CAT - Caterpillar: Long-Term Growth Appears Inevitable

2023-04-23 13:41:51 ET

Summary

- Caterpillar's shares are down by 7.07% YTD while the S&P 500 is up by 7.54%.

- Cut in interest rates by the Fed should depreciate the U.S. dollar to make domestic products more attractive.

- Increased demand for commodities would make companies want to spend more on new machinery & equipment.

- My valuation analysis via two different frameworks point to a significant upside potential. I therefore assign a Buy on CAT.

Editor's note: Seeking Alpha is proud to welcome IM Investing as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Thesis

Caterpillar (CAT) is a company that manufactures high-quality products and, in my view, is well-positioned to capitalize on future industry growth. I believe that as the Fed starts to cut rates, The Infrastructure and Jobs Act comes into effect, and the U.S. dollar starts to depreciate again, then Caterpillar would start to see even more growth. What intrigues me about the company is that even with the rate hikes, appreciating U.S. dollar, and recession talks, it still managed to grow by 17% in 2022 . My view on CAT stock is that it has a lot of potential but for the long term. Even thought the shares are down significantly YTD, I still believe they have more room to fall in the coming days or weeks as this market rally slowly dies. My entry price target is $205-$210.

Business Model

{kind=link}

Business segments

Construction ( 39% of Revenue and ~19% EBITDA Margin): This segment is primarily responsible for manufacturing high-quality machinery to support customers in infrastructure, forestry, and building construction.

Resource (19% of Revenue, ~15% EBITDA Margin): This segment is responsible for developing and manufacturing high-productivity equipment for both surface and underground mining operations around the world.

Energy & Transportation (36% of Revenue, ~14% EBITDA Margin): The company's Energy & Transportation segment supports customers in oil & gas, power generation, marine, rail, and industrial applications, including Caterpillar machines.

Financial Products (5% of Revenue, ~27% EBITDA Margin): This segment is primarily operated by Cat Financial and Insurance Services. Cat Financial provides retail and wholesale financing to customers and dealers around the world for Caterpillar products and services.

Future Industry Growth

The construction industry grew to a spending value of close to $12 trillion and is expected to grow by 3% percent per annum until 2030. I believe that as the industry grows, Caterpillar will have a good share of that growth because it is the market leader when it comes to construction equipment manufacturing. Growth in this industry is crucial for the company because construction makes up 39% of its revenue.

Source: Statista

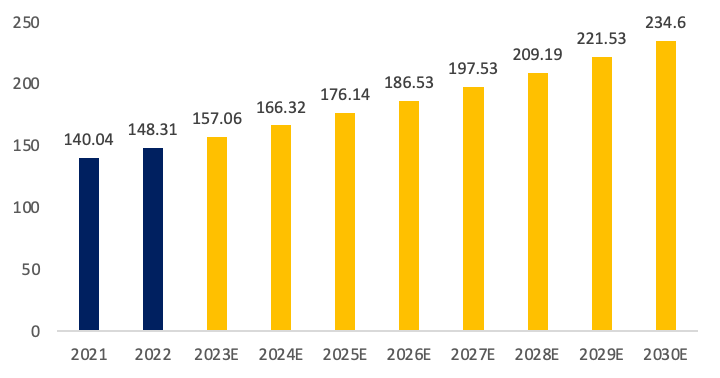

The global construction equipment market was estimated at $148.3 billion in 2022. This market is expected to increase to around $234.6 billion by 2030 at an average rate of 6%. Given that Caterpillar is the world's biggest construction equipment manufacturer, they stand to benefit from the industry's future growth.

{kind=link}

My view on future industry growth is that as the demand increases, so will the demand for construction & mining equipment. Caterpillar is well positioned to take advantage of the growth since they do spend heavily on R&D to make sure they can provide their costumers with the best products in the market. Caterpillar is also the leading provider of both mining & construction equipment globally.

Fed rate cuts

Demand tends to slow when interest rates are high. The Fed's funds rate is likely to reach 4-75%-5.00% by 2023. The Federal Reserve is planning to start cutting rates by the end of 2023. Rates are forecast to be at 3% by 2025. Historically low interest rates made construction projects attractive, including the construction of new homes and projects to alter pre-existing homes.

