CAT - Caterpillar Goes Boom! Now What?

2023-09-01 12:15:44 ET

Summary

- Caterpillar's stock is up 17% YTD and 75% from its 52-week low, despite weak economic growth indicators.

- The company reported a strong Q2 performance with sales and revenues increasing by 22% and operating profit up 88%.

- While Caterpillar's long-term growth prospects are promising, caution is advised due to the current valuation, but dividend investors may find the stock appealing.

Introduction

It's time to talk about one of my favorite machinery stocks. The Texas-based Caterpillar ( CAT ) company is having quite a year. The stock is up 17% year-to-date after rising 75% from its 52-week low!

My most recent article was written on May 25, titled Caterpillar's Potential Shareholder Value Is Nothing Short Of Impressive . Since then, shares are up 35%.

As much as I like these rallies, it's important to keep track of the risk/reward. After all, we might be in one of the most unusual situations in a very long time.

While economic growth indicators point at significant weakness, Caterpillar is doing just fine. The company was able to raise its guidance and benefit from secular growth related to construction, energy, and others.

Although I cannot make the case that CAT is overvalued, I'm getting cautious at these levels and preparing to buy more CAT shares the moment the market gives us an opportunity.

In this article, we'll discuss all of this and much more in light of new economic developments impacting CAT.

So, let's dive in!

Economic Growth Down, CAT Shares Up

Economic growth isn't in a good spot.

The ISM Manufacturing Index, for example, has been in contraction for nine consecutive months, putting tremendous pressure on economic growth in cyclical sectors.

Bloomberg

Not only that, but in general, we're seeing increasing weakness in key indicators.

For example, temporary work demand has rolled over last year. It's now flashing increased recession odds.

Bloomberg

Caterpillar doesn't seem to care.

