CAT - Caterpillar: The More It Drops The More I Buy

2023-04-09 05:29:44 ET

Summary

- Caterpillar's stock price has started to weaken as investors are starting to price in a manufacturing recession.

- While this isn't fun for the value of my dividend investment, I look forward to buying more shares on weakness.

- The company continues to benefit from subdued CapEx (versus sales), high free cash flow, and a healthy balance sheet.

- Dividend growth investors might benefit tremendously from buying CAT on weakness.

Introduction

Caterpillar ( CAT ) is one of the first stocks I bought for my dividend (growth) portfolio.

The corporation possesses several distinguishing features, such as a robust machinery business with a wide competitive moat, impressive pricing power, substantial free cash flow that is consistently utilized to fuel dividend growth, and the benefit of secular tailwinds such as the current surge in demand for commodities driven by the electric vehicle industry and energy transition.

In January, I wrote that Caterpillar is one of the best places to bet on net zero, as it will benefit tremendously from much-needed investments in mining equipment. However, I also wrote that economic challenges would provide us with better buying opportunities.

Needless to say, I'm still trying to buy (much) more as I am very bullish on a long-term basis. Given economic developments, I believe that the market will give us another opportunity in 2023.

Since then, the stock has dropped 16%. Shares are now 21% below their 52-week high.

FINVIZ

Hence, it's time to assess the risk/reward using new developments, my economic outlook, and the company's ability to generate value. After all, investors should only buy stocks on weakness when these are backed by a solid long-term bull case. Everything else would be long-term wealth destruction.

So, let's get to it!

Markets Are Smelling Economic Weakness

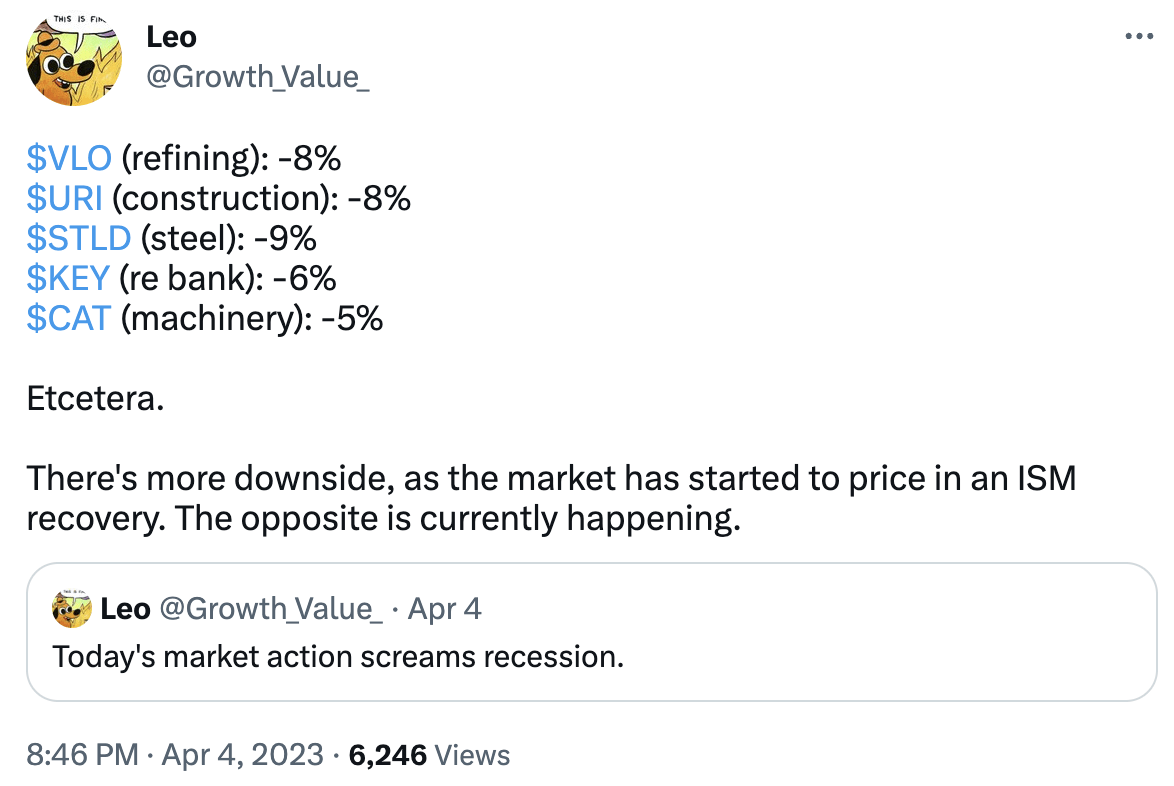

Earlier this month, I tweeted that the market was starting to price in a recession. On April 4, investors sold a wide range of cyclical stocks, including Caterpillar.