Source: Statista

My view on the interest rate cuts is that high interest rates have caused the U.S. dollar to appreciate against its counterparts. I believe that as the Fed cuts interest rates, the U.S. dollar will weaken making domestic products more attractive overseas, considering that more than 55% of Caterpillar's revenue is from outside the United States. The company depends a lot on abroad customers so the more the U.S. dollar appreciates, the less customers abroad are willing to spend.

The Infrastructure and Jobs Act

The Act will be executed over the 10 years to 2031, supporting manufacturers that produce graders and mixers. The act is a $1 trillion package that intends to invest in roads, ports, bridges, and the power grid. Caterpillar stands to benefit the most from this act because they are the biggest manufacturer of heavy equipment in the United States.

Source: IBISWORLD

It might take time for the act to fully come into affect because it will run for 10 long years but, as I said before, for me, Caterpillar is a long-term play. Given that the company dominates the U.S. market for Construction Equipment Manufacturing, they stand to benefit the most from the $1 trillion package.

Valuation

Caterpillar's stock has cooled off since hitting all-time highs on January 31, 2023. Historically the stock has traded at an average P/E ratio of 17.4x for 20 years. It currently trades at a P/E ratio of 17.4x. To evaluate the company, I examined the trading multiples of five similar companies (Deere & Company (DE), Komatsu (KMTUY), XCMG Construction Machinery, Sany Heavy Equipment International Holdings (SNYYF), and PACCR), ranging from P/E of 10.3x to 33.7x and EV/EBITDA multiple of 7.0x to 22.1x.

Multiples Valuation

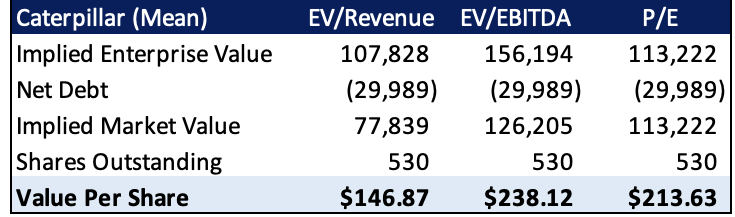

I evaluated the company by averaging out the multiples of the 5 competitors and, based on my calculations, Caterpillar's worth is estimated to be between $113 billion and $126 billion. I multiplied Caterpillar's 2022 Net income ($6,703 million) by the mean P/E ratio of the 5 competitors (16.9x), which gave me an implied market value of $113 billion; dividing this by the Shares Outstanding (530 million) led me to a stock price of $213 . I then evaluated the company using the average (mean) EV/EBITDA of the 5 competitors (13.1x) and got an estimated market value of $126 billion. I multiplied 13.1x by Caterpillar's 2022 EBITDA of ($11,895 million), which gave me an EV value of $156 billion. I then added the net debt (-$29,989 million) and got an implied market value of $126 billion; and by dividing this figure by the Shares Outstanding (530 million), I got a stock price of $238 .