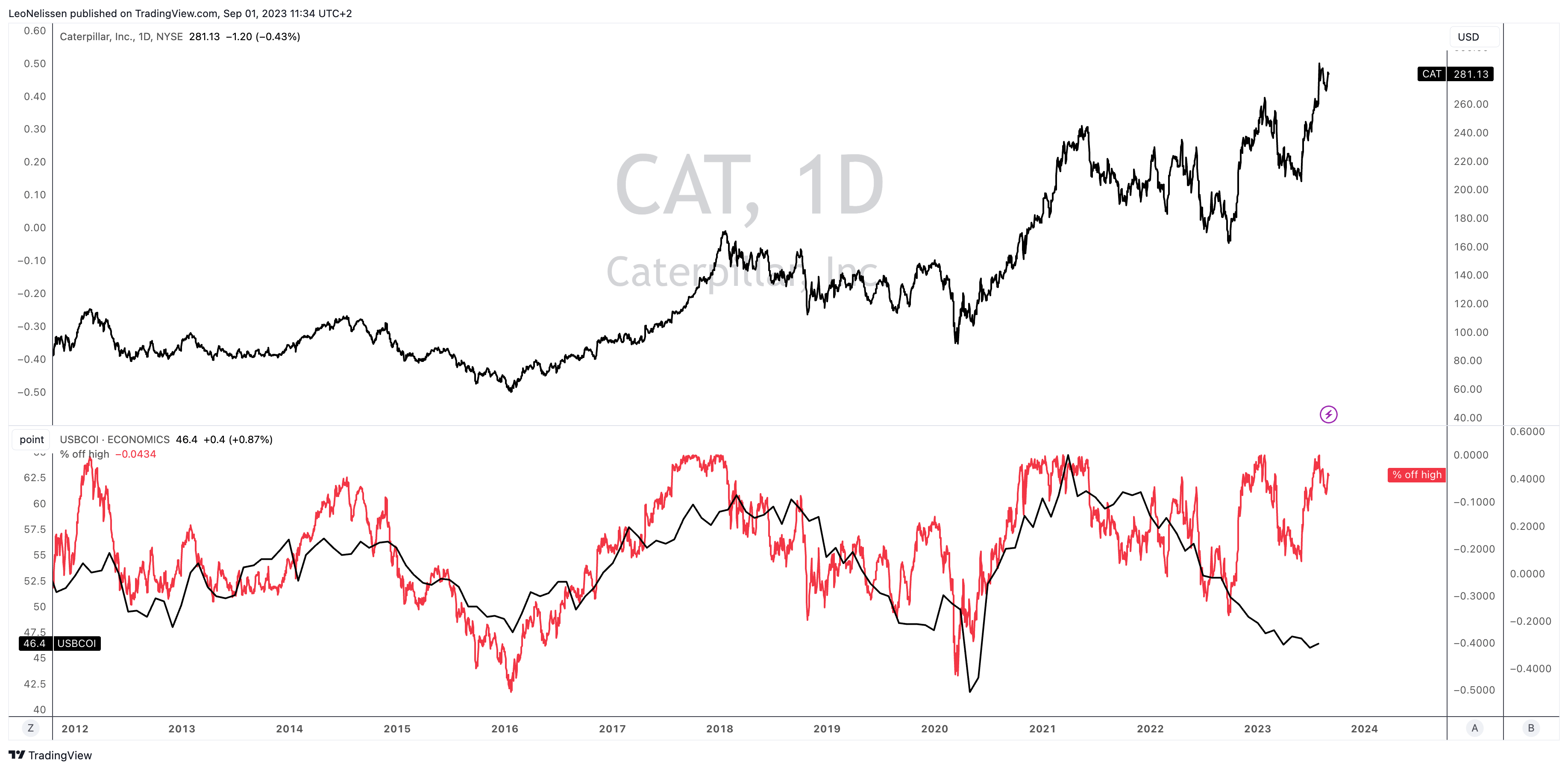

Looking at the chart below, we see the CAT stock price (upper part) and a comparison between the ISM Manufacturing Index and the total sell-off of CAT shares (percentage below their all-time high).

{kind=link}

TradingView (CAT, ISM Index)

As we can see above, CAT and the ISM index tend to move in lockstep. After all, CAT is so cyclical that lower economic expectations tend to result in lower earnings expectations as well.

Not this time.

