CATO - Cato: Long-Term Outlook Looks Fine Despite Current Headwinds

Summary

- Cato's share price has declined by ~77% from all-time highs reached in 2015.

- The company has not yet managed to break the negative sales trend.

- Profit margins are (temporarily) depressed.

- However, the long-term outlook paints a very different picture.

- This represents an opportunity to acquire shares of the company as it has enough resources to endure the current macroeconomic headwinds.

Investment thesis

The Cato Corporation (CATO) has tested the patience of investors since 2016 and the mandatory closures that took place in 2020 in order to contain the spread of the coronavirus dealt a very significant blow to the company's already weakened operations. Despite the fact that in 2021 both sales and margins improved substantially, now the company faces a very significant drop in profit margins as a result of current inflationary pressures and increased freight and labor costs, and to this, we must add the risk of a recession as a consequence of the increase in interest rates.

Still, the company has a very strong, debt-free balance sheet, with enough cash from operations and inventories to withstand current inflationary headwinds and a potential recession, which makes me believe that now is a good time to buy shares ~77% below all-time highs reached in 2015.

A brief overview of the company

The Cato Corporation is a specialty store operator that sells fashion apparel and accessories under the stores named Cato, Cato Fashion, Cato Plus, It's Fashion, It's Fashion Metro, and Versona. The company was founded in 1946 and its market cap currently stands at ~$200 million, operating over 1,300 fashion retail stores in 32 states, as well as e-commerce channels. 18.71% of shares outstanding are owned by insiders, which means that the management is the main beneficiary of the good performance of the share price and the operations of the company.

Cato Corporation (Catofashions.com)

{kind=link}

In its retail stores, the company sells a wide range of products, including tops, sweaters, denim, pants, cropped pants, dresses, jackets, vests, sets, suits, skirts, shorts, athleisure, sleep clothes, intimates, necklaces, bracelets, earrings, rings, handbags, scarves, socks, tights, ponchos, wraps, hats, belts, sunglasses, and footwear. The company's products are generally in the low-cost range, but it maintains a good quality both in the design and in the materials used for their manufacturing.

Over the past few years, the total number of locations has remained more or less stable, which has worried investors because said stability has been accompanied by a drop in sales of 23.92% since 2015, and this suggests that the attractiveness of its stores may not have adapted in time to changes in consumer preferences. Here, it is important to emphasize that the number of stores operated by the company actually decreased by 4.45% from 2015 to 2021 and that margins improved since 2018, with which the company seems to have managed to get rid of stores that were not providing enough profitability.

| Year |

| 2013 |

| 2014 |

| 2015 |

| 2016 |

| 2017 |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| Number of stores |

| 1,320 |

| 1,346 |

| 1,372 |

| 1,371 |

| 1,351 |

| 1,311 |

| 1,281 |

| 1,330 |

| 1,311 |

In this sense, the share price has not stopped decreasing since 2015 and is currently at levels close to those of the worst moments of the Coronavirus pandemic in 2020.

Currently, shares are trading at $10.22, which represents a 77.09% decline from all-time highs of $44.61 in 2015. Without a doubt, this is a very steep drop, so it will be necessary to carefully evaluate the current status of the company before considering its share price as a good long-term opportunity as investors' optimism is very negative at the moment, and it's not in vain.

