CCD - CCD: An 11% Yield Paid Monthly From Convertibles

2023-03-28 03:58:38 ET

Summary

- CCD is paying out an 11.3% yield monthly from a highly diversified portfolio built around convertible bonds and preferreds.

- The CEF has kept this distribution stable since 2021 when it was raised 16.8% from its prior payout.

- Return of capital has been employed but not since before the pandemic when it drove 46% of distributions for a nine-month period.

Calamos Dynamic Convertible and Income Fund ( CCD ) last paid a monthly distribution of $0.195 per share , in line with its prior payout, for an 11.3% yield. The closed-end fund invests in convertible and high-yield securities, an investment approach that allows CCD to target both income and growth. Convertible bonds and preferreds make up the bulk of the portfolio which held just under 600 positions as of the end of the fourth quarter of 2022.

Calamos Dynamic Convertible and Income Fund

{kind=link}

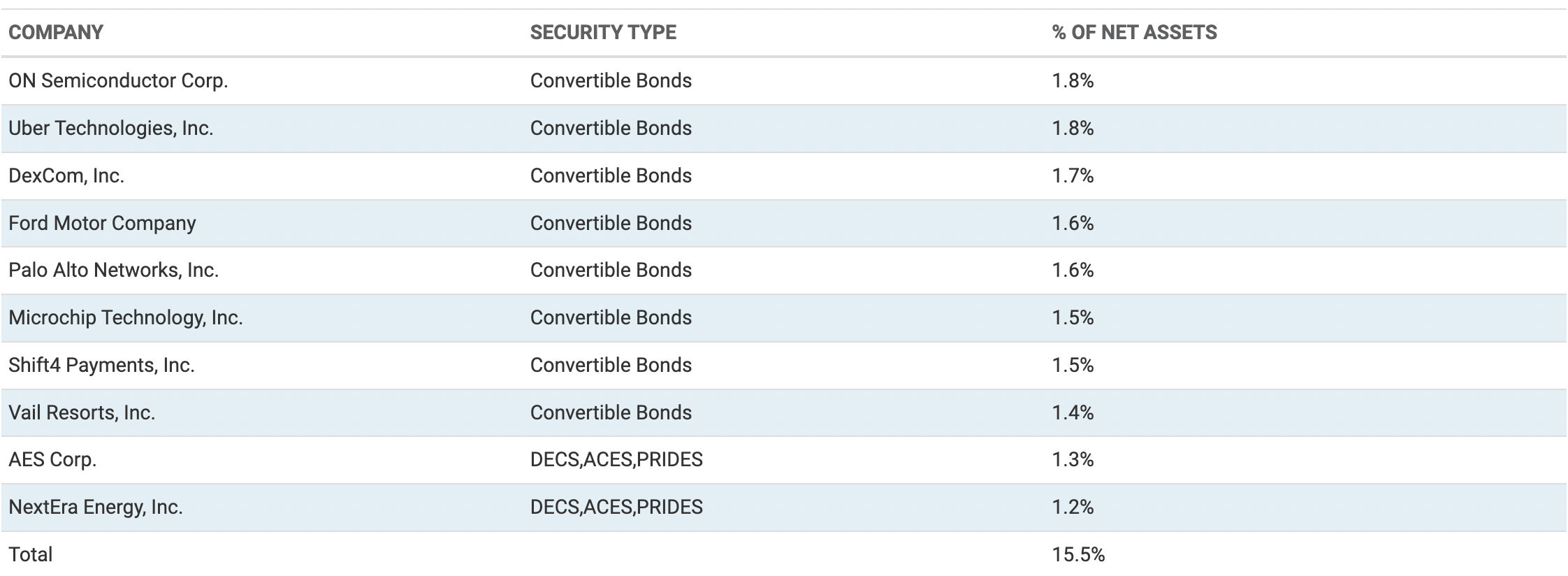

These securities can be converted into a certain number of common shares in the underlying company to allow CCD to provide upside participation in bullish equity markets with less overall downside exposure. ON Semiconductor ( ON ), Uber ( UBER ), DexCom ( DXCM ), Ford ( F ), and Palo Alto Networks ( PANW ) formed its top five positions with an aggregate of 8.5% of the portfolio as of the end of February 2023. Hence, should CCD play a role within a broader income portfolio? It depends. There's a lot to like with the monthly per share payouts staying consistent at $0.195 since 2021 when it was raised from $0.1670 .

