NDAQ - Cboe Global Markets: A Defensive Blue Chip Buy

2023-10-30 06:12:16 ET

Summary

- Utilities and consumer staples, typically viewed as defensive sectors, have underperformed during the recent market sell-off.

- Cboe Global Markets is an exchange operator and has delivered strong historical results for shareholders.

- CBOE enjoys a counter cyclical business as trading volume tends to rise with market uncertainty.

- I am initiating CBOE with a buy rating as I view the stock as an attractive defensive investment at current levels.

The recent market environment has proved especially challenging for a lot of stocks typically viewed as defensive. From the YTD high reached on July 27, 2023, the S&P 500 ETF Trust ( SPY ) has delivered a total return of -8.9%. Typically during market sell-offs, two sectors that tend to outperform due to their defensive nature are utilities and consumer staples. However, during this market sell-off that has not been the case.

Utilities, which can be proxied with the Utilities Select Sector SPDR ETF ( XLU ) have dropped nearly 12%. This move lower was driven by the sharp increase in interest rates as the sector tends to be highly sensitive to interest rate moves given low growth prospects and generally high yields.

Another sector typically thought to be among the most defensive in the stock market is Consumer Staples, which can be proxied with the Consumer Staples Select Sector SPDR ETF ( XLP ). The sector has dropped by 11% during the broad market sell-off. The move was driven by fears that new weight loss drugs such as Ozempic, Wegovy, and Mounjaro will lead to changes in consumer behavior which may result in less demand for certain products sold by the likes of companies such as Coca-Cola ( KO ), Hershey ( HSY ), and many others. Moreover, the sector tends to be a slow growth and high yield sector which means it is also susceptible to interest rate risk.

Given the challenges faced by these traditional defensive sectors, investors with limited risk tolerance should look to diversify into other defensive equities and Cboe Global Markets ( CBOE ), which surged ~14% during the recent market sell-off, represents an excellent opportunity to do just that.

CBOE Is A Defensive Mature Business

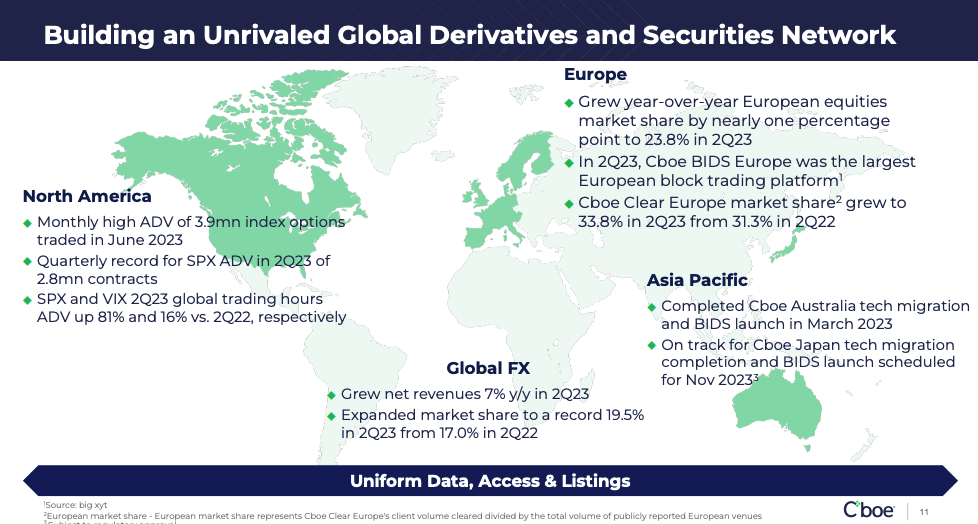

CBOE is an exchange operator with options across North America, Europe, and Asia Pacific. CBOE operates across various asset classes including equities, derivatives, FX, and digital assets.

CBOE trades its roots back to 1973 when it became the first marketplace for trading listed options. In 1983, CBOE created the first options based on the S&P 500. In 1993, CBOE created the CBOE Volatility Index ( VIX ) and in 2004 VIX futures trading was launched.

CBOE has diversified into other products through acquisitions, including most notably its 2017 acquisition of Bats Global Markets. However, options remain CBOE's biggest strength with the options business accounting for just over 51% of revenue. CBOE is the largest options exchange and has 33.2% market share in the listed options market up from 30.8% in 2021.

The North American Equities segment accounts for ~19.4% of revenue followed by the Europe and Asia Pacific segment which accounts for ~10% of revenue. CBOE has ~13.6% market share in U.S. listed equities and 23.5% share in European equities. CBOE's Futures business accounts for ~6% of revenue and the Global FX segment accounts for ~4% of revenue.

