ON - CCD: This Convertible Fund Is Best Avoided For Now

Summary

- Convertible securities are a very nice asset class because they overcome most of the problems associated with fixed-income investments.

- CCD is one of the only closed-end funds that are almost exclusively invested in convertible securities.

- The fund has generally underperformed the index, although it does have a substantially higher yield.

- The fund appears to be struggling to maintain its distribution and will almost certainly be forced to cut unless the market turns around in 2023.

- The fund is trading for an incredibly high and unjustified price.

One of the biggest problems facing Americans today is the incredibly high inflation rate that has been plaguing the economy over the past year or two. This situation has so far resulted in nineteen straight months of negative real income growth and forced numerous people to take on second jobs or enter into the gig economy just to obtain the extra money that they need to finance their lifestyles. Fortunately, as investors, we have other methods that we can use to obtain the extra money that we need to pay our bills and maintain our lifestyles. One of the best of these methods is to purchase shares of a closed-end fund that specializes in the generation of income. This is because these funds provide easy access to a professionally-managed diversified portfolio that can in most cases produce higher yields than any of the underlying assets.

Unfortunately, one of the biggest problems with most income-focused funds is that they have extremely limited potential for capital gains. This is because most of them purchase fixed-income securities or use certain options strategies that end up capping the potential gains in favor of income. A potential solution to this can be found with convertible securities. These are a somewhat rare and underfollowed type of market asset but they combine the best of both fixed-income securities and stocks. This is because they are basically fixed-income securities that can be converted into the common equity of the issuing company under certain conditions. This can be especially nice when the security is issued by a start-up company that winds up making it big one day, like Tesla ( TSLA ) ten years ago. In fact, these companies are the primary issuer of convertible securities.

Fortunately, there are a few closed-end funds that focus on investing in convertible securities, which could make these ideal vehicles for investors looking for an income boost. In this article, we will discuss the Calamos Dynamic Convertible and Income Fund ( CCD ), which currently yields a very impressive 11.13%. I have discussed this fund before but well over a year has passed since that time so obviously, a number of things have changed. This article will therefore focus specifically on those changes as well as provide an updated analysis of the fund’s finances in order to determine if this fund could be a good addition to your portfolio today.

About The Fund

According to the fund’s webpage , the Calamos Dynamic Convertible and Income Fund has the stated objective of providing its investors with a high level of total return through both current income and capital appreciation. This is hardly surprising considering that the fund is aiming to achieve this objective by investing in a combination of high-yielding fixed-income securities and especially convertibles. As mentioned in the introduction, a convertible security is a fixed-income security (such as a bond or a preferred stock) that can be converted into common equity under certain circumstances. The fact that they have this conversion feature means that the fixed-income yield is usually a bit less than a fixed-income security issued by the same company that does not have this feature. Thus, they can be a more affordable way for a start-up or financially-troubled company to obtain financing. They can provide an enormous return upon conversion to the common stock though if the company’s stock ends up being a multi-bagger or something like that. Thus, these securities offer a way to obtain the high potential returns associated with equity while still enjoying much of the safe income provided by preferred stock and bonds.

The fund claims that it invests at least 50% of its assets into convertible securities. This is much higher than other convertible closed-end funds like the AllianzGI Equity & Convertible Income Fund ( NIE ), which I discussed in a recent article . Currently, the Calamos Dynamic Convertible and Income Fund is substantially above that 50% threshold, though:

Calamos Investments

As we can see here, the fund’s portfolio currently consists of 81.60% convertible securities. This is a bit above the 75.15% convertible weighting that the fund had the last time that we analyzed it and it should be very appealing to pretty much any investor. As already mentioned, convertibles work very well for those seeking income because they do not have to give up the potential upside of the common stock in order to obtain that income. The fund will be passing that benefit through to the investors as it can see very attractive profits when it converts the security.

