CAT - Caterpillar: Highly Cyclical Business But Can Likely Keep Hiking Dividends For Years To Come

2023-06-27 07:16:43 ET

Summary

- Caterpillar has a strong dividend growth history and can continue raising dividends in the foreseeable future despite its cyclical business nature.

- The company has a healthy payout ratio and has been repurchasing shares, which allows for more earnings per share and room for dividend growth.

- The dividend yield is below its historical average for CAT despite recent hikes.

- I am also offering a way to "create your own dividend" without giving up much upside using an options strategy.

Caterpillar ( CAT ) is one of the largest machinery producers in the world and its products are involved in many different industries such as construction, infrastructure, energy and mining. While the stock currently yields only about 2%, it has an impressive dividend growth history spanning 29 years which puts the company into S&P 500 Dividend Aristocrats Index ( NOBL ). In this article we will look at the company's dividend and show that it can support raising dividends for the foreseeable future even though its business is highly cyclical in nature.

Caterpillar's dividend history shows consistently rising dividends year after year since the 90s but we can also see that it used to support much higher yields in the past as the stock's dividend yield ranged from 1% to 6% during this time with the average yield being 3%. Historically speaking, the current yield seems low but investors can expect to receive more hikes in the future if they are patient enough to hold this stock for the long term.

The stock's current payout ratio is in mid 30s which means for every $100 Caterpillar generates in net profits, it pays about $35 to investors in dividends. This is a healthy number and indicates that there is plenty of room to grow if the company chose to pay more dividends even without increasing its net income. This also provides a cushion for the company since its business is highly dependent on commodity prices and highly cyclical because it won't have to cut dividends if its profits fall slightly due to outside factors.

Dividends aren't the only way the company returns cash to shareholders either. In the last decade we've seen Caterpillar repurchase 21% of its existing shares and reduce its share count by that much. This serves two purposes for investors. First, there is more earnings to go per each existing share and second, the company can now keep raising its dividend payments without actually paying more out of its pockets because there are fewer shares to pay dividends on. If a company has 100 shares and pays $1 per share in dividends, it pays $100 in total. If the same company has 80 shares, it can now afford to pay $1.25 per share while spending the same amount.

The company's margins have been relatively stable and predictable over the years. This is especially true for its gross margins that typically ranged between 28% and 32% with very little variation. The company's operating margins varied a bit more compared to its gross margins but this is partially due to the volatile commodity market conditions we saw between 2020 and 2022 when commodity prices first crashed as a reaction of COVID lockdowns, then rallied due to inflation and then stabilized again after tightening actions from central banks around the world. The company found itself adjusting its spending to commodity prices but things seem to have stabilized for now. Moving forward we can expect it to have 30-32% in gross margins and 14-16% in operating margins barring a severe recession.

These margins also translated into good returns for the company. We are currently seeing 43% in Return on Equity, 13% in Return on Invested Capital and close to 9% in Return to Assets. The first metric could be simply a function of Caterpillar's stock being cheap more than its profitability. The second and third metrics might look unimpressive to you if you are used to looking at mostly tech companies but those figures are pretty strong for an industrial company that has to invest into factories, infrastructure and supply chains. Also notice that these metrics have been improving for the last 2-3 years after bottoming in 2021.

When it comes to dividends, cash flow is a company's bread and butter. No company can consistently keep paying (or hiking) dividends without a healthy cash flow. Currently Caterpillar generates about $7.8 billion of cash flow from its operations and $6.36 billion in free cash flow. Since the company's total market cap is $120 billion, we are looking at operating cash flow yield of 6.5% and free cash flow yield of 5.3% which tells me that it can afford to keep hiking dividends even without increasing its cash flow by much. To be honest I expect Caterpillar to spend more on buybacks than dividends in the near future because this can benefit the company more in the long run if it can reduce its share count for the reasons I mentioned above. I could see the company hiking dividends at a minimal rate around 3-5% for a few years and putting more money at work to reduce its share count so that it creates more room to hike dividends more aggressively in the future when it has fewer outstanding shares to worry about.

Moving forward, analysts expect the company to keep growing its earnings at a healthy rate. They are expecting the company to earn $17.92 this year, $18.27 next year and $19.80 in 2025. This would give it a forward P/E of 13 for this year and 12 for next year, which translates into earnings yield of 7.6% for this year and 8.3% for the next year. This makes the current yield of 2% more than safe and future dividend hikes easily achievable. There is also the risk that the global economy might enter a recession, causing commodity prices to crash and this would hurt Caterpillar's profitability at least in the short term. Luckily the company has about $7.5 billion in cash which it can use as a cushion while waiting for the economy to improve if that were to happen.