{kind=link}

This is part of a bigger trend indicating industrial underperformance. The chart below highlights this, as it shows the ratio between industrial stocks and the S&P 500. Going into this year, industrial stocks were strong, despite economic weakness. Now, investors are betting on significant economic weakness.

Essentially, we're now in a situation where the market tells us macro numbers will come in much worse in the months ahead - or something like that.

Last month, Caterpillar's CEO Jim Umpleby came out saying that construction demand was strong.

{kind=link}

As reported by Bloomberg :

"The input we're receiving from our construction customers in North America is quite good," Umpleby said in an interview at ConExpo in Las Vegas, the largest construction convention in North America. "They see projects coming either from an infrastructure perspective or some of it's government funded, some of it's other, but they're feeling quite good about what they see."

[...] He added these customers are seeing strong activity for so-called "big dirt jobs," such as new battery and chip plants.

He wasn't wrong. I get these comments from multiple industry insiders. Especially in North America, construction demand is holding up quite well, especially in light of supply chain re-shoring, another secular trend benefiting Caterpillar.

This is what the company said in its 4Q22 earnings call :

[...] there was another strong quarter as demand remained healthy for our products and services. Sales rose by 20% versus the fourth quarter of 2021, better than we expected. Supply chain improvements enabled stronger-than-expected shipments, particularly in Construction Industries, and supported an increase in dealer inventories. We achieved double-digit top line increases in each of our three primary segments and saw sales growth in North America, Latin America and the EAME, while Asia Pacific was about flat.

Moreover:

While we continue to closely monitor global macroeconomic conditions, overall demand remains healthy across our segments, and we expect 2023 be better than 2022 on both top and bottom line.

That said, cracks are starting to appear.

