CBL - CBL & Associates: Finally A Compelling Deep Value Investment

2023-09-14 10:27:12 ET

Summary

- CBL & Associates Properties stock has struggled since the company emerged from bankruptcy protection two years ago.

- The company has a dramatically better balance sheet than it did before its 2020 bankruptcy filing and operating metrics appear to be stabilizing.

- CBL generates enough free cash flow to pay a 7%-yielding dividend while also organically reducing debt by $80-$90 million annually.

- CBL stock is deeply undervalued, trading at an implied cap rate of 14%. I estimate its intrinsic value to be around $40: nearly twice the current share price.

In early 2020, CBL & Associates Properties ( CBL ) was struggling under the weight of an excessive debt load and a secular shift away from low- and mid-tier malls that was pressuring NOI and EBITDA . The COVID-19 pandemic proved to be the last straw, forcing the mall operator to file for bankruptcy in November 2020.

The subsequent reorganization shored up CBL's balance sheet, but it hasn't made the stock any more loved. The new CBL shares traded for around $30 soon after the company emerged from bankruptcy in late 2021 but have been trading around $22 in recent months.

At this level, CBL stock looks very attractive for risk-tolerant investors. First, it trades at a rock-bottom valuation, with an implied cap rate of 14%. Second, CBL generates ample free cash flow, allowing it to steadily reduce its debt while also paying a meaningful dividend. Third, virtually all of the company's debt is now non-recourse, providing massive optionality to dump underperforming properties while keeping those that are successful. Finally, CBL will be able to tap into the "hidden" value of its land over time by selling excess parking lot space and even selling entire properties when they are no longer viable as enclosed malls.

Why CBL failed

To understand why CBL stock is so attractive today, it's important to first understand why it spiraled into bankruptcy previously.

Five years ago, CBL was a classic yield trap. The stock traded for around $5 and paid a quarterly dividend of $0.20 per share, putting its annual yield at around 16%. Many investors were lulled into thinking the dividend was safe because the payout ratio was below 50% based on the company's projected 2018 FFO of $1.70-$1.80 per share.

However, between normal maintenance CapEx and addressing a tidal wave of department store closures through redevelopment, CBL spent over $150 million (see pp. 71-73) on CapEx in 2018. That meant the company had less than $1 per share in funds available for distribution. That still covered the dividend (just barely), but it left very little excess cash flow for debt reduction.

However, CBL desperately needed to reduce its debt. Its leverage ratio (debt to NOI) exceeded 7X and NOI was declining at a high-single-digit rate, with no sign of improvement, due to tenant bankruptcies and store closures as many retailers exited lower-quality malls.

Sure enough, CBL cut its dividend in late 2018 and suspended it altogether in 2019 in order to pay down debt more quickly. Yet its leverage ratio continued to inch higher as NOI collapsed. Moreover, CBL had $1.375 billion of unsecured notes in its capital structure (see p. 20). The company's inability to continue servicing that debt ultimately drove it into bankruptcy. Shareholders were left with a minuscule recovery: for every 200 shares of old CBL stock (worth about $1,000 five years ago), investors got approximately 1.1 shares of new CBL stock (worth approximately $23 today).

This time is different

The headwinds facing low-quality malls haven't disappeared. If anything, they are intensifying as inflation pressures property-level operating costs and makes it less viable for tenants to run low-volume stores. But CBL is in a better position to manage those headwinds today.

