CMG - CAVA Group: The Chipotle Of Mediterranean Cuisine

2023-08-14 08:30:00 ET

Summary

- If you've been to a Chipotle, then you already understand CAVA Group, Inc. fairly well.

- It is, in the truest sense, the Chipotle of Mediterranean food.

- Because I've worked on Chipotle so much over the years, Cava has been fairly easy to understand, and I share some basic findings with you today.

- While I do think Cava from ~$5.6B in enterprise value will ultimately be a decent investment, and while I did nibble on shares around $40/share, I plan to wait for a more attractive entry point.

- That said, I think the product and business model, atop a pristine balance sheet, are sound, and I do think this concept will succeed and then some over the long run, generating solid returns for shareholders in the process.

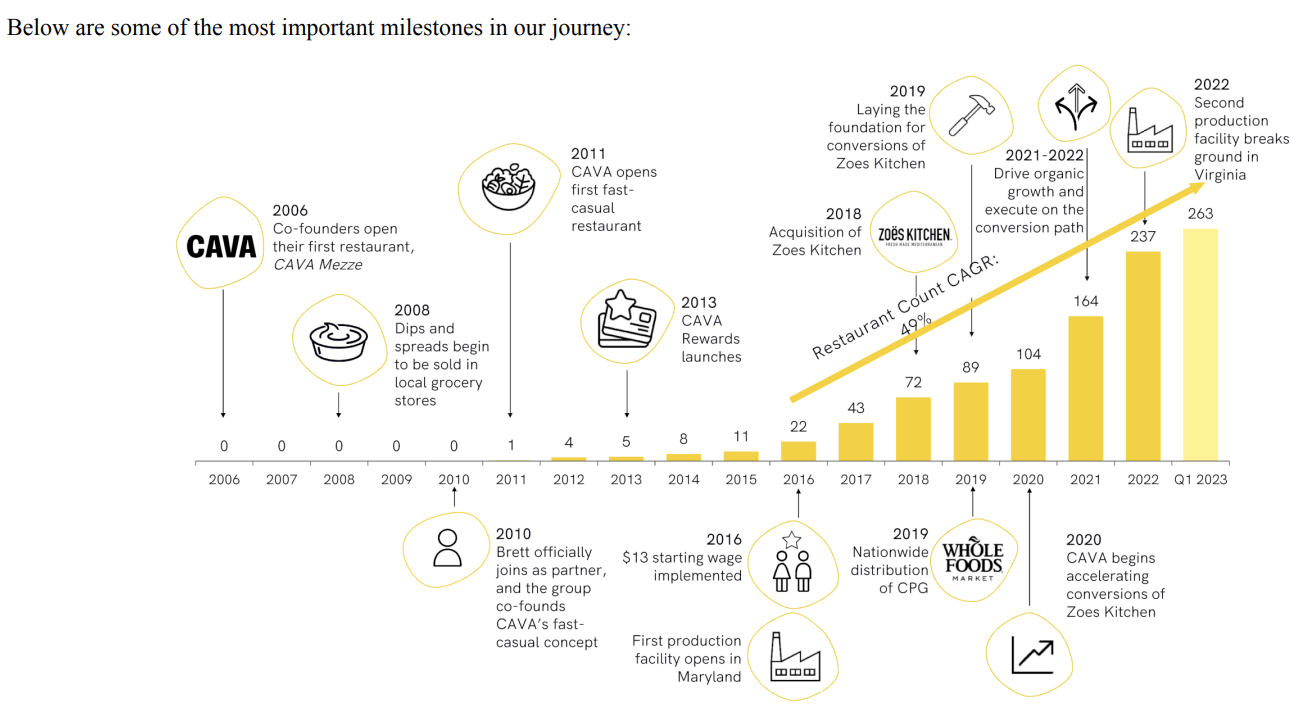

The History Of Cava Graphically Depicted

{kind=link}

I Don't Think I've Ever Been More Prepared For An IPO

Over the last handful of years, one of my consistently largest positions has been Chipotle Mexican Grill, Inc. (CMG).

Yesterday, I ate Chipotle for lunch. Over the last 10 years+, I have looked forward to eating Chipotle each week, excepting the periods in which I was serving in the U.S. army overseas.

I have written in great depth publicly about the business over the last few years in notes such as:

- Chipotle: Location Growth (Still) Makes It A Better Buy Than McDonald's .

- Chipotle: Location Growth Makes It A Better Buy Than McDonald's .

In short, I have had something of an obsession with the business of Chipotle, and this obsession has laid the foundation for what I believe could be two very attractive opportunities over the long run:

- CAVA Group, Inc. (CAVA).

- And, to a somewhat lesser extent, Dutch Bros Inc. (BROS)

Today, we won't discuss Dutch Bros, but it's certainly a business that fits within the cohort of Cava and Chipotle as "next gen, rapidly growing" consumer brands food & beverage brands that have long runways for growth.

With these ideas as our platform, let's now begin our review of my Cava thesis and the Cava business broadly.

Quantitatively Articulating Our Cava Thesis

Alex Morris' The Science of Hitting

As can be seen above, Cava has grown its unit count at an incredibly healthy rate over the last 10 years.

As has been the case for my Chipotle thesis, my Cava thesis will center around unit, or location, or restaurant (all synonymous), growth.

To be more precise, my thesis will center around unit growth as well as unit profitability, keeping in mind Cava's corporate level SG&A spend. My goal here is to make everything has concise and digestible as possible. As is always the case, I do not believe any extravagance is needed in modeling what is ultimately a simple restaurant concept with fairly simply economics, but executing a business, no matter the size, can certainly feel like doing rocket science.

