CAT - Caterpillar Could Fly Higher If Cyclical And Secular Tailwinds Align

2024-01-09 07:30:00 ET

Summary

- Caterpillar is the smallest holding in my dividend growth portfolio, accounting for 3.2% of the total portfolio value.

- The market is currently expecting a soft landing for Caterpillar, with analysts projecting 7% EPS growth in 2025 and 13% EPS growth in 2026.

- Caterpillar benefits from strong secular growth, including the anticipated surge in demand for commodities like copper and nickel for renewable technologies.

Introduction

When it comes to investing, it's all about the risk/reward. Hence, in this article, we'll take a closer look at a company that has become the smallest holding of my dividend growth portfolio: Caterpillar ( CAT ) .

On November 18, I wrote my most recent article on the stock, using the title " Dividend Brilliance And Economic Risks - An Important Message For Caterpillar Investors."

In this article, I will provide what I believe to be a very important update. We'll look at the current risk/reward in light of economic challenges and tailwinds and focus on the company's long-term growth potential, which supports the case that CAT shares may be up to 50% undervalued.

So, without further ado, let's dive right in!

It's All About The Risk/Reward

Believe it or not, Caterpillar is currently my smallest holding, accounting for 3.2% of my total portfolio value. This is not because I sold some (I didn't, and I cannot imagine a scenario where I will sell CAT stock) but because other investments performed better and because I added more to my other holdings.

As a matter of fact, my plan is to throw a lot of money (relatively speaking) at my entire bottom three this year.

| Bottom 3 |

| TICKER |

| SECTOR |

| WEIGHTING |

| 1 |

| ( CAT ) |

| Industrials |

| 3.2% |

| 2 |

| ( DE ) |

| Industrials |

| 3.3% |

| 3 |

| ( CP ) |

| Industrials |

| 3.8% |

With that said, before I continue, I want to start by looking at Caterpillar's valuation.

I am increasingly discussing the valuation at the start of articles, as it makes for a great basis to discuss growth potential in the remainder of the article.

