PDI - CEF Report February 2023 | The January Effect Didn't Disappoint

Summary

- The January Effect boosted the valuation of most areas of the closed-end fund market. Taxable bond CEFs have rallied strongly while leaving munis behind.

- We think this is an opportunity for investors for 2023, as credit spreads are likely to widen, dragging down taxable bond NAVs. We favor munis and high-quality taxables.

- Agency MBS is one of the best areas of the CEF market right now. Funds like FMY, BKT, and JMM offer up exposure to that sector. We like FMY here.

- We give our other top picks below.

So far, 2023 has been a banner year for closed-end fund ("CEF") investors. The average CEF is now up double-digits for the year, after a terrible 2022, which saw the average CEF fall by -14.5%. So, we have more room to go to fully recover.

The January Effect this year has been nothing short of spectacular, and made up for a lack of one in 2022.

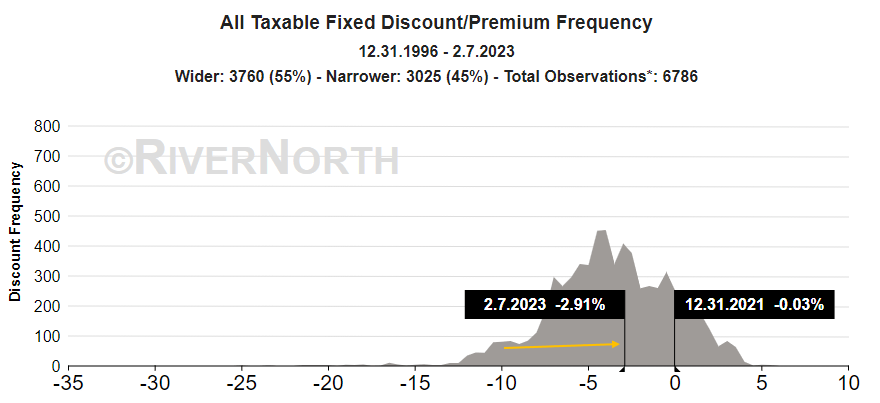

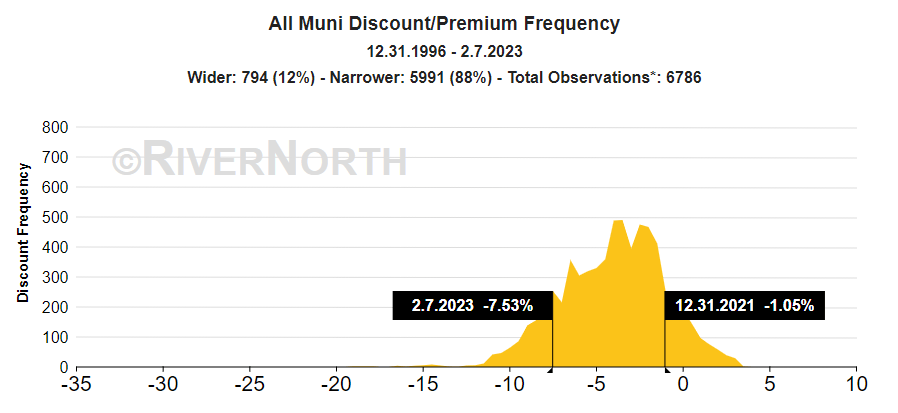

Discounts have tightened materially in taxable bonds while tax-free munis continue to trade very wide. In fact, munis are just 1.4% off their widest levels of the last year, at -7.9%. At the same time, taxable discounts have closed materially, from -6.9% to -3.3%.

alpha gen capital

In this report, we focus a lot on why this should be the reverse- with muni CEFs rallying and taxables selling off.

