CPCAF - Cathay Pacific: A Stronger Turnaround Potential In Asia

Summary

- Cathay Pacific had recovered only 4% of capacity by H1 2022.

- We expect profitability in H2 2022 on 33% capacity recovered.

- While the Asian market is risky, Cathay Pacific has a lot of capacity to deploy to said market to improve efficiency.

- Even though opportunity exists, investment in Asian airlines is not for the faint-hearted.

In a previous report , I discussed the potential for Singapore Airlines as air travel demand rebounds. What I did conclude is that driven by the potential of softening yields in both the passenger and cargo business, Singapore Airlines is not a preferred airline investment to capitalize on the release of pent-up demand in the market. Obviously, I could be wrong in my assessment, but the risk profile simply does not look appealing to me. In this report, I will look at Cathay Pacific (CPCAY).

Risks And Opportunities For Cathay Pacific

{kind=link}

In some sense, Cathay Pacific is not that different from Singapore. With that I mean is that similar to Singapore, Hong Kong does not have a huge population. So, Cathay Pacific also relies heavily on feeding passengers from Asia into Hong Kong. That means that largely the same set of risks and opportunities we see for Singapore Airlines also apply to Cathay Pacific. So, in Asia the risk is primarily for the Chinese market where relaxation of COVID-19 measures is likely to result in three COVID-19 infection spikes. The first one is happening at this moment with rules relaxed, the second one will happen shortly after the Lunar New Year in January which is typically a strong time for travel demand and then the third spike will come as people head back to work after the holidays. That is something that could ripple through the network of Cathay Pacific, which relies on mainland China.

On top of that comes the usual layer of pressures that include fuel costs and higher interest rates, though inflation is not as much of an issue to Hong Kong.

Top Line Growth Translates To Bottom Line

{kind=link}

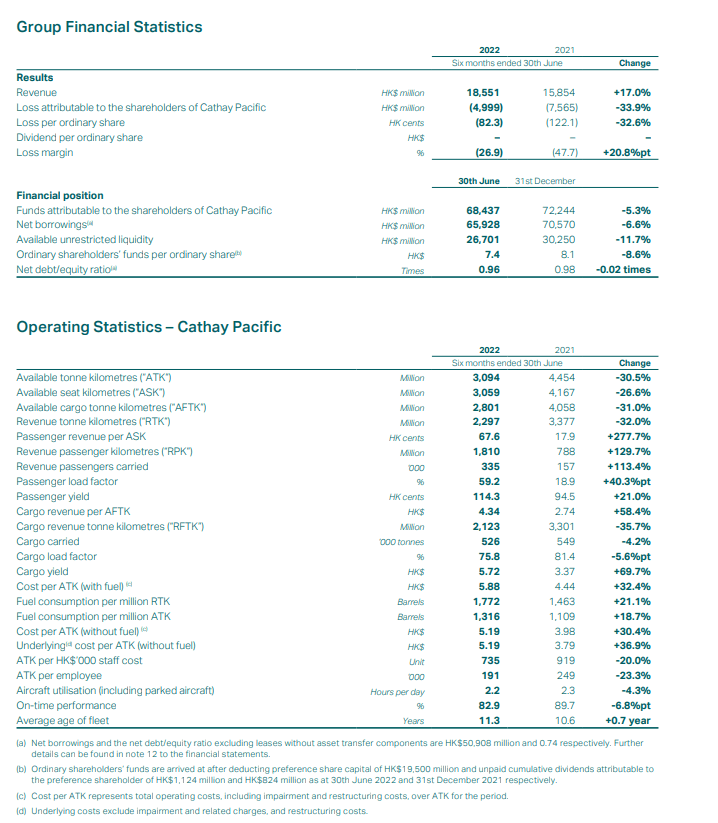

Overall, revenues were up 17% in the first half of the year. Cathay Pacific revenues accounted for 11% of the revenues and were up 177% year-over-year, while Hong Kong Express revenues accounted for less than 1% of the revenues. The cargo segment accounting for 65% of the revenues comes from cargo. On cost structure, it is hard to pick things apart due to the way Cathay Pacific reports, but we are seeing that the topline increase is translating almost one-to-one to the bottom line, which is a positive.