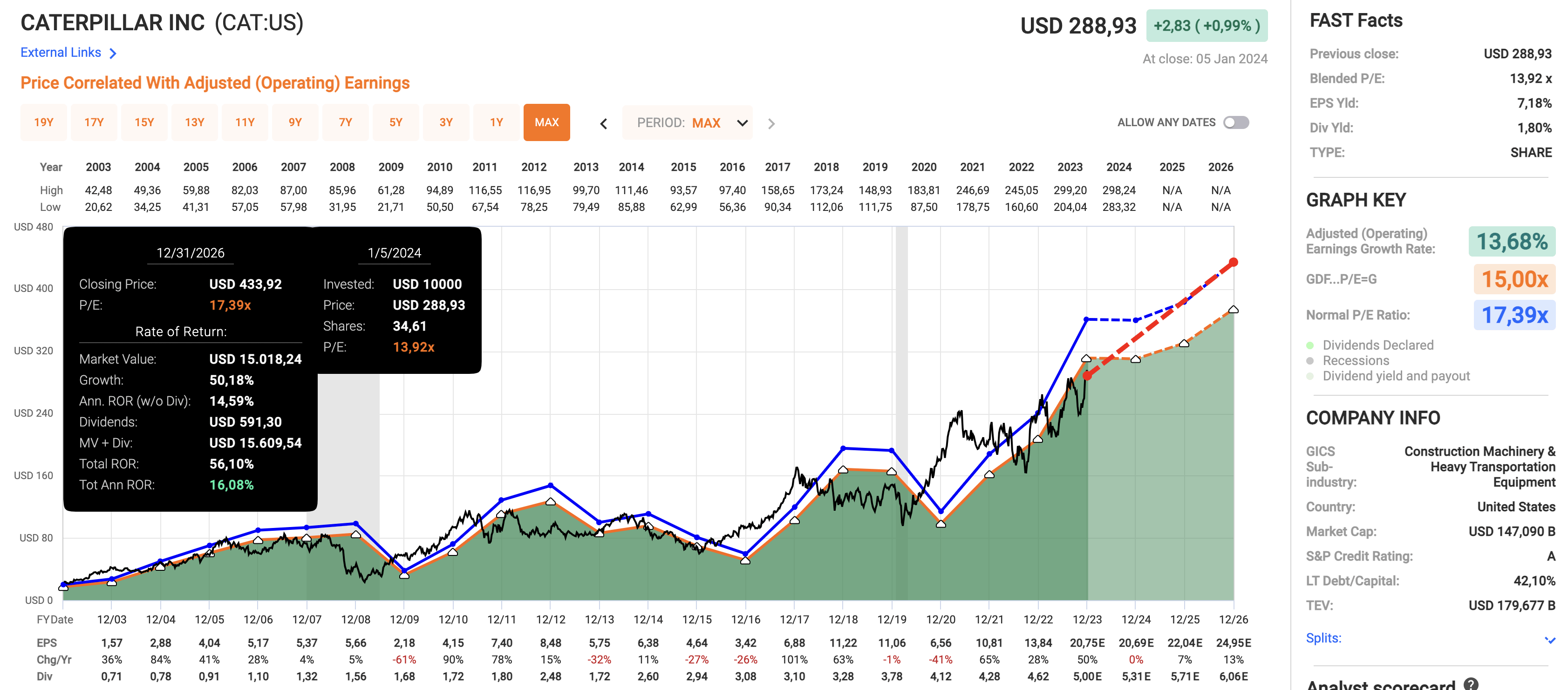

Using the data in the chart:

- We see that Caterpillar's earnings are highly cyclical, which makes sense as it sells cyclical machinery.

- However, despite prolonged contraction in economic indicators like the ISM Manufacturing Index, analysts believe that 2024 will be the worst year of the cycle with 0% EPS growth (not even contraction!).

- 2025 is expected to see 7% EPS growth, potentially followed by 13% EPS growth in 2026.

- While these expectations are subject to change, we see that the market is expecting a soft landing.

- This bodes well for its valuation. CAT shares are currently trading at a blended P/E ratio of 13.9x. This is below the long-term normalized valuation multiple of 17.4x.

- A return to a 17.4x valuation by incorporation of the expected EPS growth rates implies a fair stock price value of roughly $434, which is 50% above the current price.

{kind=link}

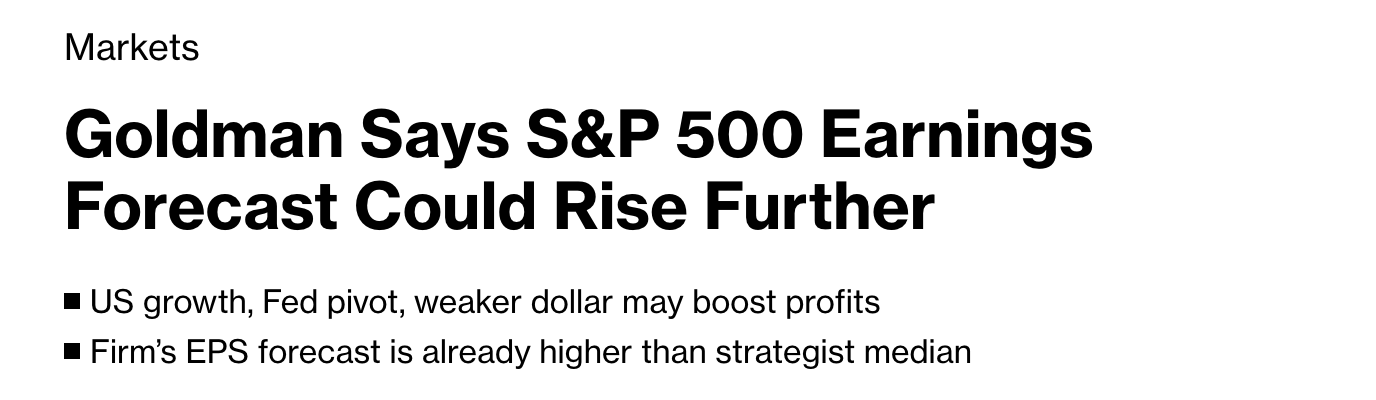

Even Goldman Sachs is now coming out, making the case that the worst is behind us.

As reported by Bloomberg, Goldman Sachs strategists anticipate that US corporate earnings in 2024 could exceed current forecasts, driven by a robust economy and declining interest rates.

According to Chief US Equity Strategist David Kostin and his team, the forecasted 5% increase in S&P 500 companies' earnings per share to $237 this year might be conservative, with potential upside from stronger economic growth, lower interest rates, and a weaker dollar.

{kind=link}

Even Yellen just made the case that the worst is behind us, although this is almost certainly politically motivated:

In recent weeks Yellen has been on something like a victory lap. In December she said economists who predicted recession were now “ eating their words ,” and she repeated her critique Friday.

“There has been a lot of pessimism about the economy that’s really proven unwarranted,” she said. “A year ago, most forecasters believe we would fall into a recession. Obviously, that hasn’t happened.”