Macro Setup

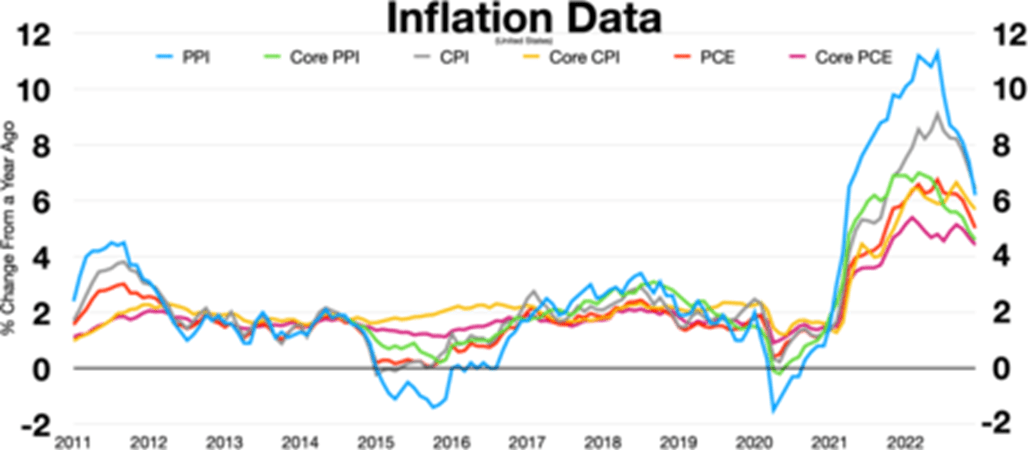

In the last six months, we've seen inflation peak, along with interest rates. But not only has inflation peaked, it is rolling over hard. CPI has fallen from just over 9% to 6%. While that is still elevated, it is falling fast now and hasn't shown any inflation in the last 3 months.

{kind=link}

Some inflation measures are close to outright deflation. Powell's preferred inflation measure of CPI ex-shelter has come down massively of late to just 0.9%.

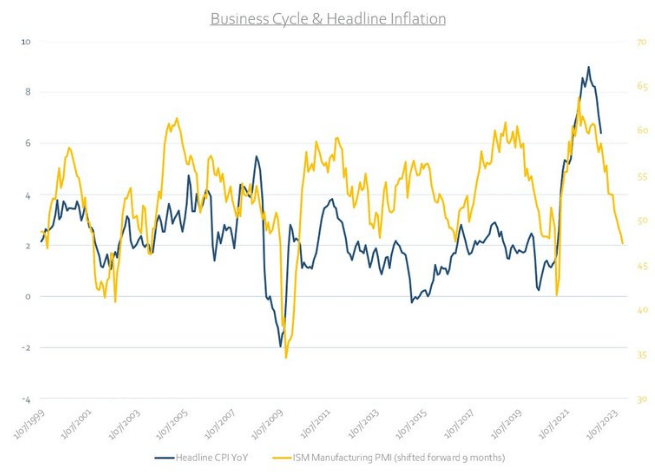

There is no doubt that the trend in inflation is definitely downward. If we add in ISM Manufacturing, we can predict where inflation will be in nine months' time. The chart below plots headline CPI inflation with ISM Manufacturing with a 9-month lead. In other words, ISM Manufacturing tends to lead inflation by 9 months.

{kind=link}

Why do we care?

Because this will be the driver of interest rates over the next year. As PMI and ISMs fall further, it should be a prescient lens into what inflation is highly likely to do.

If we think rates have peaked, and even if we don't want to own duration in case they don't come down much and instead, hang around, that makes bonds attractive here.

The Goose The Laid The Golden Egg

Anyone who has been to their local Kroger lately will know that eggs are like diamonds. Well, no, not really. But they have gone up in price astronomically.

We think the market is providing us the opportunity of a generation. The macro setup of an anomalous spike in inflation due to a Black Swan event from the Covid-19 pandemic has never happened before. The U.S. created boatloads of new dollars in an effort to stave off Armageddon. But the money creation led to a spike in spending, and, with supply chains strained, a dearth of enough supply of the goods being bought.

The Federal Reserve is currently combating that inflation problem by raising interest rates to tighten up monetary conditions. That should lead to negative money creation and help reverse the trends of the last few years.

Eventually, as we are starting to see, inflation will fall back to target (and likely beyond) and the Fed will lower rates back to neutral or below. The current neutral rate is about 3.25%-3.5% (in my opinion, that is probably 100 bps too high).

Fed Funds is currently at 4.75% and going up another 25 bps in March. That means we could see AT LEAST 150 bps coming off of Fed Funds.

