SKY - Cavco Industries: Benefiting From Long-Term Tailwinds

2023-11-29 21:24:51 ET

Summary

- The consolidation trend in the manufactured housing industry persists, with the top three companies exceeding a 75% market share.

- Despite the short-term headwinds, Cavco will benefit from the U.S. demographic structure and the housing shortage.

- From a conservative approach compared to the analyst consensus, I consider Cavco to be undervalued, assigning a fair price of $382 with a 35% upside potential.

- Cavco has a strong balance sheet with cash-in-hand above total liabilities and is repurchasing shares at low valuation multiples.

Despite experiencing declining revenues for four consecutive quarters, Cavco Industries ( CVCO ) is witnessing a stabilization in its backlog, and utilization rates may improve soon, all while the company's valuation remains historically low.

The current undervaluation provides the opportunity to benefit from long-term tailwinds in the manufactured housing industry such as the U.S. demographic structure, many years of housing undersupply, and the consolidation between fewer companies.

Cavco's Business Model

Cavco Industries is one of the largest producers of manufactured homes, which are distributed through a network of independent and Company-owned retailers (68 stores , 41 located in Texas), planned community operators, and residential developers.

Homes are constructed using an assembly-line process designed to be flexible in order to accommodate customer-requested customizations, and each module is completed in stages. This process enables Cavco to produce homes in less time (six production days on average) and at a lower cost than building them on individual sites.

To optimize every stage of the process, Cavco operates 29 manufacturing facilities in the U.S. and 2 in Mexico, most of them owned, typically located within 350 miles of the primary geographic market.

Homes are produced on demand, and after production of a particular home has commenced, the order becomes non-cancelable and the distributor is obligated to take the delivery, which allows Cavco to maintain low inventories and increase returns on capital.

On top of the housing business, the company also offers property and casualty insurance to owners of manufactured homes.

After a rapid increase in revenues and margins during 2021 and 2022, the number of houses sold and prices have been normalizing over the last quarters, reverting Cavco's financial figures back to the mean.

Industry Overview

The factory-built housing market is competitive and companies don't have much pricing power due to the lack of differentiation in their products and low entry barriers, so competitive advantages come from efficiency, scale, and the distribution network.

The bigger size allows getting better prices for the inputs used during production, which are mainly oriented standard boards, wood, steel, aluminum, and electrical items.

Factory-built housing companies are not only dependent on the cost of materials, which have been recently normalizing as shown in the chart below, but are also cyclical.

The industry is sensitive to economic conditions, employment levels, and the availability of financing. Since manufactured homes are significantly cheaper when compared to traditional site-built homes, the main clients are lower-income households that are particularly affected by periods of low employment rates.

So far, it looks like an industry one would try to avoid, but some long-term tailwinds could make Cavco an attractive buy.