The problem with these statements is that they are on thin ice. Very thin ice.

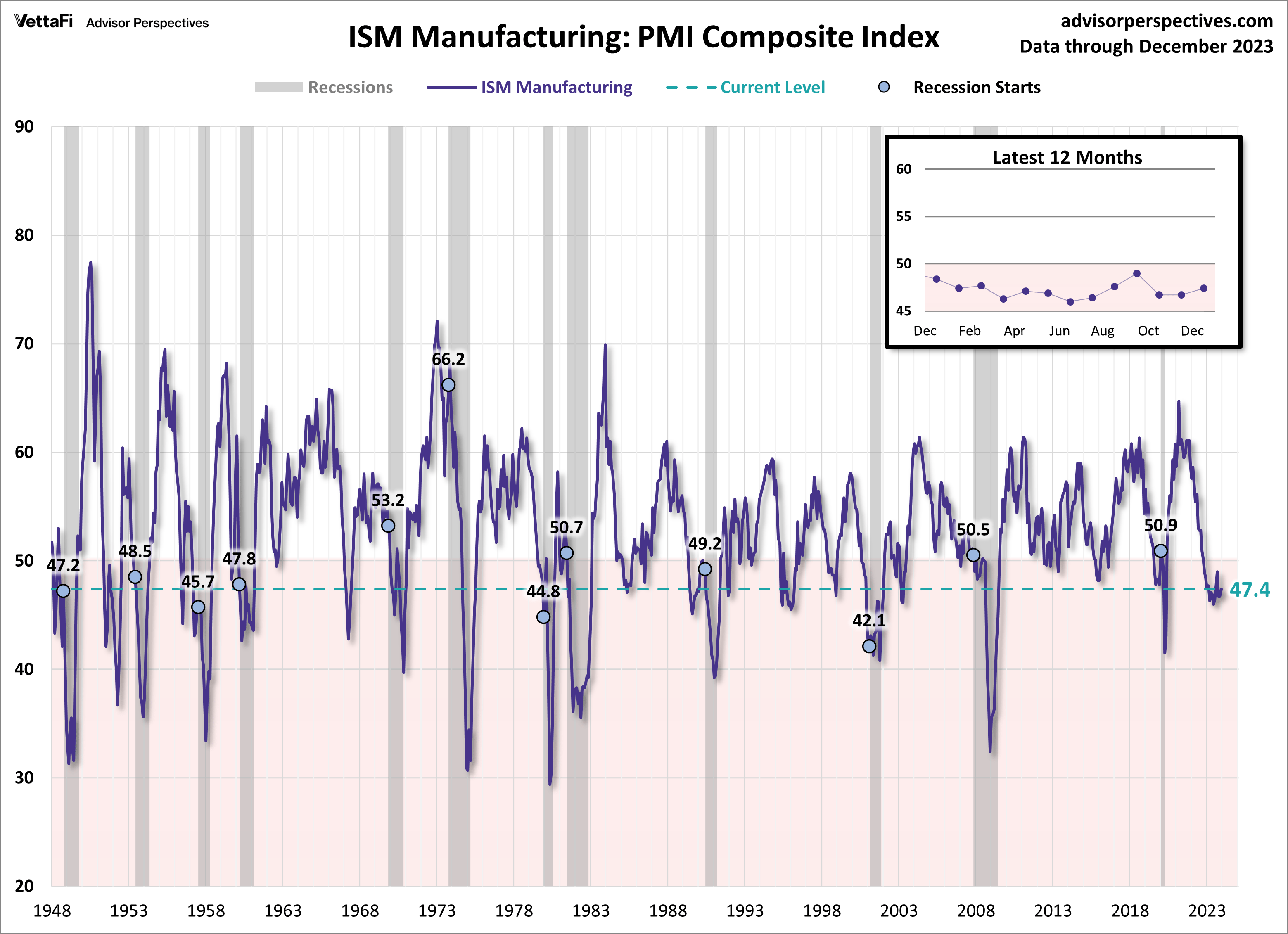

As we can see below, the aforementioned ISM Manufacturing Index seems to be bottoming. However, it's in contraction territory. It has been in contraction territory every single month in 2023.

{kind=link}

Hence, on January 3, I tweeted that this has to be the start of a turnaround or a lot of stocks will be overvalued.

With regard to Caterpillar:

- If the ISM Index is bottoming, we could see even higher growth expectations, making the risk/reward even more attractive.

- If the ISM Index is not bottoming, we could see a stock price correction.

