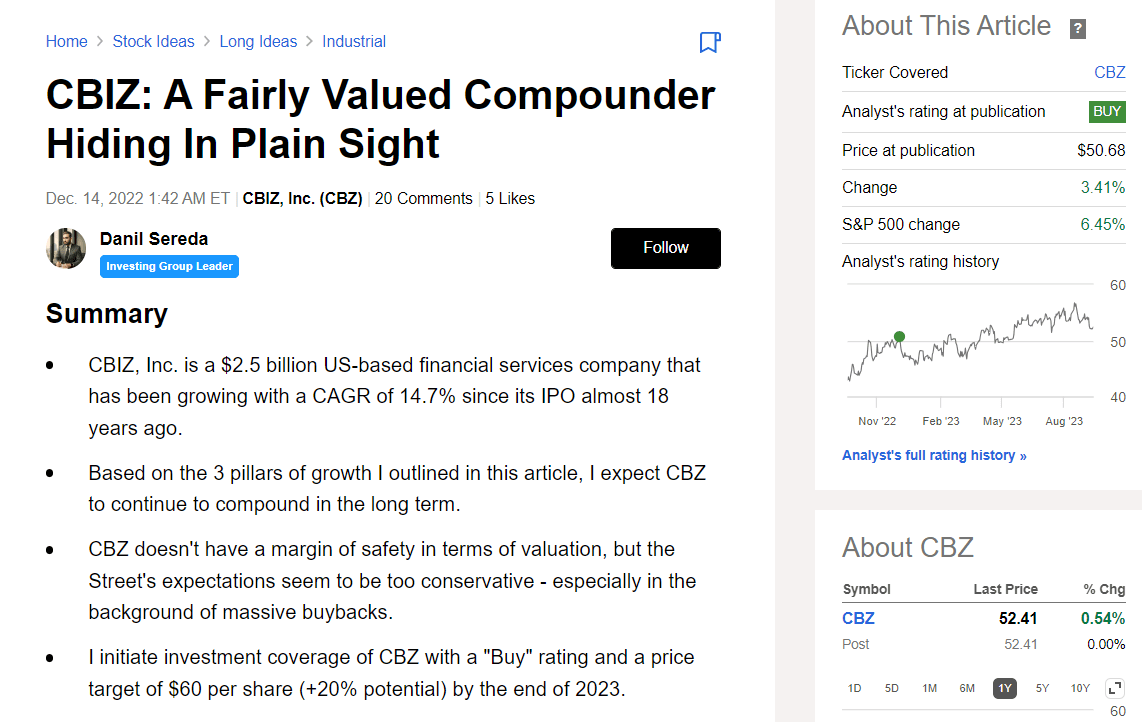

CBZ - CBIZ Stock Still Looks Fairly Valued (Rating Downgrade)

2023-09-28 09:55:41 ET

Summary

- CBIZ, Inc. has experienced challenges in its growth prospects, including contract delays and changes to tax filing timelines.

- Despite these challenges, the company saw growth in its Financial Services and Benefits and Insurance divisions.

- CBIZ's valuation appears fair, and there is no clear catalyst or margin of safety for investors, leading to my downgrade to a Hold rating this time around.

Introduction

Late last year, I wrote about CBIZ, Inc. ( CBZ ), a $2.6 billion market cap financial services company that has achieved double-digit growth since going public in the early 2000s. At the time, I assumed that the compounder's story would continue and that CBZ would post another stellar gain in 2023 due to the stability of its operations and strong buybacks. So far, however, my thesis is far from being realized.

{kind=link}

Today, I would like to reassess CBZ's growth prospects based on an analysis of recent financials, valuation, and market expectations.