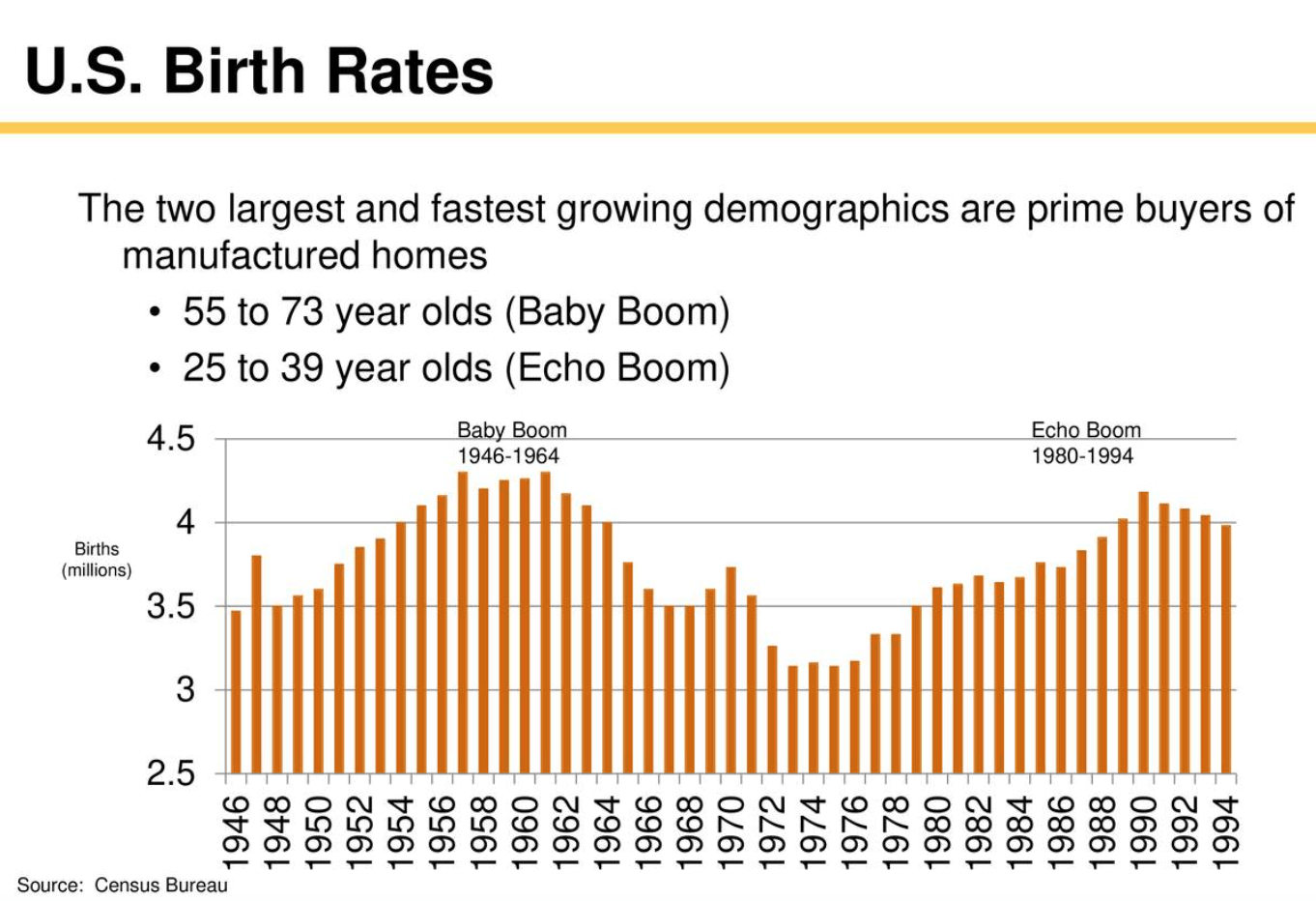

Demographics

The largest manufactured housing consumers are young single persons, young married couples, and those aged 55 and older with low household incomes.

{kind=link}

Source: Cavco Industries Investor Presentation May 2020

The current growth of the older population, driven by the large baby boom generation, is unprecedented in U.S. history and is projected to nearly double by 2060.

Also, millennials (born between 1981 and 1996) are entering the housing market, and the growing household formation trend is expected to last at least until 2030.