I know that I am essentially saying that CAT may go either up or down.

However, there's more to it, as the company benefits from a lot of secular growth, which is not measured by the ISM Index.

That's why I believe I'm in a win-win situation.

If the stock rallies, I win. After all, I am long. If the stock corrects, I will be able to throw some money at a stock I believe will do very well for many years to come.

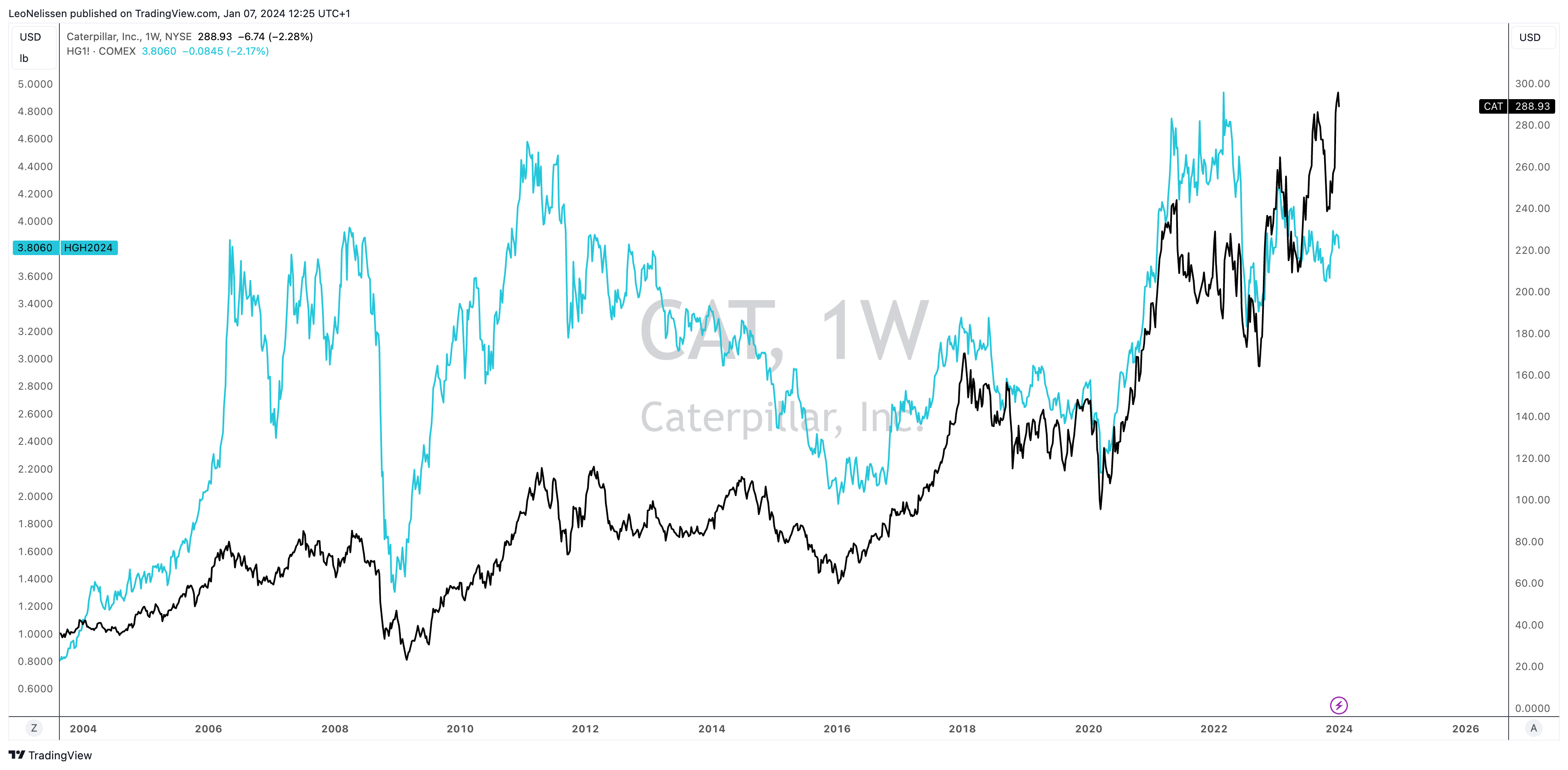

As we can see below, in the early 2000s, CAT also ignored the downtrend in the ISM Manufacturing Index. Especially after 2004, CAT more than doubled while the index declined!

{kind=link}

While the situation is different now (back then, China joined the World Trade Organization and the US dollar weakened), CAT still benefits from major tailwinds.

