CAT - Caterpillar: Strong Growth At The Top Of The Cycle

2023-07-31 00:00:03 ET

Summary

- Caterpillar demonstrates strong momentum in Q1 results, with healthy profit composition, and maintained sales momentum.

- CAT stock has strong exposure to the North American market, and its debt burden has been eased through strong earnings and without large borrowing in recent years.

- Weaknesses and risks include drifting cash flow and high inventory levels, while the business cyclicality could point to slower growth in the near term.

Investment Thesis

Company Overview

Caterpillar Inc. (CAT), founded in is a global manufacturer of construction and mining equipment, diesel and natural gas engines, industrial gas turbines, and diesel-electric locomotives. The company has various reportable segments, including Construction Industries, Resource Industries, Energy & Transportation, and Financial Products.

Strength

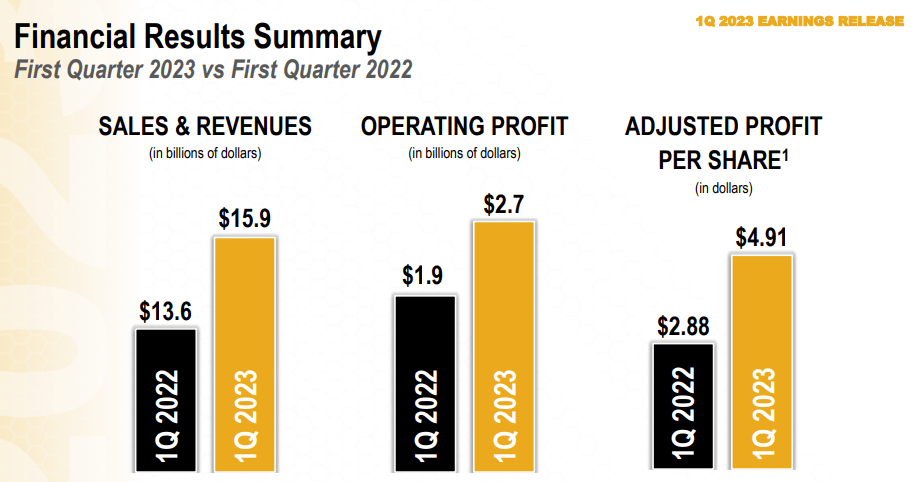

Q1 results showed strong momentum. Caterpillar has about 17% growth in Sales and revenue YoY while operating profit during the same period was up about 42%, resulting in a 70% YoY increase in per share basis.

Caterpillar: Sales and Revenue (Company Presentation 2023)

{kind=link}

The company has benefited from accelerated mining and commodity demand, growing global development in the energy complex and the increasing infrastructure investment in the US. It is well positioned to benefit not only from the traditional sources of fossil fuel but also the renewables because green energy growth sparked in-kind construction needs.

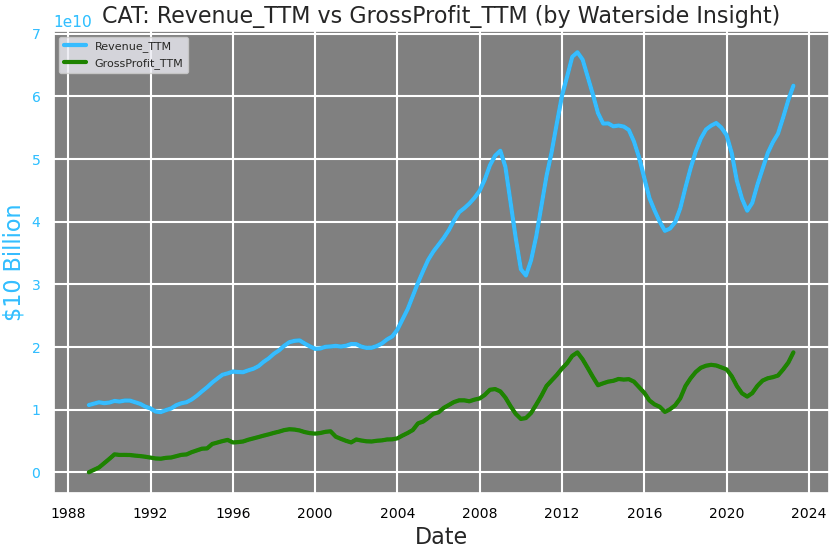

Historically, Caterpillar's revenue and gross profit reached highs in 2012-2013. During the most recent quarters, the company has returned to these levels once again. Construction Industries had 18.8% segment profit in 2022, while Resource and Energy & Transportation had 14.8% and 13.9% respectively.