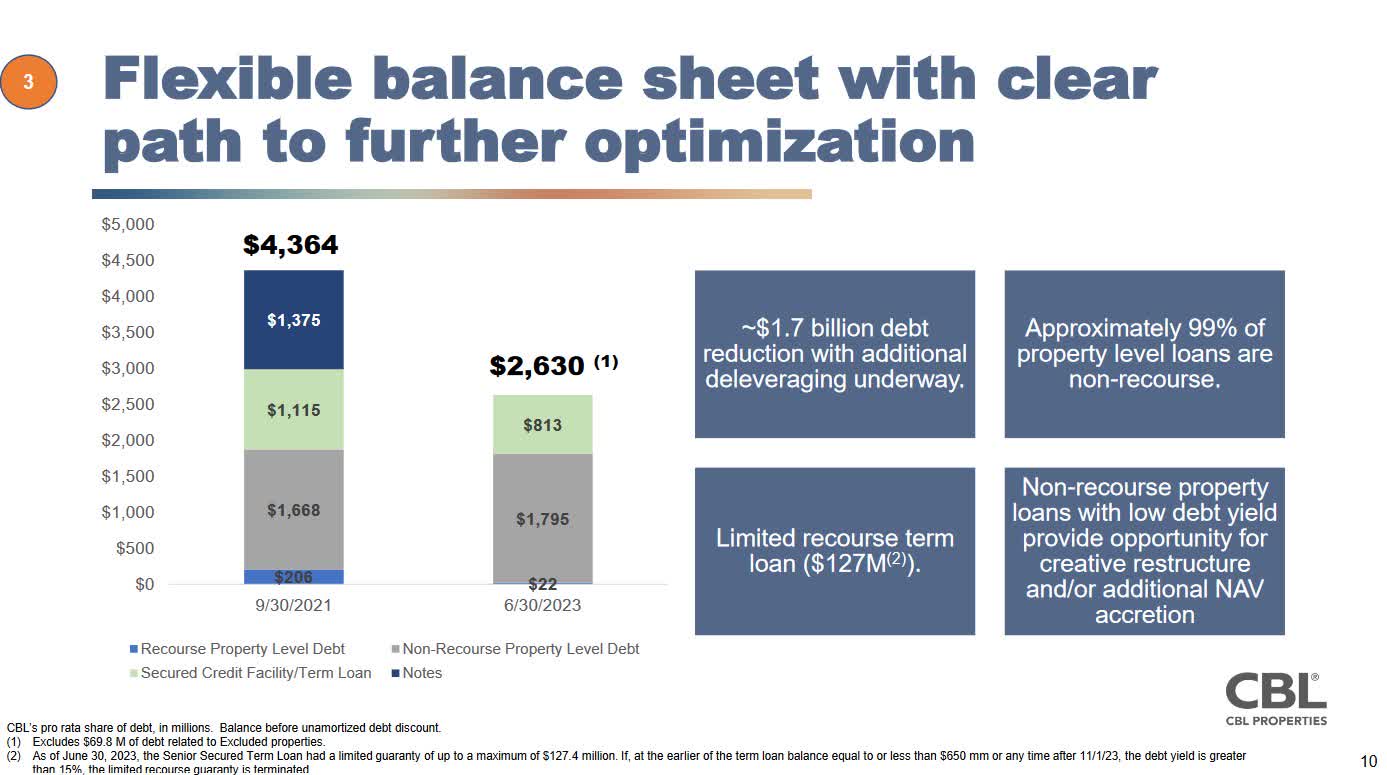

First, CBL has a much stronger balance sheet. Excluding mortgages on a pair of properties that are going back to the lenders, CBL ended last quarter with $2.63 billion of debt (including its share of JV debt), down from $4.26 billion at the end of 2019. Based on the company's projected 2023 NOI of $423 million-$440 million , leverage sits around 6x NOI today. CBL also had $280 million of unrestricted cash and investments as of last quarter.

{kind=link}

Source: CBL August 2023 Investor Presentation, slide 10.

Second, CBL has eliminated unsecured debt from its capital structure. Virtually all of its debt is now non-recourse. That creates optionality for CBL, as it effectively has a put option on its encumbered properties that it can exercise for underperforming or overleveraged assets. This capital structure essentially eliminates refinancing risk, too. The worst-case scenario is that CBL loses the underlying properties if it cannot extend or refinance particular loans: there's no threat to the corporate entity.

Third, key operating metrics look far more stable than they did prior to the pandemic. CBL has culled its portfolio of numerous underperforming properties, while the pace of retail bankruptcies has slowed considerably in recent years.

Notably, leasing spreads have turned positive in 2023 following years of declines. That will translate to easing pressure on NOI, or even modest organic growth. For 2023, CBL is calling for a 0.7% to 4.5% decline in same-center NOI. Most (if not all) of that decrease relates to one-time factors: lower percentage rent driven by moderating tenant sales volumes following an exceptionally strong 2022 and a normalization in bad debt expense.