Below, you will find Beating The Market's modeling for Cava over the next 10 years.

- Note: AUV is an acronym that stands for Average Unit Volume. This is the average total revenue one Cava restaurant generates.

In the following data exploration, in order to better understand Cava, we will also consider Chipotle's AUVs, as well as other key metrics.

| AUV (Today) |

| AUV (Yr 10) |

| Cava |

| ~$2.5M |

| $3.5M |

| Chipotle |

| ~$2.75M |

| $3.5M |

As the above chart depicts, Cava's current AUV is about $2.5M. Chipotle's AUV is a bit higher, but it is about 20 years ahead of Cava in terms of maturity.

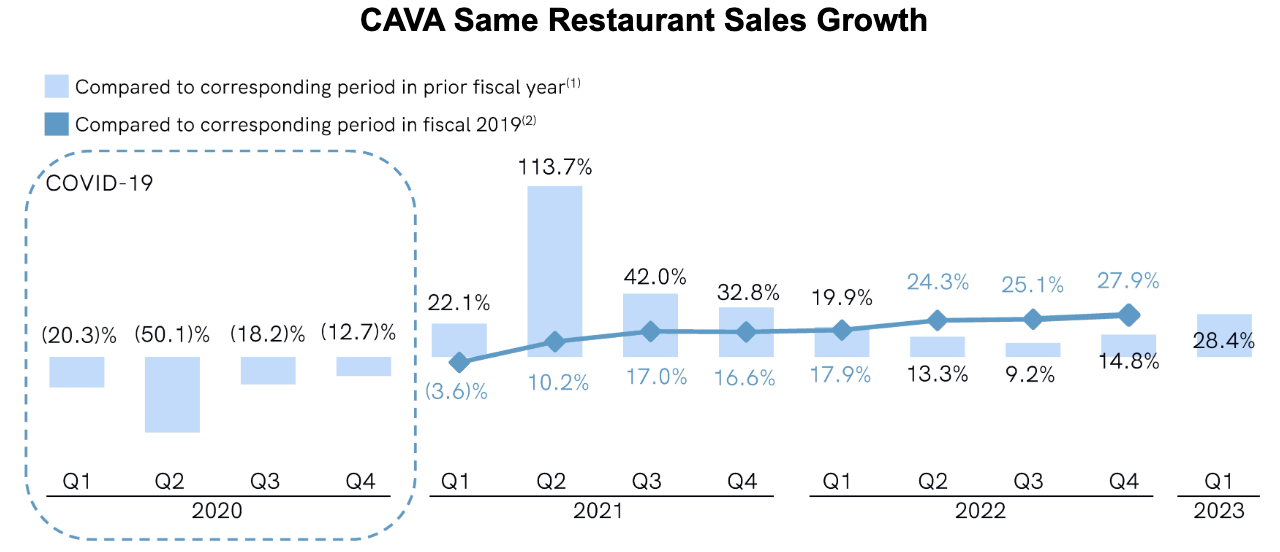

I do not believe $3.5M AUV is outlandish in any sense, as, assuming just 2% annual inflation, we would reach $3M in AUV by 2033 from a base of $2.5M in AUVs, and both Cava and Chipotle have legendary "same store sales growth" metrics, which will further propel AUVs in the decade ahead.

Cava Same Store (Restaurants) Sales Growth

{kind=link}

Most same store sales in the QSR industry hover at 5% or lower. Cava's same store sales growth mirrors what Chipotle has experienced over the last ~20 years as a public company.

Turning to unit count:

| Unit Count (Today) |

| Unit Count (Yr 10) |

| Cava |

| 300 |

| 1,000 |

| Chipotle |

| 3,000 |

| 7,000 |

As we can see, Cava currently operates about 300 units; whereas, Chipotle operates about 3,000, with line of sight to 7,000 in North America alone (we've, as in my partnership with Chipotle, been having success in EU so far, which is heartening, and it recently announced expansion into the Middle East).

This suggests that Cava has a long runway for growth ahead.

Further, Cava's management has guided for "more than 1,000" units by 2033. For conservatism's sake, we will use 1,000 in my valuation assumptions later in this note.

Turning to restaurant level margins:

| Restaurant Level Margin (Today) |

| Restaurant Level Margin (Yr 10) |

| Cava |

| 25.4% |

| 27.5% |

| Chipotle |

| 27.5% |

| 27.5% (Maybe higher) |

Incredibly, restaurant level margins for Cava and Chipotle are virtually identical (precise numbers used in lefthand column above).

I believe that these robust margins on a unit (restaurant) buttress an achievable long run free cash flow margin of 15%, which I depicted below:

| Long Run FCF Margin |

| Shares Outstanding |

| Net Cash |

| Cava |

| 15% |

| 120M (Fully Diluted) |

| ~$390M |

| Chipotle |

| 16% (Maybe higher) |

| 27.75M (Fully Diluted) |

| $1.8B |

As we can also see, Cava has about 120M shares outstanding fully diluted. Notably, it has no long-term debt, and it, post-IPO, now has about $390M in cash on its balance sheet .

As an aside, Chipotle has $1.8B in cash and no long-term debt, which is incredible and has been a key component of my thesis for the business.

As something of an aside, the majority of the businesses I own have similarly absolutely pristine balance sheets, so it is very heartening to see Cava's foundation constructed via a likewise pristine balance sheet of ~$390M in cash and virtually no long-term debt (Cava has $538,000 in long term liabilities, which is effectively $0 relative to its newly raised cash hoard).

- As one last aside, a handful of years ago, GAAP accounting rules changed such that operating leases, i.e., the rent paid to landlords, are now required to be accounted for as a liability, which impacts funding costs for businesses that pay a monthly or annual rent. You may come across "operating lease liabilities" while studying businesses' balance sheets in the liabilities section.

