CAT - Caterpillar's Potential Shareholder Value Is Nothing Short Of Impressive

2023-05-25 11:54:29 ET

Summary

- Caterpillar's recent earnings report exceeded expectations, driven by strong revenue growth, pricing power, and sales to users.

- The company generates strong free cash flow, maintains a healthy balance sheet, and consistently returns cash to shareholders through dividends and buybacks.

- Despite challenging economic conditions and market trends, Caterpillar presents an appealing investment opportunity with potential upside following a period of sideways movement.

Introduction

I believe we're living in extremely tricky times - at least when it comes to investing and trading. On the one hand, we have an economy that is considered to be extremely resilient, as confirmed by bullish comments and numbers from cyclical companies like Caterpillar ( CAT ) . On the other hand, economic growth is quickly deteriorating. Manufacturing indicators are pointing at a recession, consumer sentiment is weak, and investors are shifting their focus from value to growth stocks.

In early April, I wrote an article titled Caterpillar: The More It Drops, The More I Buy. In that article, I highlighted that Caterpillar benefits from secular growth like the EV transition, supply chain re-shoring, and strong construction demand. However, economic developments caused investors to re-assess cyclical stocks - regardless of how strong they are.

Caterpillar is in a tricky spot. The company benefits from secular tailwinds like the EV transition, supply chain re-shoring, and the fact that general construction spending is still strong.

However, cracks are starting to appear. Economic conditions are rapidly weakening, causing recession fears to trigger weakness in cyclical stocks.

Although CAT shares are attractively valued, I expect a potential move to $180 per share as investors are de-risking their portfolios.

In this article, I'm going to update my case as a lot has happened. Caterpillar has reported its earnings, economic growth is further slowing down, and the market has shifted its focus on growth stocks, leaving value stocks in the dust.

However, there's one piece of good news: CAT is quickly approaching a highly attractive valuation, which is why I am now closely watching the stock to add exposure in the weeks and months ahead.

Now, let's dive into the details!

Caterpillar Fires On All Cylinders

In 2013, Jim Cramer wrote a book titled Get Rich Carefully . Not only did I like the title, but he also wrote about how important it is to listen to a few key companies with major exposure in certain fields.

While there are exceptions and many pitfalls as companies are often careful when it comes to future statements and dependent on current consensus research, it needs to be said that Caterpillar is one of the best indicators of (global) economic growth, thanks to its footprint in construction, energy, mining, and others.

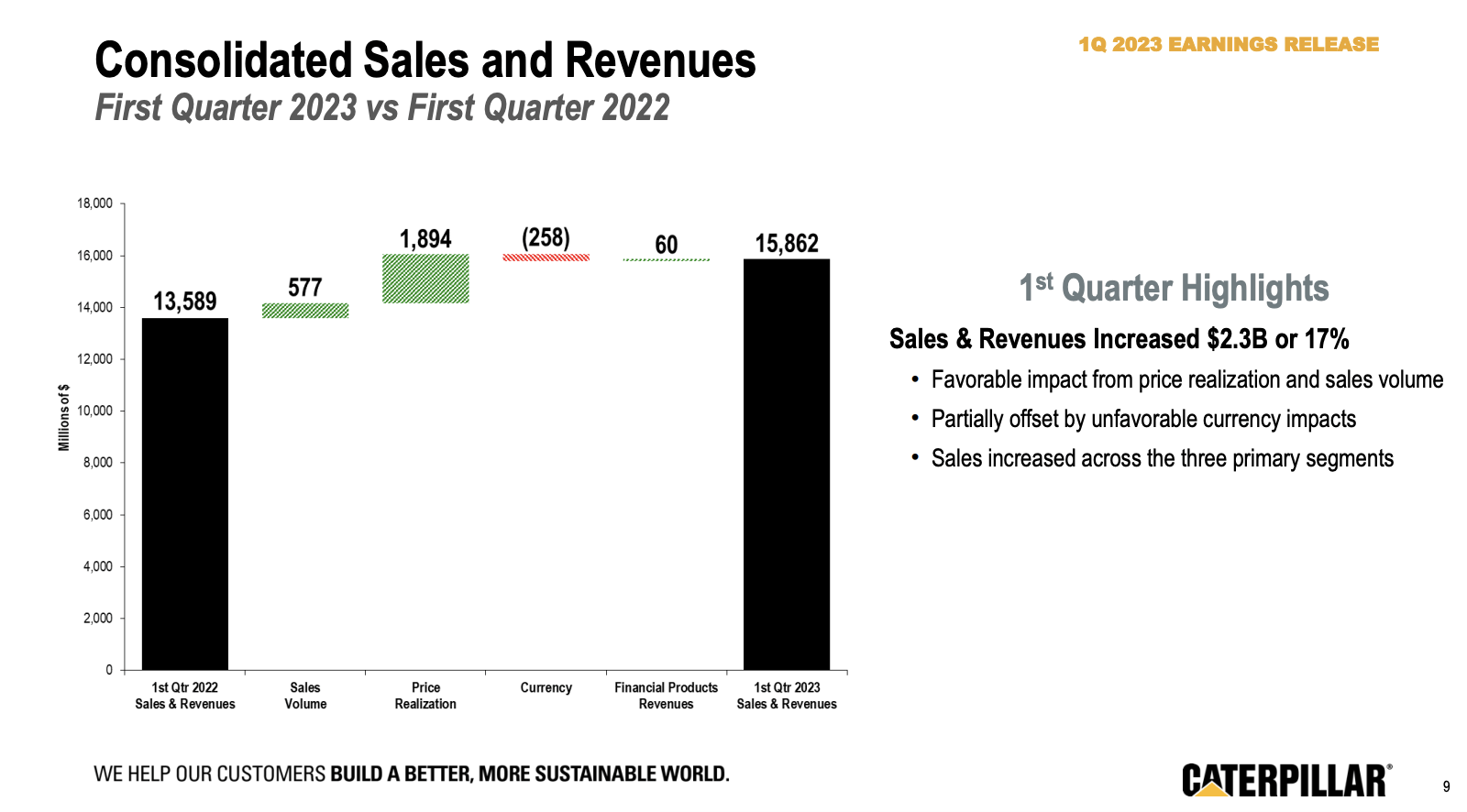

In 1Q23, Caterpillar reported $15.9 billion in revenue, an increase of 16.9% versus the prior-year quarter and a result that exceeded analyst estimates by a whopping $630 million.