Fourth, CBL is living within its means. The company expects to generate around $200 million of adjusted FFO in 2023 while reinvesting only a third of that amount. CBL's quarterly dividend of $0.375 per share costs about $48 million annually, leaving roughly $80-$90 million available for organic debt reduction. Asset sales may free up additional cash that CBL can use to pay down debt or return to shareholders via a $25 million share repurchase plan announced last month.

The valuation is way too low

As noted above, CBL stock currently trades at an implied cap rate of around 14%, with an enterprise value of just over $3 billion and projected 2023 same-center NOI between $423 million and $440 million. Despite the low quality of many of CBL's malls, that's way too cheap.

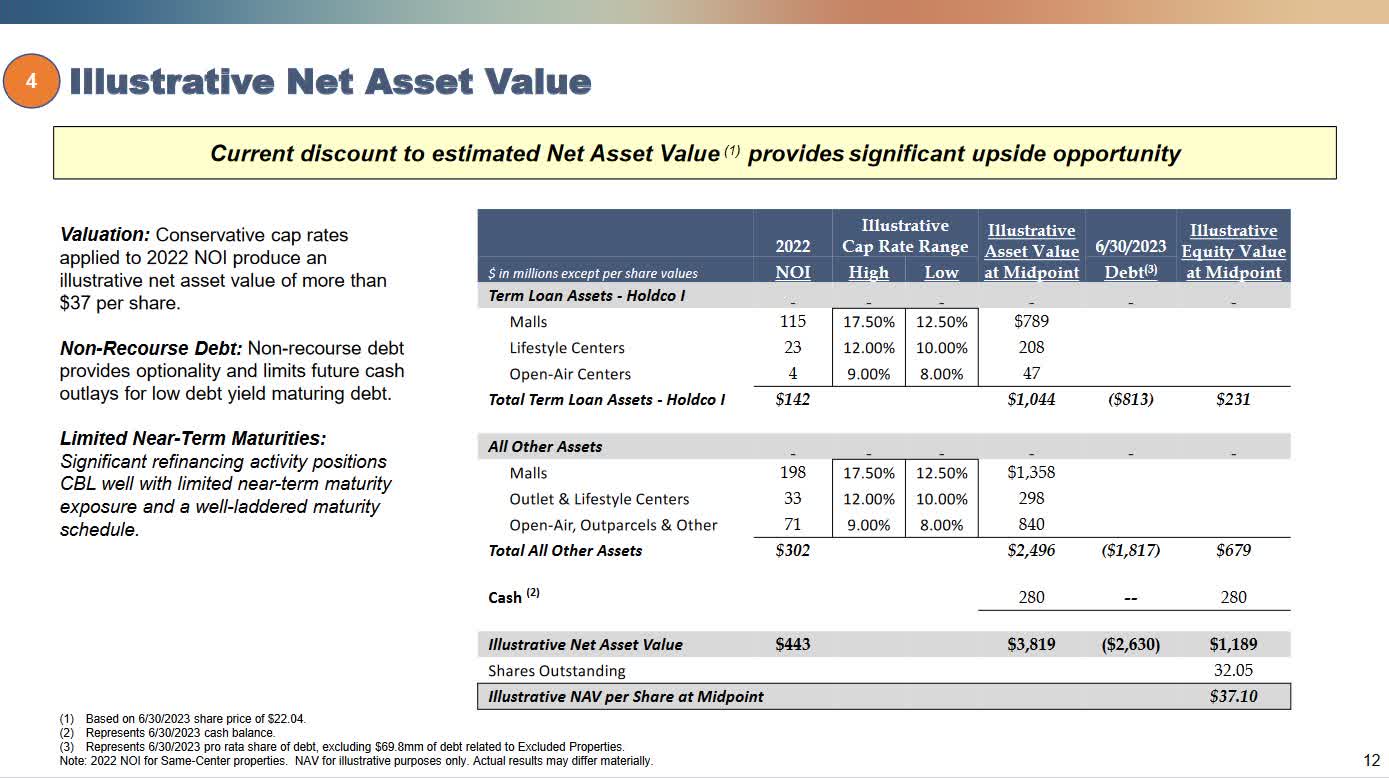

In a recent investor presentation, CBL estimated that the stock's intrinsic value would be around $37/share (see slide 12) using conservative cap rate assumptions. Indeed, the midpoints of the ranges (15% for malls, 11% for outlet and lifestyle centers, and 8.5% for outparcels and open-air centers) seem extremely conservative, particularly given the embedded optionality of CBL's non-recourse debt.

