CATO - Cato: Declining Sales And Widening Losses Could Impact Dividend Payout

2023-12-26 10:27:44 ET

Summary

- CATO Corporation has been experiencing a significant decline in sales and profit over the past nine months.

- The company's dividend payout has decreased and is not expected to increase in the near future.

- CATO reported weak third-quarter results, with declining revenues and net profit margin, and is struggling to keep up with changing fashion trends.

Investment Thesis

The Cato Corporation ( CATO ) is an American specialty retailer headquartered in Charlotte, North Carolina. In this thesis, I will analyze its third-quarter results along with its future growth prospects. I will also be analyzing its dividend payout and yield at its upside potential. I believe it has been experiencing a significant decline in sales and profit over the past nine months, and the situation is not expected to improve in the near future; hence, I assign a Sell rating for CATO.

Company Overview

CATO is an American Fashion retail company that operates under the Cato, It's Fashion and Versona brands. The flagship brand, Cato, focuses on providing a wide range of women's apparel, including dresses, suits, separates, accessories, and footwear. It's Fashion is another brand under The Cato Corporation, targeting a broader demographic with a diverse selection of trendy and affordable clothing. Versona, a more recent addition to the company's portfolio, is positioned as a specialty retailer offering accessories, jewelry, and gifts to complement various fashion styles. It operates a network of retail stores across the United States, strategically located in shopping centers and malls.

9.55% Dividend Yield

{kind=link}

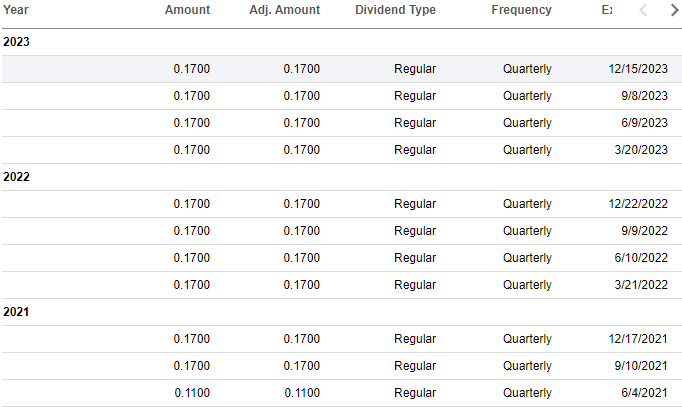

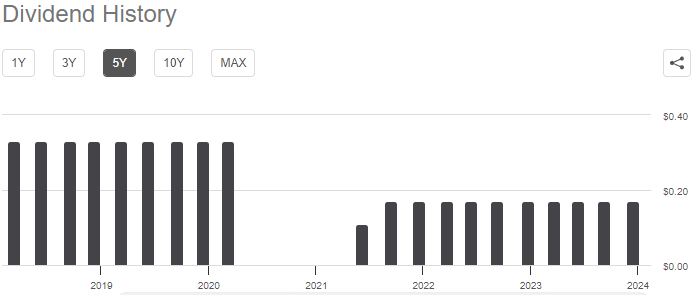

As of November 17, it declared a quarterly dividend of $0.17 , bringing the forward annualized dividend payout to $0.68, reflecting a dividend yield of 9.55% at the current share price of $7.12. As we can see in the chart above, the company increased its quarterly dividend payout from $0.11 in Q2 of FY21 to $0.17, and the payout has been $0.17 since then. But this doesn't reflect the complete picture. When we look at the chart below, we realize that the company has not been consistent with the dividend payout.

{kind=link}

The quarterly dividend payout before the COVID-19 pandemic was $0.33, then the dividend payout stopped for the next four quarters, and when it resumed, it was half the dividend payout of pre-Covid levels. Presently, the dividend payout is half of what it was before COVID-19. The primary reason behind this decline is the worsening financial performance of the company and the continued losses that it has been reporting. Given the current trend in its revenue and income growth, I think the dividend payout doesn't seem to be going up anytime soon; if anything, it could deteriorate even further. The 9.55% dividend yield might seem attractive, but I would like to highlight that the increased dividend yield is a result of a steep decline in its share price. I do not think the current quarterly dividend payout is sustainable, given the increased losses reported by the company, and I would not recommend investors looking for a stable income to invest in CATO.

Q3 FY2023 Result

CATO reported weak third-quarter results, missing the market revenue and EPS estimates by significant margins. The company experienced a decline in revenues and net profit margin. The management provided the clarification that a fall in customers' discretionary spending levels is majorly impacting sales, but I think the problem is much deeper. The company is not able to keep up with the fast-changing fashion trends, and its online platform is not very efficient either, both in terms of interface and usability, which I think is the main reason behind the sales taking a hit.

It reported total sales of $156.7 million , a significant decline of 10% compared to $175 million in the same quarter last year. As I mentioned earlier, it has not been able to adapt itself to the changing consumer preference, and that, coupled with economic headwinds, is primarily impacting its performance. The operating loss for the quarter stood at $10.3 million, reflecting an operating loss margin of 6.6%. The operating loss margins also deteriorated from 5.2% to 6.6%. As per my analysis, the company managed to control its direct and operating costs and saw a reduction in expenses, but the low revenue more than offset the cost-cutting measures. It managed to reduce its operating losses primarily by reducing the headcount. The diluted net loss per share was reported at $0.30, compared to $0.21 in the same quarter last year.

Now, let us have a look at its balance sheet. As of October 28, 2023, it reported cash and cash equivalents of $28.8 million and a total lease liability of $122.5 million. The company has significant lease liability as the majority of the stores that it operates are leased and not owned. High lease liability can severely impact its performance, especially in the current situation with a global economic slowdown and a possibility of recession in the US market. Even in the past, the company greatly struggled during the Covid-19 pandemic, which affected its growth and impacted the dividend payout. The company has not been able to recover since 2020, and another slowdown in the market coupled with $122.5 million in lease liability doesn't paint a positive picture.

Overall, the company managed to limit its expenses, but the margins still took a hit due to declining sales. This is reflected in the fall in the company's operating physical stores; in Q3 FY23, they reported total operating stores at 1245, compared to 1317 stores in Q3 FY22. The management stated that it expects to close 110 stores in 2023, of which they have already closed 44. The fall in physical sales could be justified if the online sales pick up, but that doesn't seem to be the case. The shutting down of stores is majorly due to weak demand and takes away any possibility of recovery in the coming quarters. The management has not provided any guidance for FY23.

Competitive Analysis

CATO is currently trading at a share price of $7.12, a YTD decline of 25.76%. It has a market cap of $138.4 million. The company is expected to end FY23 at an estimated loss per share of $0.37. When we compare it to its peers like Torrid Holdings Inc. ( CURV ) and Chico's FAS, Inc. ( CHS ) who have a P/E multiple of 45x and 10.66x, we realize that CATO doesn't have any upside potential in the stock price with profitability being elusive. I believe there are better investment opportunities in the market, and investors should wait for an improvement in the sales and profit margins of CATO before investing in the company.

Conclusion

The consistent fall in the company's sales and profit margins is a big cause for concern. The declining number of physical stores doesn't instill much confidence either. The company is expected to continue to face economic headwinds, and there are no significant signs of recovery. The deteriorating financial performance could also affect the dividend payout, and I believe the current dividend payout is not sustainable. Considering all these factors, I assign a Sell rating for CATO.

For further details see:

Cato: Declining Sales And Widening Losses Could Impact Dividend Payout