CATY - Cathay General: Strong Earnings Growth On The Cards

Summary

- Robust economic activity will keep loan growth at a decent level. However, high interest rates will likely cause a slowdown in loan growth.

- The deposit book is heavy on variable-rate products. Therefore, the margin is only moderately rate-sensitive.

- The December 2022 target price suggests a small upside from the current market price. Further, CATY is offering a decent dividend yield.

Earnings of Cathay General Bancorp ( CATY ) will most probably surge this year on the back of healthy loan growth. Robust economic activity in the company's markets will drive loan growth. Further, interest income will benefit from the rising rate environment. Overall, I'm expecting Cathay General to report earnings of $4.59 per share for 2022, up 21% year-over-year. For 2023, I'm expecting earnings to grow by 13.7% to $5.22 per share. The year-end target price suggests a moderate upside from the current market price. Based on the total expected return, I’m adopting a buy rating on Cathay General Bancorp.

Loan Growth To Revert To The Historical Norm

Cathay General's loan portfolio grew by 8.8% during the first half of 2022, partly driven by the acquisition of HSBC Bank USA's West Coast retail and consumer banking business. Apart from the acquisition, organic loan growth also remained high compared to previous years. The management is projecting loan growth to be between 10% to 12% this year, as mentioned in the second quarter's earnings presentation . This target is reasonable given the acquisition of HSBC’s business during the first quarter of this year.

