CATY - Cathay General Bancorp: It Might Be The Right Time For A First Purchase

2023-08-28 12:38:57 ET

Summary

- NIM has been declining for two consecutive quarters but remains higher than peers.

- The bank's loan growth is slowing down and the LDR is still quite high.

- The bank's exposure to commercial real estate loans is significant but mitigated by low loan-to-value ratios.

Cathay General ( CATY ) is a bank based in Los Angeles with a market cap of $2.50 billion. Like most banks, the Fed Funds Rate rise is putting a strain on the cost of deposits, but the NIM still remains high.

{kind=link}

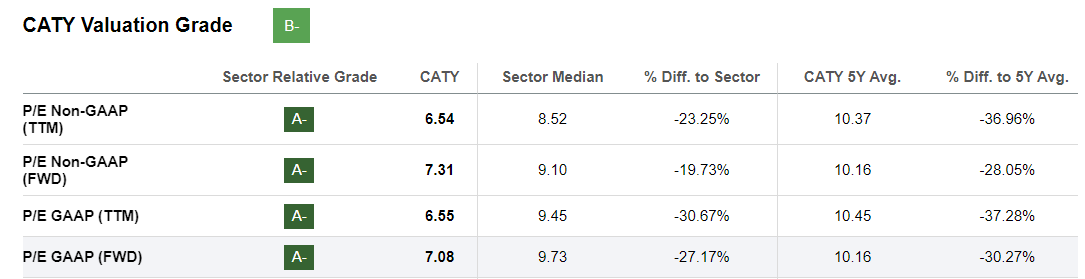

Based on the P/E, Cathay General looks like a bargain, but sometimes that ratio can be misleading, and a deeper analysis is needed to understand whether a company is undervalued or not.

In this article, I will lay out my bullish thesis on this bank, and most of the data I will include are part of the latest quarterly report.

Loans and net interest margin

Businesses and households are no longer as inclined as they were years ago to take on debt since the cost of money has risen sharply, so it is inevitable that the growth rate of originated loans is slowing down.

{kind=link}

Regardless, growth is there, quarter after quarter, but according to CFO Heng Chen's expectations , the second half of the year will see lower growth than the first.