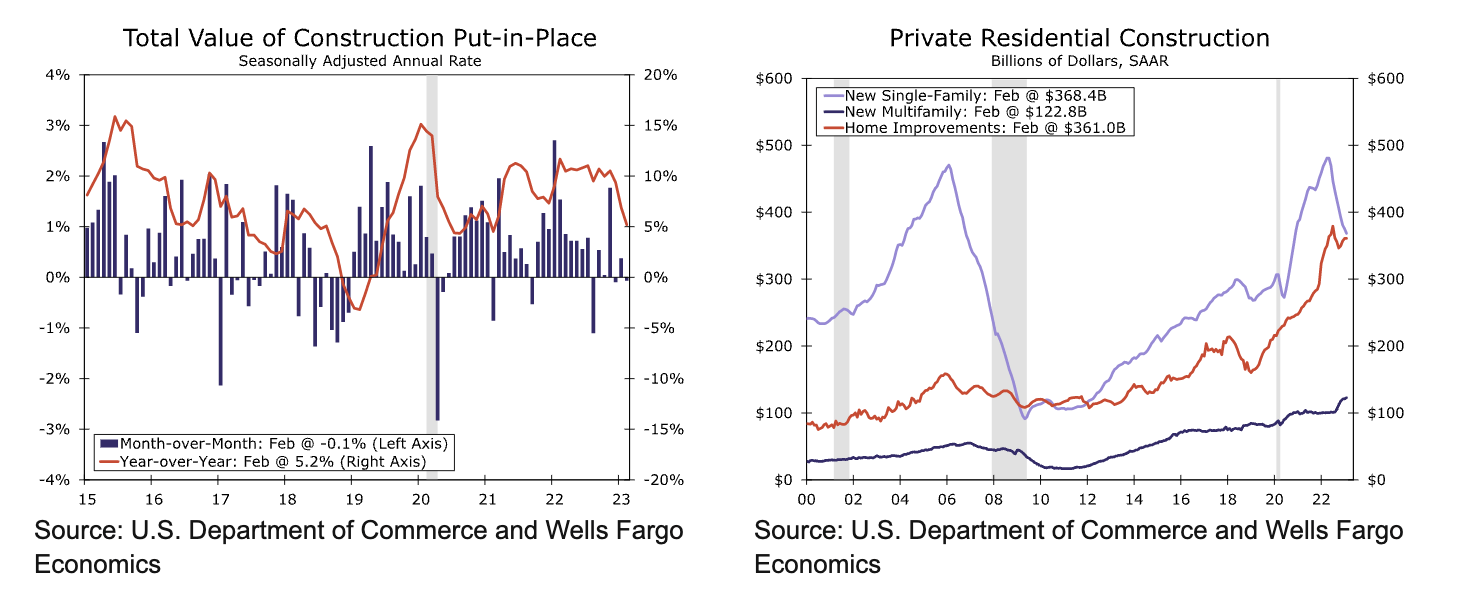

In February, construction numbers in the United States started to show weakness. The year-on-year value of construction was slightly negative at -0.1%. Year-on-year growth dropped to 5.2%. Don't get me wrong, 5.2% is a lot. It's the trend that matters.

{kind=link}

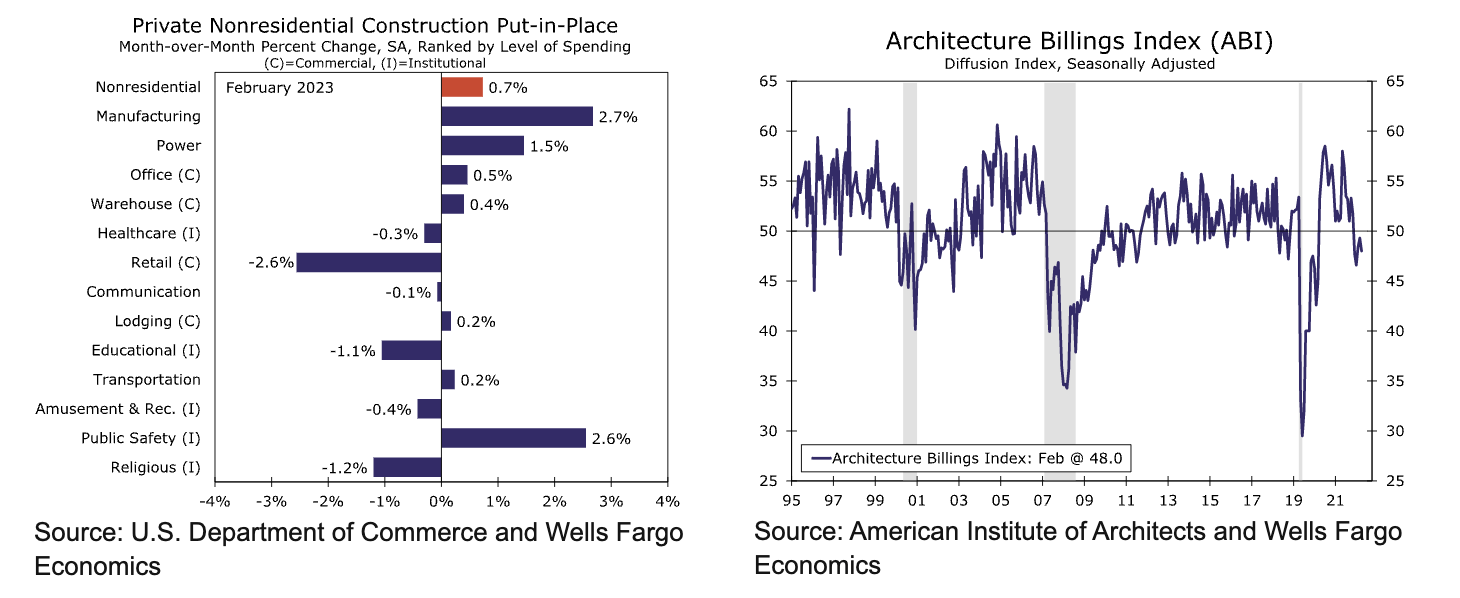

In private residential construction, we see a steep decline in single-family construction. In nonresidential construction, we see significant weakness in retail. Manufacturing is doing quite well, lifted by the aforementioned supply chain re-shoring benefits.