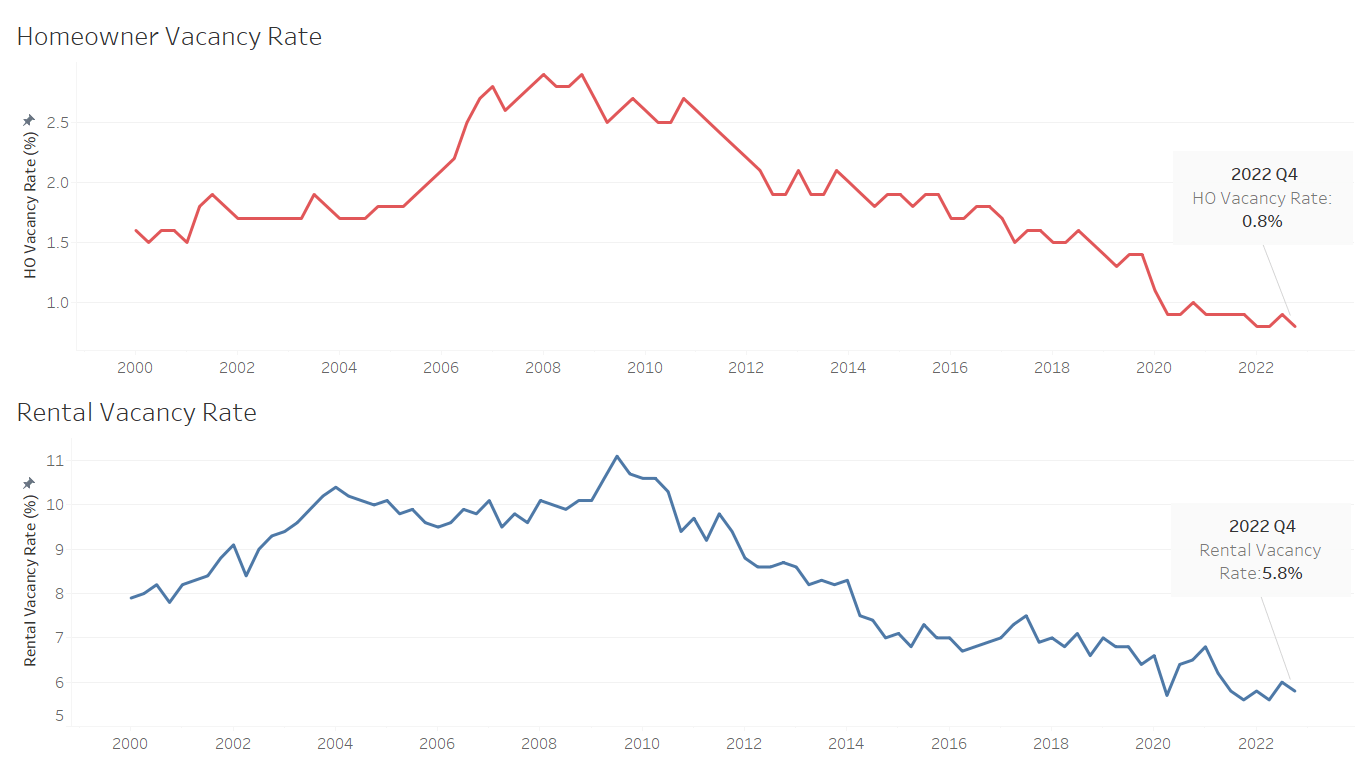

Housing Shortage

During the last twelve months, the number of households has increased by 1.5% in the U.S., or 1.92M new households, while the number of houses completed has been at 1.41M.

The housing shortage has been increasing over the last decade after the market absorbed the oversupply generated prior to the burst of the housing bubble in 2007.

{kind=link}

Source: realtor.com

The increases in raw material prices and the supply chain disruptions after the pandemic, combined with the recent increase in interest rates are not helping to reduce the gap between supply and demand, driving vacancy rates to the lowest levels in over two decades.

{kind=link}

Source: realtor.com

As long as interest rates remain high, it is unlikely that home prices decline considerably. Existing homeowners have the incentive to hold on to their homes to keep their low interest rates since 61% of mortgages outstanding have an interest rate below 4%, which is significantly lower compared to the current 7.7% average interest rate on mortgages.

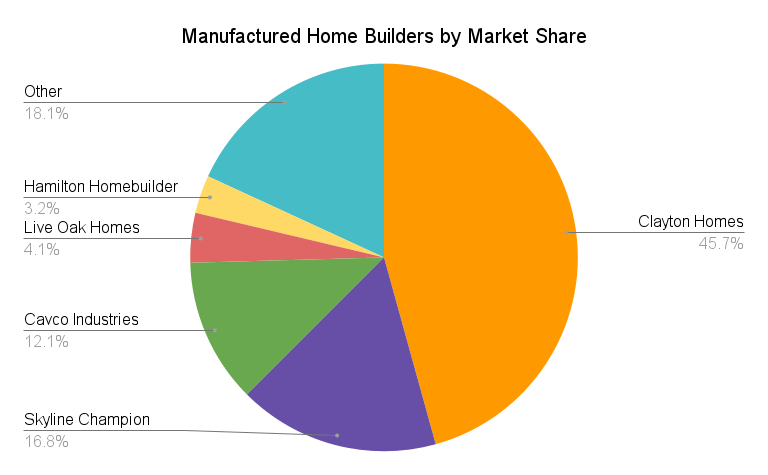

Consolidating Market

When looking at the number of companies operating in the manufactured home industry and its concentration, in 2003 the top 25 manufacturers had 78.8% of the market. Currently, the top 3 have over 75% market share.

{kind=link}

Source: Author (Data from Manufactured Housing Institute)

As shown in the chart above, the Berkshire Hathaway (NYSE: BRK.B ) (NYSE: BRK.A ) owned Clayton Homes has almost half of the market, followed by Skyline Champion Corporation (NYSE: SKY ) and Cavco Industries, which has increased its market share from 2% in 2003 to the current 12.1%.