Caterpillar: TTM Revenue vs Gross Profit (Calculated and Charted by Waterside Insight with data from company)

{kind=link}

What's interesting to us is what drove the company's profits. Its main contributors to its operating profits can be categorized as sales volume, price realization, and manufacturing cost, with the last to be negative usually. Comparing the trends we can see sales volume used to contribute the most to operating profits, and it was also the biggest drag at the depth of the pandemic. However, in the past four quarters, price realization became the largest contributor, while the manufacturing cost jumped to almost symmetrically cancel it out. Fast forward to the latest quarter, the price increase still holds the advantage while cost mitigation has taken shape. All of this was happening while its sales volume held up. This is a healthy and strong profit composition. In fact, its sales volume plus price realization advantage over manufacturing cost was at its highest since Q3 2021, at 4.48x. But with costs coming down, the company has room to lower prices. That could spur or maintain the sale volume, on the other hand, so the operating profits can at least stabilize at the current level, if not with more room to grow.

Caterpillar: Operating Profits Contributors (Charted by Waterside Insight with data from company)

Regarding how different regions impact Caterpillar's sales, there has been a myth that Caterpillar is too international and that its US exposure isn't enough to capture the domestic construction boom led by the Inflation Reduction ACT. From the chart below, we can see North America is by far its largest source of sales across the segments. It has decent exposure from Asia/Pacific and some from the Inter-segment, but the size isn't comparable to the impact coming from North America. The largest segment of Construction from North America dominates the incoming sales. In particular, 41% of its sales and revenue came from the US and 59% are outside of it. And by application, it has about one-quarter of sales come from each of the four categories, Construction, Resource, Energy & Transportation, and All Other. Construction only seems to dominate in the North American region.

Caterpillar: Sales - Segment vs Region (Charted by Waterside Insight with data from company)

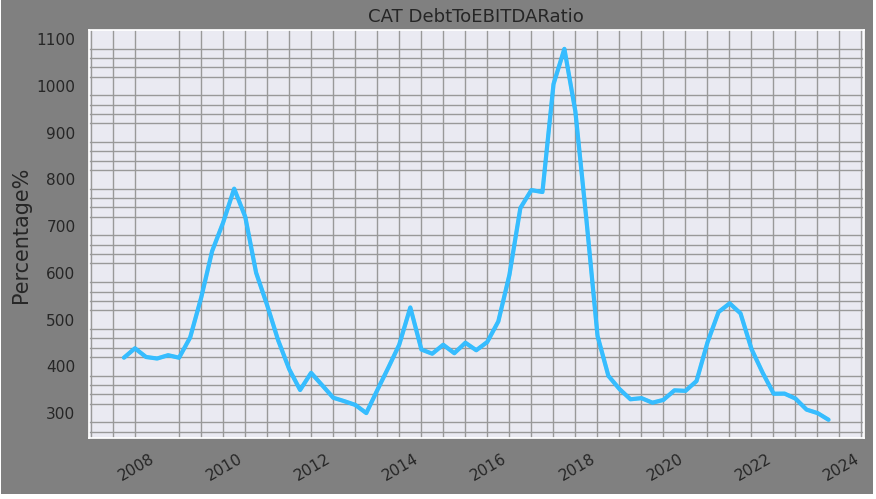

Also, Caterpillar's debt burden has been eased. Although over 3x debt-to-EBITDA ratio is nothing to sneeze about, it is the lowest for the company since long ago. This is mostly due to its fast EBITDA growth. In the past 5 years, it has increased EBITDA on a TTM basis by almost 50%, while its debt has only grown in the low single digits.

Caterpillar: Debt-to-Equity Ratio (Calculated and Charted by Waterside Insight with data from company)

