DE - Caterpillar Has A Hidden Gold Mine (And Recently Taught Me An Investing Lesson)

2023-03-09 06:14:06 ET

Summary

- Caterpillar's recent FY 2022 results saw high top line growth with margins below targets set at Investor Day.

- Profitability is clawing its way up from the impact of inflationary pressures on manufacturing costs.

- Services revenues are growing impressively, making Caterpillar's products a network of connected assets that are expected to grow services and spare parts sales.

- Caterpillar's stock price surge saw me unable to take a position, teaching me a lesson on how I will manage my portfolio from now on.

Introduction: the lesson I learned with Caterpillar

Caterpillar ( CAT ) is rewarding its shareholders beyond what many expected. To be honest, I have been unable to be part of the recent run. In fact, I suggested back in August that the stock would be a good buy in the range between $170 and $180. The stock actually traded in that range and even below for the whole month of September and the beginning of October and I should have bought it. However, during that time I had no available cash and I had no position to sell out of to raise the cash I needed. So I just sat there kicking myself for not being ready. I then also had to be careful about FOMO. In any case, since this episode I have given myself a new rule: I always want to have a little cash available for any need. I then found out that Warren Buffett has repeatedly said that Berkshire will always have a "boatload" of cash.

While this may be viewed by some as poor capital allocation, I have come to understand that available cash means freedom to operate at one's own time. Therefore, I have made it part of my portfolio strategy to increase my cash position. To do this I am taking two actions: reduction of personal debt and decision to always have some available cash for my portfolio.

Since September 2022 I have worked on my portfolio and my household balance sheet in two ways. I don't want to be levered, that is I want to have enough liquid assets to match my current debt, which actually consists of my home mortgage (no way I am going to raise debt to pay a car!). Currently, my liquid assets/mortgage ratio is 0.76 and it has improved from the 0.67 I had in September. By paying down debt and slightly increasing my savings I should be around a 1 in a year. In addition, I am monitoring my earning power, that is how well I cover my interest expenses on my mortgage through what I consider my household monthly NOPAT. Currently I am at a 4.2 and I am targeting at least a 5 by the end of the year.

While some may think I am too conservative and too worried about debt, I am learning that a conservative balance sheet means freedom to operate, whose value can't be accounted for but it is, to me, greater than any other possible gains.

I am taking these actions in order to free more cash a quickly as possible.

The second choice I made is to have around a cash position between 5-10% of my current portfolio value. Unless I see a really urgent purchase, I wait to increase or initiate a position until, at the end of the month, I fund my portfolio with a set amount. In this way I have made myself sure I will be able in any given day of the year to have the chance to take advantage of compelling opportunities, such as the one I missed on Caterpillar. Now, I am not saying Caterpillar was a once-in-a-decade opportunity, although it was becoming attractive. Nor do I want to say the it needs to be a must for my portfolio, even though it is ranked high in my watchlist. I just wanted to share how this situation had made me improve on some aspects of my portfolio management.

Now, let's get to Caterpillar.

Summary of previous coverage

So far, I shared two article on the company. In the first one, written in May, I highlighted how the company, alongside its peer Deere ( DE ) seemed to have underestimated the impact of inflationary pressure on its margins, unlike other companies that were more able to foresee and take in advance the necessary actions to defend their profitability. After a few months, I outlined how the company was getting close to a very interesting valuation , although it still had to work on restoring its well-known profitability and its strong free cash flow generation.

Caterpillar today

Favorable macro-trends

Before we crunch some numbers and make some considerations about them, it is important to recall three macro-trends that are true tailwinds for a company such as Caterpillar.

- The Infrastructure Investment and Jobs Act passed in late 2021 is going to boost construction equipment use and demand.

- Revitalization of American Manufacturing has become a political priority for the U.S.

- The role of critical minerals in clean energy transition will lead to increasing mining activity, boosting the need for highly-technological and competitive equipment.

FY 2022 results

Needless to say, Caterpillar's top line was stellar, with FY2022 sales reaching $59.4 billion, up 17% compared with $51.0 billion in 2021. Let's consider that currency had a negative impact of $1.5 billion, without which Caterpillar would have broken the $60 billion barrier.

