FLC - CEF Weekly Review: 'Best-Of-Breed' Designation Is Usually An Admission Of Ignorance

2023-05-06 03:59:06 ET

Summary

- We review CEF market valuation and performance through the last week of April and highlight recent market action.

- CEFs had a strong week to claw back some losses and finish April broadly flat.

- Investors should be cautious when told a given fund is a "best-of-breed" as this designation typically has little information content.

This article was first released to Systematic Income subscribers and free trials on Apr. 30

Welcome to another installment of our CEF Market Weekly Review where we discuss closed-end fund ("CEF") market activity from both the bottom-up - highlighting individual fund news and events - as well as the top-down - providing an overview of the broader market. We also try to provide some historical context as well as the relevant themes that look to be driving markets or that investors ought to be mindful of.

This update covers the period through the last week of April. Be sure to check out our other weekly updates covering the business development company ("BDC") as well as the preferreds/baby bond markets for perspectives across the broader income space.

Market Action

CEFs had a solid week to close out April with most sectors seeing gains as higher Treasuries and stocks provided strong tailwinds. April performance was more subdued with NAV gains offset by discount widening in the majority of sectors.

Systematic Income

After two straight months of losses, April provided a respite and came in nearly flat.

Systematic Income

The CEF space is up year-to-date after a couple of large swings.

Systematic Income

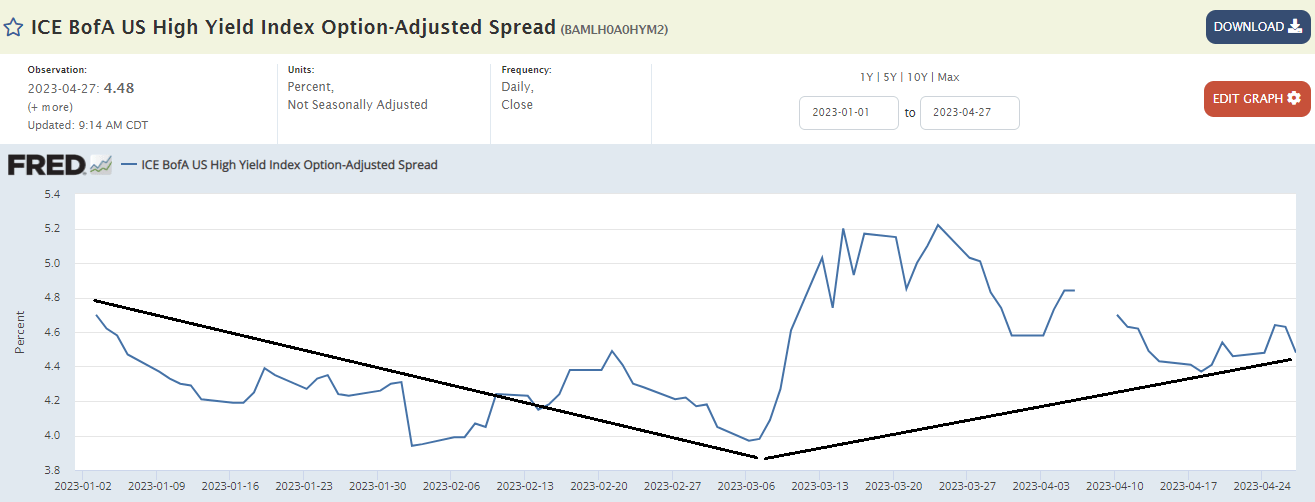

The performance of the broader CEF space largely mirrors what's happened with corporate bond credit spreads which tightened until March and then widened back out on the banks tremor, leaving them unchanged year-to-date.

{kind=link}

Discounts remain at decent levels. Equity CEF sector discounts recently gave up on their oddly expensive valuations and joined fixed-income CEF sectors at much more reasonable levels.

Systematic Income

Market Themes

A lot of CEF analysis we come across strikes us as a kind of offshoot of Aristotelian physics. Recall that Aristotle thought that a stone fell because falling was its natural tendency and, if left alone, it would fall. These days, of course, we have more rigorous explanations of motion that go beyond "nature" and that rely on the scientific method.