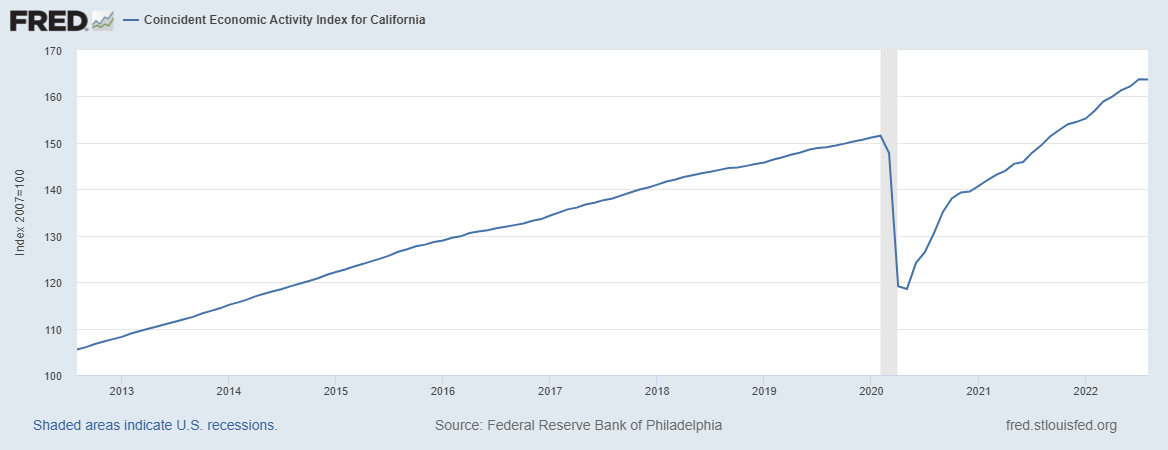

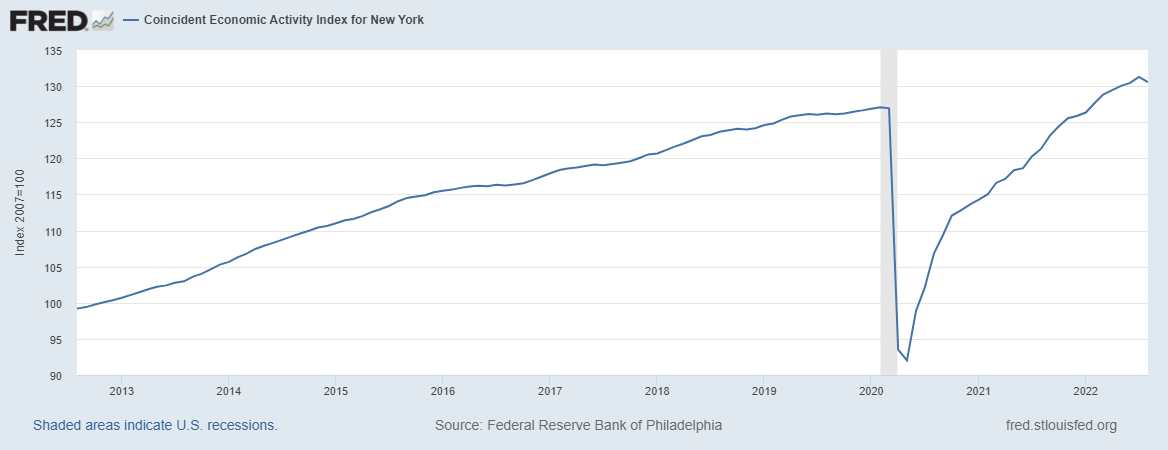

Further, good economic activity in Cathay General’s markets will keep loan growth afloat. The loan book is graphically well diversified, as the bank has a presence in nine states, from California to New York. Further, Cathay General has some presence in Hong Kong, Beijing, Shanghai, and Taipei. As borrowers from California and New York together make up a majority of the loan book, it's best to consider the economic activity of both states to determine credit demand. As shown below, trendlines of the economic activity of both states are currently steeper than they were before the pandemic.

{kind=link}

{kind=link}

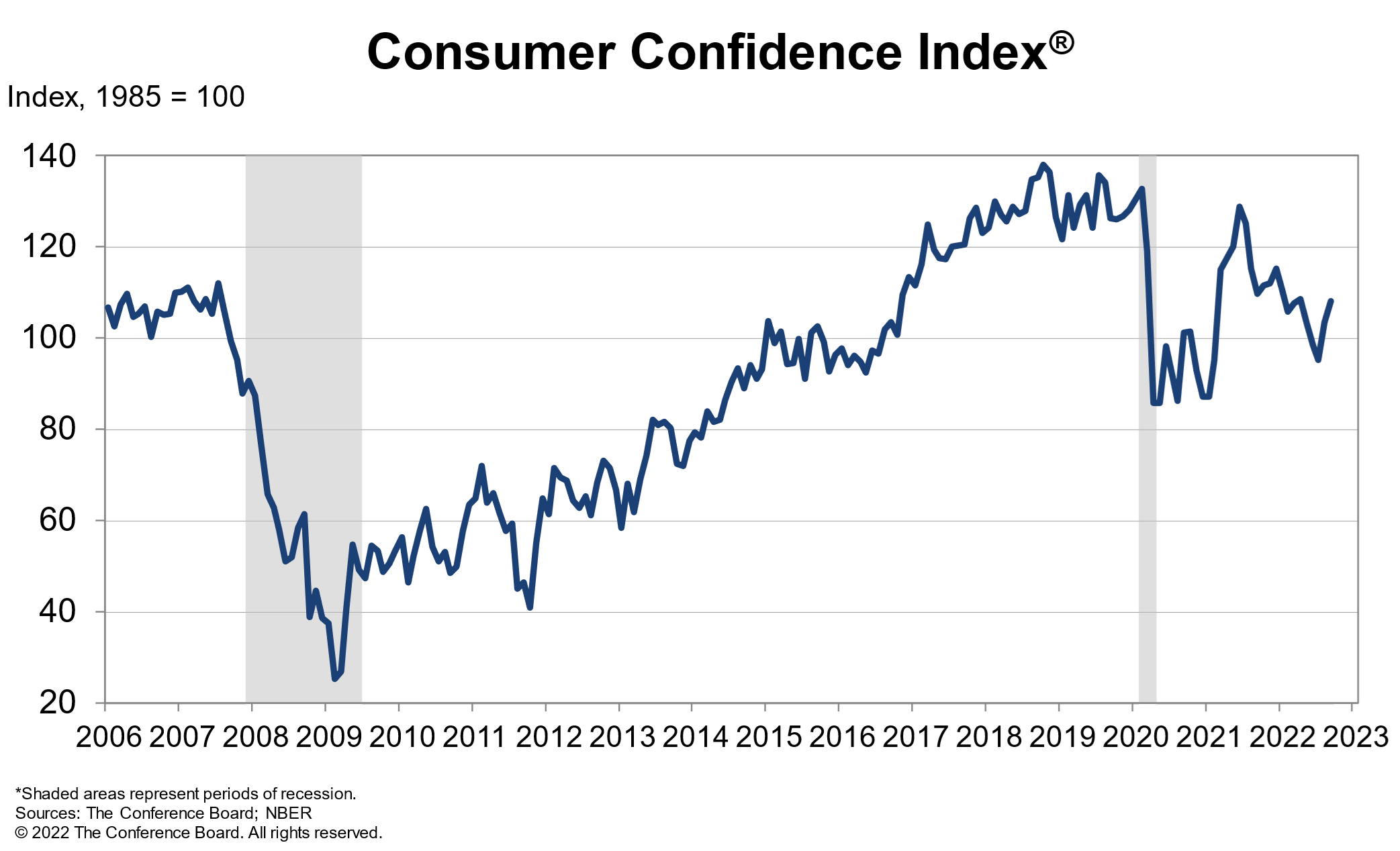

On the other hand, the ongoing interest rate up-cycle will dampen credit demand. Moreover, despite recent improvements, consumer confidence is still low from a historical context. Low consumer confidence is likely to hurt credit demand in upcoming quarters.