CBOE competes globally with other leading exchanges but its most direct competitors are Nasdaq ( NDAQ ) and Intercontinental Exchange ( ICE ). Both NDAQ are ICE are leading competitors to CBOE in both the options space and equities space. NDAQ is the second largest options exchange accounting for ~28% of the market while ICE, through its ownership of NYSE, accounts for ~16% of listed options trading.

CBOE is a defensive business because trading volumes tend to rise during times of economic stress. Higher trading volumes results in more revenue for CBOE. Moreover, CBOE's propriety VIX related products including VIX options and VIX futures tends to experience heightened trading as volatility levels increase.

{kind=link}

Historical Beta Analysis

As shown by the chart below, CBOE's historical 3yr trailing beta to the S&P 500 has averaged 0.53 and thus the stock, on average, has shown defensive properties we would expect based on the business itself. The relatively low historical beta affirms that the business itself is less cyclical than most other businesses. Additionally, CBOE's realized beta has rarely exceeded 0.8x suggesting CBOE tends to act as a defensive stock across most market environments.

History of Delivering Strong Shareholder Results

As shown by the chart below, since becoming a public company CBOE has delivered a total return of ~525% compared to a return of ~373% delivered by the S&P 500 during the same time period. CBOE has also performed well vs competitors and has outperformed both ICE and CME. The only major exchange that has outperformed CBOE in terms of delivering shareholder results has been NDAQ.

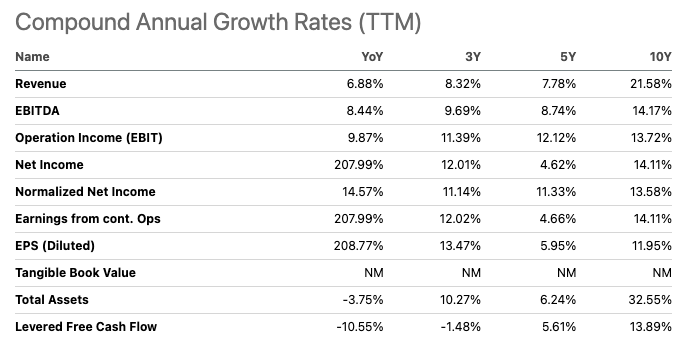

CBOE has been able to deliver strong shareholder returns due to strong financial performance. Over the past 10 years, CBOE has grown revenue at a 21.5% CAGR and net income at 12% CAGR. Additionally, CBOE has a strong record of returning excess cash to shareholders through dividends and share repurchases.

{kind=link}

Competitive Advantage

CBOE's competitive advantage is driven by its proprietary products which include SPX options as well as VIX options and futures. CBOE introduced the VIX and VIX options and thus is the exclusive trading venue for these products. Additionally, CBOE has entered into a licensing agreement with S&P Global ( SPGI ) which gives CBOE the exclusive right to offer exchange-listed options contracts in the U.S. on the S&P 500 index, Dow Jones Industrial Average, and certain other indexes managed by S&P. CBOE's license with S&P runs through December 31, 2033 with the exclusive right to trade options on the S&P 500 running through December 31, 2032.

In 2022, ~60.7% of net transaction and clearing fees were generated by futures and index options, the overwhelming majority of which were generated by exclusively listed products such as SPX options and VIX options.

Growth Opportunities

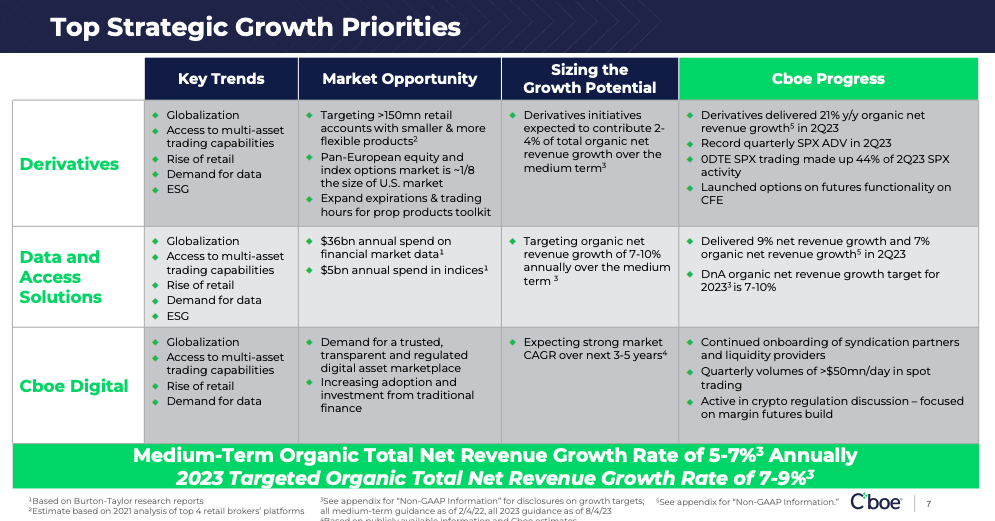

CBOE enjoys multiple potential growth drivers including increased trading volume, increased retail trading of options and micro futures, new products, increased demand for financial data, and increased trading hours of existing products.