With the above metrics in mind, we can model Cava's fcf/share by 2033, and I did so below:

| Fcf/Share (Today) |

| FCF/Share (Yr 10) |

| Cava |

| $.9375 |

| $4.375 |

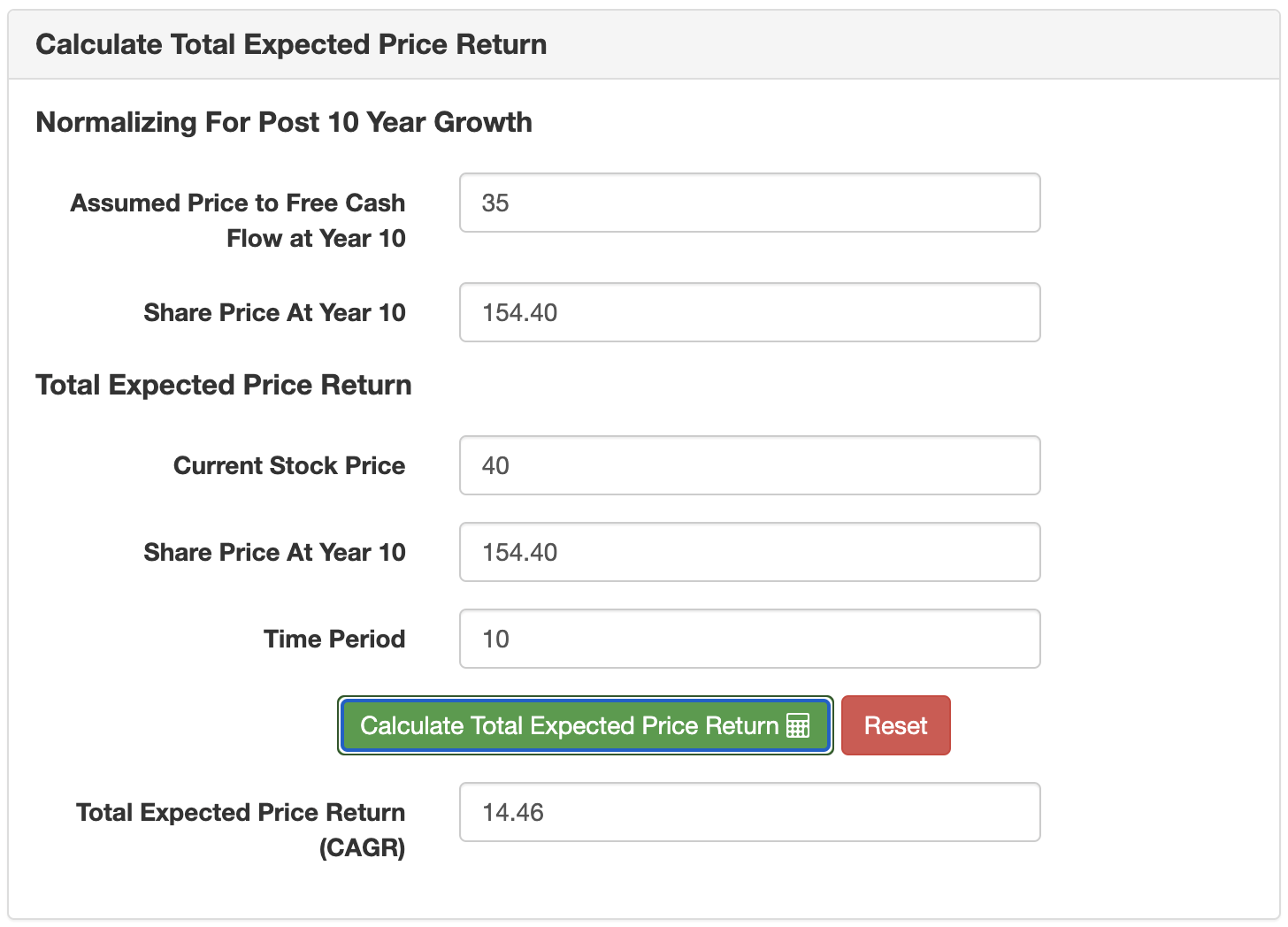

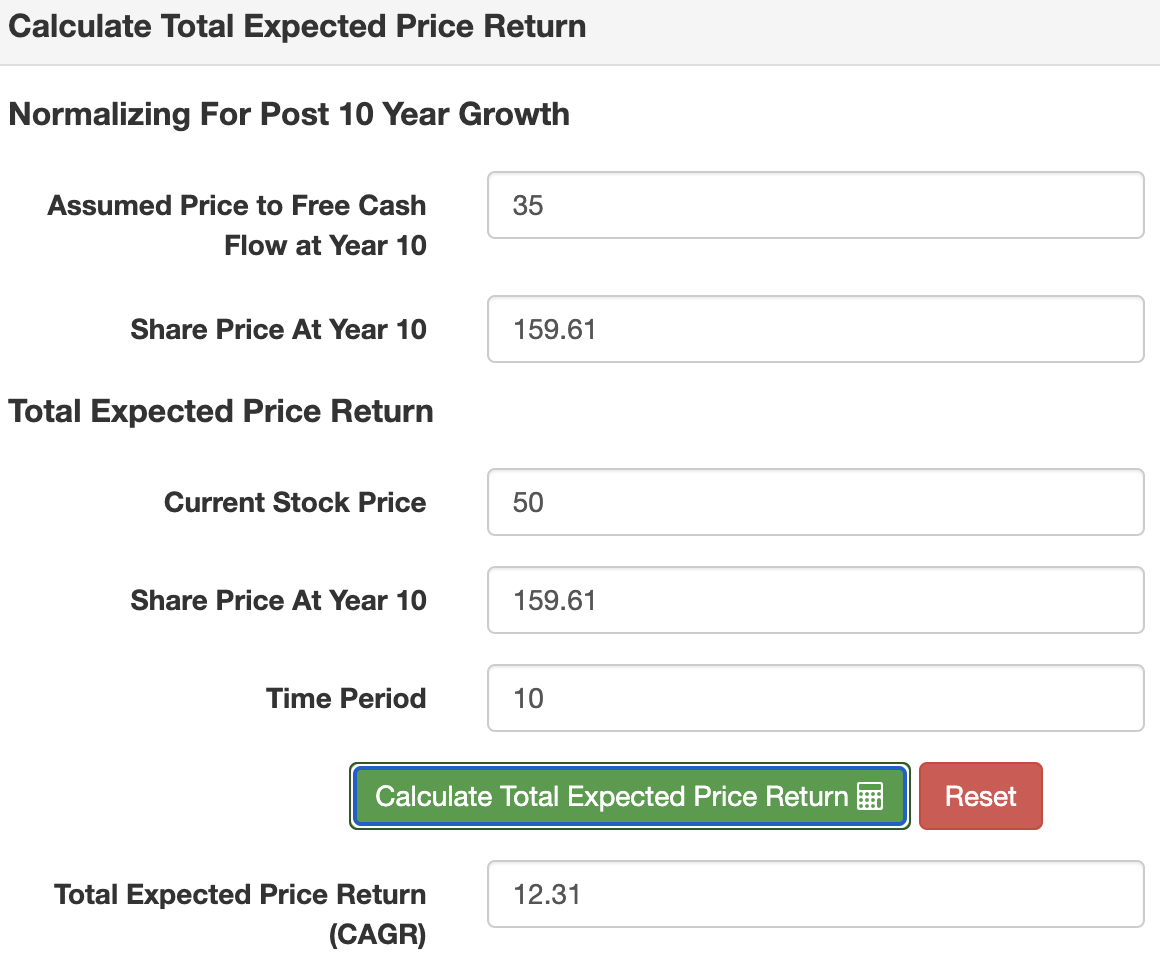

We can then apply a reasonable valuation multiple whereby we achieve a target valuation by 2033:

| Current Market Cap |

| Yr 10 Market Cap (Assumed Exit Multiple 35x) |

| Cava |

| ~$6B (120M shares * $50/share) |

| $18.375B ($4.375 in fcf/share * 35x p/fcf * 120M shares) |

| Assumed CAGR |

| ~12% |

In the above table, I used a CAGR calculator to arrive at the ~12% annualized return that we could achieve in buying Cava at ~$50/share.

