JILL - Cato Corporation: Still Attractive Despite A Worsening Of Fundamentals

2023-07-28 14:48:39 ET

Summary

- The Cato Corporation, a fashion retailer, has seen its shares fall in recent months due to inflationary pressures and a decrease in revenue, profits and cash flows.

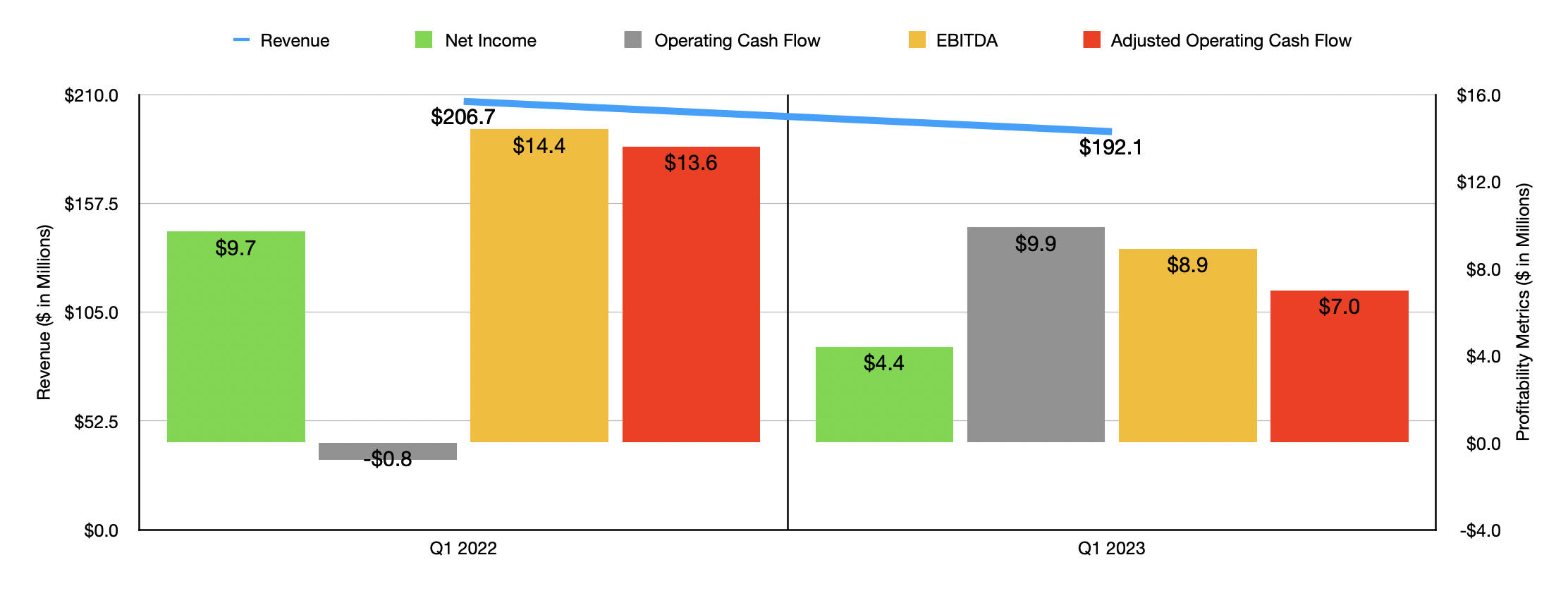

- The company's revenue dropped 7.1% to $192.1 million in the first quarter of fiscal year 2023, with net income more than halving from $9.7 million to $4.4 million, largely due to a decrease in store count.

- Despite these challenges, the company's strong balance sheet, with no debt and $131.2 million in cash and cash equivalents, makes it an appealing prospect.