{kind=link}

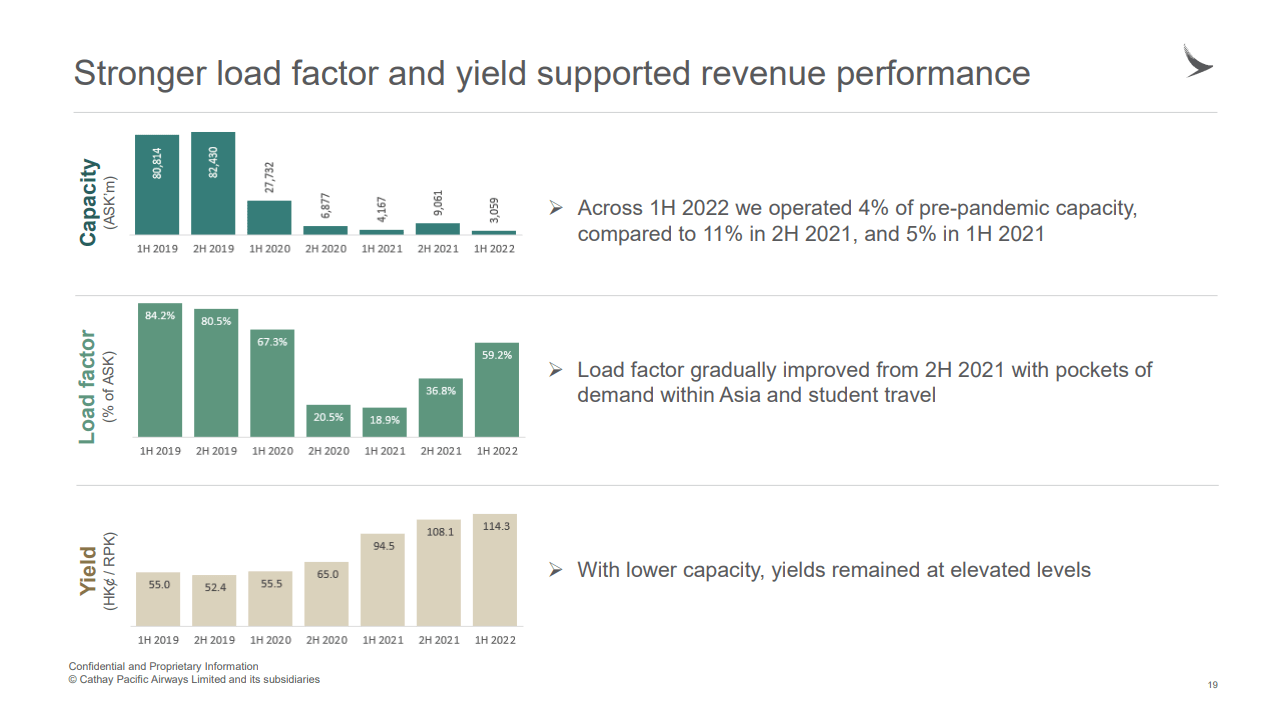

Cathay Pacific revenues are up 177.6% on a 26.6% reduction in capacity. So, for the first half, we see that whereas many operators are expanding capacity, Cathay Pacific did not. This was driven by the tightened restrictions in the first half of the year as compared to last year. On a positive note, we do see that load factors and yields are climbing. So, I would say that having positive revenue growth while operating lower capacity is impressive.