I don't believe this is optimistic. I don't believe this is conservative. I think this is precisely what we should expect from Cava over the next 10 years.

That said, in light of the rave reviews I've received regarding Cava's core product; and in light of the fact that Cava could certainly eclipse 1,000 locations sooner than 2033, I think there actually may be some conservatism in the above modeling.

I think the data below further substantiates this thinking:

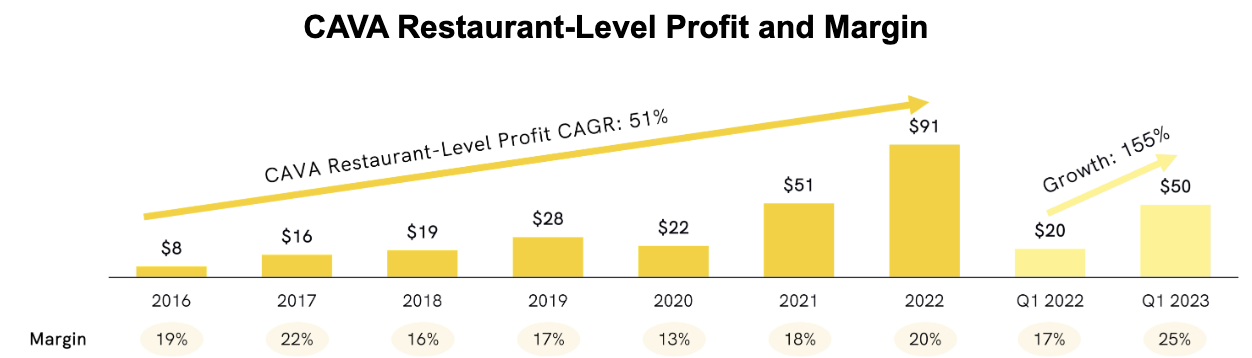

Cava Is Growing Rapidly

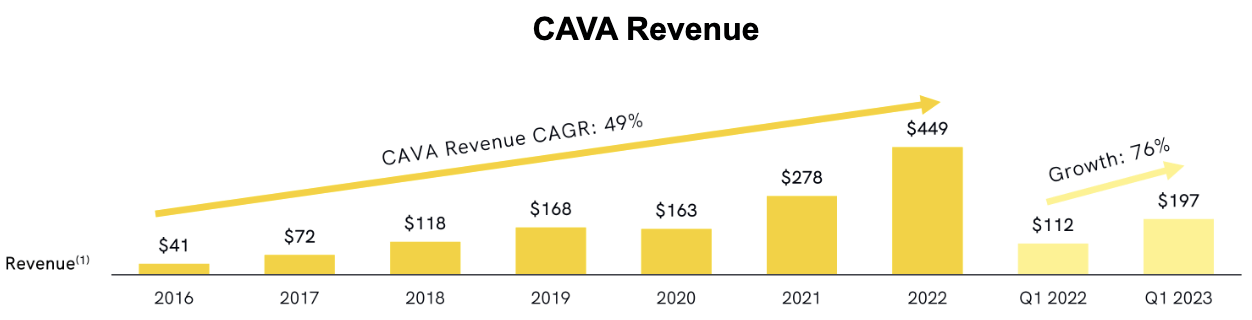

Below, we can see that Cava generated $197M in Cava restaurant sales in Q1 2023, growing at 76% year-over-year, with a restaurant level profit of $50M (25%). Incredible.