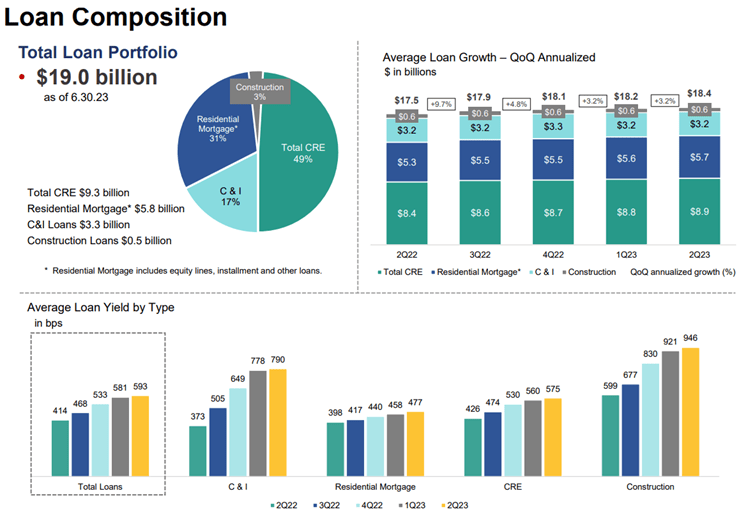

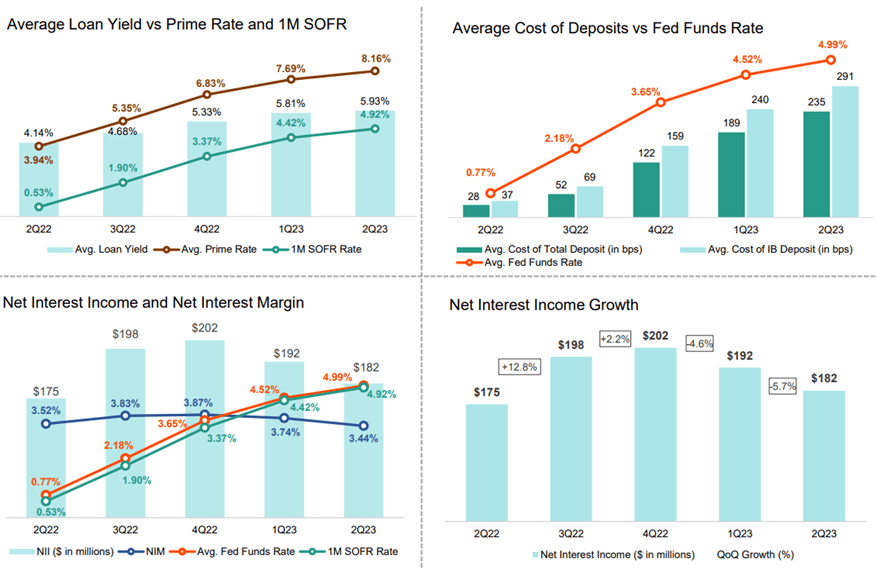

Also growing steadily was the average loan yield, which increased from 414 bps in Q2 2022 to 593 bps in Q2 2023. In particular, strong growth from last year was seen in the Construction and C&I segments, +347 bps and +417 bps respectively. Let us now look at the composition of the loan portfolio.

CRE loans make up 49%, and I would like to focus on this as they are often considered very cyclical and not so resilient in a recession. In other words, the more dependent a bank is on CRE loans, the more challenges it will face in the event of a widespread economic slowdown.

{kind=link}

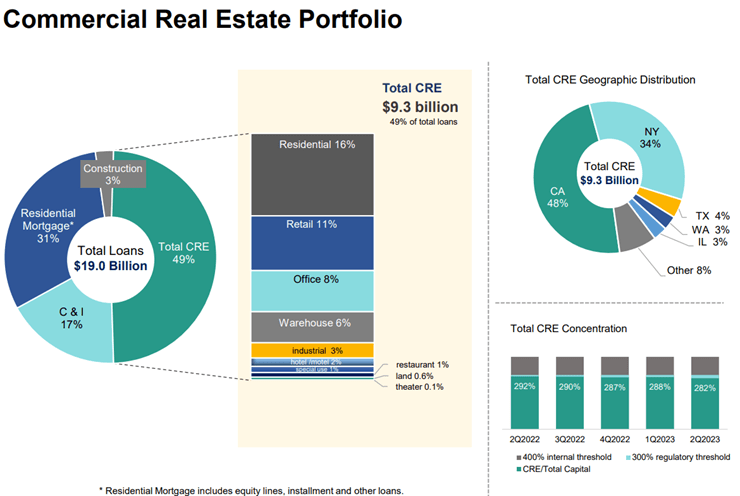

In the case of Cathay General the weight of CRE loans is significant, about half of the loan portfolio, and the CRE concentration is 282%, very close to the 300% threshold bounded by supervisors. Crossing it would not lead to serious repercussions, but new advanced risk management measures will be necessary.

Anyway, I am not too concerned about this exposure to CRE loans as the bank has taken precautionary measures to protect itself from default.

{kind=link}

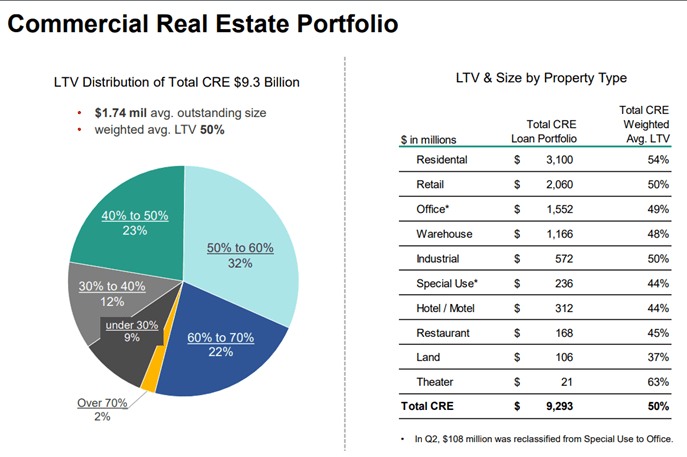

First of all, the average LTV of the entire CRE portfolio is only 50%, in some specific segments much less. For Land, it is only 37%, while Special use and Hotel/Motel is 44%. In addition, the Office segment accounts for 8% of the total loan portfolio and has an average LTV of 49%.