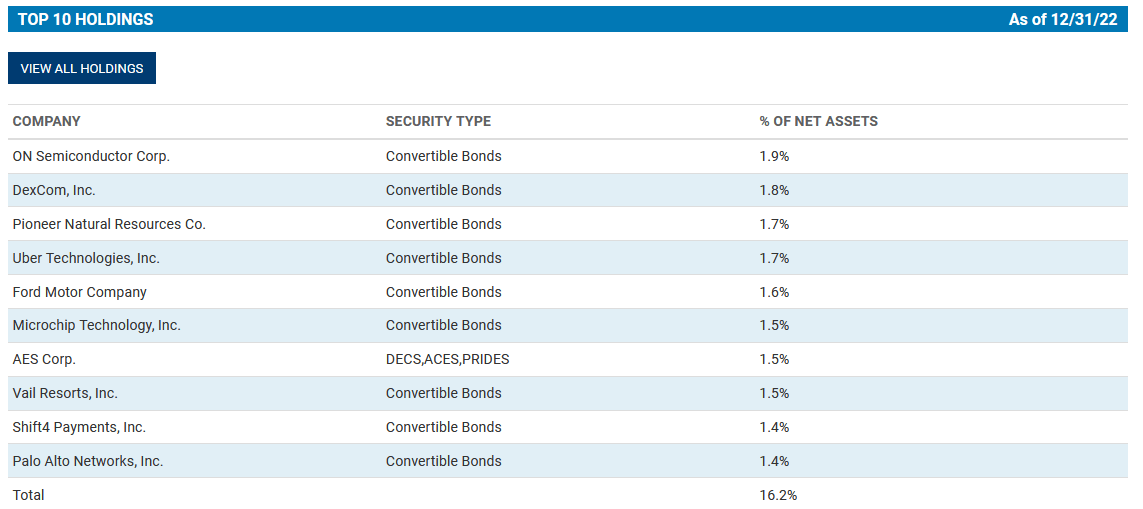

There are quite a few companies in the fund’s portfolio that may be attractive as well. Here are the largest positions:

{kind=link}

We see a number of technology companies here that delivered rather promising initial public offerings, such as Uber Technologies ( UBER ). Unfortunately, the company’s market performance has been far less noteworthy since then as it is actually down quite a bit from its debut price. Palo Alto Networks ( PANW ), on the other hand, has had a much better performance with the stock being up 157.31% over the past five years. ON Semiconductor ( ON ) has had a similar performance as its common stock has climbed 149.48% over the trailing five-year period. The fund obviously holds bonds issued by these companies but, depending on the conversion price, it may be able to convert them to common stock and walk away with a huge gain.

One thing that we notice here is that many of the fund’s largest positions are very different than the last time that we looked at the fund. In fact, only Uber Technologies, Microchip Technology ( MCHP ), Vail Resorts ( MTN ), and Shift4 Payments ( FOUR ) were on the largest holdings list both in July 2021 and today. This may lead one to expect that the fund would have a very high annual turnover. This is actually not the case as the Calamos Dynamic Convertible and Income Fund only has a 42.00% annual turnover, which is fairly low for an equity fund and middle-of-the-road for a fixed-income fund. This is something that is rather nice to see because of the fact that it costs money to trade assets in the market. These costs are billed to the fund’s shareholders, which creates an overall drag on the fund’s performance. This is because management must generate sufficient returns to overcome these added trading expenses and still provide a return that is acceptable to the investors. Unfortunately, most actively-managed funds fall short here and fail to beat a comparable index fund.

