CAT - Caterpillar Q1 2023 Earnings Preview: What To Consider

2023-04-24 22:28:49 ET

Summary

- Caterpillar's earnings release is a key moment to assess industrial sectors and get a glimpse of developing macro trends.

- I believe Caterpillar should release a top line beat, while it will be harder to see a bottom line beat.

- As manufacturing activity seems to be at a standstill, Caterpillar could be in trouble. But the company has some strong sources of recurring revenue, which can't be overlooked.

Introduction

Caterpillar ( CAT ) will report its Q1 2023 earnings on Thursday, April 27, before market open. I will share what I'm expecting for upcoming earnings and the most relevant data to look for.

The economic environment

Caterpillar is the world's leading manufacturer of construction and mining equipment, with 2022 sales and revenues of $59.4 billion. The company operates on every continent and divides its business into three main segments: construction, resource and energy and transportation. It also provides different services, such as financial.

I have often recalled how there are three macro trends that are true tailwinds for Caterpillar:

- The Infrastructure Investment and Jobs Act passed in late 2021 is going to boost construction equipment use and demand.

- Revitalization of American Manufacturing has become a political priority for the U.S.

- The role of critical minerals in clean energy transition will lead to increasing mining activity, boosting the need for highly-technological and competitive equipment.

However, some FRED data hint that manufacturing activity in the U.S. could have reached a plateau (the FRED post was first published in 2018, but all the data are updated to Q4 2022).

Upcoming earnings: What to look at

Margins, inventories, backlog. These three main aspects Caterpillar's management already discussed with analysts during the Q4 2022 earnings call will be closely looked at during the upcoming earnings call.

In addition, things are normalizing and this should lead the company toward following better the typical season pattern of its sales. Usually, Q1 is a quarter where sales are a bit slower compared to Q4.

Let's go a bit deeper.

Margins

Caterpillar, as many other equipment manufacturers, saw some pressure on its margins shrink in Q1 2022 vs. the same quarter of the previous year. This was because of inflationary pressure, linked with supply chain constraints, made it more expensive for Caterpillar to produce equipment that already had been sold in 2021 when inflation was still not reflected on pricing.

In the meantime, also thanks to strong equipment demand in 2022, the company was able to take appropriate pricing measures to offset higher production costs.

Therefore, when considering margins, in Q1 2023 we will have very easy comps. This is why I think favorable price should now lead to strong segment margins in Q1. Price should fully offset production costs. Since the operating profit in Q1 2022 was at 14.4%, any number above 16% would be very much welcomed. However, in Q4 2022, Caterpillar's operating margin already was at 19.8%. Should we expect the company to break the 20% barrier? I personally believe it won't, even though it could come close. Why do I think it will be hard for Caterpillar to come above 20%? Usually, Q1 is the weakest quarter in terms of sales. However, SG&A and R&D expenses are almost always evenly spread out across the four quarters of the year. This makes them weigh more on Q1 margins, compared to what happens in the other quarters.

My forecast: Caterpillar's revenues at $15 billion and its operating margin at or above 17%.

Let's keep in mind that in a higher inflationary environment it's harder to protect one's margins. In fact, thanks to inflation, a relatively large portion of the sales increase is due to price realization. This makes it harder to benefit from operating leverage compared to what happens in low inflation economic environments.

Inventories

Supply chain bottlenecks made inventories increase almost to all-time highs. It was quite common to see that many machines could not be completed because the company was not receiving some components necessary to finish them.

Now, as Caterpillar sees these bottlenecks ease, Caterpillar has started delivering its finished products at a quick pace. Therefore, dealer inventory is increasing. In Q4 2022, for example, it increased by about $700 million in the fourth quarter. This made the company confident enough to disclose, during the last earnings call, that within Construction Industries, dealer inventories were in their typical historical range of three to four months of projected sales.

In Q4 2022, Caterpillar saw its inventory decrease by $600 million. We will need to look closely at the new data to make sure Caterpillar is back on track in terms of manufacturing and delivering its products.

Forecast: Caterpillar's inventory will decrease by another $500 million, while dealer inventory will have reached normal levels across all the three main segments.

Backlog

As dealer inventories are increasing, a question arises. What's happening to Caterpillar's sales? Are they slowing down? Are they increasing? In other words, what's happening to the order backlog of the company?

We know that in Q4 2022 Caterpillar's order backlog increased by $400 million QoQ. At the end of last year, Caterpillar had a $30.4 billion backlog, which is about 50% of the expected sales. Considering the fact that inflation also seems to come down a bit, chances are this backlog will generate higher margins, closing the circle around the three main aspects I am considering.

Forecast: Caterpillar's backlog will increase once again, even though at a slower pace. I'm expecting a growth of $200 million QoQ.

Upcoming earnings: Expected numbers

Clearly, a company as big as Caterpillar can't be understood only through what we have seen so far.

As we move toward more normalized operations, where seasonality patterns can be once again seen, Q1 should not be a quarter to compare with Q4. However, I do believe we will still see some sales strength leading Caterpillar to reach at least a revenue of $15.5 billion, beating expectations. However, EPS will hardly be above $4 because of what I have said above about Q1 margins.

In the last few months, the dollar has weakened a bit and this could constitute a further tailwind for Caterpillar's earnings report, since the company sells all around the world.

There also are some other key aspects that are making the company quite interesting as an investment.

First of all, among its three segments, Caterpillar's has an underdog, which I believe is the Resource Industries one. Caterpillar offers heavy construction and surface and underground mining machinery. This segment is going to explode in the future because the energy transition should support strong commodity demand, expanding the total addressable market for Caterpillar. This is why I expect Resource Industries to grow by 20% in 2023, which would make it an almost $15 billion segment.