In other words, interest rates a year from now are likely to be lower (and perhaps much lower) than they are today. If we think that is a greater than 75% probability, we can invest based on that likelihood to position portfolios to exploit that outcome.

investopedia

Our macro take is that a recession is highly likely, but even if one does not materialize, those prices are already embedded into the markets. The market is in no way pricing in a recession at this point. It is barely pricing in a mild slowdown or stall to GDP.

An earnings recession is also highly likely. That could also mean lower stock prices in 2023.

In any event, we think the markets are not factoring in a recessionary outcome, so the risk is firmly to the downside. If there's no recession, great! But it is likely that we only see a limited "recovery" due to falling profit margins tanking earnings. If there is a recession, then watch out below!

Portfolio Positioning

We continue to favor the high-quality sectors based on our macro take above. That view has not changed for several months now. For those tactical traders, I do think there is a very short-term bullish setup in the markets, but medium to long term, there is little to like about this market.

daily shot

But we are not about short-term calls. We want to position for the best yield per unit of risk that we can find.

Our Active Income Portfolio has a reduced allocation to CEFs at the moment - except muni CEFs - because of the NAV risks that abound. That rationale is simply due to the high yield market essentially saying not only will there not be a recession but there won't even be a soft landing.

Investment grade is showing the same. No recession risks and almost no risk of a soft landing - in other words, the economy won't slow much from here and continue to grow at a 1.5%+ rate.

Thus, to keep this short, we want to avoid credit risk, or funds that have risk from lower NAVs as volatility increases and credit spreads widen. We want to buy when those credit spreads widen out by 250-400 bps over current levels and the VIX gets to 35 or more.

For now, we keep our focus on muni CEFs and very high quality taxable bond CEFs.

Best Options | Focus On Quality (Like A Broken Record!)

Most individual investors fail to create risk budgets and look at how much they are allocated to each segment of their portfolio. That means allocating a certain amount to junk, quality, stocks, bonds, etc.

John Cole Scott, on a recent podcast , noted that the dispersion in the CEF marketplace has been interesting. We noted this in our opening - that the market is rewarding the riskier areas of the CEF market while ignoring the safer.

We think investors should be doing the opposite, as John Cole Scott said:

But for 2023, average closed-end fund is up 12% year to date market price total return, and it's up 7% net asset value, that's a solid 5% discount narrowing for the universe and that's basically double the average January Effect that we usually see most years. It's also interesting to look back to the end of third quarter, because December was tough but not a bad quarter for a 4th quarter, closed-end funds are up almost 20% since September 30th, and that's 5.5% discount narrowing. And so the January Effect as you mentioned, is definitely full in force. When we dig a little deeper, it's interesting because the munis, a third of the universe, the discount has narrowed less than 1% this year because even though rates are higher, there's still a lot of concern for I would say the dividend cuts that have been pummeling that sector. Preferreds, they've narrowed 4%, again less duration, a little less cuts in that sector but still some pain. Equity funds have only narrowed 2%, and taxable bond funds have narrowed 4.5%. When we looked in the January data, 10% of the universe cut their distribution 10% or more, so we talked about all of the dividend cuts from '22, we said we didn't think they were done. They're not as large for many cases as during '22, but they're still significant.

Like we noted, munis are being left in the dumpster while people are buying up risk without so much as a second thought as to the downside potential. This is primarily because, as John notes above, the massive amount of distribution cuts that have plagued the muni space.

These cuts have slashed the yields of these funds to some of the lowest levels relative to taxable that I have ever seen. Most retail investors will favor a 13%+ yielding PIMCO Dynamic Income Fund ( PDI ) over a 3.5% yielding Blackrock MuniVest Fund ( MVF ) , no matter what the difference is between the valuations (PDI is at a 15% premium while MVF at a -10.5% discount).

But this is the opportunity. When people are running from an asset class, especially a high-quality one, it's time to start accumulating.

Those cuts will not last forever. When short-term rates are lowered - the so-called Fed Pivot - the leverage costs of these funds will come down and the funds will be able to re-raise their distributions. In fact, given where yields are on munis today, they may be able to raise them ABOVE where they were before the start of 2022.