Created by the Author using 10-K & Capital IQ Created by the Author using 10-K

{kind=link}

{kind=link}

DCF

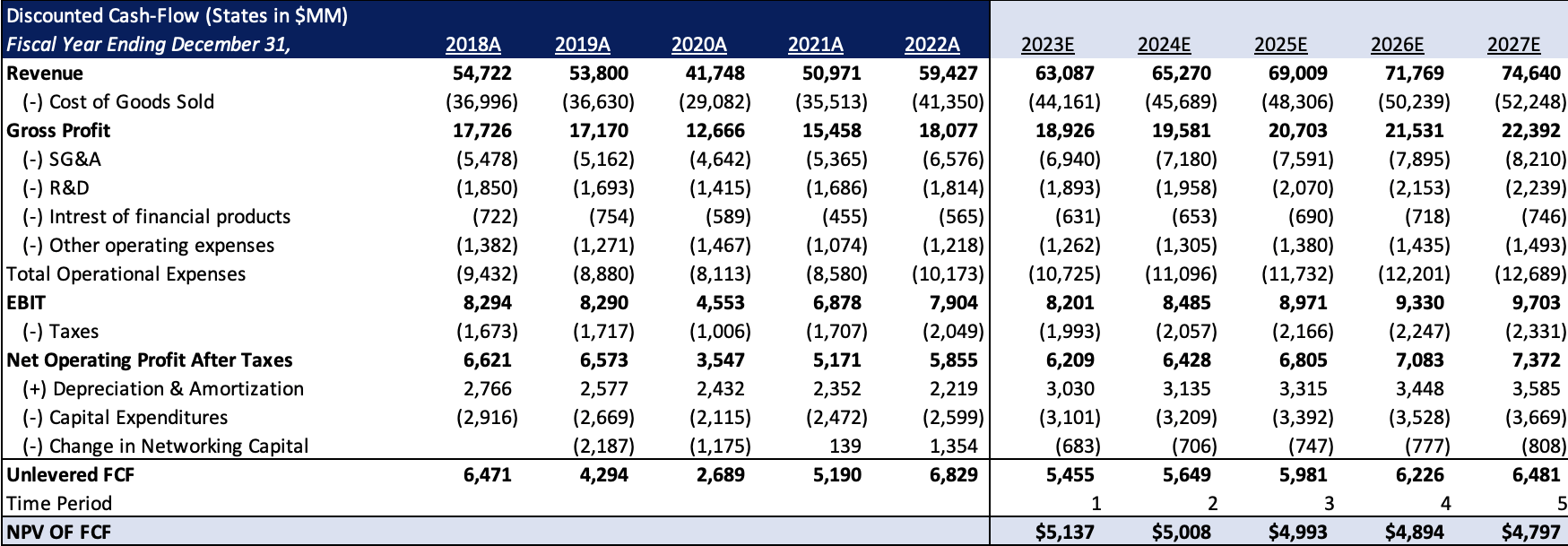

I also evaluated Caterpillar using the DCF method. The assumptions I used were that the company will grow at a 5% CAGR for the next 5 years. I then calculated the Unlevered FCF of the forecast years (calculations are below). I then discounted free cash flows back to the present using a discount rate of 6.20%. I multiplied the Unlevered FCF of the last year ($6,481 million) by (1 + Growth rate / WACC - Growth rate), which gave me a terminal value of $208 billion. I then had to calculate the PV of the terminal value by using the following calculation: ($208 billion / (1 + WACC)^5. I then arrived at an EV of $179 billion (PV terminal Value + Sum of PV FCF) and the equity value of $149 billion (EV+Cash-Debt-minority interest). Finally, I divided this equity value by the shares outstanding (530 million) to arrive at a share price of $281 .

All values in the analysis are in millions.

Created by the author using 10-K and Bloomberg Created by the author using 10-K and Bloomberg Created by the author using 10-K

{kind=link}

Risks

What if the Fed doesn't cut rates soon?

If the Fed decided to keep rates higher for longer than expected, I don't believe it would be a big issue because, as I mentioned in my thesis, even with the aggressive interest rates hike over the past year, Caterpillar still managed to grow by 17%. However, not cutting rates soon means that companies abroad would only buy the necessary equipment for their projects and Caterpillar might have to cut prices in order to be able to compete with others.

Losing Market Share

Caterpillar's revenue in the Construction segment from Asia-Pacific dropped by 13% YoY. I believe that one should look at this drop in revenue as a serious issue because Asia is one of the markets that still has huge growth potential when it comes to construction. So, Caterpillar has to find a way to capitalize on the growth.

Conclusion

In conclusion, I believe that Caterpillar's current stock price is still a little too hot for me to buy into and the current rally in the market after the PPI data isn't helping either. But if the CAT stock was to not reach my entry target, then I won't be too upset about it because I think taking a position now isn't worth the risk (at least from my point of view). But as I have said before, for me Caterpillar is a long-term play because I don't know when the Fed might start cutting rates, while the Infrastructure and Jobs Act is a 10-year long act. I think with the current market I will just have to sit back, hold a lot of cash, and wait for the market to prove itself to me.

For further details see:

Caterpillar: Long-Term Growth Appears Inevitable