Firing On All Cylinders

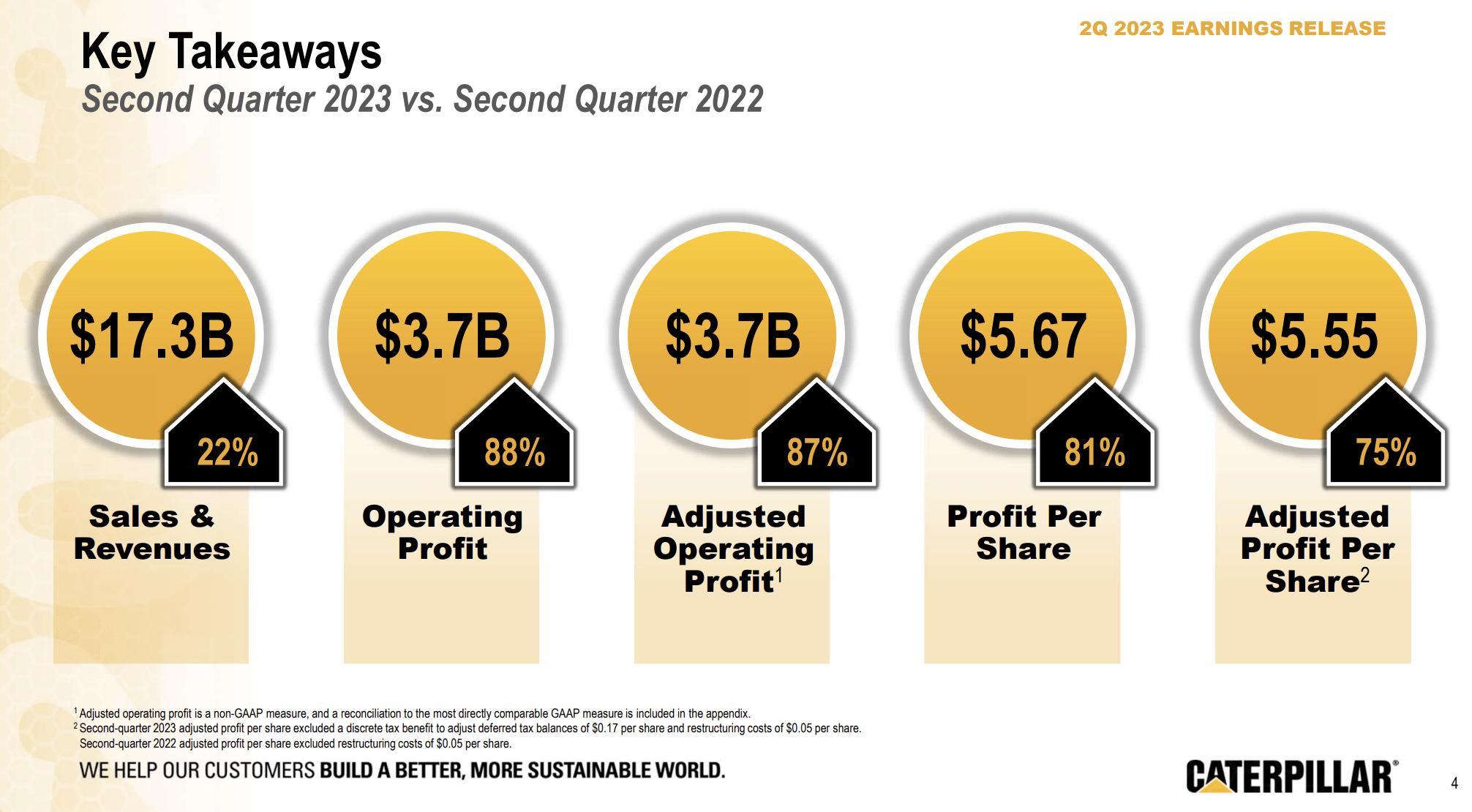

In its second quarter, the company reported a very strong performance, exceeding its own expectations.

- Sales and revenues increased by 22% to $17.3 billion, driven by higher sales volume and price realization.

- Operating profit saw an 88% increase to $3.7 billion, with an adjusted operating profit margin of 21.3%, a 750 basis point increase.

- Adjusted profit per share also increased significantly by 75% to $5.55.

{kind=link}

Caterpillar Inc.