Secondly, Caterpillar is consistently investing in its services business. In 2022, the company generated more than 30% of its revenues from this business, with $22 billion. Caterpillar has now more than 1.4 million connected assets, up from 1.2 million in 2021. In addition, 60% of its new delivered equipment has a customer value agreement and it is linked to the Cat Central app that aims at driving growth in e-commerce sales to users.

And Caterpillar is not done growing in this business, as it targets to achieve our $28 billion services target in 2026.

In a cyclical company like Caterpillar, such a massive source of sure and steady revenue is a great plus. In fact, services and spare parts sales have very high margins and often require low capex. Therefore, they generate a lot of free cash flow. More or less, Caterpillar is quite consistent in generating at least $3 billion of free cash flow per year, even when market conditions are tough. As Caterpillar's services keep on growing, I expect to see an impact in terms of free cash flow generation. Truly, this is Caterpillar's hidden and overlooked gold mine .

In addition, speaking of free cash flow, let's keep in mind that it will see a strong tailwind from the fact that inventories are going down. We could see an impact of an extra $600 million per quarter and this would make the stock seem cheaper on a price/fcf basis. Considering Caterpillar already trades at a free cash flow yield of 6%, the stock seems cheap compared to the results it could release.

It's particularly important to make sure Caterpillar generates enough free cash flow to support its dividend and its Dividend Aristocrat status.

It's well known Caterpillar has a safe dividend that yields a 2.2%, whose five-year growth rate has been an interesting 9%. The payout ratio is 34%. This goes along with share repurchases, whose amount can vary depending on economic conditions. In 2022, during what probably seems the strongest year of the cycle, Caterpillar spent $4.23 billion to repurchase its stock. This adds up to the $2.44 billion paid out as dividends for a total shareholder return of $6.67 billion, around 6% of the current market cap.

Valuation

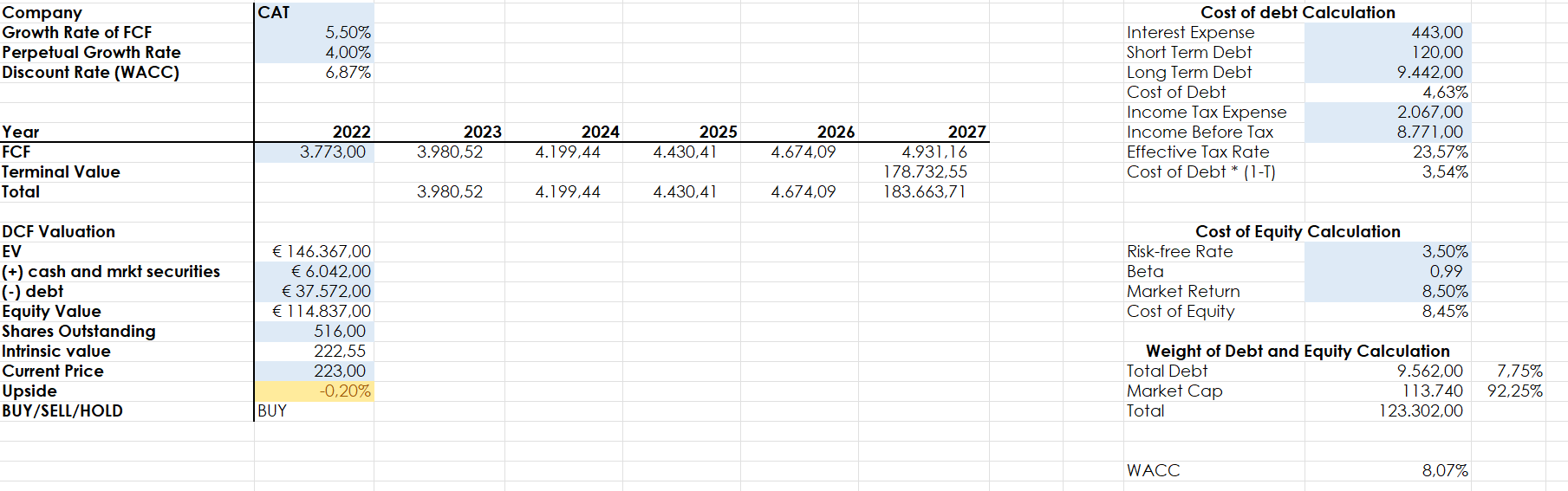

I still believe Caterpillar's revenue in 2023 will come close to $70 billion, which makes the company trade today at a fwd price/sales ratio of 1.6. With a net income margin of 12%, the company is currently trading at a fwd 2023 PE of 13.5. Not exactly cheap, but not even that expensive considering Caterpillar often trades at higher multiples. Considering the consistency in free cash flow generation I ran this discounted cash flow model and came to a result that confirms what we are seeing from a multiple perspective: Caterpillar stock is neither cheap nor expensive, but it's actually trading near its fair value.

{kind=link}

This may lead some investors to wait for a further drop. However, buying at what can be considered fair value territory already is buying a good deal. This spot, for example, could be the right one to initiate a position with a small amount.

Conclusion

Caterpillar will probably beat top-line estimates, while it might come short on the bottom line. However, this earnings report is not just about revenue and EPS. As I tried to explain, it's much more relevant for investors to know that margins are moving in the right direction, while inventories normalize and the order backlog, though decelerating, keeps on growing at a reasonable pace. In addition, no investor can overlook Caterpillar's efforts in the services business and the results it's achieving. For these reasons, I do believe Caterpillar is a buy as its earnings report approaches.

For further details see:

Caterpillar Q1 2023 Earnings Preview: What To Consider