{kind=link}

Source: CBL August 2023 Investor Presentation, slide 12.

Looking at CBL's valuation from another perspective, the company's market cap is approximately $680 million today. Net of unrestricted cash and investments on the balance sheet, it's just $400 million.

For that $400 million, investors "own" the equity value of CBL's encumbered properties, along with 15 unencumbered malls and a handful of smaller unencumbered properties. Collectively, the encumbered properties are on track to generate roughly $70 million of cash flow this year after CapEx and debt amortization, with NOI roughly in line with 2022. The equity value of these properties alone almost certainly exceeds $400 million due to their strong cash flow, stable NOI, and the optionality inherent in property-level mortgages.

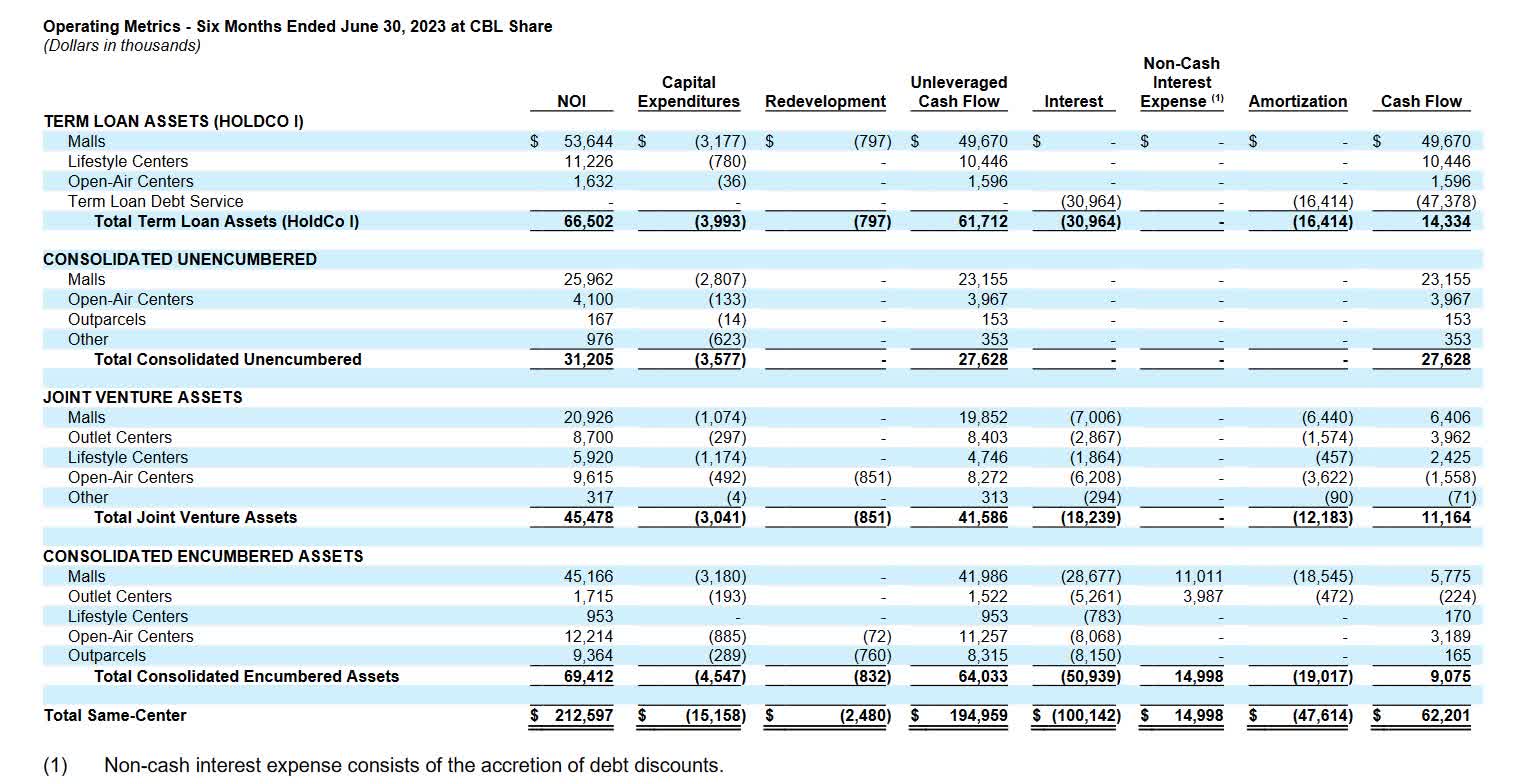

Meanwhile, CBL's unencumbered properties generated $31.2 million of NOI and $27.6 million of cash flow (after CapEx) in the first half of 2023. This category primarily consists of CBL's least successful malls. NOI for these properties declined 15% year over year in the first half of the year.

{kind=link}

Source: CBL Q2 2023 Supplemental, p. 25.

Investors should expect NOI to continue declining for this portfolio. Even so, these properties should generate at least $200 million of cash flow over the next five years. Moreover, their terminal value isn't zero. Regional malls typically occupy dozens of acres of land near prominent intersections. That gives them substantial potential for redevelopment ranging from open-air retail to industrial uses . As a result, I would estimate the present value of these assets at around $300 million, with potential upside to as much as $400 million.

In short, CBL's net asset value is likely at least twice the company's $400 million ex-cash market cap. And if interest rates moderate over the next few years, mid-tier mall cap rates could improve significantly (particularly if NOI for those properties continues to stabilize), adding to the upside potential.

What are the risks?

With an ample cash cushion and virtually all debt being non-recourse, CBL stock is dramatically less risky than it was five years ago. Even if the mall industry takes another turn for the worse, CBL has tremendous optionality to continue squeezing cash out of its assets by renegotiating or selectively defaulting on mortgages, tapping into the underlying land value, etc.