{kind=link}

{kind=link}

{kind=link}

This implies that Cava currently trades at a valuation far lower than a cursory glance might suggest; hence, its post IPO pop makes a lot of sense.

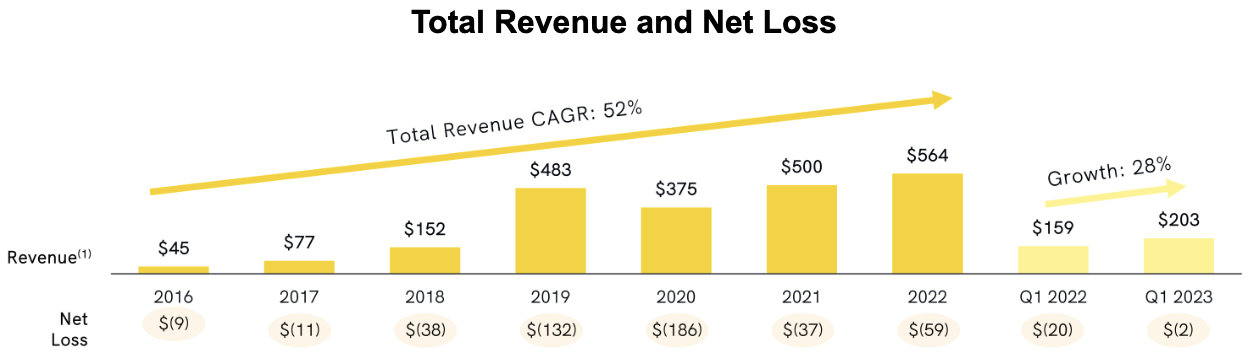

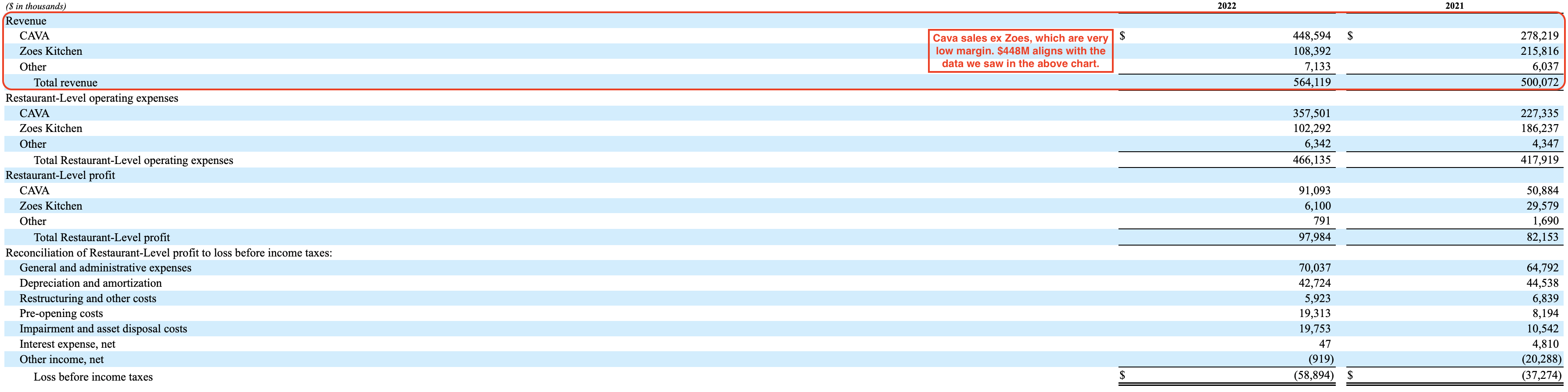

- Note: Zoes Kitchen's revenue distorts total revenue a bit. Please disregard total revenue and focus exclusively on Cava revenue. Here's the S-1 breakdown that substantiates as much:

{kind=link}

If we annualize Q1 2023, Cava will generate about $800M in sales for 2023 (it could come in closer to $1B considering same store sales growth and unit growth).