{kind=link}

Weakness/Risks

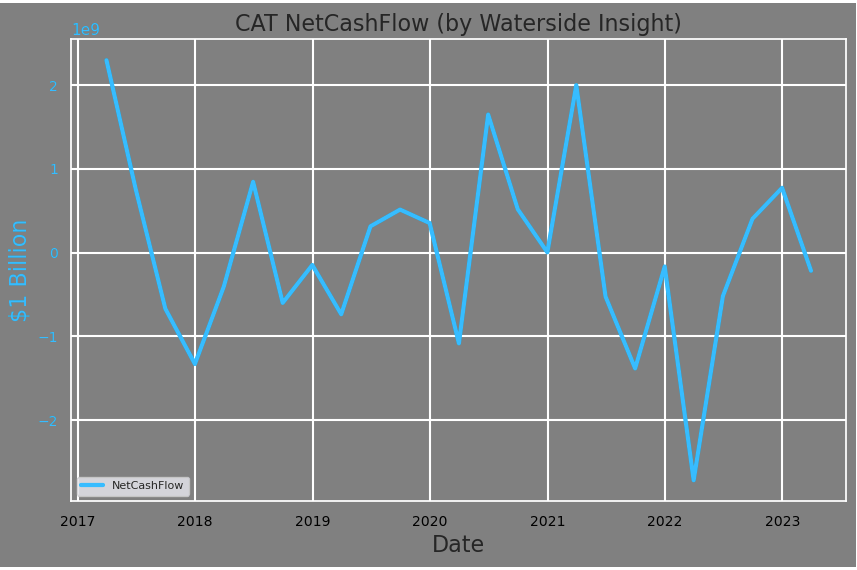

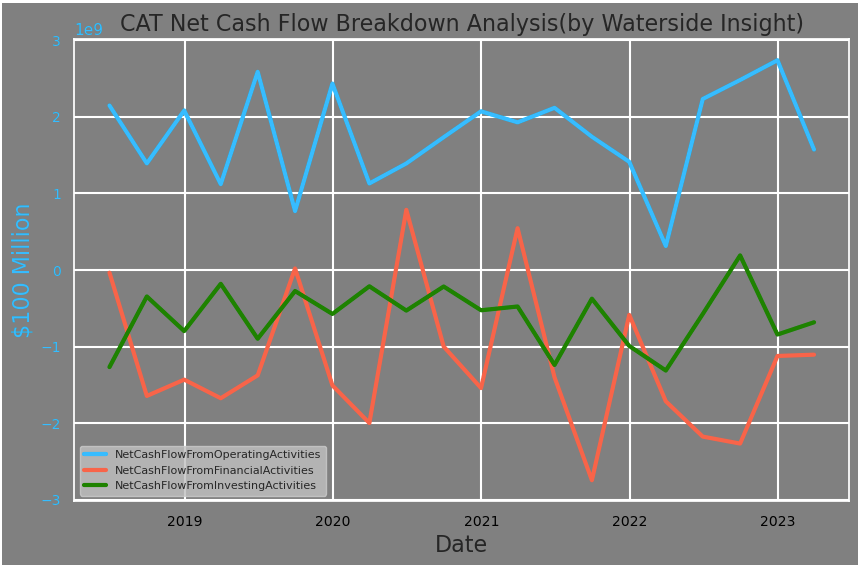

Despite the strong topline and profits growth, Caterpillar's net cash flow was the weakest in 2022 compared to the past five years, and the latest quarterly results are still heading in the negatives.

Caterpillar: Cash Flow (Calculated and Charted by Waterside Insight with data from company)

{kind=link}

It is largely due to the drop in both cash flow from financing and operations in 2022. The company's latest free cash flow margin is only about 5% also. Overall, its cash flow isn't in its best shape in contrast to the overall strong financials. Note that the company made one of the largest shareholder returns in the form of repurchase plus dividends in 2022. We don't expect the company will repeat that any time soon.