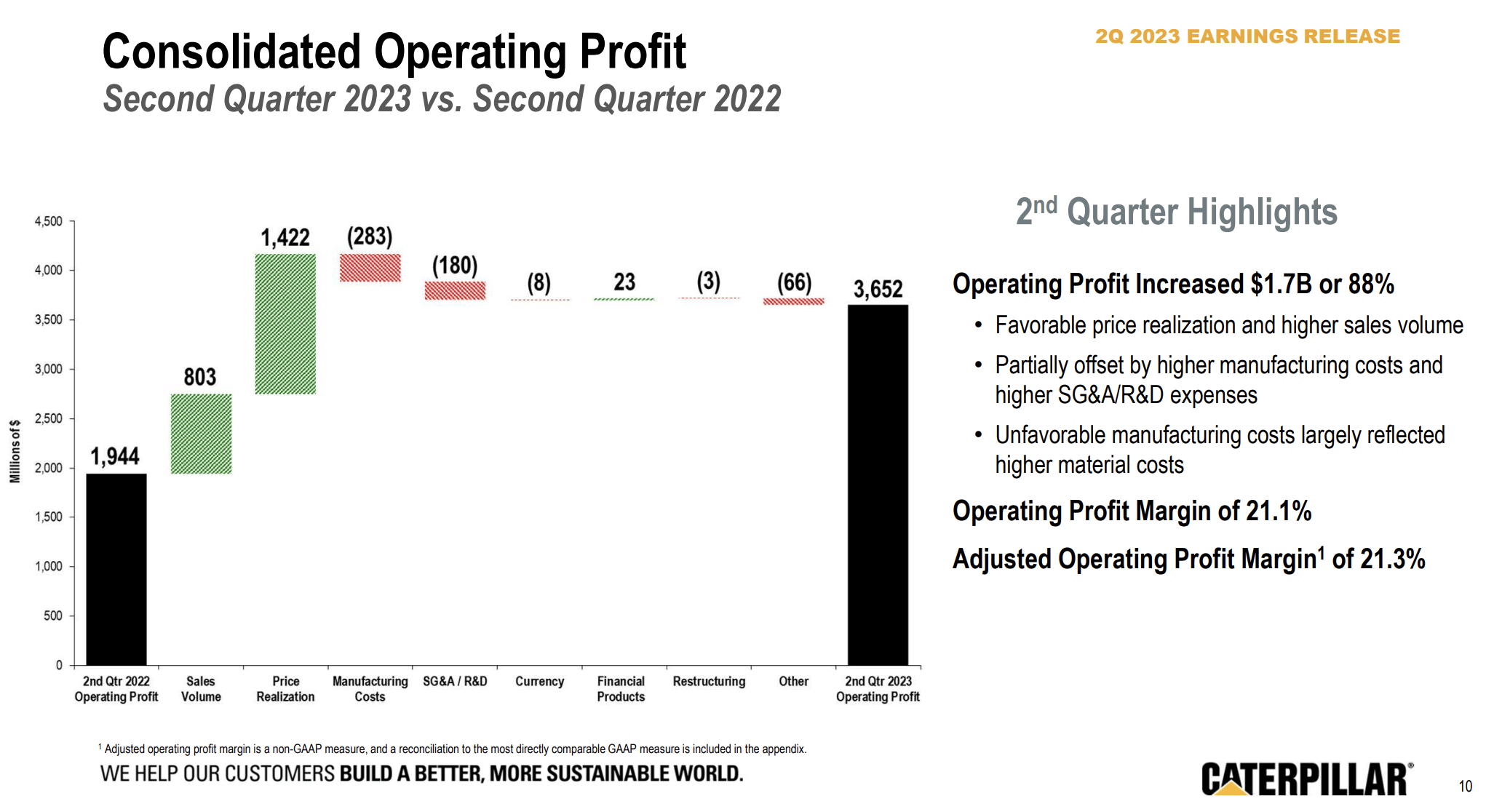

This stellar performance was attributed to both higher sales volume and price realization.

The chart below perfectly shows that CAT benefited from higher volumes and pricing power. Pricing power alone added $1.4 billion to the operating profit in the second quarter.

Meanwhile, cost headwinds declined. Manufacturing costs were a headwind of just $283 million.

{kind=link}

Caterpillar Inc.

Furthermore, sales to users grew by 16%, driven by robust demand across various end markets.

- The Construction Industries segment reported a 19% increase in sales to $7.2 billion, with strong performance in North America.

- Resource Industries saw a 20% sales growth to $3.6 billion, mainly due to price realization and higher sales volume.

- Energy & Transportation reported a 27% sales increase to $7.2 billion, with double-digit growth across all applications.

Profit margins in these segments also exceeded expectations, with Construction Industries at 25.2%, Resource Industries at 20.8%, and Energy & Transportation at 17.6%.

With regard to supply chain issues, which have been a drag on companies like CAT in the past, the company was upbeat.

During its earnings call, the company highlighted improvements in the supply chain, which allowed for increased production during the quarter. This was also visible in the operating profit bridge I just showed.

However, challenges persisted, particularly in the large engines segment, impacting Energy & Transportation and larger machines.

I expect these issues to fade completely by early 2024.

On top of sales growth in every segment, significant pricing power, and higher margins, the company is upbeat about its future.

Now What?

Not even the company's outlook was bad in this environment.

