VOLAF - Caterpillar Stock: Company Likely To Beat Q3 Earnings Estimates Focus On 2024

2023-10-23 11:22:44 ET

Summary

- Caterpillar's upcoming quarterly report may provide insight into the company's future amid a global economic slowdown.

- The company has been benefiting from macro trends such as infrastructure spending and the transition to clean energy.

- However, factors such as rising rates and geopolitical instability may impact Caterpillar's overall results in the coming quarters.

Introduction

Caterpillar ( CAT ) will report 3Q earnings at the end of the month. Though quarterly reports can create a lot of unnecessary noise, I believe this report, together with the next one, might be a turning point to understand where the company is headed. In fact, news from the industry is hinting a significant slowdown could be taking place, apart from North America. Therefore, it's important we try to understand what's going on and how it could impact Caterpillar in the short and the long term.

Summary of previous coverage

Since the recovery from the pandemic took place, Caterpillar has been on the run, both in terms of its organic operations and results and its stock performance. There are, in fact, significant tailwinds that the company is benefiting from. In particular, I want to highlight three main macro trends:

- The Infrastructure Investment and Jobs Act approved in late 2021 is literally dispersing money to increase construction equipment use and demand.

- Revitalization of American manufacturing is now an ever-growing political priority for the U.S.

- The role of critical minerals in the transition to clean energy is pushing mining activity, increasing the need for highly technological and competitive equipment.

On the other side, the picture appears to be more complex. In fact, rising rates, hot inflation, and geopolitical instability are all affecting the global economy, slowing it down. The US Manufacturing PMI Index has been falling since its peak in 2021 and it's now in contraction territory, even though in September it has ticked up, suggesting the beginning of a new manufacturing cycle.

All that said, Caterpillar had a business model with a hidden gold mine . In fact, out of its $64-plus billion in revenues, $22 billion comes from services. This is truly massive for an industrial company because it means around one-third of its revenues are recurring. And Caterpillar is not done growing this business because it's targeting to reach $28 billion by 2026.

Earnings Preview

Caterpillar is on a winning streak this year with its past two quarterly reports beating EPS estimates by 29.5% and 21.2%. It literally seems unstoppable and this has been reflected in its stock price: Every time it dips, investors buy it hand over fist. This is why, year-to-date, it has vastly overperformed Deere ( DE ), one of its main peers.

But Caterpillar has been keen on warning investors that this wonderful run won't continue forever. In fact, starting with Q3 there will be some new factors impacting overall results. Let's look at them one by one.

- On a comparative basis, Caterpillar will start to lap the stronger price it benefited from the third quarter onwards last year. True, manufacturing costs will decrease due to lower inflation, but for this quarterly result, it's more important to know that price benefit will reduce as well. As a result, we can't expect another quarter of strong margin improvement.

- Customers are becoming capital-disciplined. This may hurt Caterpillar's financial branch. However, if customers are in need of replacing their equipment and choose not to, their fleet age will increase, creating demand for services and future equipment.

- Usually, Q3 shows weaker sales compared to Q2, though YoY it can have higher sales and higher margins.