{kind=link}

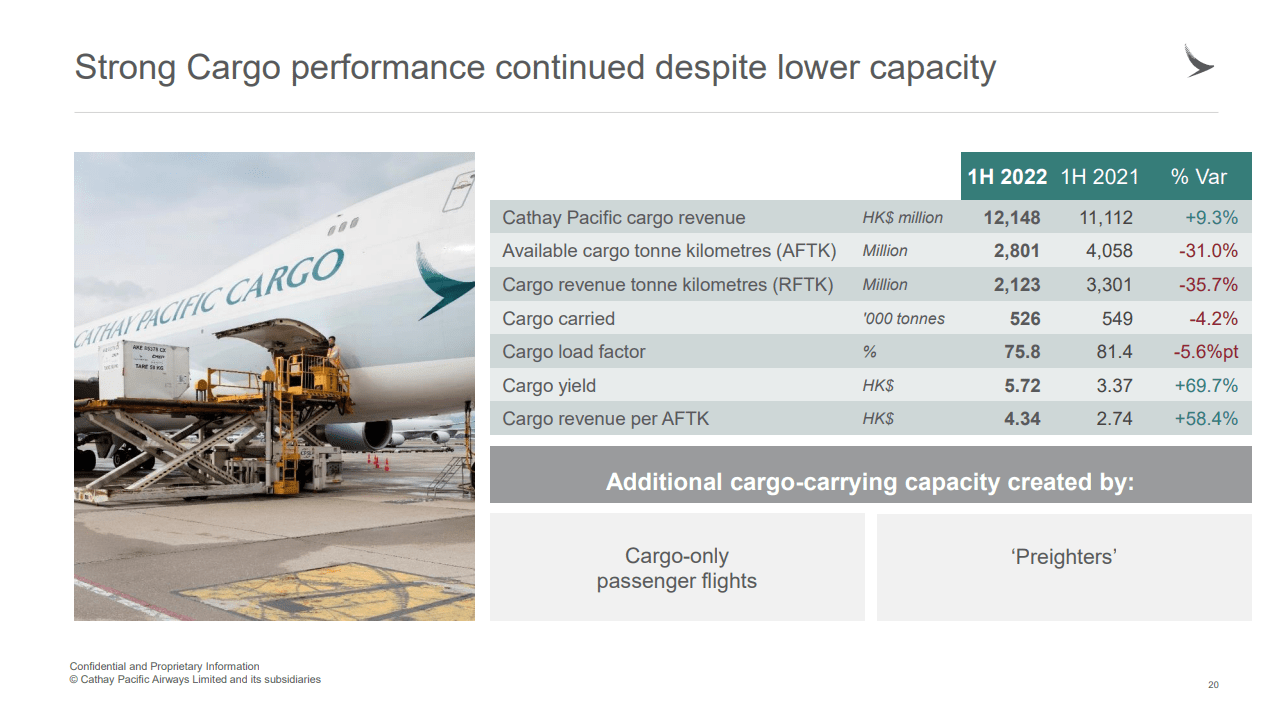

The bulk of the revenue comes from the Cargo segment, which due to COVID-19 restrictions was operating at significantly lower capacity year-over-year as well. Nevertheless, the cargo segment showed strong growth on strong off-peak load factors and yields at fresh highs.

Overall, I would say that results were impressive given the airline operated at just 4% of pre-pandemic capacity and only 32% of the pre-pandemic cargo capacity due to tight restrictions in the first half of the year.