Critically, the CEF broadly passes two of the three factors to be considered when making a CEF investment decision. The portfolio, the health of distributions, and positioning in the year ahead. Chasing the 11% yield in the face of relenting but falling inflation is the prize but if this can be gained with lower risk elsewhere then the investment case for CCD would be weakened.

Convertible Securities Against Market Volatility

Whilst it's expected for CCD to somewhat mirror the S&P 500 ( SPY ), the performance dichotomy between both has been extremely small. This is important as CCD charges a 2.51% expense ratio , with leverage fees at 1.4% constituting the bulk of this. CCD is down 10.8% on a total return basis over the last year versus a loss of 11.6% for SPY. Over the last three years and CCD is up just under 70% versus 64% for SPY. Volatility is intrinsic here with the underlying price movements of the convertible securities driven by the dynamic between the ratio of shares at conversion and common share price movements. The $848 million portfolio has somewhat of a high turnover at 42% with leverage at 37% of the portfolio also used to enhance returns.

Calamos Dynamic Convertible and Income Fund

{kind=link}

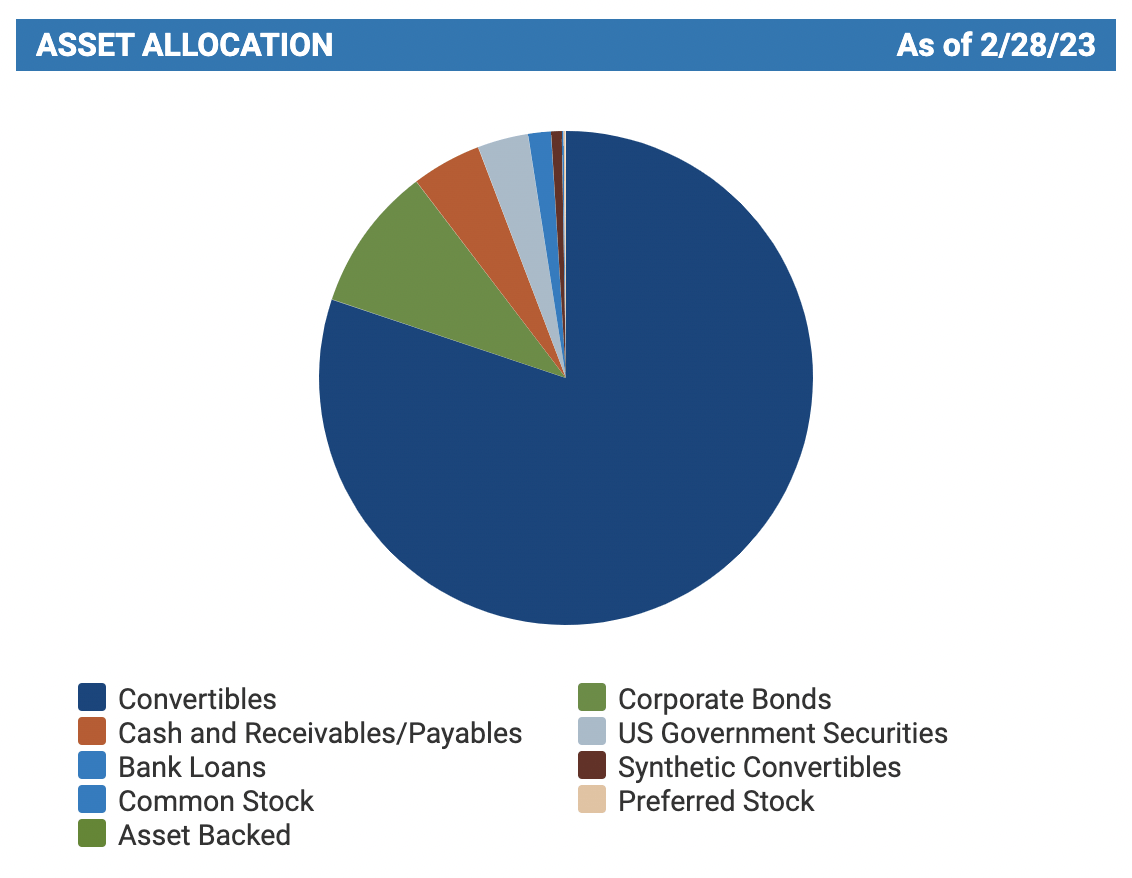

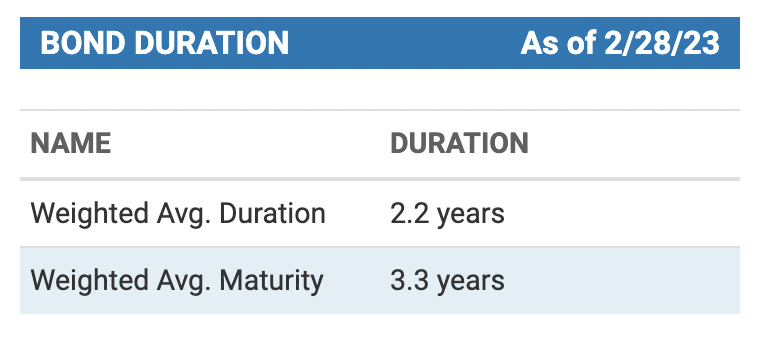

Convertibles constitute 80% of the portfolio with corporate bonds at 9.5% and cash at 4.56% forming the other two largest positions in the CEF. CCD's weighted average duration of 2.2 years is healthy against a still-rising Fed funds rate environment. Essentially, the CEF should be able to more actively recycle these to higher-yielding securities when they mature versus sitting on lower yields for longer. Bonds are positive duration assets which means their overall utility moves inversely to interest rates. A less than 3-year timeframe to maturity represents a medium-term holding period that would allow any unrealized losses in their broader bond portfolio to be removed when bonds mature at par.