During its earnings call , the company revealed a lot about the state of its business and the markets it services, which I will support in this article with my own findings.

First of all, the company noted that sales and revenues exceeded expectations, driven by better-than-anticipated price realization, dealer inventory, and sales to users.

While dealer inventories are a part of sales volumes in the overview below, we see a great visualization of the company's comments. Not only did the company benefit from strong price realization (in a high-inflation environment), but it also benefited from higher sales volumes.

{kind=link}

In addition to the positive implications of higher sales volumes, it's worth noting that this signifies the company's strong pricing power. Unlike many competitors, they haven't compromised sales in favor of raising prices. This is particularly impressive given the current business landscape.

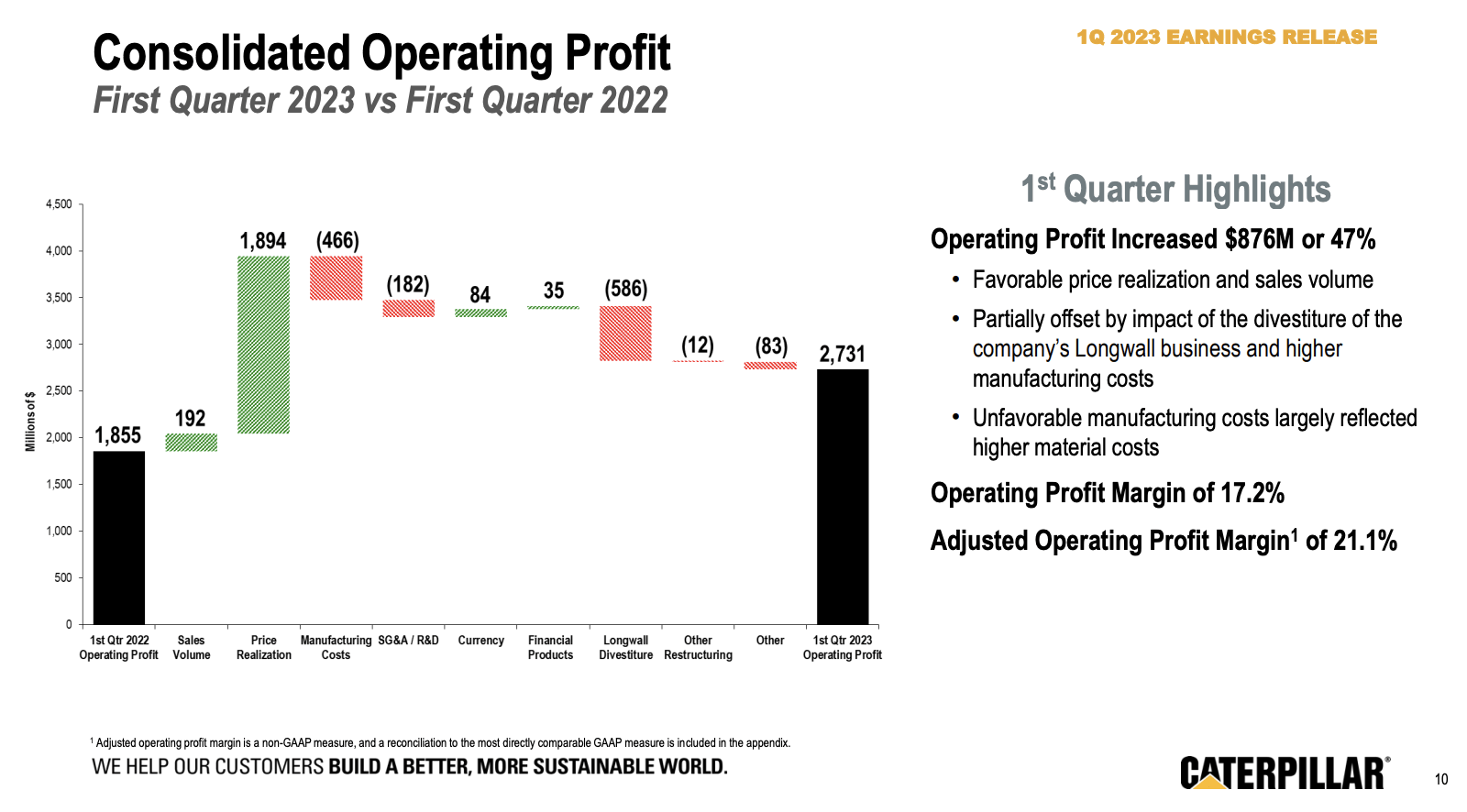

Furthermore, the company highlighted double-digit growth in each of its three primary segments and emphasized that adjusted operating profit margins reached 21.1% - significantly better than anticipated.

Caterpillar attributes this margin improvement to factors like better-than-expected manufacturing costs, including efficiencies and absorption, and stronger price realization on top of volume growth.

The overview below displays these tailwinds. Sales volumes were strong while pricing more than offset manufacturing cost headwinds and even a one-off divestiture.