{kind=link}

The leading Architecture Billings Index fell to 48.0 in February. Although this is just modestly below the neutral 50.0 line, it does indicate another month of expected contraction.

Another indicator that continued its downtrend in contraction territory is the ISM Manufacturing Index. This index came in at 46.3 in March, led by weakness in new orders.

Bloomberg

While it is hard to estimate how bad things could get, I believe that cyclical stocks could see more downside.

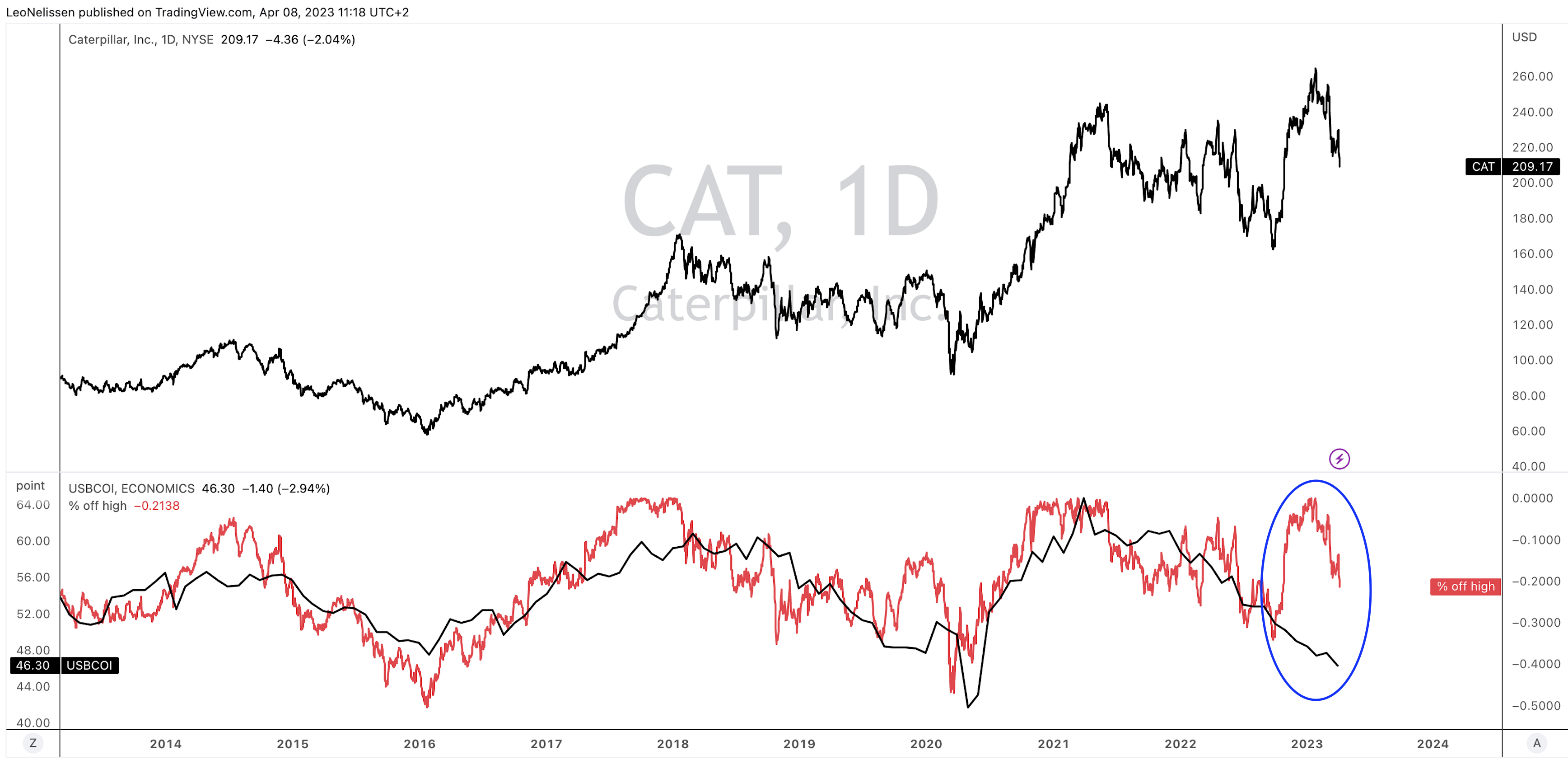

While a recession is obviously not a bullish development, it leads to fantastic buying opportunities. To visualize this, I made the chart below.