A consolidating market with fewer companies makes it easier for them to increase margins due to higher volumes of raw materials, providing better prices, and increasing utilization and efficiency at the production plants.

For the upcoming years, I don't expect this trend to revert, since it is becoming harder for smaller participants to compete against the biggest companies in the industry.

Cavco's Financials

Cavco has been building a strong financial position over the years, with above-average returns on invested capital, increasing margins, and a higher cash-in-hand balance than total liabilities, positioning the company to successfully navigate the market cycles.

Revenues

During the last quarter, the number of homes sold has decreased by 16.9% YoY and the average price has decreased by 6.7% YoY to $102k per home sold.

{kind=link}

Source: Author (Data from Cavco Industries Financial Reports)

The decrease in price per home sold during the last quarter was primarily due to more single-wide in the mix and to a lesser extent product pricing decreases, so the question is why the number of homes delivered has been decreasing despite the housing shortage.

There are two main reasons to explain the most recent results. First, Cavco enjoyed abnormal growth rates during 2021 and 2022, with revenues increasing by 46.8% in FY2022 and 31.7% in FY2023. When excluding the acquired companies during those years (Commodore in 2021 and Solitaire in 2023), revenues increased by 34% and 31%, which is still above its ten-year average.

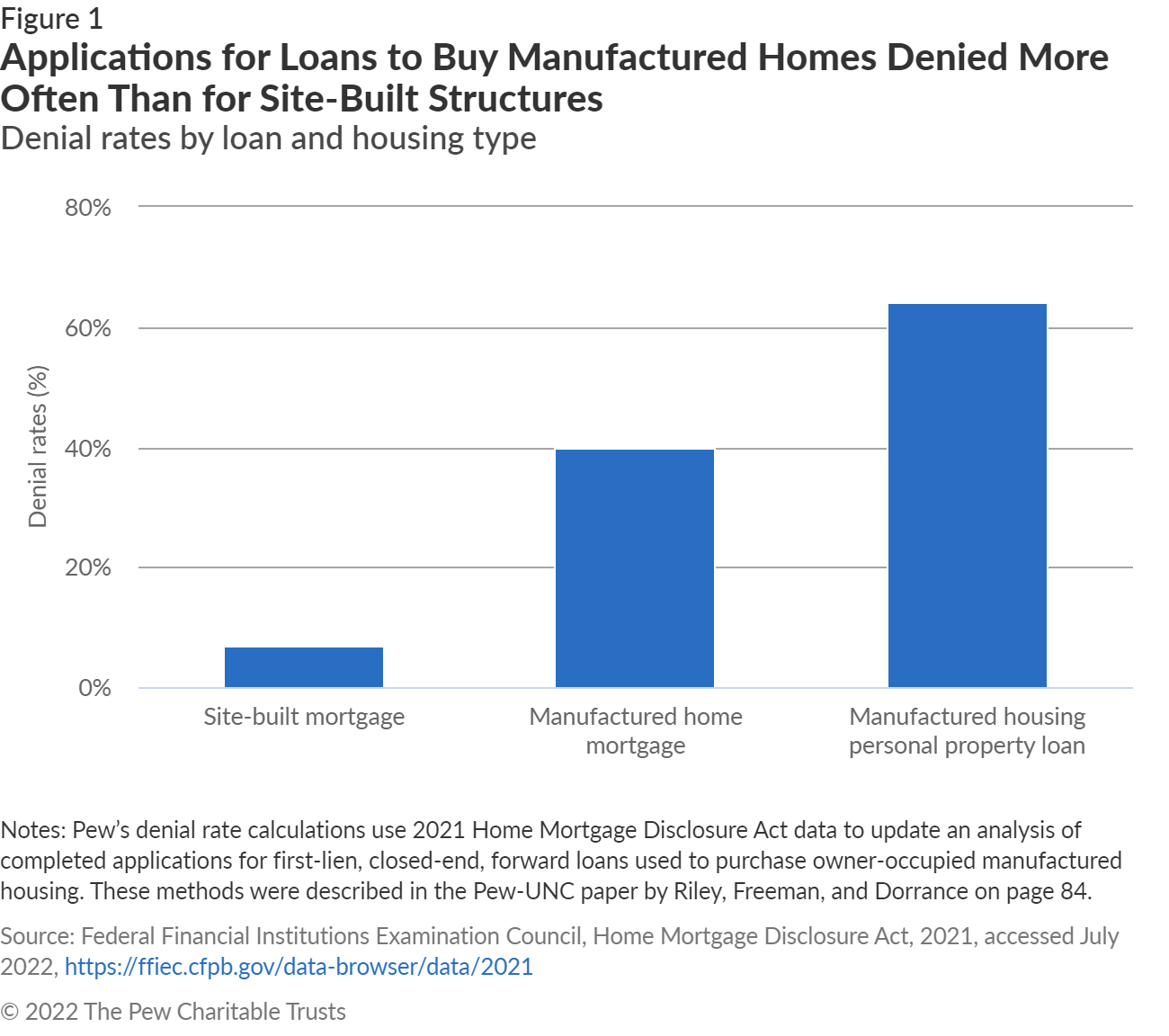

The second reason to explain the decrease in the number of manufactured houses sold is the higher denial rate compared to site-built homes, making the former more sensible to interest rates .

Over 75% of new manufactured homes are purchased as personal property for which there is no federal loan program, and as a result, buyers have few financing options. Moreover, manufactured home buyers are often held to higher credit standards, resulting in higher denial rates .

{kind=link}

Source: Federal Financial Institutions Examination Council, Home Mortgage Disclosure Act, 2021, accessed July 2022