{kind=link}

Also, the backlog remained very healthy, supported by strong user demand.

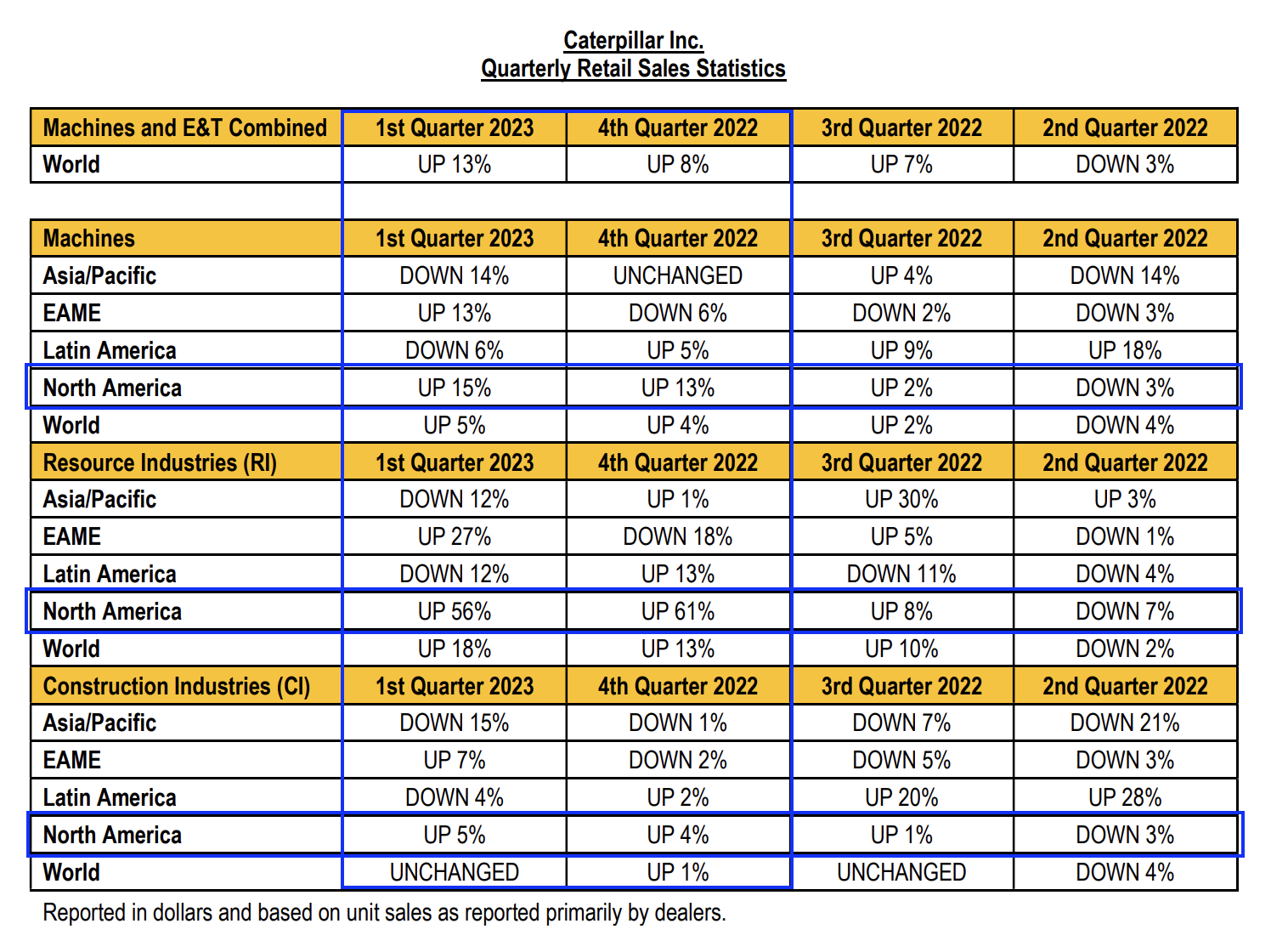

The company reported that sales to users increased by 13% compared to the same period in 2022. In Construction Industries and Resource Industries, sales to users rose by 5%, while Energy & Transportation experienced a 39% increase.

A major driver was strong North American sales to users, especially in nonresidential and residential construction.

The company also saw higher sales to users in the Middle East and improved availability of excavation products.

Unfortunately, Caterpillar saw that sales to users declined in Latin America and Asia Pacific, including further weakening in China, which somewhat underlines that North America is a bit of an outlier in the current global economy. I highlighted this in the overview below.

Caterpillar (Including Author Annotations)

{kind=link}

Even better than a good 1Q23 result is the fact that the company was upbeat about its future.

According to Caterpillar, this year is expected to surpass previous projections in terms of both top-line and bottom-line performance. The company plans for increased sales in the second quarter, following the typical seasonal pattern.

In contrast to the previous year, there will not be a dealer inventory build in the second half of 2023.

For example, in its Resource Industries segment, the company sees healthy demand driven by favorable commodity prices that remain above investment thresholds. This means that mining companies are able to invest in their businesses as operations are profitable.

{kind=link}

Furthermore, production utilization levels are expected to remain elevated, and the aging fleet, coupled with a lower level of parked trucks, is anticipated to support future demand for the company's equipment and services.

The company also cited the energy transition as a factor that would expand the total addressable market and create opportunities for profitable growth. I highlighted this in a recent article on Caterpillar's position in the global energy transition.

But wait, there's more.