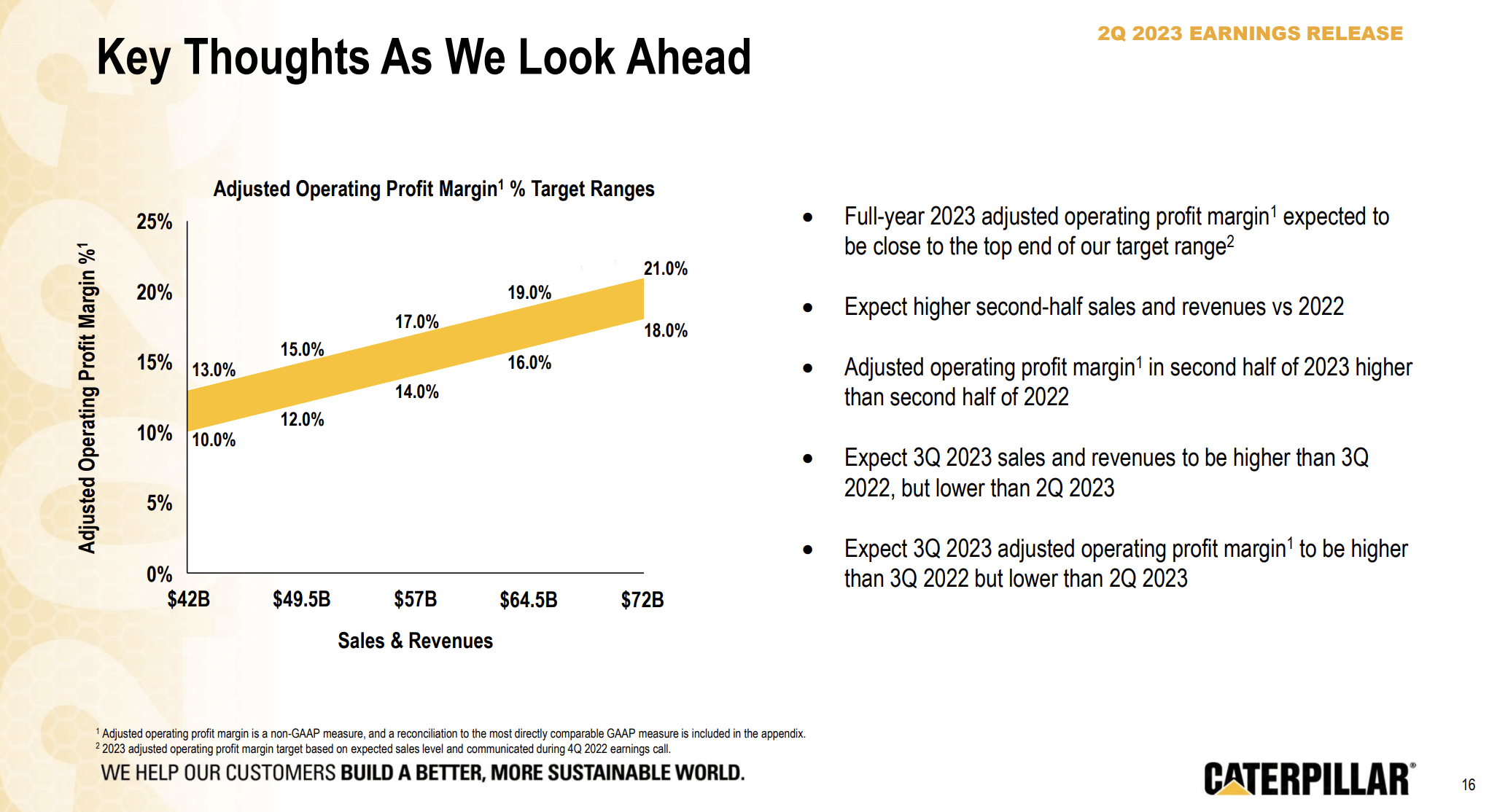

Caterpillar's second-quarter results led to a revised positive outlook for 2023.

The company anticipates higher total sales and revenues compared to the second half of the previous year, with positive sales to users and price realization.

{kind=link}

Caterpillar Inc.

Dealer inventories, which tend to be challenging to predict precisely, are expected to remain at satisfactory levels.

CAT also expects adjusted operating profit margins to be close to the top of its targeted range for the full year.

- In the third quarter, sales are expected to be higher than the same period in 2022, with typical sequential declines compared to the second quarter.

- Margins in the third quarter are expected to be impacted by lower volume and cost absorption, with increased investment in strategic initiatives across primary segments.

Going into more detail, in North America, the company foresees positive momentum driven by non-residential construction growth due to government infrastructure investments.

Looking at the chart below, we see that total construction spending in the U.S. is now close to $2 trillion, boosted by a massive surge in manufacturing construction spending, which is now close to $200 billion.

While construction-related demand is likely to slow, I expect total order levels to remain healthy for the next few quarters.

Looking on the other side of the Pacific Ocean, Asia/Pacific (excluding China) is expected to see growth in Construction Industries, while China's sales are anticipated to remain weak.