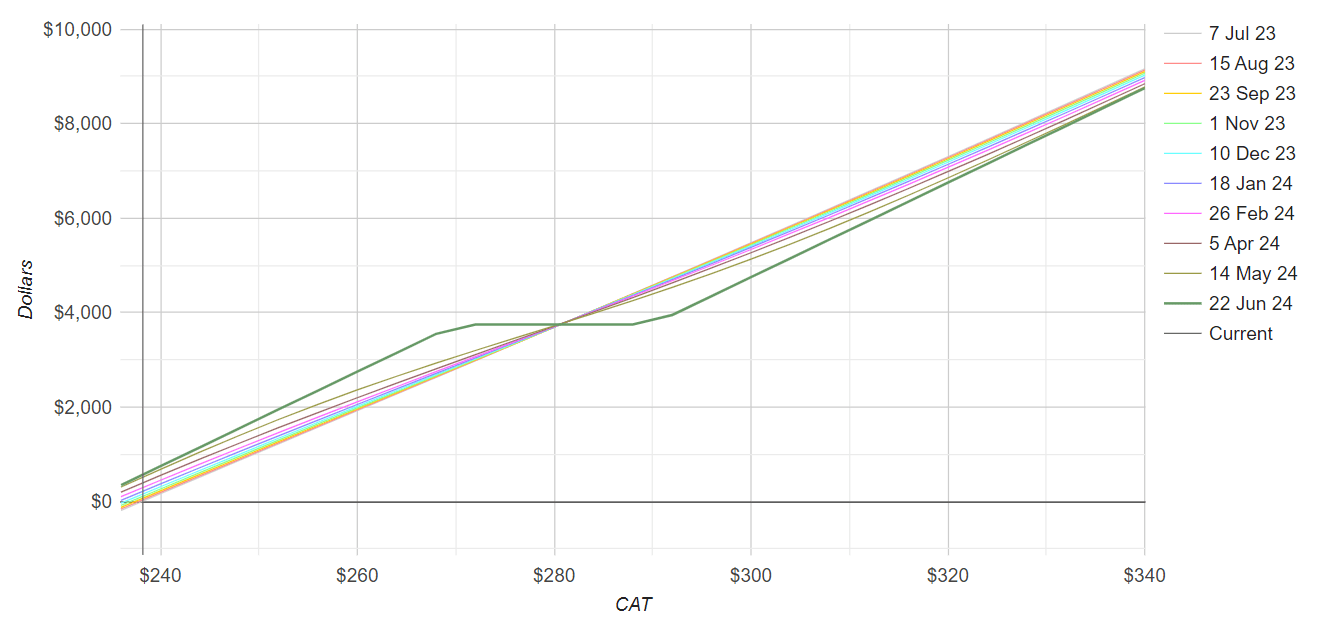

Some investors might like the company but not its low yield so they might want to boost this dividend yield by selling covered calls. Since the company's current valuation is very low, I don't recommend selling covered calls flat out but you can sell call spreads against your shares instead. This way you still get to collect a premium (although smaller) but participate in any outsized upside as well.

How does it work? In traditional covered call strategy you own 100 shares of a stock and sell 1 covered call position against that share at a strike price at or above the current price. In this strategy you still do that but also buy a call option at a higher price. This way if the stock suddenly climbs significantly higher, you take advantage of that too.

In this example, we are selling a Jun 2024 $270 Call option which is about 14% above the current price. Then we are buying a Jun 2024 $290 Call option. This transaction gives us an additional yield of 2.4%. If the stock stays flat or drops, we keep this 2.4% on top of the 2% dividend the company was already paying so we effectively more than doubled our yield. If the stock rises, we will benefit from any rise up to $270 and then any rise above $290.

{kind=link}

This is a good way to add more yield to a stock without giving up too much upside. If you were sell covered calls instead, you would have collected a bit more on premiums but given up practically most if not all of the upside if the stock were to rise significantly.

I expect Caterpillar to keep hiking dividends and repurchase its shares at an accelerated rate in the future. The company's current earnings and future prospects mostly support that barring a severe recession or a crash in commodity prices. While possible, I find those scenarios unlikely at the moment.

For further details see:

Caterpillar: Highly Cyclical Business But Can Likely Keep Hiking Dividends For Years To Come