Revenues keep declining, but the long-term outlook looks different

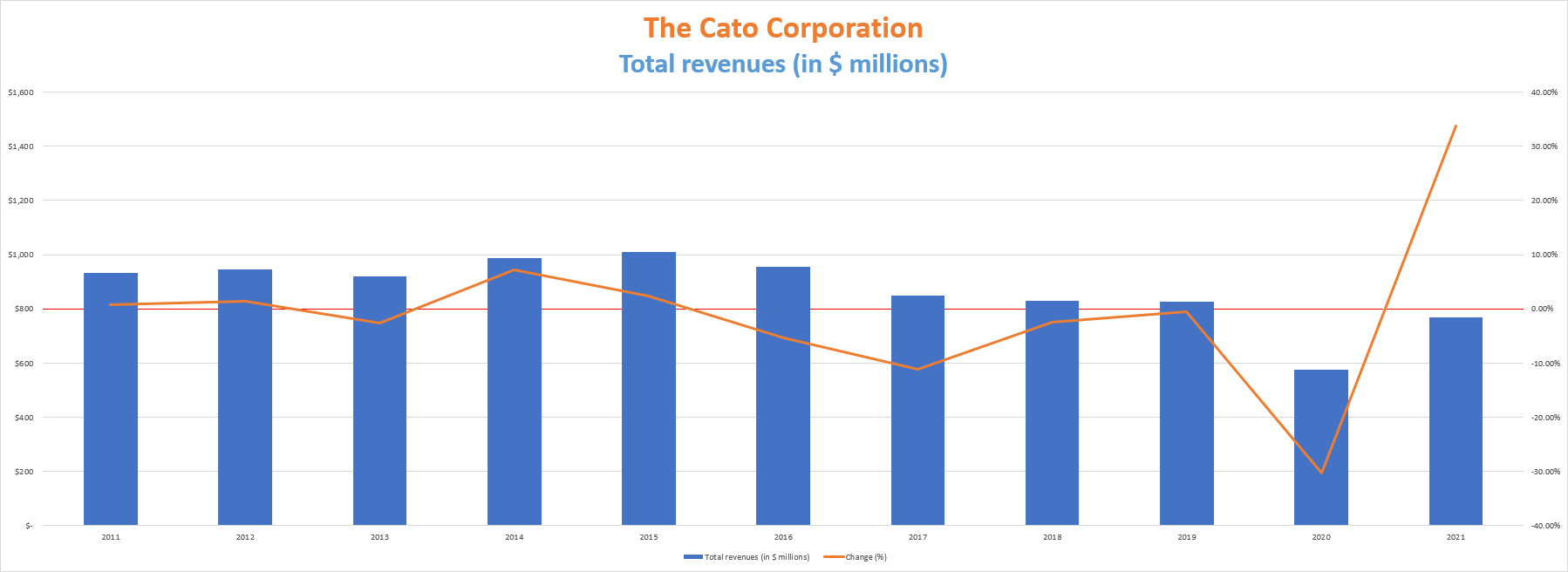

Until 2015, the company managed to increase its sales to the $1 billion mark, but since then said sales have not stopped falling. Although it is true that 2021 delivered a sizable increase compared to 2020 as a result of the lifting of restrictions due to the coronavirus pandemic crisis, they still represent a 6.79% decline compared to 2019. In this sense, net sales reached $769 million for the fiscal year that ended on January 29, 2022, which represents a 33.76% increase compared to the prior year, but the last few quarters have shown a slight worsening.

The Cato Corporation total revenues (10-K filings)

{kind=link}

For the current fiscal year, revenues declined by 2.98% year over year during the first quarter, by 5.32% during the second quarter, but increased by 2.59% during the third quarter. In this regard, trailing twelve-month revenues currently stands at $748.5 million, which represents a 9.31% decline compared to 2019, before the coronavirus pandemic crisis. It is therefore that we can conclude that the negative trend continues to be effective as of today.

The share price decline linked to the continuous drop in sales since 2015 has caused a sharp fall in the P/S ratio, which currently stands at 0.273.

This means the company generates $3.66 in revenues for each dollar held in shares by investors, annually. This ratio is 57.94% lower than the average of 0.649 during the past decade and a 78.72% decline from the decade highs of 1.283, which shows a high level of pessimism on the part of investors as they are willing to pay much less for the company's sales compared to the past. In this regard, it is not only declining sales that are increasing pessimism in the markets, but also a drop in profit margins that has seriously affected the company's profitability since the start of the pandemic.

Margins are (temporarily) depressed

Since 2018, the company managed to slowly increase its profit margins after a significant drop in 2017, with which it seemed that the strategy of closing stores was having a positive effect on the profitability of the company. But despite this, the positive trend was broken in 2020 due to the coronavirus pandemic crisis and the mandatory restrictions derived from it, and after a substantial improvement in 2021, things started to look ugly again in 2022 due to a series of headwinds the company is currently enduring.

In this sense, the trailing twelve months' gross profit margin currently stands at 34.25%, and the EBITDA margin at 1.11%. But if we look at the past quarter, the gross profit margin was 29.94% and the EBITDA margin was -4.83%, which paints a much worse picture in the short term. This has been caused by a rise in the cost of goods sold to 70.7% of total retail sales, compared to 61.1% during the same quarter of 2021 and 62.6% during the same quarter of 2019, before the coronavirus pandemic crisis.

This drop in profit margins has caused a drop in the cash generated through operations despite a strong recovery in 2021 as inflationary pressures, as well as increased labor and freight costs, continue to impact the company's operations.