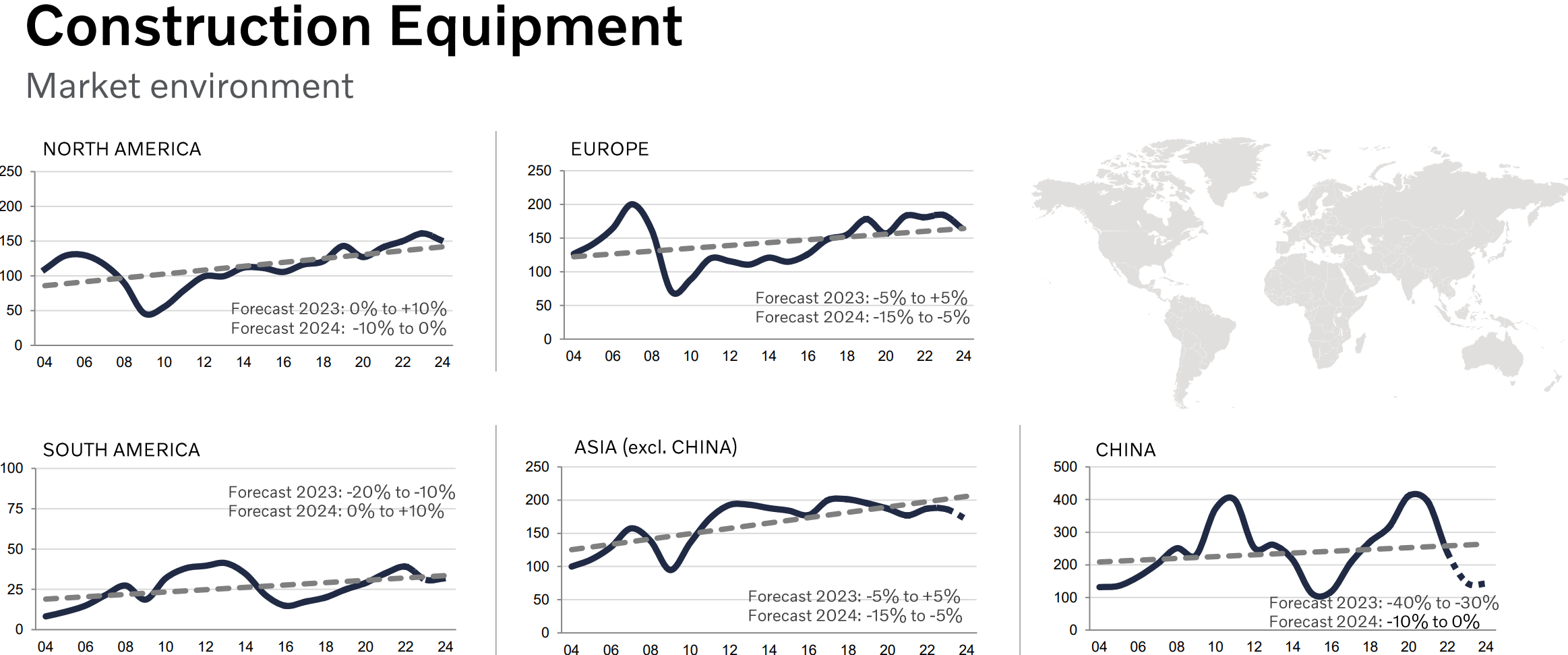

In addition, we can look at two companies related to Caterpillar: Volvo Group ( VLVLY ) and Terex ( TEX ). The latter has recently said it expects FY 2023 EPS to be $7.05, lower than the estimate of $7.16. The former, in its Q3 earnings report , has - as expected - delivered strong sales, but order intake in construction equipment decreased by 27% with deliveries down another 21%. The decline in orders, according to Volvo, was "largely driven by lower demand in China following the economic slowdown as well as by cautiousness among customers and dealers in Europe." The Volvo Group also reported that the only region where it saw construction growing was North America, thanks "to continued large infrastructure projects and a strong commercial construction sector that more than offset weaker residential construction amid rising interest rates." While construction is not as important for Volvo compared to trucks, it is for Caterpillar because, as of last quarter, it makes up 41.7% of total sales. Of this 41.7%, which in the last quarter was worth $7.2 billion, around 55.5% is earned in North America. From what Volvo reported, I can assume this quarter will see North America grow within Construction Industries, while total sales of the segment will shrink some. Since Caterpillar is highly exposed to North America, I think the dynamism of the continent will offset the weakness seen elsewhere. Nonetheless, we won't see this segment keep on exploding as we have seen.