A lot of explanations for CEF performance these days, however, are stuck in the pre-scientific dark age. Many times you hear that the reason why a fund has outperformed is because it is simply a "best-of-breed" fund. This explanation also harks back to a kind of "nature" to explain performance. In reality, of course, using "nature" or "best-of-breed" as an explanation is no explanation at all.

Which brings us to the Flaherty preferred suite.

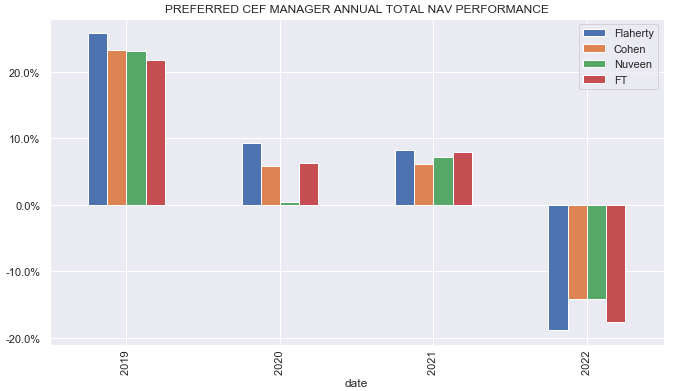

The Flaherty suite of preferred CEFs (FFC, FLC, DFP, PFD, PFO) had another distribution cut. The 5-fund suite has cut its distributions for a total of around a third since the end of 2021 at the rate of about double the broader sector average. It has also underperformed in total NAV terms since the end of 2021 and even more in total price terms.

If you go back to 2021 you'd trip over articles that kept talking about how these funds (particularly FFC) were "best-of-breed" preferred CEFs. This was entirely based on their strong performance through to 2021. And, obviously, few people bothered to ask exactly why these funds enjoyed such strong performance.

Whenever people can't explain performance in the CEF space they typically fall back on the black magic formulations like "best-of-breed". The reality is much more prosaic. The Flaherty funds don't use interest rate hedges in their portfolios. Many other preferred CEFs (e.g. Nuveen, Cohen funds) do use hedges to shorten up the duration of their holdings and fix leverage costs.

Preferreds, particularly the retail / exchange-traded flavor, can often have extremely long duration due to their perpetual and fixed-rate profile. Institutional preferreds tend to have a lower duration because the vast majority are in the Fix/Float format which limits their fixed-rate term, and hence duration to, typically, 5 years. Preferred CEFs can shorten up their duration profile by using instruments like interest rate swaps to make their portfolios less volatile and sensitive to changes in rates.

The other role of interest rate hedges is that they fix the cost of the leverage. This is because the funds pay fixed / receive floating on interest rate swaps. The pay-fixed leg shortens up the duration (i.e. partly offsetting the receive fixed-rate preferreds) and the receive-floating leg of the swap offsets the pay-floating leg of the credit facilities (which are usually Libor + 0.75% or so).

Net funds with rate hedges in place benefited since the end of 2021 because they suffered much less net income compression (since the cost of leverage did not rise very much, being largely fixed) and they suffered less from the rise in rates (because the hedges also lowered their duration profile).It's no surprise therefore that we find the Flaherty funds having to sharply cut their distributions - much more than the broader sector. And it's no surprise that the previous outperformance turned to underperformance in 2022.

{kind=link}

None of this is to say that certain funds don't have all-around advantages whether it's a lower fee structure or greater scale that can generate alpha in all market environments. However, it's important not to confuse these with features like the presence of hedges which work well in certain market environments (e.g. falling / low rates) and don't work well in other market environments (e.g. rising / high rates).

Ultimately, however good a manager is, it's very hard to push against the gravitational forces of their structural choices. This also means that if rates start to fall, the Flaherty funds structural choices will become tailwinds rather than headwinds. Once this process is underway we will consider switching our Cohen preferred CEF allocations, which have outperformed Flaherty funds in the rising rate environment, to Flaherty funds.

For further details see:

CEF Weekly Review: 'Best-Of-Breed' Designation Is Usually An Admission Of Ignorance