Calamos Dynamic Convertible and Income Fund

{kind=link}

The Premium To NAV And Expected 2023 Returns

CCD operates on a term limit structure which will see shareholders elect collectively whether or not to liquidate the fund at NAV in 2030. The impact of this is usually to reduce the discount and premium to NAV the CEF trades, especially as its nears liquidation. There are some perpetual fixed-income CEFs like PIMCO's famous PTY which once traded on premiums to NAV as material as 40% in the era before rates started to rise.

CCD currently roughly trades on an 8.8% premium to NAV, the highest level in over 3 years. With the shares still experiencing weakness, the premium can be attributed to a fall in NAV from what's been a more than year-long bear market. Ford is down 27% over the last year with Uber and DexCom down 11% and 6% respectively. Hence, whilst it's the income that matters and price movements could get tuned out over the longer term by consistent DRIPing, buying now could see some losses if the premium to NAV reverts back to zero.

I like that CCD has not had to lean on return of capital for its distributions since the start of the pandemic with the bulk of these being driven by long-term capital gains. The CEF did use ROC for nine straight months to power 46% of its distributions in the year before the pandemic.

{kind=link}

But October 2019 was the last time ROC was used by the CEF. It would be hard to see the usefulness of paying a 2.51% expense ratio for your capital to be returned to you. Zero ROC since 2019 increases the investability of the CEF against its elevated premium and expected macroeconomic headwinds in 2023. I'm neutral on taking a position and this is a hold.

For further details see:

CCD: An 11% Yield Paid Monthly From Convertibles