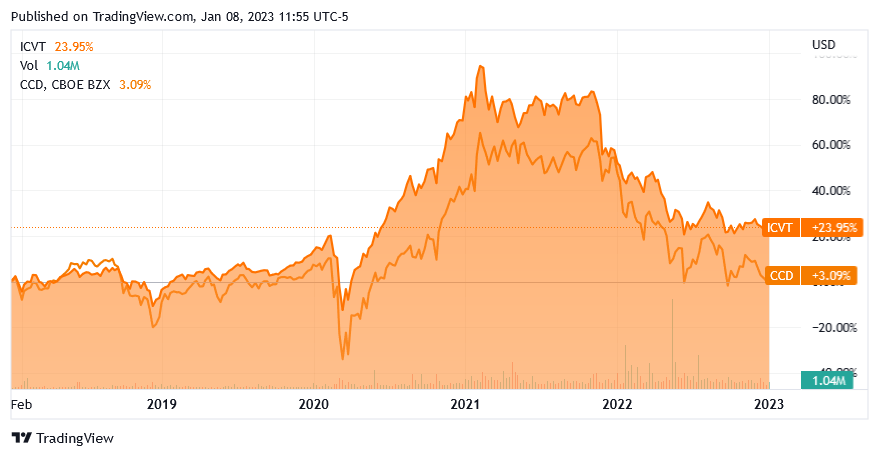

With that said, I would much rather have an actively-managed fund if investing in convertible securities. This is because the index may not time the conversion to common stock (if it converts the security at all). In addition, convertible securities are frequently issued by companies that are already financially distressed and so cannot obtain affordable financing through normal means. A convertible bond index would mix securities issued by these companies with convertibles issued by the true home-run companies. A good management team may be able to separate the two and achieve much higher returns overall. Unfortunately, the Calamos fund seems to fail at this task. As we can see here, the Calamos fund has underperformed the Bloomberg U.S. Convertible Cash Pay Bond Index ( ICVT ) over the past five years:

{kind=link}

The Calamos closed-end fund does boast a substantially higher yield as the index fund is only yielding 1.91% as of the time of writing. However, even its higher yield cannot make up for the roughly 20% underperformance here. We can overall see the advantage of convertible securities versus bonds though as the Bloomberg U.S. Aggregate Bond Index is down 8.87% over the same five-year period. Thus, the convertibles substantially beat ordinary bonds, which is expected because of the ability to convert them into equities.

As my long-time readers on the topic of closed-end funds are no doubt well aware, I do not generally like to see any individual asset in a fund’s portfolio account for more than 5% of its total assets. That is because this is approximately the point at which that asset begins to expose the fund to idiosyncratic risk. Idiosyncratic, or company-specific, risk is that risk that any asset possesses that is independent of the market as a whole. This is the risk that we aim to eliminate through diversification but if the asset accounts for too much of the portfolio, then this risk will not be diversified away. Thus, the concern is that some event may occur that causes the price of a given asset to decline when the market does not. In such a scenario, an asset may end up dragging the entire fund down with it if it accounts for too much of the portfolio. As we can see earlier in this article though, there is no particular asset that accounts for an outsized portion of the portfolio so we do not really need to worry about that here. This is something that is quite nice to see as the fund appears to be quite well diversified.

A few times in this article, I mentioned that convertible securities may frequently be issued by companies that have difficulty raising capital affordably through conventional fixed-income options. As such, one would likely expect that many of the securities in the fund have fairly high default risk. This is a risk that we should certainly investigate. Fortunately, this is quite easy as the major rating agencies (Moody’s, S&P, and Fitch) assign letter-grade ratings to fixed-income offerings that theoretically tell investors how likely the issuing company is to default on its debt. Here is a high-level overview of how the securities in the fund’s portfolio are rated:

Calamos Investments

An investment-grade security is defined as anything rated BBB or above. As we can see, that only describes 15.5% of the portfolio. This is something that may be immediately concerning as the remainder of the securities is classified as speculative-grade, which are colloquially known as “junk bonds.” As such, many investors may immediately be worried about the high risk of default possessed by some of these securities. However, this may not necessarily be the case since 70.0% of the bonds held by the fund do not have any rating at all. Thus, we do not actually know what risk is possessed by the majority of the assets in the portfolio. It is logical to assume that they are probably speculative grade though since it seems somewhat unlikely that any company with a strong enough balance sheet to qualify as investment-grade would opt to have its bonds unrated and pay the higher interest rate that accompanies such an offering. Thus, the risk of principal loss due to defaults should not be ignored here. However, the fund currently has 596 securities in the portfolio so that offsets this risk somewhat. After all, such a large number of securities means that any individual security only accounts for a relatively small proportion of the fund’s total assets so even a default would have almost no noticeable impact on the portfolio as a whole. The only risk that we really need to worry about would be if a large number of companies default all at once and in that case the economy has bigger problems than a few investors in a fund losing some money. Overall, then, there is no real need to worry about principal loss due to defaults with respect to this fund.

Leverage

Earlier in this article, I stated that closed-end funds like the Calamos Dynamic Convertible and Income Fund are able to utilize certain strategies that have the effect of boosting their portfolio yield above that of any of the individual assets in the fund. One of these strategies is the use of leverage. In short, the fund is borrowing money and then using the borrowed money to purchase convertible bonds. As long as the yield on the purchased securities is higher than the interest rate that the fund has to pay on the borrowings, this strategy works pretty well to boost the yield of the overall portfolio. As the fund is capable of borrowing at institutional rates, which are substantially lower than retail rates, this will usually be the case.