{kind=link}

In past years, loan growth has been in the mid-to-high-single-digit range. Considering the factors given above, I'm expecting loan growth to revert to the historic norm. I'm expecting the loan portfolio to grow by 1.25% every quarter till the end of 2023. Meanwhile, I'm expecting other balance sheet items to grow somewhat in line with loans. The following table shows my balance sheet estimates.

| FY18 |

| FY19 |

| FY20 |

| FY21 |

| FY22E |

| FY23E |

| Financial Summary |

| Net interest income |

| 566 |

| 575 |

| 552 |

| 598 |

| 702 |

| 783 |

| Provision for loan losses |

| (5) |

| (7) |

| 58 |

| (16) |

| 21 |

| 20 |

| Non-interest income |

| 32 |

| 45 |

| 43 |

| 55 |

| 61 |

| 54 |

| Non-interest expense |

| 264 |

| 277 |

| 283 |

| 287 |

| 300 |

| 316 |

| Net income - Common Sh. |

| 272 |

| 279 |

| 229 |

| 298 |

| 346 |

| 393 |

| EPS - Diluted ($) |

| 3.33 |

| 3.48 |

| 2.87 |

| 3.80 |

| 4.59 |

| 5.22 |

| Source: SEC Filings, Author's Estimates (In USD million unless otherwise specified) |

Actual earnings may differ materially from estimates because of the risks and uncertainties related to inflation, and consequently the timing and magnitude of interest rate hikes. Further, a stronger or longer-than-anticipated recession can increase the provisioning for expected loan losses beyond my estimates.

Moderately High Total Expected Return Warrants A Buy Rating

Cathay General is offering a dividend yield of 3.2% at the current quarterly dividend rate of $0.34 per share. The earnings and dividend estimates suggest a payout ratio of 26% for 2023, which is below the five-year average of 37%. The below-average payout ratio suggests that there is plenty of room for a dividend hike. Nevertheless, I’m not expecting any change in the dividend level because Cathay General does not often increase its dividends.

I’m using the historical price-to-tangible book (“P/TB”) and price-to-earnings (“P/E”) multiples to value Cathay General. The stock has traded at an average P/TB ratio of 1.51 in the past, as shown below.

| FY18 |

| FY19 |

| FY20 |

| FY21 |

| Average |

| TBVPS - Dec 2022 ($) |

| 28.9 |

| 28.9 |

| 28.9 |

| 28.9 |

| 28.9 |

| Target Price ($) |

| 37.8 |

| 40.7 |

| 43.6 |

| 46.5 |

| 49.4 |

| Market Price ($) |

| 42.6 |

| 42.6 |

| 42.6 |

| 42.6 |

| 42.6 |

| Upside/(Downside) |

| (11.3)% |

| (4.5)% |

| 2.3% |

| 9.1% |

| 15.9% |

| Source: Author's Estimates |

The stock has traded at an average P/E ratio of around 10.7x in the past, as shown below.

| FY18 |

| FY19 |

| FY20 |

| FY21 |

| Average |

| EPS 2022 ($) |

| 4.59 |

| 4.59 |

| 4.59 |

| 4.59 |

| 4.59 |

| Target Price ($) |

| 39.9 |

| 44.5 |

| 49.1 |

| 53.7 |

| 58.3 |

| Market Price ($) |

| 42.6 |

| 42.6 |

| 42.6 |

| 42.6 |

| 42.6 |

| Upside/(Downside) |

| (6.3)% |

| 4.5% |

| 15.3% |

| 26.0% |

| 36.8% |

| Source: Author's Estimates |

Equally weighting the target prices from the two valuation methods gives a combined target price of $46.3 , which implies an 8.8% upside from the current market price. Adding the forward dividend yield gives a total expected return of 11.7%. Hence, I’m adopting a buy rating on Cathay General Bancorp.

For further details see:

Cathay General: Strong Earnings Growth On The Cards