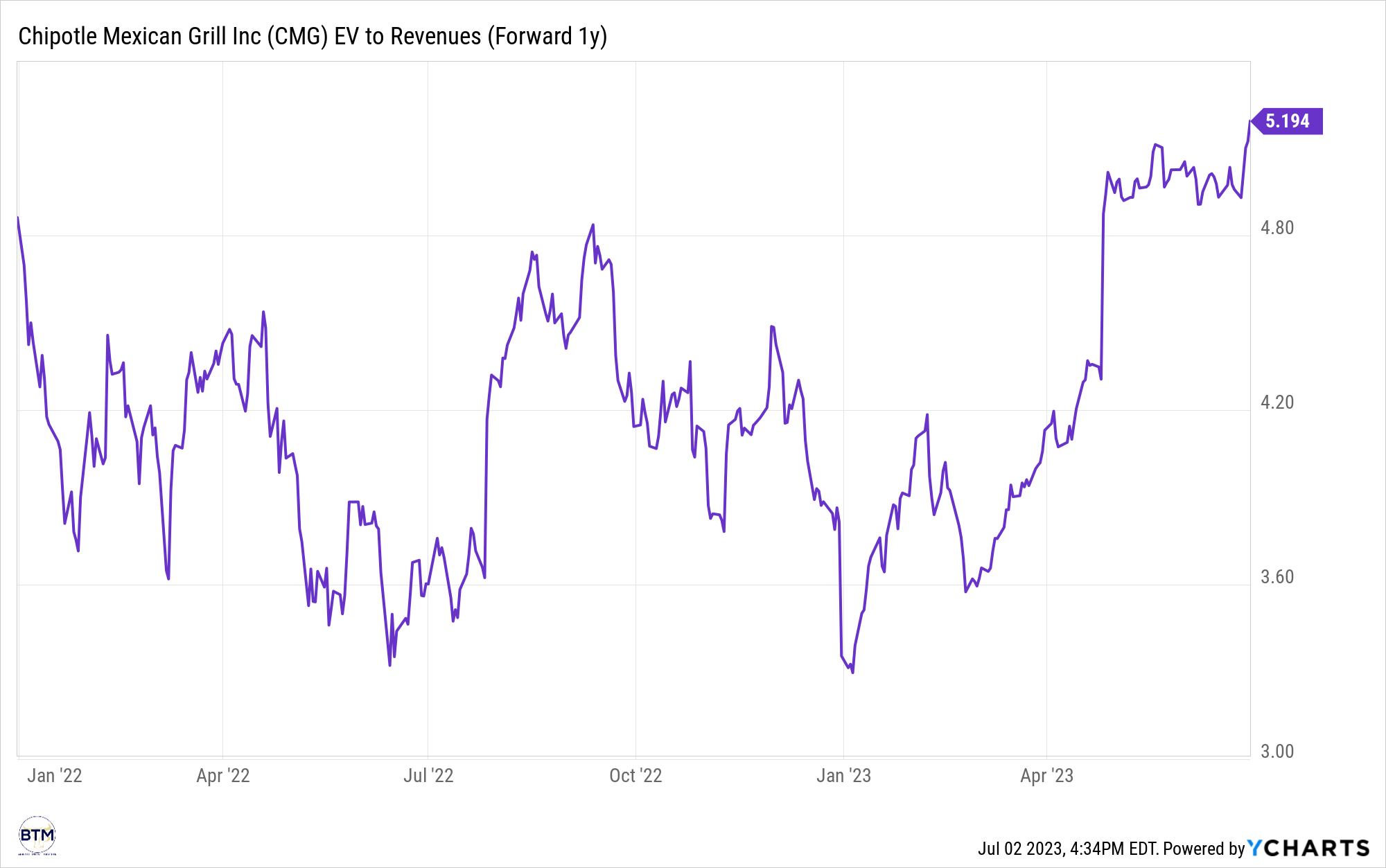

At $5.4B in enterprise value, today, Cava isn't much more expensive than Chipotle, despite have a vastly longer runway for growth, alongside proven unit economics and a proven beloved format (scale is all that is unproven, but the same could be said for every younger company ever. It is the risk that generates the return in the risk = return equation).

Chipotle's EV/Fwd. 12 Months Sales

{kind=link}

In fact, Cava very well could turn out to be less expensive depending on where growth lands in the next 12 months!