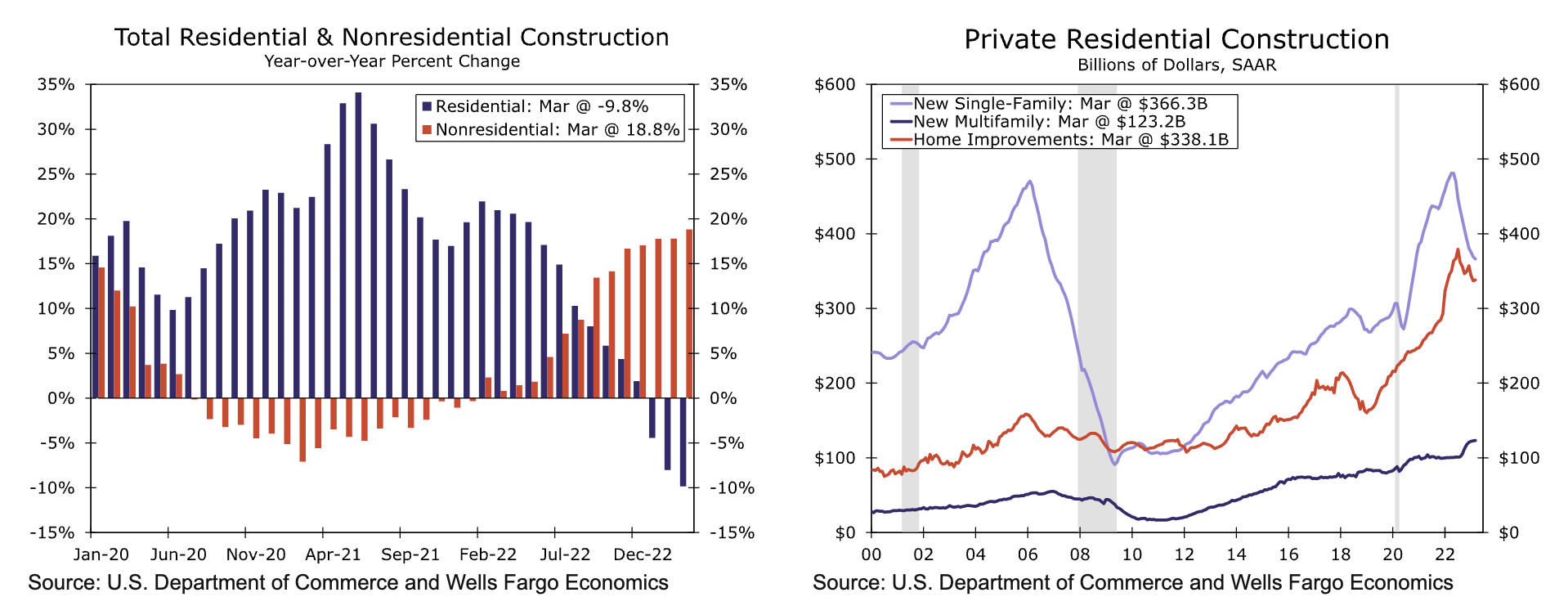

The company also anticipates continued growth in the heavy construction and quarry/aggregates sectors, primarily due to major infrastructure and nonresidential construction projects.

At this point, I have to mention that the company is spot on. While construction, in general, is weakening a bit, nonresidential construction remains in a great place.

According to Wells Fargo (based on the charts below):

The upturn in the nonresidential category was driven by another strong gain in manufacturing project spending. The 4.6% monthly gain brings manufacturing outlays 62.3% above the pace registered in the same month last year. The remarkable rise largely reflects the build out of electric vehicle production supply chains as well as new semiconductor manufacturing facilities.

{kind=link}

Adding to that, while customers in the oil and gas industry remained disciplined (they aren't looking to boost production as they did prior to the pandemic), the company expressed encouragement regarding the continued strength in demand for both well-servicing and gas compression.

In power generation, the company expects healthy demand for reciprocating engines, driven by strong growth in data centers. New equipment orders and services for solar turbines in both the oil and gas and power generation sectors were robust.

The industrial sector was also described as healthy.

Additionally, the company anticipated strength in high-speed marine transportation as customers continued to upgrade their aging fleets.