CBOE believes it can grow net revenue by 5-7% per year over the medium-term and I believe this goal is easily achievable. Wall Street analysts agree and consensus estimates currently call for CBOE to grow revenues and EPS by mid single digits over the next few years.

I believe CBOE guidance is conservative and thus believe the company is likely to grow even faster than current estimates.

{kind=link}

Valuation Analysis

Seeking Alpha quant scores give CBOE a valuation grade of F. I disagree with this characterization as I believe CBOE deserves its premium valuation.

CBOE is currently trading at 20.6x 2024 estimated earnings. Comparably, the S&P 500 trades at 17x 2024 estimated earnings.

Given that I expect both the S&P 500 and CBOE to be able to grow long-term earnings by high-single digits, on the surface the S&P 500 appears more attractive. However, I believe CBOE deserves a premium valuation due to the counter cyclical nature of its business (exhibited by the 0.53x historical beta.)

Defensive below market growth stocks generally trade at a premium to the S&P 500. For example, Coca-Cola trades at 20.6x 2024 earnings and Procter & Gamble ( PG ) trades at 22.8x 2024 earnings. Both KO and PG are expected to grow earnings at mid-single digits which is in line with the consensus growth estimate for CBOE.

Given that I expect CBOE to grow earnings by high-single digits, I believe it is attractive relative to other traditional defensive stocks.

CBOE trades roughly in-line with its exchange peers ICE, CME, and NDAQ. Similarly, CBOE is trading roughly in-line with its own historical valuation history.

Q3 2023 Earnings Preview

CBOE is set to report Q3 2023 earnings on November 3, 2023. Consensus estimates call for the company to report EPS of $1.84 per share which represents a year-over-year increase of 5.8%. Revenues are expected to be $478.8 million which represents an 8.2% increase on a year-over-year basis. The consensus EPS estimate has been revised higher by 2.06% over the last 30 days to current levels. Thus, expectations are high and I expect CBOE to deliver strong results.

Risks To My View

In my opinion, the biggest risk to CBOE as a long-term investment is the potential that CBOE is unable to maintain exclusive trading of S&P 500 options and VIX options.

While CBOE has the exclusive rights to trading of S&P 500 options through December 2032, there is no guarantee that this contract will be extended in the future. However, there is no reason to believe that the contract will not be renewed as the relationship between S&P and CBOE has only deepened over the years. The contract was last renewed in 2013.

Another way that CBOE could lose its exclusive rights to trading of S&P 500 as well as VIX options is if there is regulatory reform. Notably, the EU has recently adopted legislation which requires benchmarks used to value a financial instrument in the EU to be made available on a non-discriminatory basis to all EU trading venues. If such regulation were to take hold in the U.S. then CBOE would see challenges to its role as the exclusive provider of S&P 500 options and VIX options trading. While it is difficult to predict regulatory change, it is a risk that investors must actively monitor.

Conclusion

CBOE's business as an exchange operator is counter cyclical as trading volumes tend to rise during times of economic stress. The company is the market leader in exchange traded options and enjoys exclusive rights to trading in a number of key products such S&P 500 options, VIX futures, and VIX options.

CBOE has delivered strong results since becoming a public company and has significantly outperformed the S&P 500. In addition to having a counter cyclical business, CBOE also enjoys significant growth opportunities.

While CBOE is currently trading at a modest premium to the S&P 500, it is trading in line with high quality defensive stocks which tend to grow at slower rates.

The biggest long-term risk to my view is that CBOE is unable to maintain exclusive rights to trading in its key products such as S&P 500 options, VIX futures, and VIX options. While the relationship with S&P is strong and runs through 2032 for S&P 500 options, investors should monitor any signal that this license may not be renewed. While the rights to the VIX index are owned by CBOE, the company still faces risk of losing exclusivity related to that product in the event of U.S. regulatory reform which requires products to be traded on multiple exchanges.

Overall, CBOE represents an attractive defensive Blue Chip stock in a stock market where many traditional defensive stocks have lost their defensive properties. As such, I view CBOE as a very attractive building block to any defensive equity portfolio right now.

For further details see:

Cboe Global Markets: A Defensive Blue Chip Buy