However, the use of debt is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage since this would expose us to too much risk. I do not usually like to see a fund’s leverage above a third as a percentage of its assets for this reason. Unfortunately, the Calamos Dynamic Convertible and Income Fund is above this level as the fund’s leveraged assets currently comprise 38.48% of the portfolio. While convertible securities are somewhat safer than common stocks and so can tolerate a bit higher leverage than a common stock fund, this is still a bit high. Investors would be wise to keep the risks here in mind as the fund will probably decline much faster than the index during a time of market weakness.

Distribution Analysis

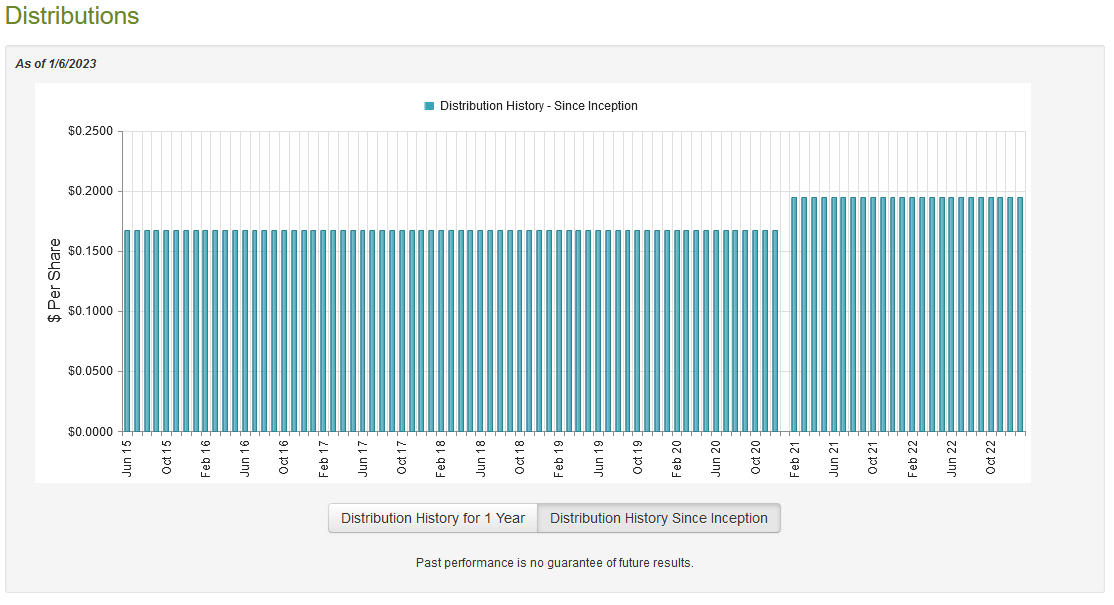

As stated earlier in this article, the primary objective of the Calamos Dynamic Convertible and Income Fund is to provide its investors with a high level of total return, which consists of both current income and capital income. In order to accomplish this, the fund maintains a leveraged portfolio of convertible securities that act much like high-yield bonds in most circumstances. As such, we would likely assume that the fund would have a very high yield. This is certainly the case as the fund pays out a monthly distribution of $0.1950 per share ($2.34 per share annually), which gives it an 11.13% yield at the current price. The fund has been remarkably consistent about this payout over the years as it has never cut the distribution, which is unique among fixed-income funds. The fund also increased the distribution back in 2021, which is nice to see:

{kind=link}

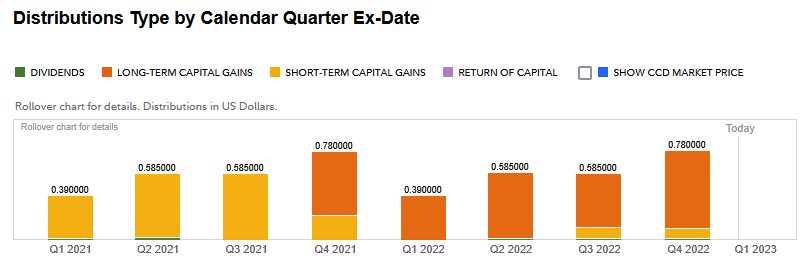

This strong distribution history will likely endear the fund to those investors that are looking for a safe and secure source of income that they can use to pay their increasing food and energy costs. Another thing that might be comforting is that these distributions consist entirely of capital gains. There is no return of capital component, which is likewise somewhat rare among funds with such a stable distribution history:

{kind=link}

One of the reasons why this may be comforting is that a return of capital distribution can be a sign that the fund is returning the investors’ own money back to them, which is obviously not sustainable over any sort of extended period. We clearly do not need to worry about that here. However, capital gains distributions require that the fund actually generate capital gains in order to be sustainable. There is no guarantee that the fund can generate such gains consistently. Thus, there could still be some concern about distribution sustainability here, particularly considering that the market has been pretty weak over the past year. Thus, it would be a good idea to have a look at the fund’s finances in order to determine how sustainable its distributions are likely to be.

Fortunately, we have an incredibly recent document that we can consult for this task. The fund’s most recent financial report corresponds to the full-year period that ended October 31, 2022, which makes this the most current full-year report of any fund that is available as of the time of writing. This report should obviously give us a very good idea of how the fund weathered the first few interest rate hikes and the accompanying market decline. During the full-year period, the fund received a total of $10,352,596 in interest and $5,672,349 in dividends from the investments in its portfolio. However, a sizable proportion of the interest was considered a repayment of the principal so is not considered actual income. The fund actually reported a total income of $6,437,197 during the period. It paid its expenses out of this amount, which left it with a net investment loss of $10,855,830. Obviously, that is nowhere near enough to pay any distribution, but the fund still paid out $59,155,624 to the shareholders. At first glance, this certainly looks quite concerning.

However, the fund might still be in good shape if it had sufficient capital gains to cover both the net investment loss and the distributions that were paid out. As might be guessed given the market’s performance in 2022, that was certainly not the case. The fund did manage to achieve net realized gains of $54,790,568 during the period but this was offset by $276,717,230 in net unrealized losses. Overall, the fund’s assets declined by $261,941,408 after accounting for all inflows and outflows. Thus, the fund clearly failed to cover its distribution. The fund did, unsurprisingly, have a much better performance during the November 2020 to October 2021 period as it both managed to cover its distributions and increase the size of the portfolio but even that strong performance was not good enough to carry it during the most recent year. As of November 1, 2020, the fund’s assets stood at $612,023,624 but they were down to $526,612,762 at the close of business on October 31, 2022. This could be a very real sign that the fund is overdistributing and it may have to cut its distribution unless the market turns around fairly quickly. That optimistic scenario seems somewhat unlikely and the fact that this fund currently has a double-digit yield indicates that the market appears to agree. A buyer of this fund should beware at this point.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a closed-end fund, the usual way to value it is by looking at the fund’s net asset value. The net asset value of a fund is the total current market value of all of the fund’s assets minus any outstanding debt. It is therefore the amount that the fund’s shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can acquire them at a price that is significantly less than the net asset value. This is because such a scenario implies that we are purchasing the fund's assets for less than they are actually worth. That is unfortunately not the case with this fund today. As of January 6, 2023 (the most current date for which data is available as of the time of writing), the Calamos Dynamic Convertible and Income Fund had a net asset value of $19.70 per share but the shares currently trade for $21.02 a piece. This gives the fund’s shares a 6.70% premium to net asset value at the current price. That seems like an incredibly high price to pay for a fund that will almost certainly be forced to cut its distribution in the near future, especially since that is higher than the 5.08% premium that the shares have traded at on average over the past year. The price looks far too high here, overall.

Conclusion

In conclusion, convertible securities can offer a good solution to many of the biggest problems that we have when investing in fixed-income securities. The biggest of these problems is that we are giving up the upside potential of common stock in exchange for income today. The Calamos Dynamic Convertible and Income Fund is one of the only closed-end funds that is almost exclusively invested in convertible bonds, which by itself makes it very attractive. Unfortunately, the fund’s attractive qualities end there as it appears very likely that it will have to cut its distribution in the near future and an investor will have to pay through the nose for this downside. I could see this fund being a reasonable buy if it could be purchased at a discount to net asset value, though.

For further details see:

CCD: This Convertible Fund Is Best Avoided, For Now