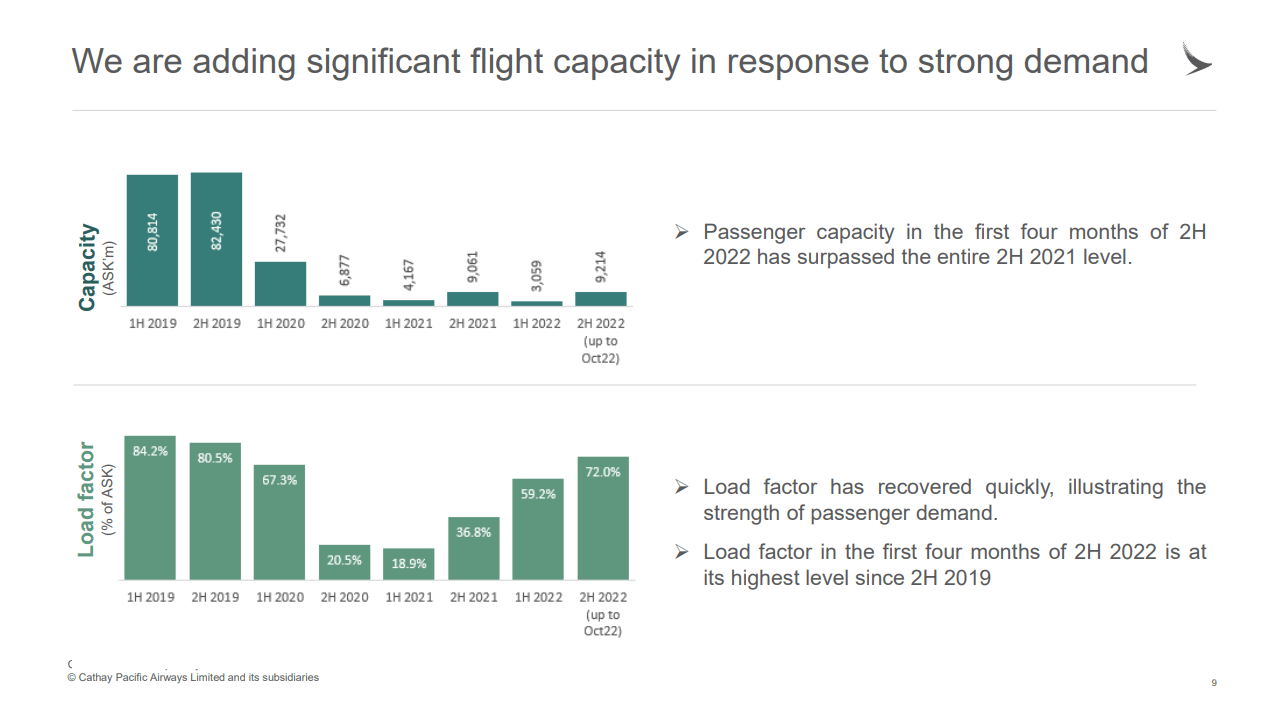

What I like most about Cathay Pacific is the fact that with restrictions easing, they can significantly reduce unit costs. Currently, the daily utilization of their fleet is just 2 hours per day, which goes to show how heavily underutilized the assets are. Cathay Pacific only reports its financials twice a year, so we don't have detailed third quarter results, but we do have details from the analyst briefing which includes capacity and load factor information up to October and those results are promising.

{kind=link}

Passenger capacity is up 20% while load factors have further improved as compared to the first half of the year, indicating that Cathay Pacific is performing much better in H2 2022. The same cannot be said about the cargo business, but depending on how you look at it, this could have been expected. The past two years were really exceptional times for cargo transport, and we are now seeing some normalization in that. The reduction of 20% in cargo revenues shows the strength of the past two years, while much of 2022 was subdued by tight restrictions. While the rates are softening, we could see Cathay Pacific making bigger inroads in the cargo space again. So, Cathay Pacific as a whole is seeing improvements in passenger capacity, but its cargo capacity is down, and maybe that is not a bad thing. Yields are softening, so it might be wise to opt for prudent capacity deployment, trying to balance the market.

Conclusion: A Long Recovery Runway For Cathay Airways And Its Stock

Cathay Pacific has a long recovery runway ahead, and that is both a good and a bad thing. The good thing is that whatever results they show now, it is just the start of things. By October, 21% of the passenger capacity had been recovered and by year-end this should be 33% while 63% of the cargo capacity is recovered. When Singapore Airlines pointed at yields softening due to capacity additions from competitors, they were without doubt talking about Cathay Pacific. The airline is set to improve capacity to 33% by year-end, 70% in 2023 and fully recovered by 2024.

Obviously there is the risk of demand falling due to new spikes in infections, but Cathay Pacific despite recent industrial actions announced does have a lot of recovery runway ahead that will increase asset utilization and push down unit costs and because that recovery runway ahead is so long, I do expect that the capacity that Cathay Pacific can bring to the market will overpower any weakening it will see in yields and the first expected step is profitability in the second half of the year, which would be an accomplishment given that it has another 66% in capacity to recover beyond that point.

For further details see:

Cathay Pacific: A Stronger Turnaround Potential In Asia