In this regard, trailing twelve months' cash from operations currently stands at -$0.32 million, and the company reported cash from operations of just $2.3 million during the third quarter despite an increase of $3.6 million quarter over quarter in accounts payable while accounts receivable increased by only $0.9 million and inventories increased by just $0.1 million.

At this point, it is important to note that it often takes quite a while to pass on such a large increase in costs directly to consumers as the company still has to take pricing actions in order to stabilize profit margins and get back to business. generate positive cash from operations. Nevertheless, inflation still has to stabilize before expecting the pricing actions to have a lasting effect over time.

However, the company was generating, before the coronavirus pandemic headwind, much more cash than enough to cover current capital expenditures of ~$16 million, which suggests, in my opinion, that the business model is actually viable in the long term despite the current headwinds which seem temporary as they are directly linked to the current macroeconomic context. For this reason, it is important to assess all of the resources that the company currently has to overcome current inflationary pressures until they are a problem of the past.

A debt-free balance sheet provides a safety net to overcome current inflationary headwinds

One of the most positive aspects of the company is that the long-term risk is, in my opinion, quite low thanks to a debt-free balance sheet. In this sense, the company currently holds cash and equivalents of $17.28 million while its inventories are worth $116.72 million.

This gives the company plenty of leeways to navigate the current macroeconomic headwinds for a very long time since its annual capital expenditures are only ~$16 million while there are no interest expenses as no debt exists on its balance sheet. Furthermore, if we look at the evolution of revenues since 1990, we can see that the company has actually managed to increase its business size over the years despite the current difficult situation, with which the potential return for investors if its resources are enough to overcome the current inflationary crisis, as well as the potential upcoming recession as a consequence of rising rates by the central banks in order to reduce the high levels of inflation, is high.

But for this to be possible, the management could (and maybe should) temporarily reduce or even completely cancel the dividend in order to preserve cash until the current macroeconomic outlook allows the company to return to the sales growth path that was taking place prior to 2015 and to the path of improving profitability as it had been experiencing in the years before the coronavirus crisis in 2020. This is, in my opinion, one of the main risks that investors must face in the short to medium term in exchange for the current deep discount in the share price.

There is a short-term risk of a dividend cut, but the long-term dividend yield on cost is more than reasonable

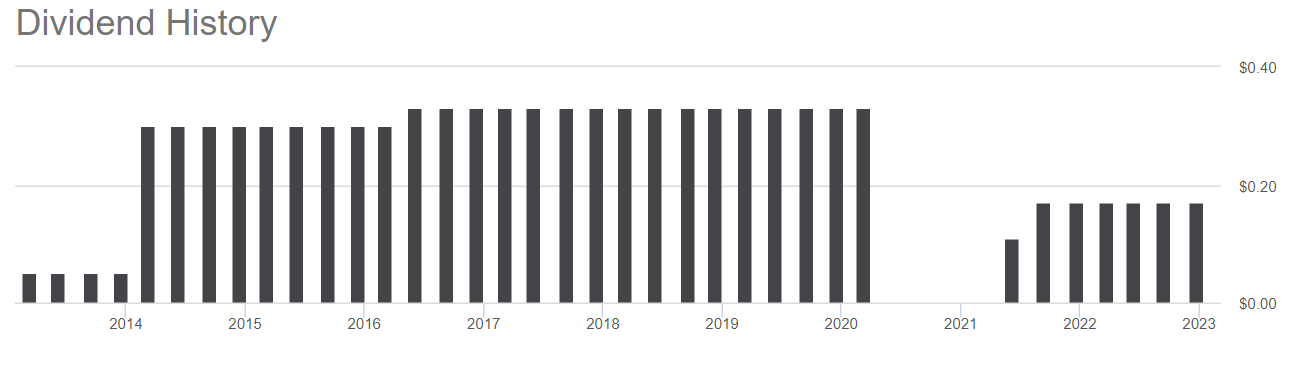

Since 2014, the company was paying a quarterly dividend of $0.33 per share, which was canceled during the coronavirus pandemic crisis and resumed during the second half of 2021 at $0.17.

The Cato Corporation dividend history (Seeking Alpha)

{kind=link}

This leaves a dividend yield of over 6.5%, which is more than reasonable taking into account that if the company manages to turn things around and resumes the full quarterly dividend of $0.33 per share, the potential dividend yield on cost for shareholders would be over 12.50%.

But please, be advised that this will only be possible in the long term if the company manages to return to the situation it was in in 2015, that is, to surpass again the $1 billion sales mark and an EBITDA margin in the 10-15% range, which will require the stabilization of inflation and a macroeconomic context free from recession. Therefore, I believe that although in the long term the potential dividend is very tempting, it is more important to focus on the ability that the company currently has to cover its current quarterly dividend of $0.17 per share.