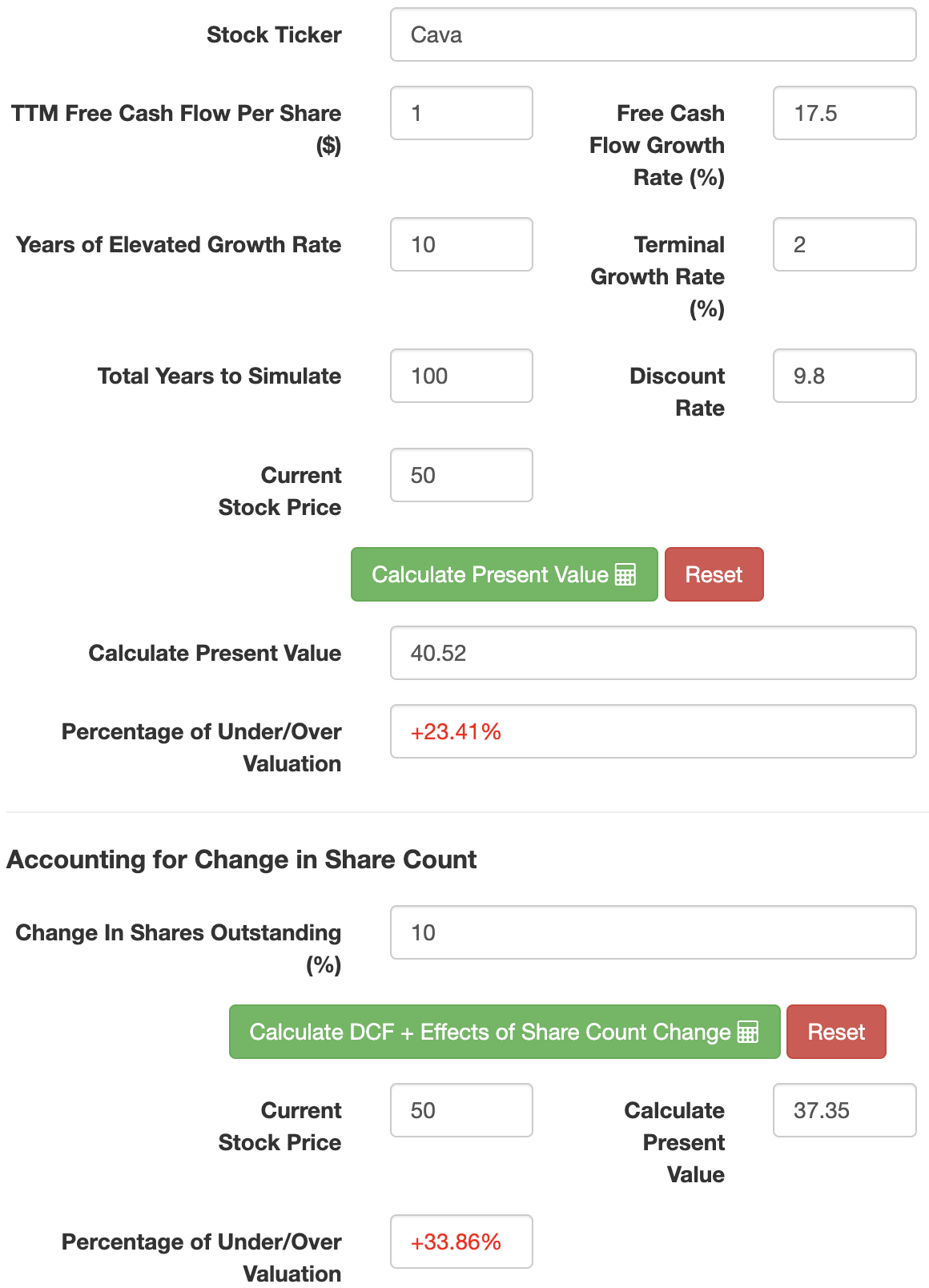

LASV Model

With these ideas in mind, let's perform a valuation walkthrough using my proprietary valuation model:

Proprietary Valuation Model Created By Author

{kind=link}

Proprietary Valuation Model Created By Author

{kind=link}

{kind=link}

As we saw, Cava is presently growing at 76%, so I think growth of 17.5% for the next 10 years (annualized) is more than achievable.

It may be too conservative! And, in that vein, we could still generate ~12% annualized returns, which suggests we have a margin of safety here.

Further, like Chipotle has been for its North America target unit count, I think Cava could be a bit too conservative in how many units it can deploy.

The world is hungry for more Chipotle-like concepts; however, they are so challenging to execute/make profitable at scale that we've been deprived of them.

Leadership

The parallels between Cava and Chipotle are quite striking.

From their margins to their products, there are many similarities.

One of the more striking similarities that I've found was how they both began.

In this note , I detailed the idea that McDonald's (MCD) was integral in the formation of Chipotle, as one of its major early investors (though McDonald's would ultimately sell its shares in 2006; #neversell).

Cava has had a similar experience, with Panera Bread's founder investing a large sum of money into the business. Mr. Ron Shaichs also helped broker the deal between beleaguered Zoes Kitchen and Cava, in which Cava acquired Zoes Kitchen with the intention to convert the locations into Cavas, and this has allowed Cava to scale rapidly with little need for investment in real estate.

Further, Mr. Shaichs assumed the role of Executive Chairman of Cava's board of directors.

Here's a link through which you may learn more about this gentleman:

Lastly, like Chipotle in its early years as a public company, Cava is Founder-CEO led.

You may learn more about Cava's Founder-CEO via the link below:

The Zoe's Kitchen Acquisition & Subsequent Conversions

Washington, D.C.-based Cava, a privately held company with 66 restaurants, agreed to acquire the Plano, Texas-based Zoe’s, a public company with about 260 units, for $12.75 a share, a 33 percent premium over Zoe’s Thursday close of $9.56 in a share.

Cava Group to acquire Zoe's Kitchen

Our category-defining brand, authentic offering, and attractive business model are supported by powerful unit economics that drive our strong performance. We increased the number of CAVA Restaurants from 22 as of the end of fiscal 2016 to 263 as of April 16, 2023, representing a CAGR of 49%. We have steadily grown CAVA Revenue each year since 2016, except for a slight decline in fiscal 2020 as a result of the COVID-19 pandemic. Since the Zoes Kitchen acquisition, through April 16, 2023, we have successfully converted 145 Zoes Kitchen locations into CAVA restaurants, in addition to opening 51 new CAVA restaurants during such period.

At the same time, we have successfully managed through the mid-to-high-single digit inflationary environment and were able to expand CAVA Restaurant-Level Profit Margin to 20.3% in fiscal 2022, despite only increasing our in-restaurant menu price by less than 5%.

Cava's S-1 (emphasis added).

As we read, the bulk of Cava's unit growth has come via Zoes Kitchen conversions.

When I first heard about this, I was concerned as we always far prefer pure, organic growth, but, after studying how this has gone in my local region of Northeast Florida (they've not added locations to St. Augustine just yet), I was pleasantly surprised.