{kind=link}

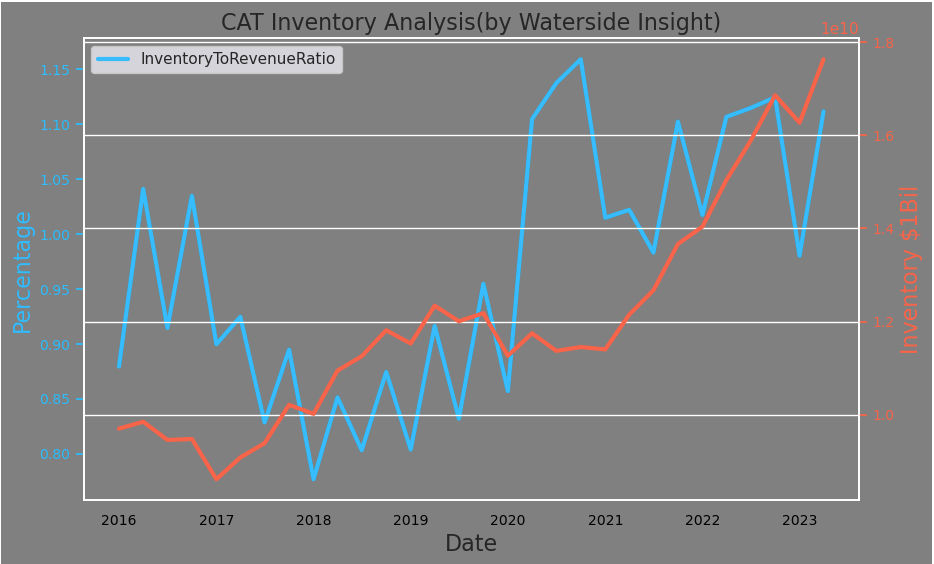

On the other hand, CAT has reached one of its highest inventory levels, even when sales were strong. With the overall supply chain shock normalizing, it will also need to normalize its inventory level as well.

Caterpillar: Inventory (Calculated and Charted by Waterside Insight with data from company)

{kind=link}

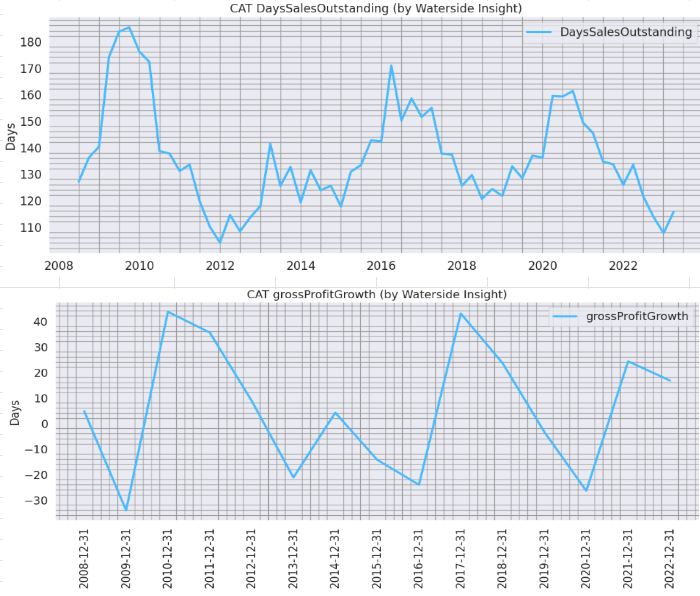

Caterpillar's business seems to follow a pattern that goes from peak to trough within a few years' time. The cyclicality of CAT's growth has reached a local peak based on the pattern formed since 2008. Its days of sales outstanding is at the lower bound of the range from 90 days to about 185 days, and its gross profit growth is at the higher bound of the range from 40% to negative 30% annually. Indeed, the Inflation Reduction Act could provide a boost to Caterpillar's growth in the medium term, but will that be strong enough to extend the peak further or even break out of its previously formed business cyclicality? If not, we could soon see the cyclicalities continues, and both the pace for sales and gross profit growth will slow down.

Caterpillar: Sales and Gross Profit Growth (Calculated and Charted by Waterside Insight with data from company)

{kind=link}

Financial Overview

Caterpillar: Financial Overview (Calculated and Charted by Waterside Insight with data from company)

{kind=link}

Valuation

Based on our analysis above, we use our proprietary models to assess the fair value of CME by projecting its growth ten-year forward. In our base case, we factored in the business cyclicality of Caterpillar with optimism for 2023 but expect a slowdown in the next two years while the cyclicality continues; it was priced at $264.51. In our bullish case, a sharper slowdown was spared and the company was able to forge a stable recovery from any sign of weakness; it was priced at $309.19. In our bearish case, indeed a slowdown not only due to the macro environment but also from cyclicality starting later this year will bring its fair value down to $219.22, almost retesting its low reached earlier this year. Compared with our estimates, the market currently is neither highly bullish nor bearish on the stock, even though it retesting its highest price levels currently.

Caterpillar: Fair Valuation (Calculated and Charted by Waterside Insight with data from company)

Conclusion

There are plenty of reasons to be bullish on Caterpillar, from the infrastructure push in the US to global energy and resources demand. Heavy-duty machines are not a high-margin business, but CAT made great profits along with stable revenue and renewed growth momentum from its existing applications. Twenty years ago, we had the chance to visit the company's factory floor. The impression was neat and efficient. It is well-managed and well-respected. We believe if the macro environment can avoid recession, it will have more upside. But with uncertainty still on the horizon and the inflation fight not yet over, investors are right to stay neutral at the moment. We recommend a hold currently.

For further details see:

Caterpillar: Strong Growth At The Top Of The Cycle