The biggest risk is another wave of store closings and bankruptcies among department stores. CBL has particularly high exposure to J.C. Penney. While J.C. Penney cut its debt load after filing for bankruptcy in 2020, that isn't an absolute guarantee against a second bankruptcy if the company continues to lose market share to better-capitalized competitors. Losing multiple anchor tenants can send a mall into a death spiral by depressing shopper traffic.

Rising interest rates also pose a modest risk to CBL. The company has over $1 billion of variable-rate debt, and many of its fixed-rate mortgages will need to be refinanced within the next three years. Higher interest expense would sap cash flow. That said, interest rate risk is biased to the downside at this point. The yield curve indicates that two years from now, short-term rates are likely to be lower than today's level, not higher.

A great risk-return proposition

For CBL's $400 million ex-cash market cap, investors get 15 low-quality but cash-generating malls, several other unencumbered assets, a substantial cash stream from dozens of encumbered properties, and optionality around retaining or discarding those mortgaged assets, some of which are quite attractive.

The chance that this pool of unencumbered assets, cash flow from encumbered assets, and optionality is worth less than $400 million is very small. My ballpark valuation is around $1 billion, which implies a fair value for CBL stock of around $40: slightly above management's conservative estimate of $37.

There aren't clear near-term catalysts to close the gap between the share price and NAV, other than the possibility of a significant decrease in short-term interest rates. CBL's $25 million buyback might help on the margin, but it's too small to move the needle in a meaningful way.

Over time, though, as CBL continues to reduce its debt and exit underperforming properties (while also hopefully maintaining flat to slightly positive same-center NOI), investors are likely to grow more comfortable with the business. That should translate to a higher valuation for CBL stock. In the meantime, investors can enjoy a 7% yield as they wait for the market to catch on to CBL's true value.

For further details see:

CBL & Associates: Finally A Compelling Deep Value Investment