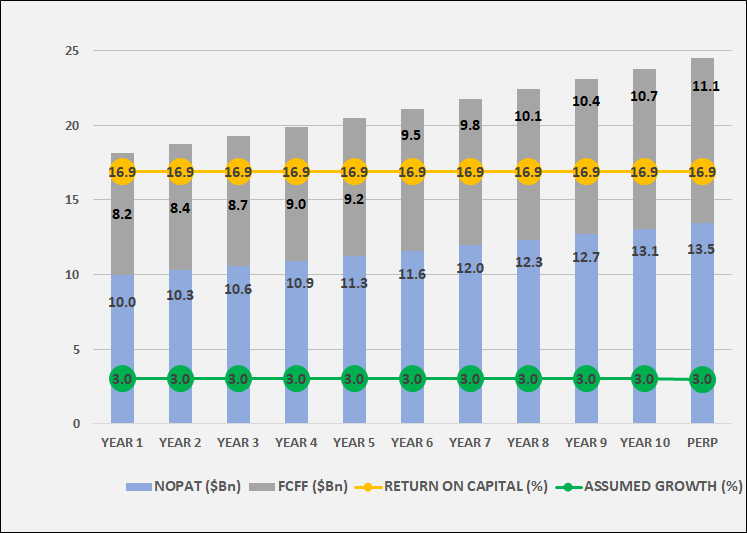

Plot 1 below shows the key figures from a DCF valuation that returns the current price of $286. To reach that value it was assumed that the company was already in the steady growth phase with expected growth of 3% (as discussed earlier) and the adjusted ROC steady at its current level of 16.9%. The same value of growth was also used in the perpetual phase; this value is in line with long term global GDP growth estimates , and so fitting for a large MNC like CAT. In the calculation, I used a WACC of 7.6% and a long-term market premium of 4% with the risk-free rate taken as the 10Y treasury yield. These figures return an increase in adjusted FCFF 3 from $7.8 billion at present to $9.2 billion after 5 years and $11.1 billion after 10 years.

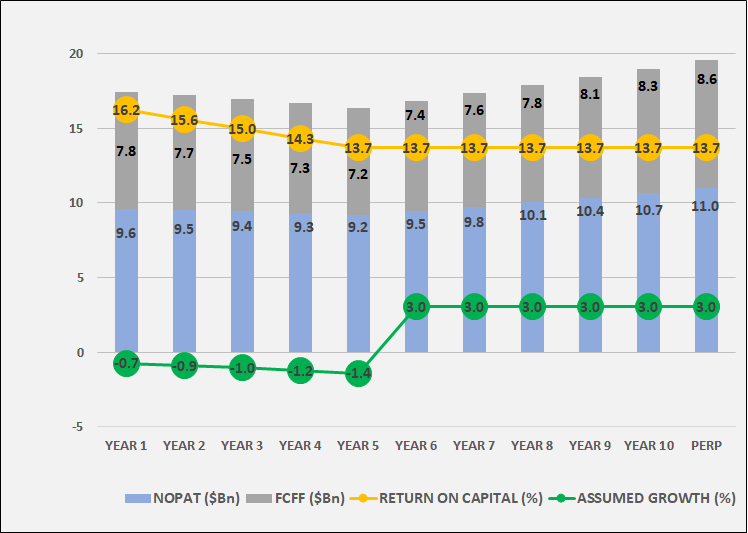

Plot 2 shows the key figures from a second DCF analysis, in this model, all inputs are identical to the first, however the ROC is assumed to reduce to its pre-COVID value of 13.7% over an initial five-year period. In the same way that a rising ROC is providing a boost to EBIT growth at present, a falling ROC has the opposite effect, 2 with this becoming negative if ROC returns to historical levels and only returning to expected levels when the ROC stabilizes. In this scenario, adjusted FCFF reduces to $7.2 billion after 5 years and $8.3 billion after 10, and the estimated value is only $216.

The market price therefore would appear to assume that the current positive pricing environment and level of profitability will continue indefinitely, however this may be a fragile assumption. As the below statement from the Q2 Call by CFO Andrew Bonfield shows, the company expects pricing tailwinds to ease towards the end of the year and whereas recession fears have recently subsided, the global economy isn’t exactly booming at the moment. If the current favorable pricing environment does recede, then you can expect CAT’s ROC to take a hit with a corresponding drop in both earnings and the stock price.

Price realization should remain positive that the magnitude of the favorability versus the prior year is expected to be lower in the second half as we lap the more favorable pricing trends from last year. Therefore, the increases in margins that we have occurred -- that have occurred from price outpacing manufacturing cost inflation should moderate in the second half of this year.

{kind=link}

Plot 1: Key Figures from a DCF Valuation of $286 (Authors' Own Calculations)

Plot 2: Key Figures from a DCF Valuation of $216 (Authors' own calculations)

{kind=link}

Risks

The lower DCF valuation assumes that CAT’s profitability as measured by its ROC will return to pre-COVID levels, and the majority of the current gains have come from the positive pricing environment. It should be considered however, that CAT’s Enterprise Strategy is to concentrate on areas that create value and that will deliver long-term profitable growth. This strategy has been in place since 2017 and so could be responsible for the increased levels of profitability. The company has also invested significantly in restructuring , with over $740 million being recorded over the last 3 years which would also be expected to improve profitability. We should also consider that the current favorable pricing environment could be around for a long while and even without the benefit of operational improvement, the current ROC can be maintained. In either of these cases, the current market price is fair value and an uptick in the global economy that boosts sales further could see the stock rise.

Recommendation

CAT is a great company, they make real products that matter to the global economy, they pay a regular dividend, and the value of the stock rises over the long term. One criticism that is often made however is that their returns are volatile. This is the nature of the company I’m afraid and with demand for their products at the mercy of macroeconomic factors, they will always be cyclical. At the moment however, they are riding high on the sweet spot of the demand curve and making hay while the sun shines.

CAT is not the type of company that you would normally buy to make a quick buck and if you have a long position and can ride out any peaks and troughs, then the stock is a clear hold. Where it goes in the short term however depends on whether profitability can be maintained at present levels. The current stock price implies that this is a new normal, and for the stock to be a buy for me, this would need to be justified by the current Return on Capital being maintained for an extended period. With earnings growth being largely supported by a favorable pricing environment however, then I believe that it is more likely to be a short-term phenomenon. If the company does face a reduction in pricing power, earnings are likely to take a hit and it will be difficult to maintain the current price.

Footnotes:

1. The presented figures are derived from adjusted NOPAT, this is adjusted to convert GAAP data to economic earnings, removing one-off and non-operating items, asset write-downs etc. (amongst others). Additional adjustments are also made to Invested Capital.

2. The equation that describes this additional component of EBIT growth is shown below. This equation also works in reverse, so if ROC reduces, then negative EBIT growth can be expected.

Equation Showing Additional Component of EBIT Growth (Aswath Damadoran)

3. Adjusted FCFF is derived from the adjusted NOPAT figure.

For further details see:

Caterpillar: Beware The Dip