Q4 was even above this number, as sales increased by 20% YoY to $16.6 billion.

However, the operating profit as a percentage of sales was 13.3% vs. 13.5% in 2021. On the other hand, if adjusted we see an operating profit at 15.4% of sales, compared to 13.7% of 2021. The same thing is seen in the quarterly result: operating profit margin of 10.1% that becomes 17% if adjusted.

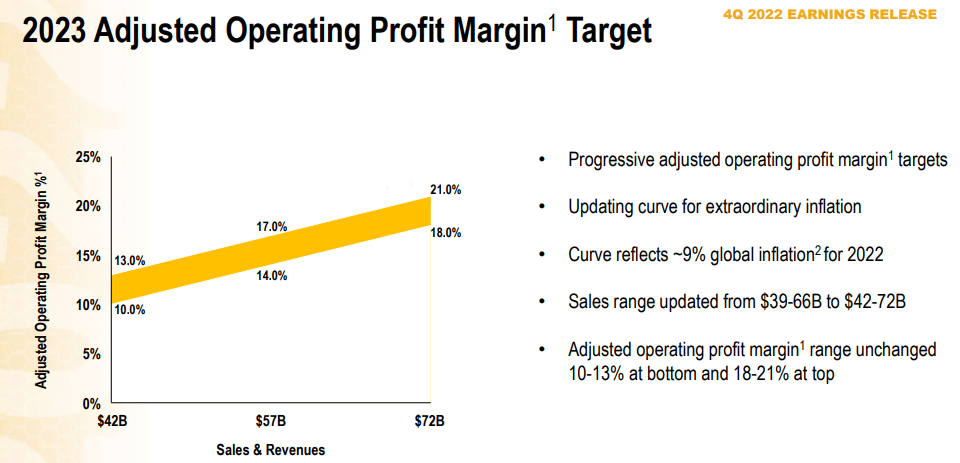

In any case, the trend is clear: quarter after quarter Caterpillar is clawing its way back to higher profitability. This has made the company update its profit margin target for 2023 based on sales.

{kind=link}

It is quite understandable how operating margin go up as sales increase. It then becomes important for investors to have some visibility on the possible revenue the company will achieve this year.

In its Annual report, Caterpillar reported the following order backlog:

The dollar amount of backlog believed to be firm was approximately $30.4 billion at December 31, 2022 and $23.1 billion at December 31, 2021. Compared with year-end 2021, the order backlog increased for both the Energy & Transportation and Construction Industries segments, with the largest increase in Energy & Transportation. Of the total backlog at December 31, 2022, approximately $5.5 billion was not expected to be filled in 2023.

If we do some math, we have $30.4 billion less $5.5 which won't be filled in 2023. This gives us $24.9 billion.

Let's see what happened in the previous years. At the end of 2021, the company had a backlog of $23.1 billion. Caterpillar ended up with $51 billion. In 2020, Caterpillar finished the year with a backlog of $14.2 billion and it ended up with $42 billion. Since I think we are still in the same manufacturing cycle that started after the pandemic, with a lot of pent-up demand still to be fulfilled, I think it is reasonable to expect that, according to the trend seen in the past, Caterpillar will reach a revenue 2.25x its order backlog. So we should see the company in between $56 and $68.4 billion, without counting the effect of price increases. A more bullish view may see Caterpillar at or above $70 billion for this year, which would be a staggering result. In any case, I think it is correct to place Caterpillar's expected profit margin for this year in the upper range of the graph shown above.

To paint a more accurate picture on Caterpillar's future results, let's take a look at the revenues breakdown by segment Caterpillar shared in its annual report.

{kind=link}

Construction and E&T (Energy and Transportation) are more or less equivalent with $25.3 and $23.8 billion in sales. Resource Industries is about half the size of the other two with $12.3 billion. However, the outlook for these three is quite different.