So Much Shareholder Value

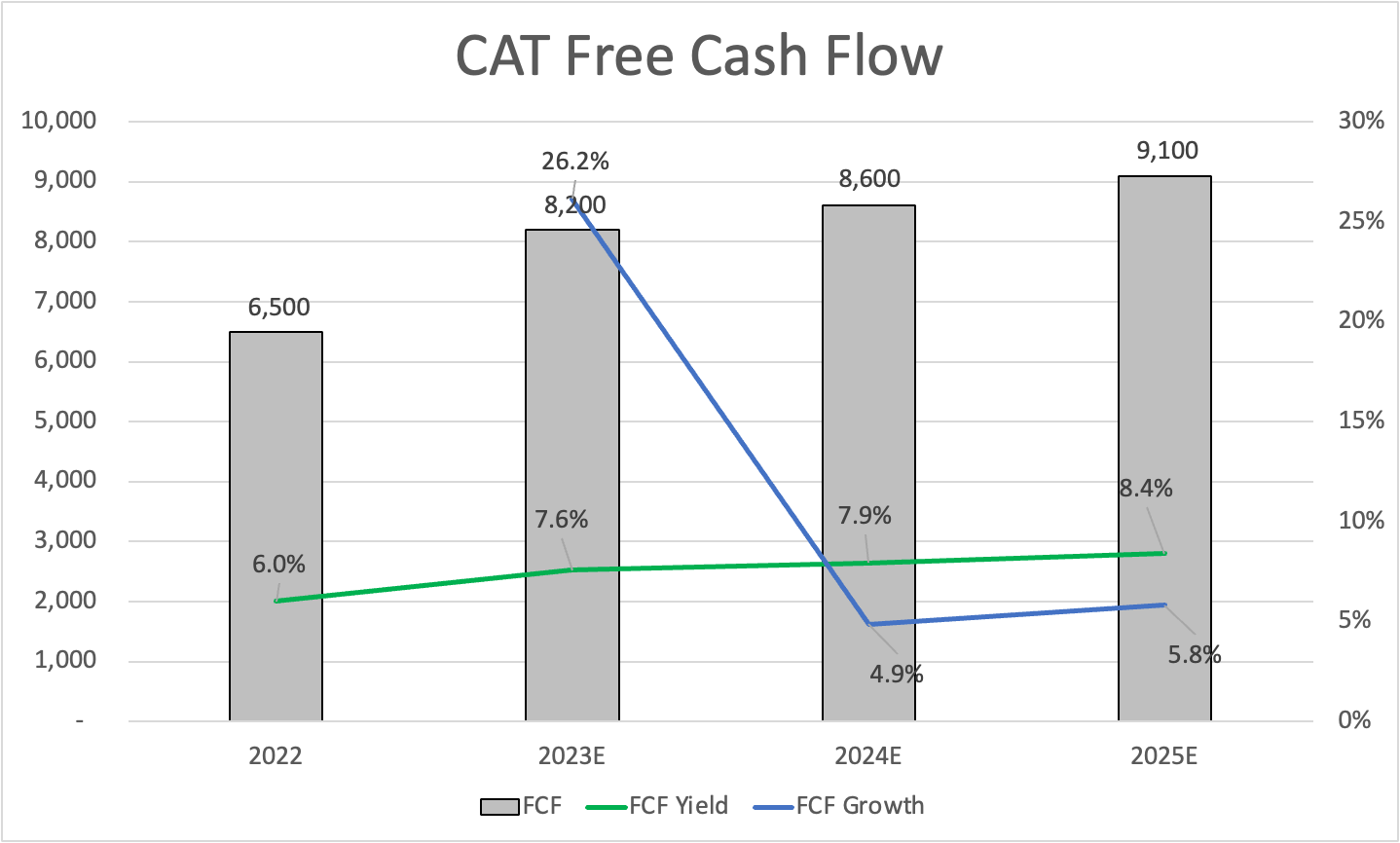

Analyst estimates confirm the company's outlook. Looking at the data below, we do not see a slowdown in the company's free cash flow, a core component of its ability to reward shareholders. Despite an expected CapEx increase from $1.3 billion in 2022 to $1.5 billion in 2023, the company is expected to generate $8.2 billion in free cash flow this year. That number is expected to gradually increase to $9.1 billion in 2025.

{kind=link}

Based on the company's current $108 billion market cap, we're dealing with an implied 2023 free cash flow yield of 7.6%. That number is set to grow to 8.4% in 2025.

This means a number of things. First of all, if these numbers turn out to be correct, CAT is very cheap. The implied free cash flow multiple is in the low 10x range, which indicates that CAT hasn't been this cheap in almost a decade.

Furthermore, it is great news for investors. CAT has a very healthy balance sheet. It has a cash balance of $6.8 billion, a 2.3x 2023E net leverage ratio, and an A+ credit rating.

This means the company does not need to prioritize debt reduction. It can use shareholder distributions to get rid of its (future) cash.

According to the company:

We remain proud of our dividend aristocrat status and continue to expect to return substantially all ME&T free cash flow to shareholders over time through dividends and share repurchases.

In the first quarter, the company generated $1.4 billion in free cash flow in its core business. $1.0 billion was returned to shareholders. This consisted of $600 million in dividends and $400 million in buybacks.