Taxables have rallied nice since Christmas and are now at fair value. But as we discussed, we don't think investors are being compensated for the risks assumed.

{kind=link}

Now, that doesn't mean having zero taxable bond CEFs in your portfolio. That just means reducing your overall exposure to an underweight weighting.

Meanwhile, muni CEFs remain at some of their cheapest levels ever going back to 1996. According to RiverNorth, discounts have only been wider about 10-12% of the time over the last 27 years. That is cheap, cheap, cheap.

{kind=link}

So our best ideas will center on the tax-free muni market.

One caveat. While we like muni CEFs, we also really like individual municipal bonds. While many individual investors do not like buying individual bonds (for reasons I don't understand), we would strongly advise learning to get past that.

BlackRock, one of the larger fund sponsors of muni CEFs, shows the problems in this market. Distribution coverage, despite cuts, remains below 100% on many funds, and UNII (essentially, the running tally of inception to date net investment income vs the distributions paid) are almost all negative.

The best muni CEFs have coverage above 100%, and UNII levels that are positive or at least trending in a positive direction. This is not the case here, with most of their funds - even with large distribution cuts.

{kind=link}

The canary in the coal mine: MFS Funds, a smaller CEF sponsor, has a very different distribution policy compared to, say, PIMCO. They adjust the distribution almost monthly to equal net investment income ("NII"). Thus, their UNII levels never get significantly negative and they simply pay out what their funds are earning from the bonds in the portfolio.

Conversely, there are fund sponsors like PIMCO who rarely alter the distribution, preferring to make large cuts or increases as a rare event rather than adjust too frequently. This is preferred by the marketplace, since it allows the investor to have confidence that their payout will remain fairly steady.

The MFS funds can be good proxies for future muni CEF distributions if they are trending in one direction or another. The February distribution announcement showed a sizable increase in the distribution for their funds.

Now, one month does not make a trend - and short-term rates did fall nicely during January, which have since reversed somewhat - but it is a hopeful sign.

Our take is that by the end of this year we could see much lower short-term rates, which would allow the funds to start increasing their distributions again. But patience is required.

And I would not wait until year-end to buy, because the discounts are likely to close significantly by then as investors anticipate the move. The play is to continue to buy now at these large discounts even though yields are low, and then be patient for the short rates to come down, which will be the catalyst to close the discounts.

Best Options For Risk Averse (3 or less risk rating)

- RiverNorth Managed Duration Municipal Income Fund II Inc ( RMMZ ), discount -7.0%, yield 6.96% *** The last 19-a notice shows that the fund covered 36.7% of the distribution through net investment income and the rest was return of capital. This fund came to market a year ago and suffered from severe tax loss selling last year. The discount has closed about 5 points already but could close another 5 points.

*** = large chunk of this is taxable income or return of capital

- Nuveen Municipal Credit Income Fund ( NZF ) , discount -10.8%, yield 4.18%. The fund cut the distribution three times in the last year for a total reduction in the payment by 35%! UNII is barely below zero and we will see if the most recent cut in January will start to rebuild that UNII balance. If it does, we could see the last cut for this fund, and investors could think of the 4.2% yield as the low point for the next couple of years.

- Nuveen Municipal High Income Opp ( NMZ ) , discount -4.6%, yield 5.0%. This was a long-term holding for us up until about a year ago. The fund was obviously not immune to the dynamics of the space. They first cut in August of last year and then again in November and lastly in January. Coverage is back over 101% but UNII is still -4.3c. We really need to see a reversal of that UNII trend to be sure that the last cut has been made. However, if you believe a year from now rates will come down, the next cut is immaterial. For those wanting 4.5%+ tax-free yield with reasonable safety, this is a good option. Long term performance has been very strong.

- MainStay Defined Term Municipal Opportunities Fund ( MMD ), premium +2.1%, yield 5.40%. This is a term fund that liquidates in 2024. So any premium should be considered a potential loss if you hold for the long-term. That said, I do think the chances of them converting this to a perpetual fund is fairly high given their performance and the market rewarding that performance with a premium valuation. They FINALLY cut the distribution by half a cent (-6%). Coverage is 106% and UNII a very strong 24c. If you can buy this at a discount, you win.