Truth be told, I believe that one of the most misunderstood companies on the market today is none other than retailer The Cato Corporation ( CATO ). For those who may not know, the company operates as a fashion retailer that sells a wide variety of apparel, accessories, and so much more. On top of selling products offered up by other firms, it also has its own private brands that it sells. Over the past several months, shares of the business have taken a beating even at a time when the broader market has improved. Inflationary pressures have not done the business a favor. On top of seeing revenue pull back, profits and cash flows have also been slammed. But when you look at the strength of the company's balance sheet, it's difficult to understand how the market could price the company the way it is today.

A lot of pain

Back near the tail end of January, I wrote an article that took a bullish stance on Cato. Up to that point, the company had been facing pressure on its top and bottom lines, with sales, profits, and cash flows, all pushed lower. In general, I am not a fan of retail because it is highly competitive. Margins tend to be low and even one or two bad years can spell disaster for a brand. So when you look at a business that is experiencing pain that fits in this undesirable market, you might think that I would be very bearish about the company in question. But because of how cheap the stock was and how strong its balance sheet was, I had no choice but to rate it a ‘buy’ to reflect my view at the time that shares should outperform the broader market for the foreseeable future. Unfortunately, that call has so far proven to be rather bad. While the S&P 500 is up 16% since the publication of said article, shares of Cato have plunged 14.3%.

{kind=link}

Author - SEC EDGAR Data

I'm not going to say that some pessimism was not warranted. To some degree, it was. Consider the financial performance that management revealed for the first quarter of fiscal year 2023. During that time, revenue came in at $192.1 million. That's 7.1% lower than the $206.7 million the company reported one year earlier. Some of this pain was undoubtedly driven by weak comparable store sales. After all, management has stated that inflationary pressures and difficult economic conditions have harmed its business. But the bigger driver of the downside for the company was almost certainly the decrease in store count. At the end of the most recent quarter, the company operated 1,264 stores. This was down from the 1,315 locations that it operated at the end of the same quarter last year. On top of this, management has been very clear about what the future holds. The current expectation is for the company to close somewhere around 80 stores throughout the 2023 fiscal year in its entirety. During the first quarter alone, it closed 20 stores, though it also opened four new ones.

The decline in revenue brought with it a decline in profits as well. Net income was cut by more than half from $9.7 million to $4.4 million. This is not a surprise given that even a small drop in revenue in the retail space can have a large impact on the bottom line. Other profitability metrics largely followed suit. The one exception was operating cash flow. It went from negative $0.8 million to $9.9 million. But if we adjust for changes in working capital, it was cut by almost half from $13.6 million to $7 million. Meanwhile, EBITDA for the firm dropped from $14.4 million to $8.9 million.