- Upper part : the upper part of the chart below displays the Caterpillar stock price.

- Lower part : the lower part displays the ISM index we just discussed (black line) and the total sell-off from Caterpillar's all-time high.

{kind=link}

Note the correlation between CAT's stock price and the ISM index. This makes sense, as the ISM index is forward-looking. Once investors witness weakness, they start to sell cyclical stocks like Caterpillar to incorporate higher demand risks.

Also, note that I highlighted this year's performance. CAT's stock price performance was strong going into this year, ignoring economic weakness. Now, investors are confronted with more weakness and the need to reduce their expectations - regardless of secular growth benefits.

While this could indicate between 10% and 20% more stock price downside, it's great for investors (like myself) who like to buy high-quality stocks at great prices.

High Shareholder Value & Valuation Benefits

Caterpillar has a fantastic Seeking Alpha dividend scorecard. The company scores high in all categories, with outperforming grades in dividend growth and dividend consistency.

{kind=link}

Despite a number of recessions, CAT has hiked its dividend for 29 consecutive years, making it a dividend aristocrat. Its current yield is 2.3%, backed by a conservative payout ratio of 34%. Over the past five years, the average annual dividend hike was 8.7%.

These are the latest hikes:

- June 2022: 8.1%

- June 2021: 7.8%

- July 2019: 19.8%

While we already briefly discussed the low payout ratio, CAT benefits from a number of tailwinds allowing it to grow its dividend.

- The company is on track to generate $7.0 billion in free cash flow this year, followed by an expected surge to $8.2 billion in 2024. This implies a 2023 free cash flow yield of 6.5%. That number could be 7.6% in 2024. This number is boosted by a declining CapEx-to-revenue ratio, thanks to strong post-pandemic sales. This accelerates free cash flow.

- CAT has $28.3 billion in 2023E net debt, which is 2.4x 2023E EBITDA.

The company's balance sheet is A-rated. It allows the company to distribute almost all of its free cash flow to shareholders, as the company reiterated in its Evercore ISI Industrial Conference discussion last month.

Hence, over the past ten years, the company has bought back 21% of its shares, adding to earnings per share growth.

During this period, the company has deleveraged its balance sheet, which means that buybacks and dividend growth were highly sustainable. Given the free cash flow outlook, we can assume that this remains the case - even if a potential recession causes negative outlook adjustments.

That said, the company is trading at 11.8x 2023E EBITDA. This is based on its $108 billion market cap, $28.3 billion in 2023E net debt, and $4.2 billion in pension liabilities.

My base-case scenario is that CAT is about 25% undervalued. This would put CAT at $258. The current consensus estimate is $247.

However, economic challenges could end up reducing the company's outlook. I would not make the case that CAT will reach this target in the months or quarters ahead.

I believe that the stock could fall to $180, which would result in a very attractive risk/reward. If the stock falls to that level, the implied dividend yield would be 2.7%, which would be a great deal.

Takeaway

Caterpillar is in a tricky spot. The company benefits from secular tailwinds like the EV transition, supply chain re-shoring, and the fact that general construction spending is still strong.

However, cracks are starting to appear. Economic conditions are rapidly weakening, causing recession fears to trigger weakness in cyclical stocks.

Although CAT shares are attractively valued, I expect a potential move to $180 per share as investors are de-risking their portfolios.

While it will hurt my CAT position, I'm eager to add more shares during corrections. After all, CAT continues to prove that it is a fantastic dividend growth stock benefiting from a very healthy balance sheet, subdued CapEx (versus sales), and (related) rising long-term free cash flow.

I expect both buybacks and dividend growth to continue and believe that investors will get a chance to buy at (or close to) $180.

Going forward, the next major event is the company's 1Q23 earnings call, which I expect to reveal more about changing demand dynamics. I believe management will confirm my expectations.

For further details see:

Caterpillar: The More It Drops, The More I Buy