According to Caterpillar's annual report, the Construction Industries segment will see positive momentum only in North America limited to non-residential construction (we have already seen the favorable macro-trends) while residential construction is moderating. In other areas of the world, we have a mixed picture with Asia growing apart from China (not a minor detail), Europe and Latin America flat, while in the Middle East demand should be strong. Therefore I don't expect this segment to increase dramatically. Let's say that between price and volume mix, it could increase 10% (price hike of 6.%) . This would be a revenue of $27.8 billion.

Energy & Transportation is the segment for the oil and gas industry and for marine, rail and industrial applications. The product portfolio include, as the company explains in its annual report:

reciprocating engines, generator sets, integrated systems and solutions, turbines and turbine-related services, electrified powertrain and zero-emission power sources and service solutions development, the remanufacturing of Caterpillar engines and components and remanufacturing services for other companies, diesel-electric locomotives and other rail-related products and services and product support of on-highway vocational trucks

Now, this segment is expected to grow sales due to strong order rates in most applications. For example, new equipment orders for solar turbines seems quite strong. Therefore we can expect this segment to grow not only due to price hikes but also due to strong demand. This could make the segment grow by 16% to $27.5 billion.

But what I am actually inclined to think will grow the most is the "underdog": Resource Industries, which offers heavy construction and surface and underground mining machinery. Caterpillar's equipment is used to extract and haul copper, sands, coal, aggregates and various minerals and ores. Now, as we have seen above, this segment is really going to explode in the future. Caterpillar is well aware of this trend and does indeed expect strong mining demand, also thanks to the autonomous solutions it has developed. As the company writes: "the energy transition is expected to support increased commodity demand, expanding our total addressable market and providing opportunities for profitable growth".

What does this mean? The segment will grow more than the other two and, in my view, this is something we will see not only in 2023 but for some years. So, let's use the assumption the segment will grow by another 20% this year. We are at $14.8 billion.

If we sum up the three we are around $70 billion, in the high range of the graph shown above. Still, though we fall within the guidance Caterpillar released, we are before huge numbers. Now, hidden within this number there is a golden nugget: services

Services

Caterpillar is pouring a lot of effort in converting its equipment sales into a source or recurring revenue. So far, Caterpillar doesn't break down its service business in its report, however, just look at the numbers below to see how impacting this business is on the overall results: in 2022 the company achieved $22 billion in revenue, more than 30% of the total result.

{kind=link}

During the earnings call , James Umpleby, Caterpillar's CEO, rightly highlighted the steps the company is undertaking to generate more and more services revenues:

we generated $22 billion of services revenues in 2022, a 17% increase over 2021. Services growth in 2022 benefited from our ongoing initiatives and investments as well as price realization. We now have over 1.4 million connected assets, up from 1.2 million in 2021. We delivered over 60% of our new equipment with a customer value agreement and the launch of our new app called Cat Central to help drive growth in ecommerce sales to users. We also had the highest level of parts availability in our history. Overall, our confidence continues to increase that we'll achieve our $28 billion services target in 2026.

Delivering 60% of new equipment with such an agreement is truly the foundation of very solid future results, whose margins are bound to be high.

It is a pity Caterpillar doesn't disclose more about this business, as it has a considerable size and a huge impact on margins. However, if I look at Paccar ( PCAR ), whose spare parts and services is very high-quality , margins for this business can top 30%.

Takeaway

Even with the recent price surge, Caterpillar is not trading at an unreasonable valuation thanks to the strong results the company reported. In fact, with a current fwd EV/EBITDA of 13.5 we are right at the middle of the range Caterpillar has traded at in the past decade.

It is not cheap, but it is not even that expensive. If we factor in that, as we move forward, Caterpillar's revenues will become more valuable thanks to the growing services business, Caterpillar can still be seen as a buy.

Therefore, here is what I am doing. I will initiate a small position in the next few days because I have come to realize the company is more valuable than I initially thought it was. In addition, as I have explained earlier, I will always have some cash aside to dollar cost average if the opportunity comes, especially if interest rates keep on being hiked more than expected and create some market turmoil.

For further details see:

Caterpillar Has A Hidden Gold Mine (And Recently Taught Me An Investing Lesson)