{kind=link}

Author - SEC EDGAR Data

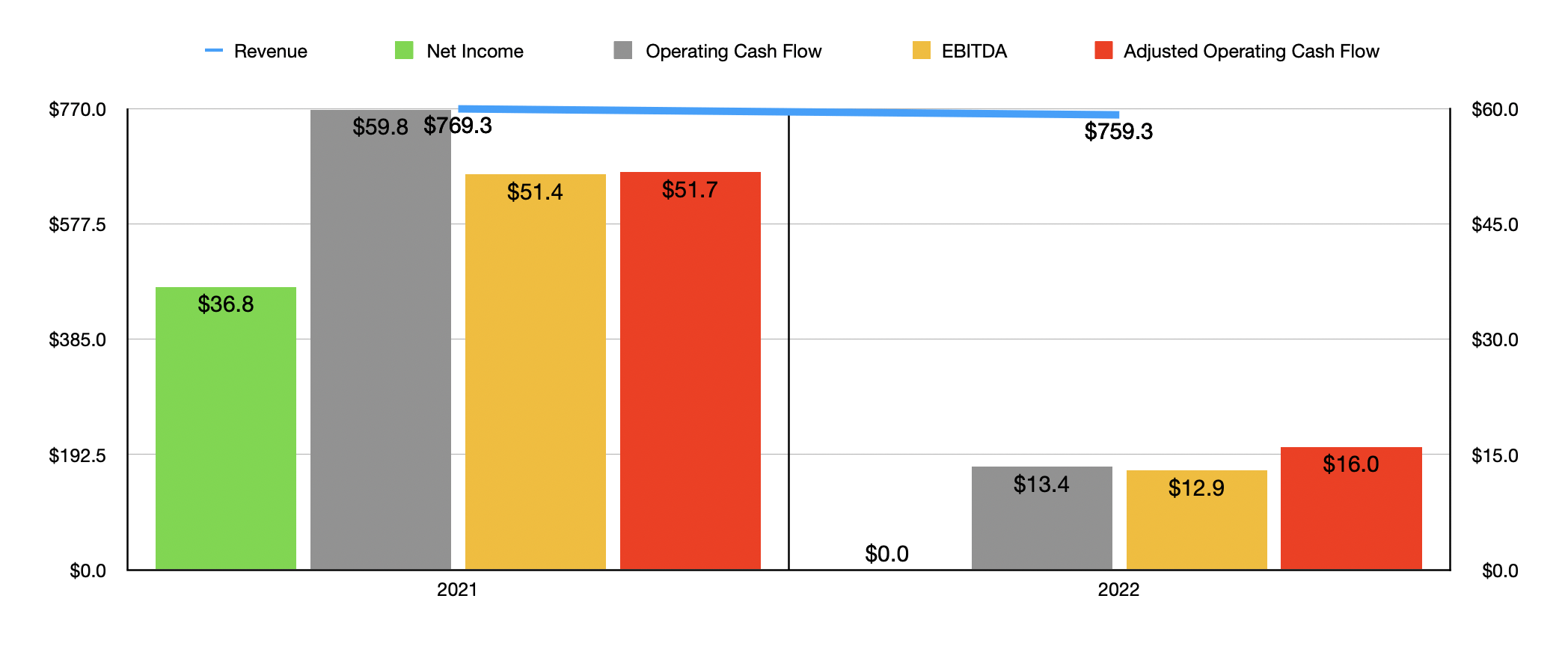

The results experienced in the first quarter of the 2023 fiscal year compared to the same time last year were not a one-time thing. As you can see in the chart above, financial performance for the business worsened from 2021 to 2022 . This was true not only from a revenue perspective, but also from a profit and cash flow perspective. Given these facts, you might think I am peculiar for liking the company. However, the reason I do like it is because of what I have described previously as its fortress balance sheet. The firm has no debt on its books. On top of this, it boasts $131.2 million in cash and cash equivalents. By comparison, its market capitalization is only $158.6 million as of this writing. That brings the enterprise value down to only $27.3 million. That is exceptionally small and requires very little in the way of profitability in order to be attractive.