Last month, the Wall Street Journal ran an article with the headline China's Worsening Economy Is Hurting Corporate America .

{kind=link}

Wall Street Journal

According to the article:

Companies embedded in China’s ailing manufacturing, construction and export industries are reporting weaker sales . In some cases, they are warning of further trouble to come as growth grinds to a near halt and economic readings are dour .

The slowdown is registering in earnings results across a range of companies, from chemical giants DuPont and Dow to heavy-equipment suppliers such as Caterpillar. Some companies expressed disappointment with Beijing’s stimulus measures and cut their sales outlook for the country into this year.

China's largest banks are cutting interest rates as its construction market (the biggest in the world) is crumbling. For the foreseeable future, I expect China to remain a big issue for producers like Caterpillar.

We mentioned during our last earnings call that we expected sales in China to be below the typical 5% to 10% of our enterprise sales. We now expect further weakness as the 10-tons and above excavator industry has declined even more than we anticipated. - CAT 2Q23 Earnings Call

EAME markets are expected to be mixed, with strong construction demand in the Middle East but a downturn in Europe.

With regard to the ISM Manufacturing Index, this is what the HCOB Manufacturing Index in Germany looks like:

S&P Global

Other European nations aren't doing much better, which explains the company's mixed (but still upbeat) outlook.

Latin America is expected to experience a decrease in construction activity.

In Resource Industries, healthy mining demand is expected to continue, supported by elevated production levels and the transition to renewable energy.

This is a long-term secular bull case I've mentioned in almost every single article. Due to the push for renewables, we're seeing significant growth in mining demand, which requires new mines and expansions. That's very bullish for Caterpillar.

We continue to believe the energy transition will support increased commodity demand, expanding our total addressable market and providing further opportunities for profitable growth. - CAT 2Q23 Earnings Call

{kind=link}

Bloomberg

Having said all of this, I'm getting a bit more cautious.

Valuation

As much as I agree with CAT's comments that secular growth in construction and mining is likely to last, the air is getting a bit thin at current levels.