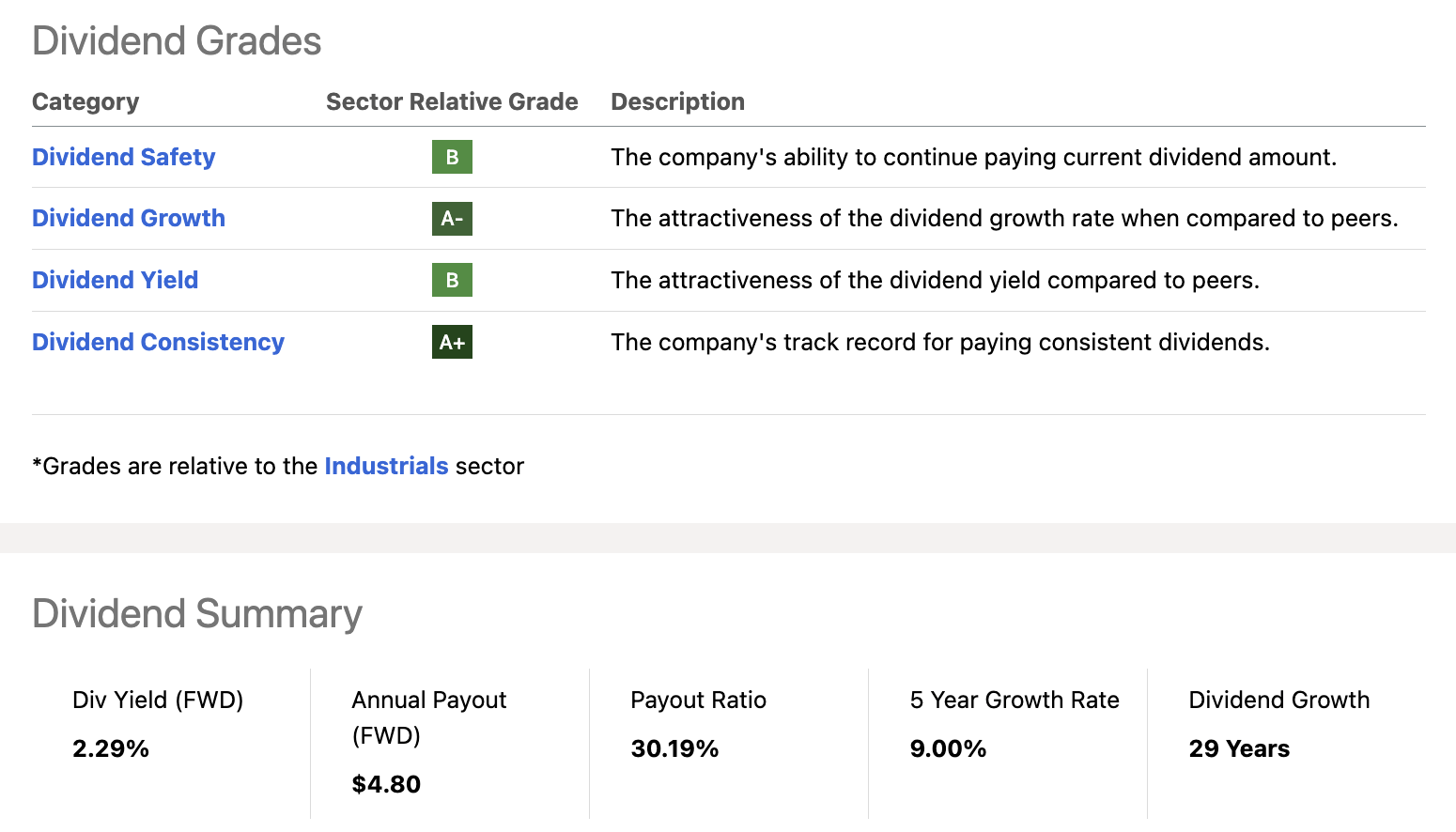

Over the past ten years, CAT has bought back a fifth of its shares. During this period, its dividend has doubled.

- Over the past five years, the dividend has been hiked by 9.0% per year (on average).

- On June 8, 2022, the company hiked by 8.1%.

- I expect a juicy hike in June of this year.

- The current yield is 2.3%.

- The current payout ratio is 30%.

- The 2023E cash payout ratio is also 30%

{kind=link}

Despite all the good news, it needs to be said that markets aren't buying the company's comments and analyst estimates, which is why the valuation is so attractive.

CAT shares are 21% below their 52-week high and down 12% year-to-date.

FINVIZ

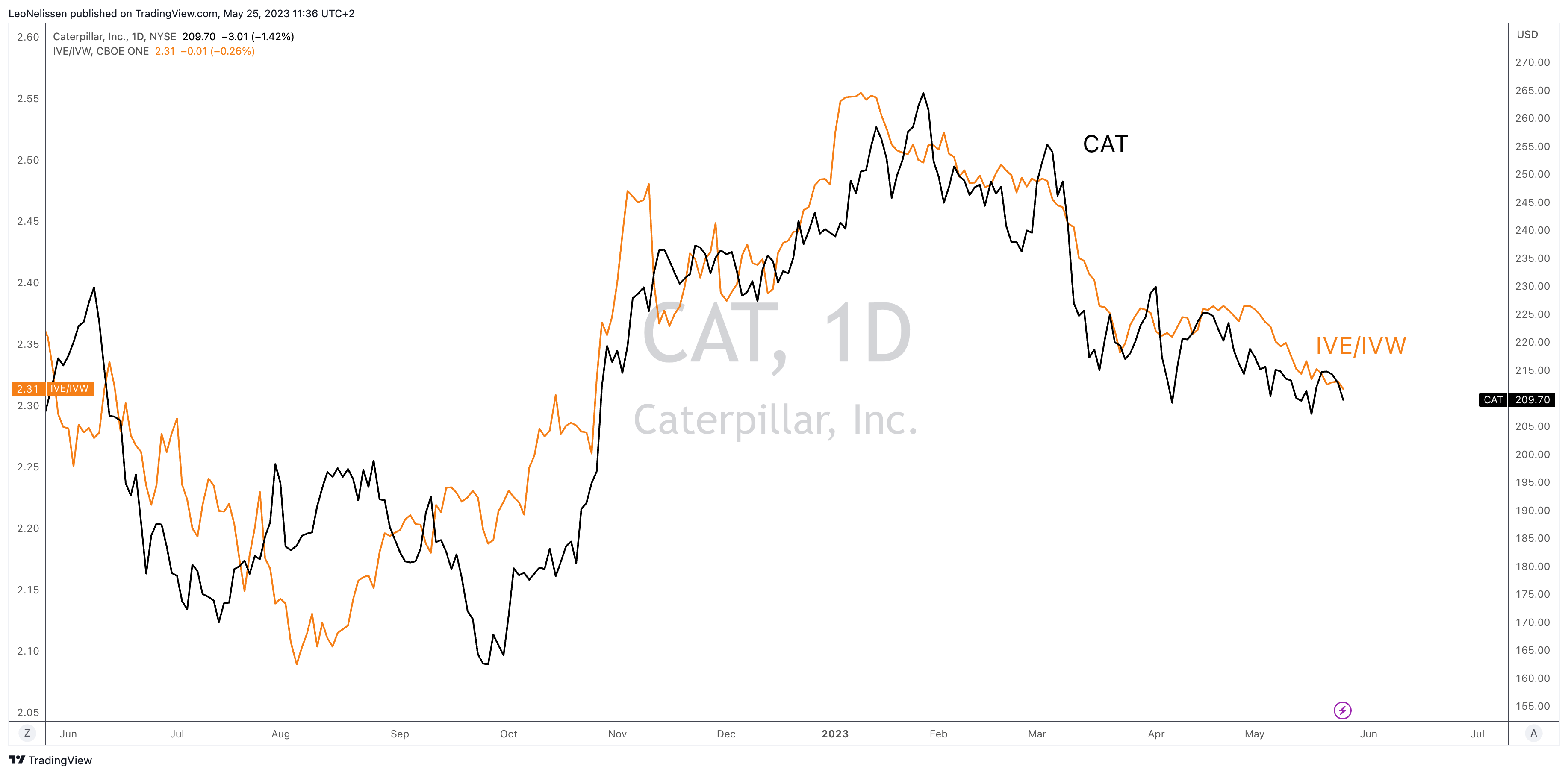

Meanwhile, the S&P 500 is up 7.5% year-to-date as investors have shifted their focus from value stocks to growth stocks.