Caterpillar's Many Tailwinds

I am bullish on a lot of mining companies. However, I do not own most of them, as I own Caterpillar. Caterpillar allows me to use it as a proxy for mining demand.

{kind=link}

As we can see above, the CAT share price is highly correlated to the price of copper.

However, the relationship isn't perfect for one major reason:

- Caterpillar is a company that adds value by buying back stock, growing its dividend, and allowing investors to buy a part of a growing enterprise.

- Copper is just a commodity.

On top of buying back close to 20% of its shares over the past ten years, the company has hiked its dividend by 117% since 2014.

Even better, the company's dividend has been hiked for 30 consecutive years, making it a dividend aristocrat.

On top of that, it has a 25% payout ratio and a five-year dividend CAGR of 8.8%.

The only reason why its current yield is just 1.8% is its stellar stock price performance: since early 2020, CAT shares have risen 164%, excluding dividends.

It also needs to be said that the dividend isn't just protected by a low payout ratio and consistent EPS growth expectations but also a 1.7x 2024E net leverage ratio and a fantastic credit rating of A.

Going back to its ability to create value and secular growth tailwinds, in November, the company held a special call where it discussed business opportunities, headwinds, and business developments with JPMorgan ( JPM ).

One of the most important takeaways is that the mining industry outlook for the next 5 to 10 years appears promising.

The optimism is grounded in the anticipated growth driven by the global energy transition.

Rio Tinto

As the world shifts towards cleaner energy sources, there is a foreseen surge in demand for commodities like copper and nickel, essential for renewable technologies.

Despite potential challenges such as high interest rates and the time-consuming permitting process, the long-term perspective remains bullish.

With regard to elevated interest rates, the company noted that elevated rates have the potential to impact demand for loans, affecting Cat Financial's role in supporting equipment sales.

Despite this, the company highlighted its conservative management approach within Cat Financial, managing credit risks effectively. The provision for credit losses in Cat Financial is near historic lows, showing a robust risk mitigation strategy.

It also needs to be said that the machinery giant is increasingly focusing on added value.

During the call, the company acknowledged the intensifying global competition, especially outside North America, where strong price competition is observed.

The company addresses this challenge by emphasizing its competitive advantages. The focus is on adding value through technology, improving services, and strategically managing the cost structure.

{kind=link}

So far, with approximately 600 autonomous trucks globally, customers have reported up to a 30% improvement in productivity.

This reminds me of Deere & Company, which isn't competing with smaller tractor brands but building a business focused on next-gen technologies for larger farms.

In the case of CAT, features like Cat Command, which allows remote operation of machines in hazardous situations, and VisionLink, which monitors machines for cost reduction and improved safety, show its dedication to delivering value beyond cost considerations.

Furthermore, in terms of pricing strategy, the company considers various factors, including input costs and competitive situations in different markets. The historical track record indicates minimal instances of negative pricing, and Caterpillar expects pricing to cover increases in manufacturing costs.

The company is also increasingly looking to lease equipment to customers.

On a long-term basis, Caterpillar's outlook is optimistic, supported by the company's commitment to exceeding performance expectations.

Especially the emphasis on organic growth opportunities is a key aspect of Caterpillar's strategy.

The target to double service sales by 2026, coupled with investments in digital capabilities and e-commerce, positions the company to tap into untapped markets, especially among smaller customers.

Meanwhile, Caterpillar's focus on profitable growth, measured by operating profit after capital charge ("OPACC"), aligns with a broader vision of expanding its total addressable market.

Bottom Line

Caterpillar is in a very interesting spot. The stock price has completely ignored weakness in economic growth indicators for two reasons.

- The market is betting on an economic turnaround, implying that economic growth indicators will rebound.

- The company benefits from strong secular growth, business improvements, and its ability to reward investors through aggressive distributions.

As CAT is now my smallest position, it is time to buy more stock.

I am closely watching the ticker and will likely pull the trigger if I get a 10% to 15% correction opportunity, which tends to happen on a regular basis.

I believe we could get a correction opportunity, as the market may have gotten a bit ahead of itself when it comes to pricing in a stronger economy.

If I am wrong, I will watch the market go higher, holding the largest cash position since I started investing. If I'm right, I will soon get to buy my favorite stocks at better valuations.

On a longer-term basis, I believe that CAT shares have room to appreciate at least 50%, with much more upside if the ISM index gains upside momentum soon.

For further details see:

Caterpillar Could Fly Higher If Cyclical And Secular Tailwinds Align