Despite the short-term headwinds, according to data reported by the Manufactured Housing Institute, industry home shipments decreased by 27.0% for the calendar year through August 2023, while Cavco's deliveries decreased by 16.9%, showing a better performance than its competitors .

Profitability

Cavco has an operating leverage of ~2 times, meaning every percentage point of increase in revenue increases operating profits by 2% since its business model incurs significant fixed costs such as production plant maintenance and wages.

When demand increases, the company enjoys higher utilization rates on its plants and improves margins, but the opposite happens when there is a decrease in revenues.

Source: Author (Data from Cavco Industries Financial Reports)

Note: Data for 2024 are author estimates based on 1H2024 results and analyst consensus .

As shown in the chart above, as revenues started to decrease in late 2022, operating margins and returns on invested capital ((ROIC)) reverted to the long-term average. But still, despite utilization rates decreasing from 80% at the end of 2022 to the current 60%, operating margins have improved significantly from pre-pandemic levels.

Part of the compensation paid to production employees is dependent on efficiency and production levels, which aligns interests between the company and its employees while helping adjust costs in low-demand environments.

Also, Cavco has been focused during the last quarters on managing costs and has reduced plant operations to a four-day-a-week schedule.

When comparing Cavco's profitability with Skyline Champion Corporation, its closest competitor, we can see that the latter has better margins, higher inventory turnover, and returns on assets, suggesting it has superior operating efficiency.

Source: Seeking Alpha

Balance

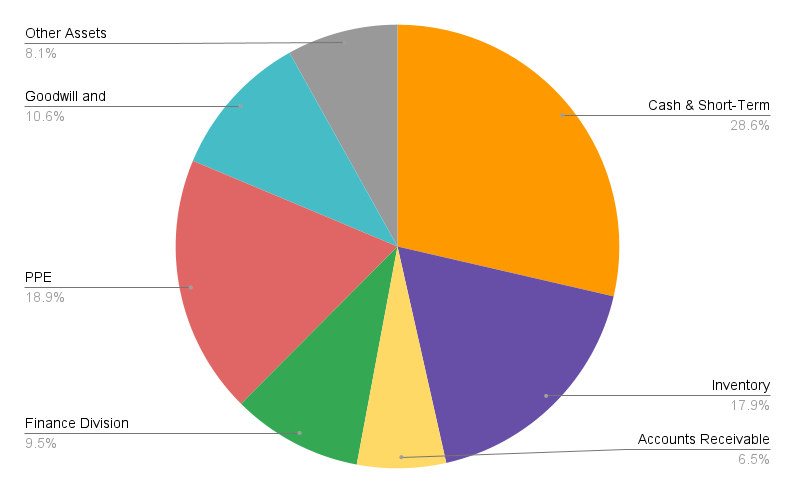

Cavco has a healthy balance sheet, with $1.36B in assets and just $349M in total liabilities, which are mainly accrued expenses for raw materials, wages, and customer deposits.

All liabilities can be covered with the current cash in hand ($377M), which I believe is important for a company operating in a cyclical industry.