In general, only 2% of CRE loans have an LTV above 70%, while 76% have an LTV below 60%. Finally, this ratio tends to decrease over time since as payments are made the numerator decreases, while the denominator increases as property prices rise.

Cathay General Q2 2023

The second reason I consider the CRE portfolio to be high-quality is that both classified loans ratios and nonperforming asset ratios are very low and improving from the previous quarter. This does not detract from the fact that as quarters go by, borrowers may become insolvent, but it is still a good base from which to start. In any case, even if they were, the low average LTV would allow the bank to limit the damage.

{kind=link}

On the margin side, NIM deteriorated for the second quarter in a row as upward pressure on the cost of deposits outpaced the increase in loan yields. Regardless, the NIM is 3.44%, which is still quite high. The average NIM of banks with assets between $5-49 billion is 3.26% , so Cathay General exceeds this threshold by 18 basis points.

In addition to NIM, NII is also shrinking, and the room for improvement is limited given the rigidity of the financial structure.

Cathay General Q2 2023

The LDR is 98% and this makes the room to originate new loans narrow. Deposits can barely cover loans and this limits operations.

According to Heng Chen's words during the conference call, the bank is trying to raise this ratio to 90% but is not succeeding because it does not want to give up originating new loans at current rates when the opportunity comes. For example, there was strong demand in June and the bank preferred to postpone the reduction of the LDR.

As long as the demand for loans does not collapse I doubt that this ratio can reach its target. On the one hand it is necessary to take advantage of opportunities when they arise, but on the other hand one should not be too greedy. Should deposits decline, it is likely that the 100% threshold will be exceeded, and the bank will have to borrow at high market rates.

Deposits and capital requirements

{kind=link}

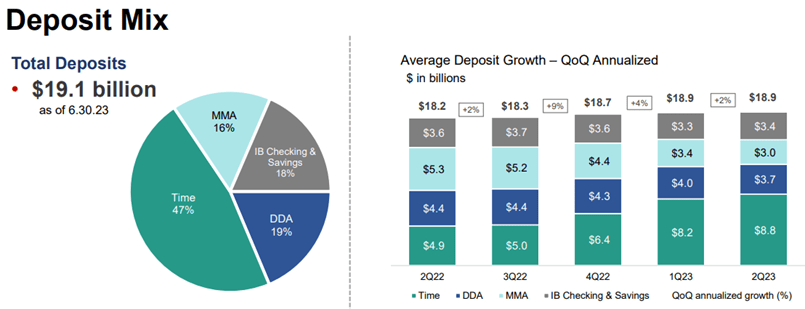

Just as with loans, deposits have been growing slowly and steadily in recent quarters. In any case, compared to last year the composition has totally changed, in fact DDAs have decreased by $700 million while Time Deposits costs have increased by $3.90 billion. As noted earlier, the rapid increase in the cost of deposits resulted in the reduction of NIM and NII for the second quarter in a row.

{kind=link}

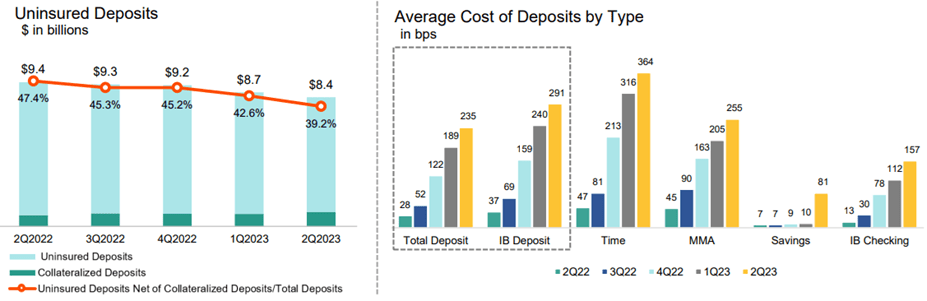

The positive news is that this migration from non-interest bearing deposits to interest-bearing deposits seems to have stopped. This is what CEO Chang Liu expressed:

We are not seeing any additional sort of outflows. I think at this point, given the rate hikes and some of the sensitive clients with the cash and liquidity that had them in checking to money market. They to the extent they wanted to move them into higher yielding accounts, they have already done so at this point. So, we believe that the non-interest bearing core should remain relatively stable.