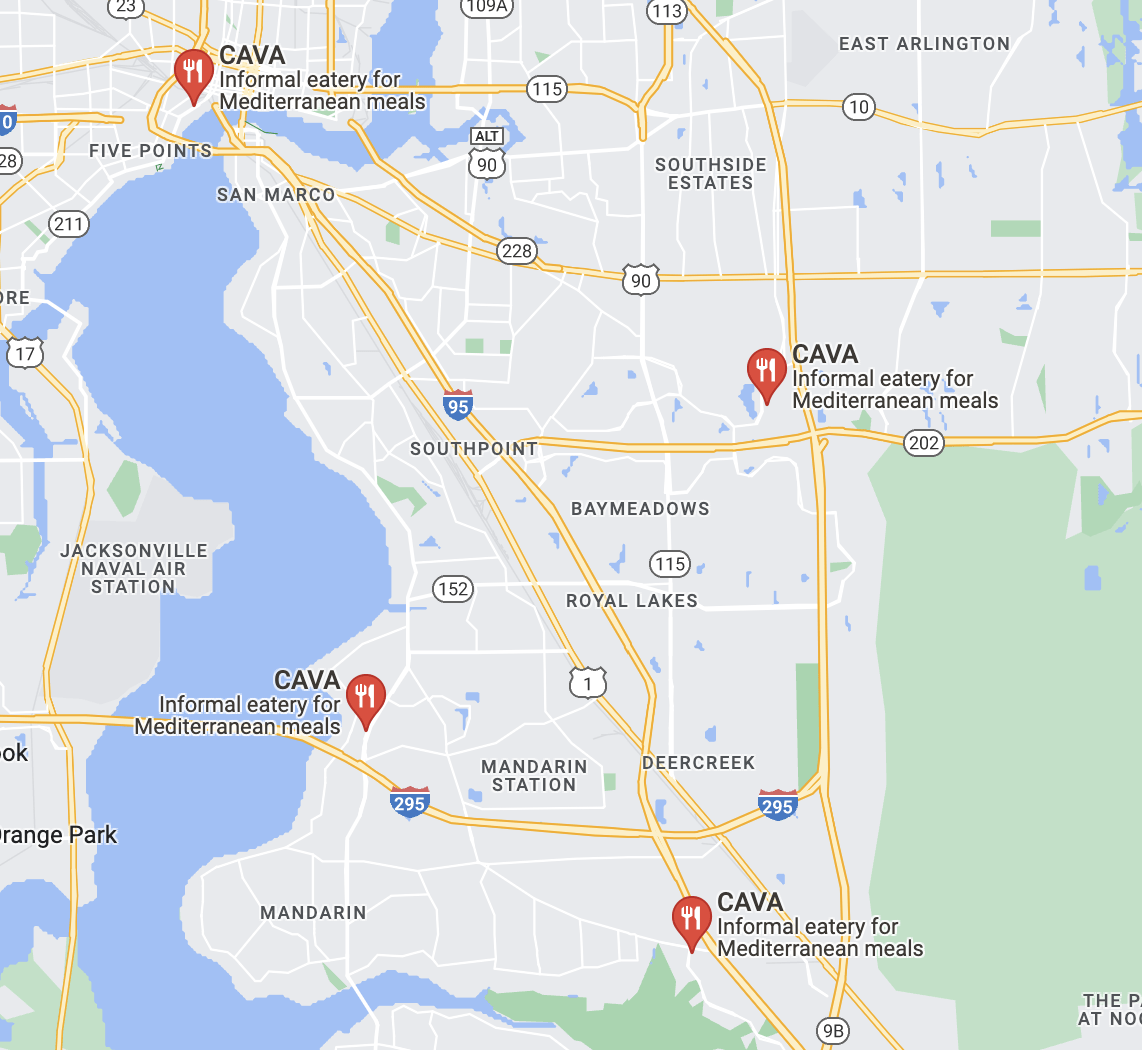

Every single conversion has performed exceptionally well thus far. As we can see below, Zoes Kitchen used to operate in Northeast Florida.

Google Maps

Today, they are all closed according to Google Maps, but, when we search for Cava, we can see that they are not closed technically speaking; instead, they are now Cava locations.

{kind=link}

If you don't take my word for it, I would invite you to Google Jacksonville, FL, and check out the reviews for each Cava location to discern how these locations have performed.

The App

Integrated Loyalty Program

Our loyalty program creates a value-added experience for guests both in-restaurant and through our digital channels, enabling them to earn rewards as they purchase. Our payment and loyalty pass is integrated, including the ability to use digital wallets such as Apple Pay, creating greater utility and convenience for our guests. As of April 16, 2023, we had approximately 3.7 million loyalty members, representing a 56% year over year increase in loyalty membership.

As a connoisseur of the Chipotle app, I was excited to try Cava's app, and it has not disappointed.

Additionally, it appears to have been executed positively exceptionally, with ~65k Apple App Store ratings and a 4.9 star average (as opposed to Chipotle's 4.6 star average. I've noted in the past that Chipotle had issues with its app's execution over the last 5 or so years).

This is certainly one of the most exciting aspects of the Chipotle and Cava thesis: I get a free Chipotle meal (worth about $10) every three weeks via using the Chipotle app, which is very easy and convenient to use, so I am excited to test the Cava app in the weeks ahead.

Concluding Thoughts: The Duopoly

I plan to visit the southernmost Cava depicted in the Google Maps above in the coming weeks (perhaps this week, as I am so excited by Cava, because I've thought for a long time that we need more another Chipotle-like concept as legacy fast food, e.g., KFC or Burger King, winds down a bit.).

I will share my findings when I visit; however, as I've mentioned, most folks I've talked to have raved about Cava in the same way I've raved about Chipotle.

I think, like the duopoly of McDonald's and Burger King, we may find that Cava and Chipotle form something of a duopoly over the next 10-20 years.

At any rate, as a fan of these concepts, I am excited to try Cava, and I am excited for what I am fairly certain will become a "hopefully forever" partnership with Cava in the months ahead.

As of today, I've not bought a lot of Cava, but the financials are totally sound in my mind. The Zoes Kitchen conversion situation was my one point of uncertainty, but it appears that they've executed this brilliantly.

The business has a giant cash hoard of ~$390M and virtually no long-term debt.

At some point in the next 10 years, it will very likely begin buying back shares, and that will accelerate the growth of fcf/share even further beyond what unit count will achieve.

I nibbled on Cava at about $40/share, but I plan to wait until there's a solid bout of market pessimism and/or it reports its first quarterly results formally to begin accumulating in earnest.

For further details see:

CAVA Group: The Chipotle Of Mediterranean Cuisine