EXG - CEF Weekly Review: Blinkered View Of Distribution Coverage Can Mislead Investors

- We review CEF market valuation and performance through the last week of July and highlight recent market action.

- CEFs had a great July, erasing all of the June losses.

- We highlight one take on distribution coverage which makes little sense and which can mislead investors.

- And highlight DMO and EOI.

This article was first released to Systematic Income subscribers and free trials on July 30.

Welcome to another installment of our CEF Market Weekly Review where we discuss CEF market activity from both the bottom-up - highlighting individual fund news and events - as well as top-down - providing an overview of the broader market. We also try to provide some historical context as well as the relevant themes that look to be driving markets or that investors ought to be mindful of.

This update covers the period through the last week of July. Be sure to check out our other weekly updates covering the BDC as well as the preferreds/baby bond markets for perspectives across the broader income space.

Market Action

The CEF market was on fire in July with all sectors finishing in the green. Convertible bonds led the pack rallying by close to 14%.

Systematic Income

The CEF market gain over July was nearly identical to its June loss as shown below.

Systematic Income

The CEF index rallied back to its previous peak. Interestingly, it has also been able to break through the previous pattern of lower highs.

Systematic Income

Discounts have done well, tightening to their levels from earlier in the year.

Systematic Income

Market Themes

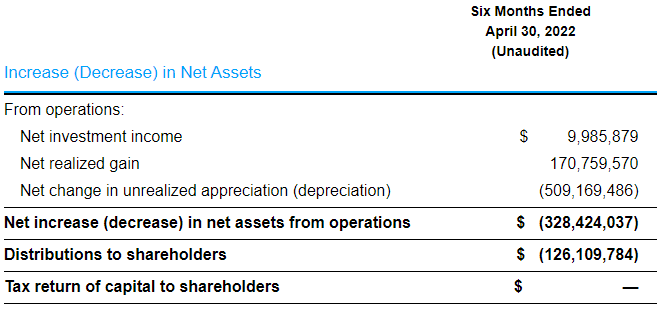

The topic of distribution coverage of equity CEFs, and in particular, that of the Tax-Managed Global Diversified Equity Income Fund ( EXG ) came up on the service.

One view is that the EXG distribution is fully covered because its distributions this year have come entirely from realized gains and net income - no ROC was distributed to support the distribution. This is indeed what we find if we look at the fund's latest shareholder report. Based on this, the fund has fully covered its distribution for the reported period.

{kind=link}

This is all well and good. However, the very obvious elephant in the room is that along with the $10m in net income and $171m in realized gains there is also the small question of $509m in unrealized depreciation.

There are different definitions of distribution coverage. The definition that makes the most sense to us is one that simply looks at net investment income versus distributions. It's fairly stable year to year and pretty intuitive.

However, a number of equity CEF commentators like to use total NAV returns to see whether the distribution is covered or not with the idea that so long as the fund generates enough total value (income and capital gains) to cover distributions it's fine.

In our view, investors in equity CEFs shouldn't really worry about distribution coverage because equity returns are so variable. For example, because of the strong performance of the equity market in 2021 most equity CEFs had distribution coverage (using the total NAV return definition) of 200%+. This year, equity returns have been poor so equity CEF distribution coverage is something like -200% so far this year. Maybe using the definition of distribution coverage that swings from +200% to -200% from year to year is helpful to some investors but it's not all that helpful to us.

However, be that as it may - let's leave aside the merits of the total NAV definition of distribution coverage. A definition of distribution coverage that 100% doesn't make any sense is to ignore unrealized appreciation / depreciation and only focus on realized gains and net income which is what the EXG coverage argument does above. Pretending that somehow unrealized depreciation is not real or somehow less real than realized gains is a ludicrous idea and investors should avoid this "magical thinking" definition of coverage.

Market Commentary

Franklin Templeton / Western Asset released share repurchase numbers for Q2. For example, they bought 31K of [[DMO]] shares along with shares in 6 other CEFs. These are not large numbers – for DMO it was about 0.3% of all outstanding shares but it’s still good to see. First, it is accretive to the NAV if the manager buys the stock at a discount. The effect is small but it can add up over time. The second benefit of share repurchases is that it supports the price. Overall, having an active repurchase share program is a nice thing to have both from an economic returns perspective as well as being a signal that management are trying to do the right thing for shareholders even if it decreases their management fees by reducing assets under management.

The Enhanced Equity Income Fund ( EOI ) came up on the service and whether it's basically the same as holding the S&P 500 but earning an 8% yield (rather than the [[SPY]] 1.5% yield, presumably). The short (and long) answer is no.

EOI is a covered call fund with an S&P 500 benchmark, however, covered calls are not outright equity. For any historically uptrending asset like stocks, a covered call fund is almost guaranteed to underperform an outright equity fund. It’s no different with EOI which underperforms SPY by 2.5% and 3% per annum over the last 5 and 10 years in total NAV terms.

The other thing is that for taxable fund investors EOI is not going to be as efficient as SPY which distributes a small amount of qualified dividends. EOI distributes a combination of capital gains, ordinary income and return of capital. Lots of investors like covered call ROC because it's tax free in that year. A high level of ROC can be nice but it does reduce your cost basis so, in effect, it becomes a potential long-term capital gain impact later on in a taxable account. So, overall, EOI offers lower historic returns and a worse tax profile for taxable holders than holding outright equity. Covered call funds are often viewed as a slam-dunk replacement of equity holdings but they do have downsides that investors should take into account.

Stance and Takeaways

We have been adding to our CEF allocations through the drawdown this year by rotating away from more resilient assets in our Income Portfolios. However, apart from a relative value switch within the PIMCO taxable suite, we have stayed on the sidelines through this rally. Our view is that the market appears to be pricing in a pivot by the Fed which is not real. Powell's comment that the Fed is already at the neutral rate suggests that there is not much more hiking to do and that a soft landing is possible. This seems like wishful thinking. In our view, the Fed will not be constrained by any theoretical estimate of the neutral rate and will keep hiking until inflation has decisively shifted lower and has come within striking distance of its 2% target. If that's right, there should be more volatility in the CEF space into the rest of the year for investors to take advantage of.

For further details see:

CEF Weekly Review: Blinkered View Of Distribution Coverage Can Mislead Investors