In other words, those who were planning to get a remuneration on their cash have already transferred their funds, so as of now the situation should have stabilized.

Finally, in terms of capital requirements, Cathay General is well above the minimum threshold.

Cathay General Q2 2023

CET 1 is 12.38% while the Tier 1 leverage capital ratio is more than double the 5% threshold. With such values, a buyback could be considered - not least because the price per share is still far from the all-time high - but the CFO during the conference call emphasized that at least for the time being it is not a priority.

{kind=link}

This is a change in strategy, as in recent years the purchase of treasury stock has been an important resource to remunerate shareholders. Before returning to it, management first wants to better understand the future economic outlook as the soft landing is not entirely a foregone conclusion. Should the economy prove resilient until early 2024 then there could be a new buyback.

Conclusion

{kind=link}

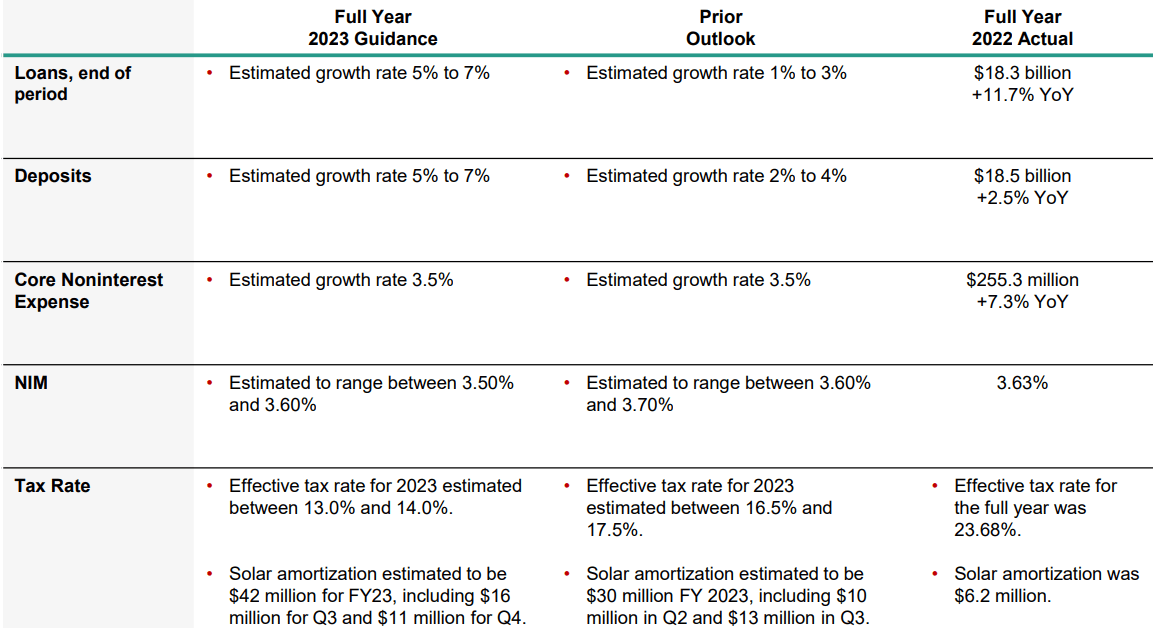

Guidance was revised upward for both deposit growth and loan growth, but NIM is expected to be down from previous estimates, between 3.50-3.60%. The cost of deposits will probably once again grow faster than the yield on loans.

As for valuation, I don't think this bank deserves valuation multiples as low as the current ones. Beyond the low P/E of 6.55x, the P/TBV today is 1.13x while its historical average for the past 10 years is 1.66x. Multiplying the latter figure by the current TBV per share of $30.62, the fair value amounts to $50.82 per share. Thus, based on these figures, Cathay General seems undervalued and not by a small margin.