The Company

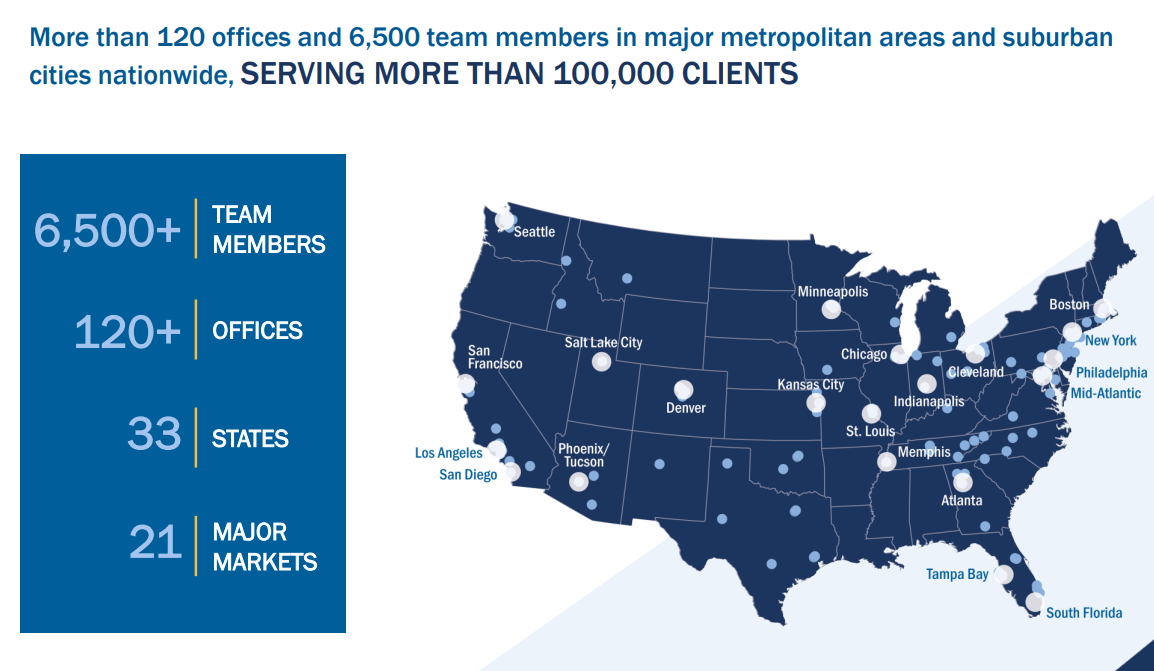

Incorporated in 1987 and headquartered in Cleveland, Ohio, CBIZ, Inc. provides financial, insurance, and advisory services in the United States and Canada. It primarily serves small and medium-sized businesses, as well as individuals, governmental entities, and not-for-profit enterprises, operating through 3 business segments:

- Financial Services [72% of total sales] offers accounting and tax, financial advisory, valuation, risk and advisory, and government healthcare consulting services.

- Benefits and Insurance Services [25%] provides employee benefits consulting, payroll/human capital management, property and casualty insurance, and retirement and investment services.

- National Practices [3%] offers information technology-managed networking, hardware, and healthcare consulting services.

{kind=link}

75% of CBIZ's recurring revenue comes from services like tax compliance, health benefits, consulting, insurance, payroll, retirement plans, and technology support. The remaining 25% is derived from compensation studies, executive search, financial consulting, litigation support, risk advisory, transaction advisory, and valuation services.

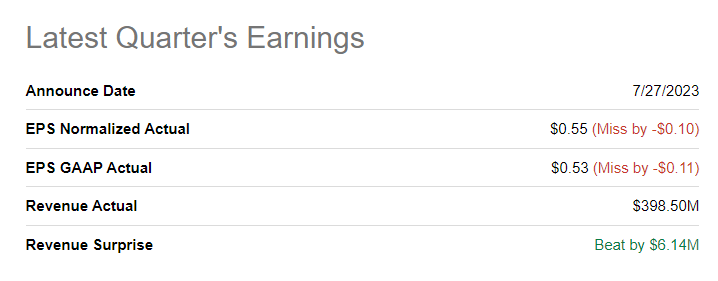

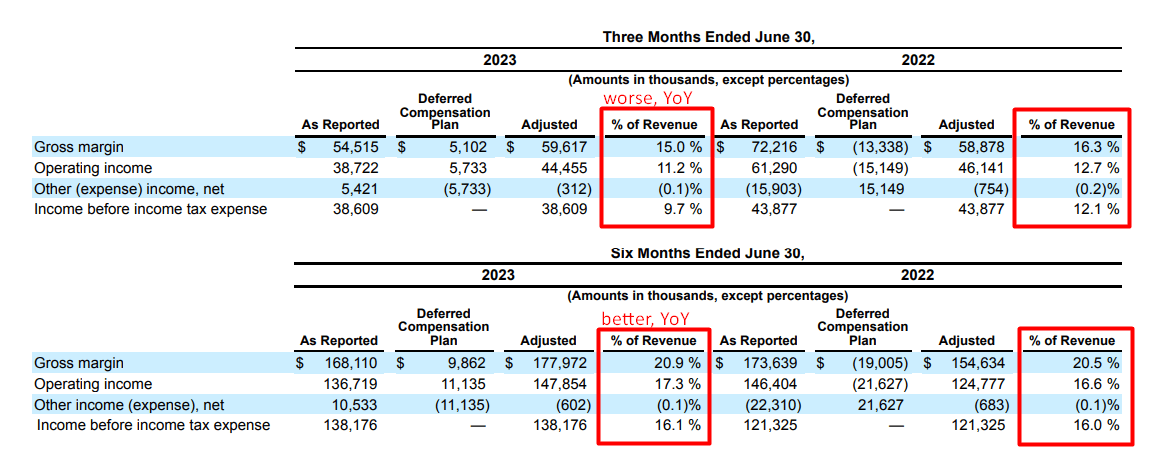

In Q2 FY2023, the company's overall performance was in line with expectations, except for two areas: Government Health Care consulting faced contract delays, and there were changes to tax filing timelines in California affecting the traditional accounting and tax business. These delays had an impact on earnings, mainly due to staff costs. So the firm wasn't able to cope with Wall Street consensus EPS expectations:

{kind=link}

Despite these challenges, the Financial Services division experienced 12.2% total revenue growth and 3.9% organic revenue growth. The Benefits and Insurance division also saw organic revenue growth of 4.5% YoY, with contributions from various service lines.

{kind=link}

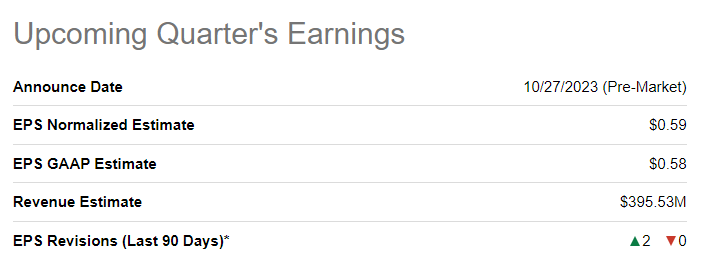

As far as I understood from the earnings call , the management expects growth in 2H FY2023, particularly in the Government Health Care consulting business. I think that's the reason why the analysts have revised their forecasts for Q3 upwards:

{kind=link}

Quarter-on-quarter, Q2 margins are down, but if we compare 2 half-years, we see improvement in GP margin:

{kind=link}

CBIZ continues to focus on strategic acquisitions and share repurchases, with a strong balance sheet and leverage of ~2x adjusted EBITDA.

The company raised its revenue guidance to improve by 11% [the mid-range] for FY2023 and affirmed its adjusted fully diluted EPS guidance to improve by ~12% over FY2022 results. The effective tax rate should amount to ~28%. The fully diluted weighted average share count is expected to be between 50.75 million shares for the year [in the mid-range].

Since 2018, the company has completed a slew of M&A deals, expanding its revenue base by $589.4 million [CAGR of +10.4%] and reducing shares outstanding by 11 million units (~$366.2 million or ~14% of current market cap). The EPS growth numbers cited in the guidance for FY2024 look impressive but fall short of the 5-year CAGR of 15.7% (on a TTM basis). While this is obviously not the most fantastic time for the industry, CBZ is likely to continue to hold its market cap based on management's outlook for shares outstanding at the end of FY2023.

I don't see any bright red signs in this compounder's story: CBZ's financial position looks solid, and the Q2 headwinds were most likely temporary, so Q3-Q4 should see a recovery. And despite the rather modest forecast numbers for FY2023, I expect FY2024 and beyond to be better.

The Valuation & Expectations

At first glance, CBZ stock seems quite expensive based on various multiples, one of which is the FCF yield of just 4.12%. But from a historical perspective, this low FCF yield is quite good - yes, the investor is not buying CBZ at rock bottom price now, but on the other hand, the current yield seems acceptable given the company's rapid growth over the past 5 years.

In the context of P/E ratios, CBZ stock currently trades at ~22 times next year's earnings, but the FY2024 EPS forecast implies a P/E of ~19.2x, according to Seeking Alpha Premium data . What does it mean? The market is putting on a multiple contraction, which is perfectly normal. However, this contraction doesn't give us much room for an upside. If we assume CBZ stock returns to its 5-year average P/E of ~21.4x, then the stock should be worth $50.9 at the end of 2023 [-2.8% from last close] and $58.2 [+11.1%] at the end of 2024.

CBZ's higher upside will only be explained by a possible increase in the multiple due to the continuation of a large share buyback program. That's quite real, but it doesn't provide a margin of safety for value investors if you consider yourself one.

The Verdict

Traders say you can’t “marry" a stock, you just have to “date" it. Don't get me wrong, but even though today's analysis shows that CBZ's current valuation is fair, I am still "married" to this company because it has given investors good growth since its IPO.

Only common sense keeps me from a "Buy" rating this time because, for a buy recommendation, there must be either a good catalyst or a margin of safety [both are better]. But I see neither in CBZ just yet.

So I downgrade CBZ to Hold and recommend investors possibly selling puts, or having a limit order and waiting for a lower price to initiate a position.

Thanks for reading!

For further details see:

CBIZ Stock Still Looks Fairly Valued (Rating Downgrade)