- Nuveen Corporate Income 2023 Target Term Fund ( JHAA ) , discount -2.5%, yield 3.25%. This is a target term fund that liquidates on December 1 of this year. Any discount will be captured as the investor receives the NAV upon liquidation. The fund has just 75 bonds, 25% of which are investment grade and 55% being high yield. Almost all of that high yield is BB (the best high yield credit rating). All of the holdings mature in 2023 or 2024 - with the majority in the latter half of this year. So the overall risk here is very low. As they mature, they will pay down leverage and start building cash.

- Invesco High Income 2024 Shares ( IHTA ) , discount -6.1%, yield 4.9%. This is another term fund that invests mostly in BBB-rated commercial mortgage backed securities. While the fund won't hit their target - in all likelihood - there is still a ton of value here. The NAV at $8.58 means they would need to gain $1.25 over the next 20 months. Possible, but not probable. If they do, you hit a home run as you capture the 6.1% discount, collect a 4.9% yield, and would see a cap gain in price of 21.8%. That would be a total return of ~36%.

- First Trust Mortgage Income Fund ( FMY ) , discount -6.7%, yield 5.7%. This is primarily an agency MBS (~34%) and non-agency mortgages (~60%) of the portfolio. While non-agency is the larger portion, these are not your father's subprime mortgages. The rules surrounding mortgage issuance is much stricter and the risk much lower.

Best Options For Risk Takers (3.5 or more risk rating)

- FS Credit Opportunities Corp. ( FSCO ) , discount -23.8%, yield 12.04%. This is a new CEF, at least a publicly-traded one. The fund converted from a private fund structure, which is why the discount is so large. Instead of being locked into the fund investors can now sell at any point, though they take a 23% haircut in the process. This fund portfolio is mostly senior secured loans, and while I'm no longer bullish on the loan space for 2023, I still like the fund because of the catalyst of the conversion to a CEF. As the marginal sellers wanting to sell get flushed out, we could see the discount close materially. Note: On December 14, 2020, FS Global Credit Opportunities Fund-A (FSGCO-A), FS Global Credit Opportunities Fund-ADV (FSGCO-ADV), FS Global Credit Opportunities Fund-D (FSGCO-D), FS Global Credit Opportunities Fund-T (FSGCO-T), and FS Global Credit Opportunities Fund-T2 (FSGCO-T2) (the Funds) merged into FS Global Credit Opportunities Fund (FSGCO). On March 23, 2022, the Fund was renamed FS Credit Opportunities Corp. ( FSCO ).

- First Trust High Yield Opportunities 2027 Term Fund ( FTHY ) , discount -10.3%, yield 10.6%. This is another term fund, but it has 3.7 years until liquidation. The large discount would then close upon closing in on that liquidation date. The yield is juicy at over 10.5% for a fund that invests in junkier credits. The fund is a mix of mostly bonds with a smattering of loans. The avg yield to worst is a whopping 9.97%, as the average price of the holdings is just $86.37. Lots of value here. And you get an additional 2.4% tailwind yield from the closing of the discount.

- Nuveen Mortgage and Income Fund ( JLS ) , discount -11.8%, yield 8.13%. This was a former term fund that converted to perpetual, which allowed the discount to float, and float it did. The average discount of 4.8% was destroyed and is now closer to -10.8%. The fund holds just 167 positions, but it is a mix of ABS, cMBS, collateralized mortgages, and corporate bonds. About half of the portfolio is rated non-investment grade and another quarter is not rated at all. The discount is attractive and the fund has a lot going for it, which we like.

Concluding Thoughts

The CEF market is a bit of upside down at the moment, with taxables being bought up and discounts closing materially in January but investors not touching munis. We think the muni side offers far better return per unit of risk at the moment thanks to NAV risk from spread widening. Watch your positions closely, especially the quality, and be comfortable with the amount of junkier holdings (single B or below) before committing new capital.

For further details see:

CEF Report February 2023 | The January Effect Didn't Disappoint