The Volvo Group also released its forecast for this fiscal year and the next. It looks gloomy. For Construction equipment, North America is the only continent clearly still expanding, while Europe and Asia (ex. China) will be around flat, and South America and China will be down big. But if we look at Volvo Group's forecast for 2024, it is not pretty: Even North America will be down YoY.

The Volvo Group Q3 2023 Results Presentation

{kind=link}

I think we have many signs showing the cycle has peaked and that now we're moving toward a new trough.

After all, in the last earnings call, Caterpillar acknowledged both growing demand in Energy and Transportation, while it has seen some softness in Resource Industries and Construction Industries. In terms of sales, which matters most as we try to figure out what the report will be like, Caterpillar's management said that we should see a decrease.

We continue to believe the energy transition will support increased commodity demand, expanding our total addressable market and providing further opportunities for profitable growth. In heavy construction and quarry and aggregates, we anticipate continued growth due to major infrastructure in non-residential construction projects. In Construction Industries, as is our normal seasonal end, we expect lower sales compared to the second quarter. In Resource Industries, which can be lumpy, we anticipate slightly lower sales compared to the second quarter. We expect sales in Energy & Transportation will increase slightly compared to the second quarter.

So we know sales will be lower than $17.3 billion, but higher than $15 billion (Q3 2022 results). I'm personally inclined to see sales above $16.2 billion because I'm factoring in a general 8% price increase compared to last year. Now, though sales are going to be slower, both because of seasonality and softening demand, as we move toward the bottom line, operating profit margins should expand YoY. Of course, since third quarter usually sees lower volume compared to the prior quarter, if we compare the two, operating profit margin will probably be down.

Since in Q2 2023, it was 21.3%, while in Q3 2022 it was 16.5%, we know the range within which it will fall this quarter. It's still quite wide. Personally, I believe we will still see an operating profit margin around 20%, in the range between 19.5% and 20.5%. Why do I say this? Because, compared to last year, commodity prices have gone down further, creating less pressure on cost management.

This gives us an operating profit of 3.24 billion. Considering a 22% tax rate, we can expect a net income of $2.53 billion. Divided by the 510 million shares outstanding, we reach an EPS of $4.95, which is higher compared to consensus EPS estimates of $4.77. This will probably make the market celebrate, but we might actually see an initial surge in price, followed by a correction as soon as the earnings call starts and the outlook for the future will be a bit dimmer compared to the past. Expecting Q4 earnings around $4.87, we have 2023 EPS forecasted to be $20.28. This doesn't lower that much the fwd PE, since it brings it from 12.48 to 12.32. This is true if the number of outstanding shares remains the same. Since Caterpillar does buybacks, the multiple might come down a little bit. But I think it's clear that Caterpillar is not currently trading at a hidden discount. What matters most is what is the 2024 multiple it's trading at. Next year, it might be hard for Caterpillar to beat its 2023 results, which are the last leg of a relay started in late 2020. We might see a decline in EPS, assuming a flat share count. Next year, the big game changer should be share repurchases. At $250 per share, the stock for me is rated as a hold. To buy it with a margin of safety, I would use no more than a fwd PE of 11, which leads to a price of $223. Even better, if the stock falls below $210, I would see it offering a better margin of safety. Of course, if it dips below $200, we are before a potential strong buy.

Takeaway

This preview might not be pleasant for many investors and fans of the company. I want to reassure both: Caterpillar is in a cyclical industry, and though it has a strong service business, it can't be totally immune from the downward part of a cycle. Many signs suggest this time is coming or, perhaps, it has already begun. Is that a real issue? Not really. Long-term investors have a double choice: Either lock in some gains or just keep holding onto their shares.

Those who are still waiting to initiate a position will probably benefit from some downward pressure on the stock which will lead to valuations with a higher margin of safety compared to now.

In any case, let me end with one picture. These are my two-year-old son's favorite toys. Any doubt about Caterpillar brand's strength and its future?

{kind=link}

For further details see:

Caterpillar Stock: Company Likely To Beat Q3 Earnings Estimates, Focus On 2024