The chart below compares CAT's stock price to the ratio between S&P 500 value ( IVE ) and S&P 500 growth ( IVW ) stocks. While the long-term correlation doesn't hold, the data confirm the current situation of shifting sentiment.

{kind=link}

The reason is that underlying economic growth is quickly deteriorating, leading market participants to believe that analysts will have to make adjustments to their expectations.

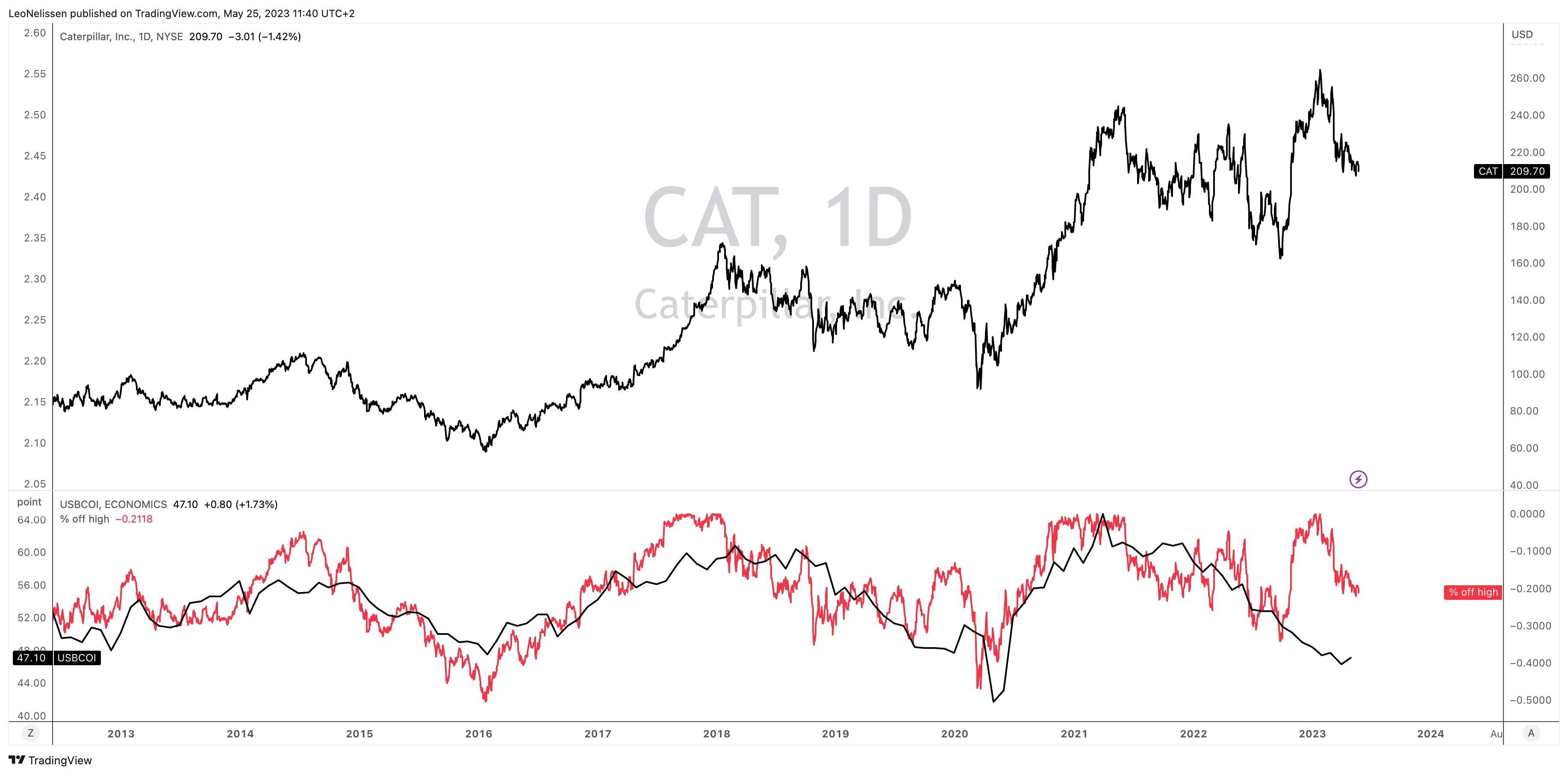

The lower part of the chart below compares the total CAT share price sell-off (% off its all-time high) to the ISM Manufacturing Index.

{kind=link}

Currently, CAT shares are roughly 22% below their all-time high. Usually, when the ISM index is this low, CAT shares are between 40% and 50% below their all-time high.

While I would make the case that downside risks are elevated, there is a good reason why CAT shares are holding up so well. Secular growth provided by construction and materials is not something CAT benefited from during prior downcycles.

With that said, the company's EV/EBITDA valuation is also attractive. Incorporating its $108.3 billion market cap, $4.0 billion in pension liabilities, $28.4 billion in 2023E net debt, and $12.5 billion in 2023E EBITDA, we get an 11.3x multiple.