Moreover, even if it did not prove to be so undervalued, shareholders would benefit in the meantime from a high, growing, and sustainable dividend.

{kind=link}

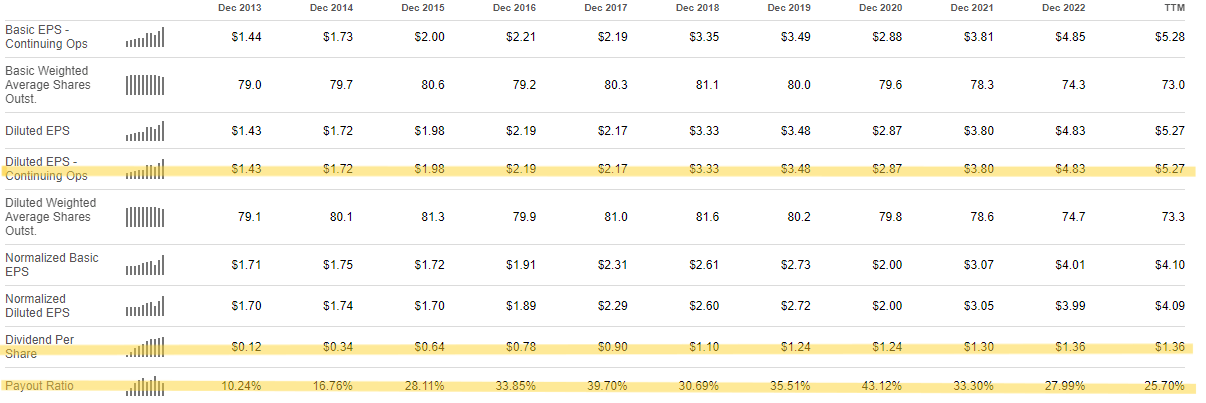

The payout ratio is only 25.70%; the dividend yield is 3.94%; with the exception of 2020, the dividend per share has always increased since 2013; diluted EPS shows an upward trend over the long term. In short, Cathay General has proven to be a good bank in the past and at the right price I think it can prove to be a good investment. I currently rate it as a "buy," but I would like to point out that this investment is by no means risk-free.

{kind=link}

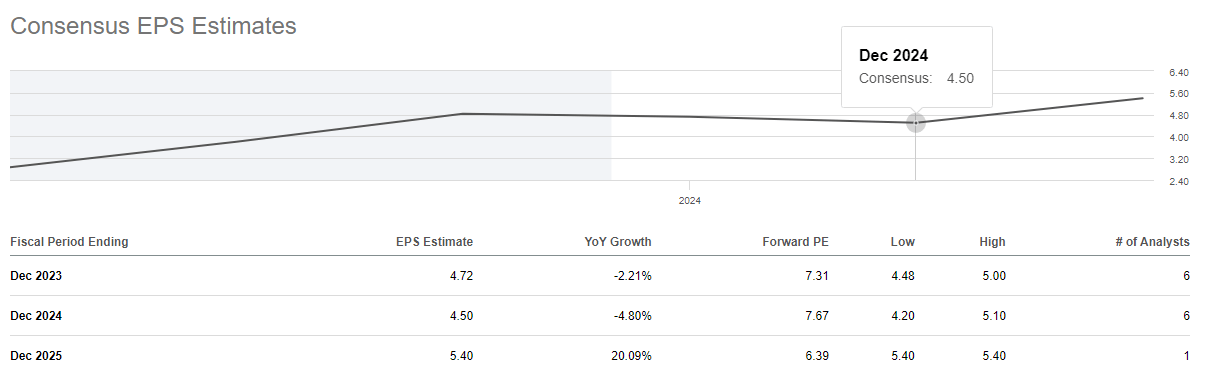

Street estimates predict flat EPS growth through the end of 2024, then return to growth in 2025. The rigidity of the financial structure and the rising cost of deposits could be issues that will continue for a long time to come. I expect high volatility in the short-to-medium term, but I remain confident in the long-term view.

For further details see:

Cathay General Bancorp: It Might Be The Right Time For A First Purchase