To do this, I have decided to calculate what percentage of cash from operations the company has allocated to cover its dividend expenses over the years in order to calculate its sustainability through actual operations, and then I'll also explain how real the risk is of another dividend cut if profit margins fail to recover soon as inflation continues to be high.

| Year |

| 2013 |

| 2014 |

| 2015 |

| 2016 |

| 2017 |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| Cash from operations (in millions) |

| $92.96 |

| $117.46 |

| $93.85 |

| $72.13 |

| $35.99 |

| $60.24 |

| $53.40 |

| -$30.71 |

| $59.79 |

| Dividends paid (in millions) |

| $5.85 |

| $33.89 |

| $33.57 |

| $35.43 |

| $33.73 |

| $32.58 |

| $32.59 |

| $7.91 |

| $9.97 |

| Cash payout ratio |

| 6.30% |

| 28.85% |

| 35.77% |

| 49.12% |

| 93.72% |

| 54.08% |

| 61.04% |

| - |

| 16.68% |

As we can see in the table above, the dividend has been sustainable over the years (except for 2017 when it was too tight). Furthermore, in 2021 the cash payout ratio was as low as 16.68% despite negative cash from operations in 2020. The problem is that the actual annual dividend cost of $10 million is unsustainable in the long-term as trailing twelve months' cash from operations is negative at -$0.3 million while margins have worsened in the last quarter. Therefore, even though the company has cash and equivalents of $17.28 million and inventories of $116.72 million, the management could temporarily cancel the dividend in order to protect the balance sheet in the long term as they did in 2020 during the coronavirus pandemic.

However, dividends have not been the only way that the management has used to reward shareholders as it has also done so through share buybacks, which have expanded the positions of shareholders who have held the shares throughout the years.

A long tradition of share buybacks

The company has historically repurchased its own shares in order to reduce the total number of shares outstanding, a tradition that continues to this day. This means that each share represents, over time, a larger portion of the company, which leads to improve per-share metrics as the company's results are then divided into fewer shares.

In this regard, the company has managed to reduce the total number of shares outstanding by a whopping 26% over the past decade and, although this strategy could be paused for a while until profit margins improve again, long-term investors could expect further share buybacks in the future, eventually allowing dividend payouts to improve.

Risks worth mentioning

It's certain that a debt-free balance sheet greatly reduces the company's risk, but there are still certain risks that are very important to be aware of before considering the current share price decline as an opportunity to purchase the company's company shares.

- During the past few years, the number of stores has been slightly reduced from 1,372 in 2015 to 1,311. This allowed for a slight improvement in profit margins in subsequent years, but current inflationary pressures, as well as increased labor and freight costs, have once again caused a collapse in profit margins. Therefore, it is very important for the management to make a very conservative use of its reserves (basically cash and equivalents and inventories) to navigate current headwinds until they stabilize.

- To restore investors' optimism, it is important for the company to return to the sales growth path. For this to happen, it will first be necessary for margins to stabilize again and to use cash from operations to open new stores that achieve higher returns than the stores closed in the past. Otherwise, the company could continue to suffer sales declines in the coming years, as well as declining margins.

- A potential recession as a consequence of rising interest rates by central banks as a consequence of the current high inflation rates could have a very significant impact on the company's operations due to decreasing consumer purchasing power.

- Both dividends and share buybacks could be canceled in the short to medium term in order to preserve a healthy balance sheet during the current complex macroeconomic landscape.

Conclusion

The Cato Corporation is going through a bad time, and proof of this is the fall in the share price of 77% from all-time highs reached in 2015. To a negative trend in terms of sales has been added a significant worsening in the margins caused by current inflationary pressures and increased freight and labor costs, which has led the company to lose the ability to generate positive cash from operations.

Still, it is very important to remember that the company has been successfully operating since 1946 and that the trend has historically been positive. The store closures they've performed for the past few years were bearing fruit (in terms of profit margins) before the outbreak of the coronavirus pandemic, which leads me to believe current difficulties essentially represent temporary headwinds.

Therefore, I believe that now is a good time to buy the company's shares in order to achieve a good dividend yield on cost in the long term (despite the short-term risks of a dividend cut) and profit from an ever-increasing position size thanks to the company's long tradition of making share repurchases.

For further details see:

Cato: Long-Term Outlook Looks Fine Despite Current Headwinds