{kind=link}

Author - SEC EDGAR Data

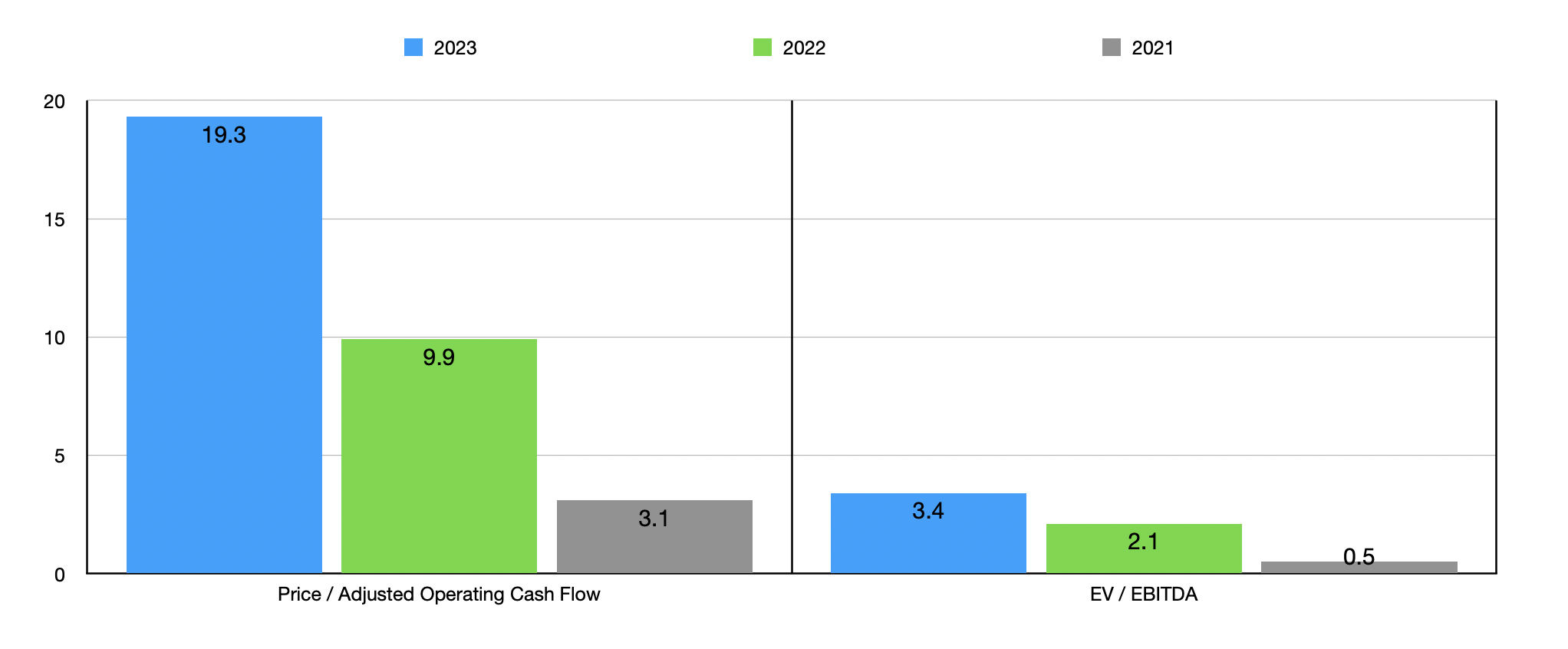

Do you see what I mean, let's annualize results experienced so far for 2023. In this case, adjusted operating cash flow would be $8.2 million, while EBITDA would come in at only $8 million. In the chart above, you can see how the company is priced using this data, as well as using results from both 2021 and 2022. In pretty much every instance, the stock looks attractively priced. The one exception would be the price to operating cash flow multiple for 2023. But again, we really should be focusing more on the enterprise value than the market capitalization in this case. And even with bottom line results deteriorating significantly, shares look very attractive on an absolute basis here.

As I have done with other companies in the past, I also compared Cato to five similar firms. In the table below, you can see the companies priced on a price to operating cash flow basis and on an EV to EBITDA basis. In the price to operating cash flow scenario, three of the five businesses ended up being cheaper than our prospect. Using the EV to EBITDA approach, meanwhile, only two of the firms were cheaper than it.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| The Cato Corporation |

| 9.9 |

| 2.1 |

| Tilly's ( TLYS ) |

| 48.2 |

| 21.9 |

| Citi Trends ( CTRN ) |

| 13.3 |

| 1.5 |

| J. Jill ( JILL ) |

| 4.0 |

| 3.8 |

| Express ( EXPR ) |

| 7.7 |

| 0.6 |

| Destination XL Group ( DXLG ) |

| 5.8 |

| 3.9 |

Takeaway

Operationally speaking, Cato has been experiencing some pain. In the near term, I suspect that pain will continue. Having said that, the company has a tremendous amount of flexibility and safety because of its balance sheet. The stock looks very affordable on an absolute basis and is probably more or less fairly valued compared to similar firms. Given all of these facts, I have no problem keeping the company rated a ‘buy’ even in light of recent share price weakness.

For further details see:

Cato Corporation: Still Attractive Despite A Worsening Of Fundamentals