I believe that we're dealing with about 15% more downside and significant upside.

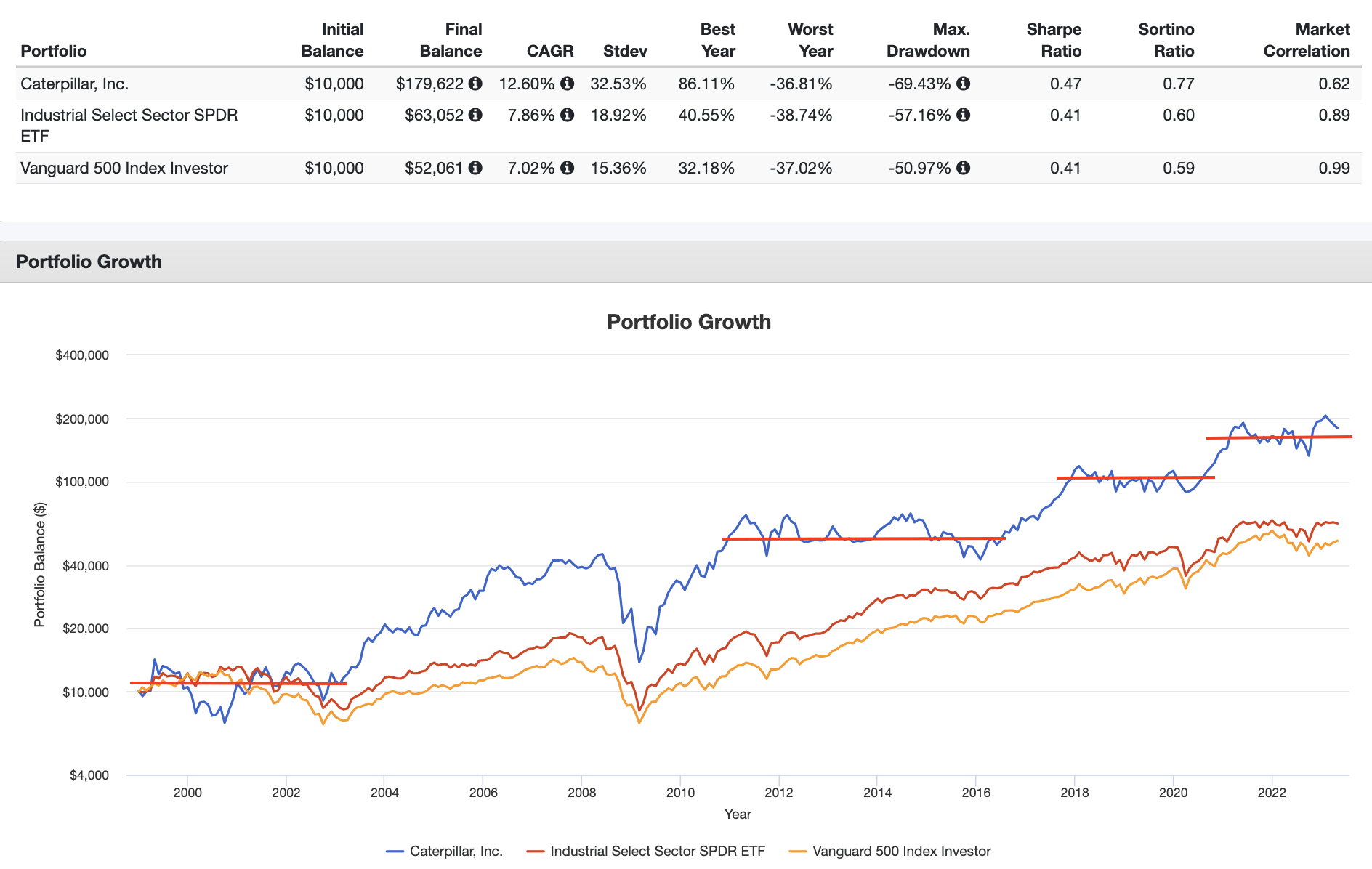

When looking at the company's history, prolonged (and volatile) sideways movements are often followed by significant rallies. This is the reason why the company has returned 12.6% per year since the early 2000s. Despite its elevated standard deviation (volatility), the company has outperformed the industrial select ETF ( XLI ) and the S&P 500 on a risk/adjusted basis (Sharpe Ratio) as well.

{kind=link}

The moment the ISM index bottoms, I expect Caterpillar shares to do extremely well, as investors will get to apply a higher multiple to a company that will benefit from both strong cyclical and secular growth in such a situation.

Hence, I believe there is a high likelihood that CAT shares rise to $320 over the next three years.

While I have close to 50% industrial exposure already, I'm looking to add to my position close to $190. I believe that price offers a great long-term risk/reward.

Takeaway

Caterpillar presents an appealing investment opportunity despite the challenging economic climate and market trends. The company's recent earnings report exceeded expectations, driven by strong revenue growth, pricing power, and sales to users. CAT's healthy backlog and favorable market conditions in various sectors, such as construction and energy, contribute to a positive outlook.

From a shareholder perspective, Caterpillar generates strong free cash flow, maintains a healthy balance sheet, and consistently returns cash to shareholders through dividends and buybacks.

The stock's current valuation is attractive, and historical patterns suggest a potential upside following a period of sideways movement.

CAT shares have faced downward pressure due to shifting market sentiment, but this presents an opportunity for investors. As economic conditions improve, CAT is well-positioned to benefit from cyclical and secular growth, potentially driving the stock price higher.

For further details see:

Caterpillar's Potential Shareholder Value Is Nothing Short Of Impressive