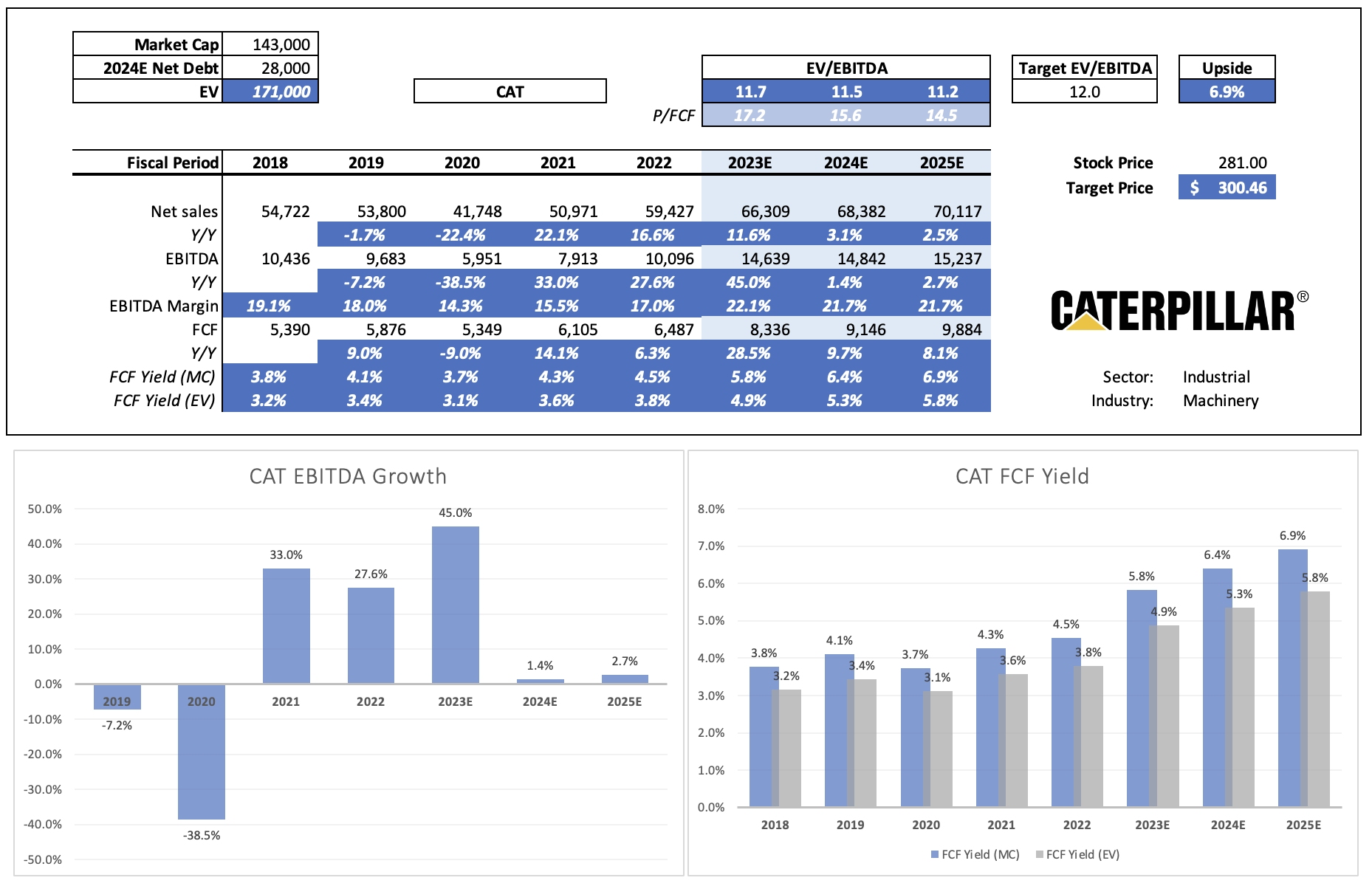

CAT is currently trading at $281, which is exactly in line with the consensus price target.

I tend to agree, as my own numbers show roughly a 7% upside using estimates that go as far as 2025. Please note that the 2024E net debt numbers in the overview below include $4 billion in pension-related liabilities.

After massive EBITDA growth in 2021 through 2023E, the company is expected to see flat-ish EBITDA growth in 2024 and 2025. Analysts are unwilling to be more bullish, which makes sense in light of ongoing economic developments.

{kind=link}

Leo Nelissen (Based on analyst estimates)

While I believe that CAT is fairly valued at 12x EBITDA, there's good news for dividend investors.

The company, which currently yields 1.8% after an 8.3% dividend hike earlier this year, is expected to grow free cash flow by high-single-digits in both 2024 and 2025.

Over the past five years, the company has hiked its dividend by 8.9% per year. It has a track record of 29 consecutive annual hikes, making it a dividend aristocrat.

Based on its current market cap, the company could end up with a 7% free cash flow yield in 2025, which is great news for its dividend, buybacks, balance sheet health, and ability to invest in its business.

The company is expected to end this year with a sub-2x net leverage ratio.

It has an A+ credit rating, one of the best credit ratings on the market, not just in machinery industries.

Having said all of this, the road ahead for dividend growth investors looks fantastic. The only issue is its valuation.

If we get a situation of further deteriorating economic growth and sticky inflation keeping the Fed from lowering rates (unless it is forced to at some point), I expect CAT shares to offer us a new buying opportunity.

As a shareholder, I'm looking to add to my position close to $220 if I get the chance.

Takeaway

While economic indicators signal concerning weaknesses, Caterpillar remains resilient, benefiting from growth in construction, energy, and other sectors.

Its second-quarter performance was stellar, with sales surging by 22%, accompanied by an 88% increase in operating profit.

However, with CAT trading at $281, in line with the consensus price target, caution is warranted.

While the company's long-term growth prospects look promising, the current valuation leaves little room for immediate upside.

For dividend investors, Caterpillar's commitment to growing free cash flow, a strong balance sheet, and an A+ credit rating offer a promising proposition.

As a shareholder, I'm keeping a watchful eye, anticipating a potential buying opportunity of around $220 if economic headwinds create a more favorable entry point.

For further details see:

Caterpillar Goes Boom! Now What?