{kind=link}

Source: Author (Data from Cavco Industries 10-Q September 30, 2023)

Despite the strong balance position, one of the aspects that should be monitored over time is the Finance Division Loans. Currently, 64% of the consumer loans have a FICO score over 680 points, and 32% are between 620 and 679. The average loan is maturing in 164 months with an interest rate of 8.1%.

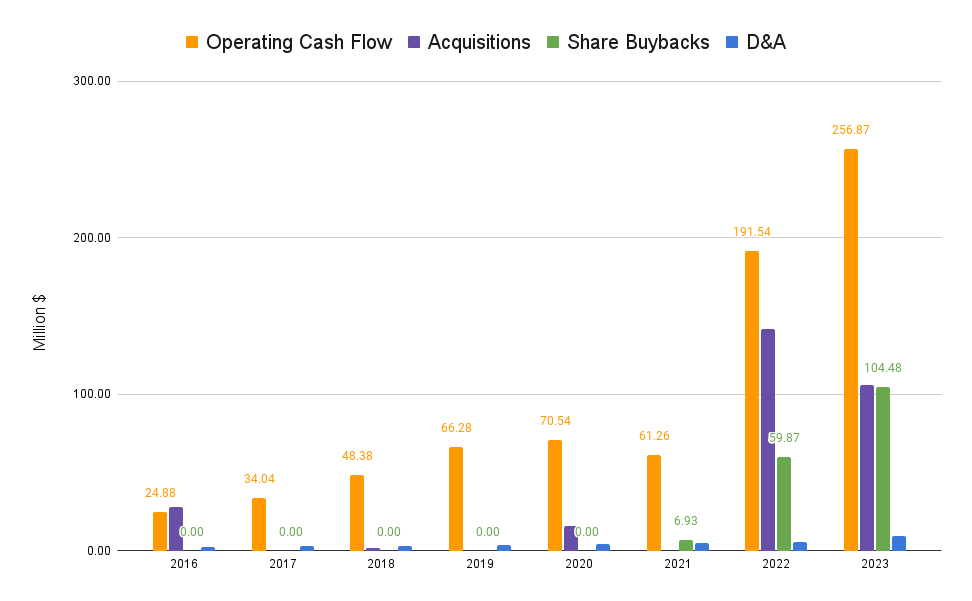

Capital Allocation

Cavco has never paid a dividend and has been mainly allocating its cash flows into acquisitions over the last ten years (~$300M), expanding its operations while eliminating competition on the way, and contributing to the consolidation in the manufactured housing industry.

In 2015 , Cavco acquired Chariot Eagle and Fairmont Homes for $28.1M, which contributed $88.3M in revenues (0.3x Revenue), in 2017 it acquired Lexington Homes for $1.6M, Destiny Homes in 2019 for $16M (0.4x Revenue), and more recently it acquired Commodore for $146M (0.43x Revenue) and Solitaire Homes for $105M (0.76x Revenue).

As the industry consolidates among fewer companies, it is becoming more difficult for Cavco to pursue significant acquisitions that will be accretive from a revenue and net income point of view, and it has shifted part of the capital into share buybacks, reducing the outstanding share count by 6% since late 2021.

{kind=link}

Source: Author (Data from Cavco Industries Financial Reports)

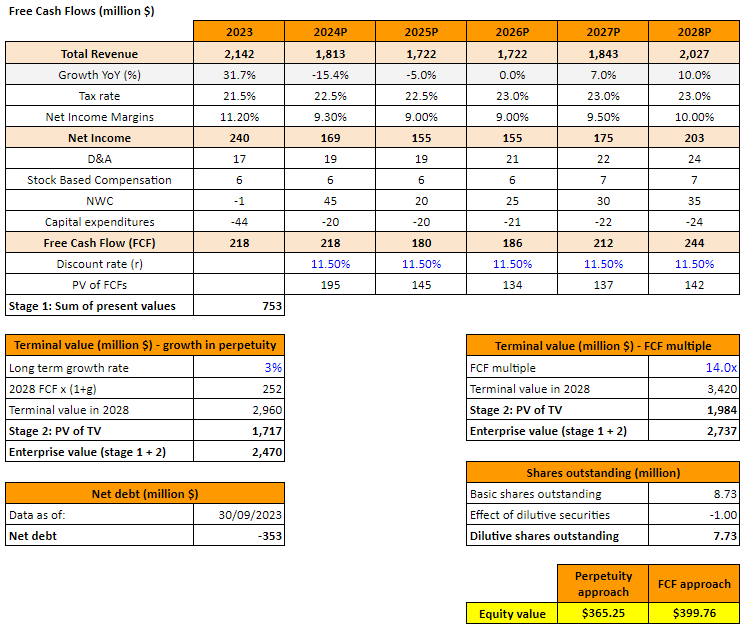

Expectations and Valuation

After four consecutive quarters of decreasing revenues, the backlog remained almost flat during the last quarter, suggesting capacity utilization might improve next year.

Given the sensitivity of Cavco to interest rates and financial availability, the forward expectations regarding interest rates could benefit the company, improving revenues after 2026.

As the dealer inventories get under control after piling up during 2022, in a base case scenario I expect Cavco's revenues to decrease by 5% in 2025 due to a deterioration in macroeconomic conditions, and to start improving from there moving forward.

These estimates are conservative when compared to the analyst consensus ($1.93B in revenues for FY2025) since I don't expect rates to decrease before the economic conditions deteriorate, delaying new house construction.

{kind=link}

Source: Author

After a period of normalization, as economic conditions improve and interest rates reduce to the 3% to 4% range, I expect Cavco's revenues to grow at 7% in FY2027. Since it will become harder over time to deploy capital into acquisitions, I forecast the share count to reduce by 3% yearly.

With a 3% long-term growth rate based on inflation and population growth, and assuming a 14x FCF multiple, which is significantly lower than its most recent average multiple, I consider Cavco to be undervalued and assign it a fair price of $382 , presenting a potential upside of 35%.

When looking at the current valuation, Cavco is trading at its low valuation range from a cash flow perspective, providing an opportunity to benefit from the short-term headwinds and invest at a discount in a company with a strong market share and above-average returns on capital.

{kind=link}

Source: Seeking Alpha

Risks

As a company operating in a cyclical business and despite being a long-term winner in its particular market, Cavco faces some risks that investors should monitor over time.

Weaker Macroeconomic Conditions

Despite my base case scenario being more pessimistic than the analyst consensus, I am assuming a moderate decrease in GDP for 2024 and unemployment increasing just to 4.5% from the current 3.9%.

If the macroeconomic conditions were to deteriorate at a faster pace, the short-term lag between the decrease in interest rates and lower consumption levels could cause Cavco's revenues to decrease for longer than expected.

Despite the current situation being far from the one we had in 2007 during the great financial crisis, it is important to note that Cavco's revenues decreased by 38% from 2007 through 2009.

Higher Delinquency Rates

Due to Cavco's $130M exposure to consumer and commercial loans, tougher macroeconomic conditions with higher unemployment could drive delinquency rates up.

During the last quarters, Cavco has tightened its credit standards, but in 2020 and 2021, 44% of the consumer loans were given to consumers with FICO scores under 680.

The company has 44% of the outstanding balance of the consumer loans portfolio concentrated in Texas and 13% in Florida.

Zoning Ordinances

Manufactured housing communities and individual manufactured homes are subject to local zoning ordinances and other local regulations. Communities apply zoning restrictions to manufactured housing that do not apply to traditional housing, which limits the number of manufactured homes that can be placed in a given community.

Some federal district courts held that restrictions on manufactured homes are justified by resident perceptions that manufactured homes are incompatible with traditional homes, threaten the tax base, or depreciate the market values of traditional housing.

The attempts of cities discriminating against manufactured housing, restricting community owners from replacing units when someone moves, or looking at banning them altogether, have caused a decrease over the last decades to the current all-time lows.

{kind=link}

Source: U.S. Census Bureau

Conclusion

I expect Cavco to continue gaining market share as the manufactured housing industry continues its consolidation process while enjoying long-term tailwinds such as the demographic structure and the current house undersupply.

Going forward, it will become tougher for Cavco to grow through acquisitions due to its currently high market share, but the management is allocating the capital wisely and is benefiting from the current undervaluation to buy back shares.

The short-term decrease in revenues and backlog might be providing investors with the opportunity to buy Cavco at a discount when compared to its fair price of $382, and as interest rates go down, I expect the company to continue providing above average-returns, assigning it a buy rating .

For further details see:

Cavco Industries: Benefiting From Long-Term Tailwinds