FUND - CEF Weekly Review: Is A Net Income Snap-Back In The Cards For CEFs?

2023-06-19 04:01:13 ET

Summary

- We review CEF market valuation and performance through the second week of June and highlight recent market action.

- CEFs continued their rally over June, in reversal of the weakness over May.

- We take a look at whether CEF net income will move back to its previous level once the Fed starts to cut rates.

- And highlight distribution updates from a number of funds.

This article was first released to Systematic Income subscribers and free trials on June 11.

Welcome to another installment of our CEF Market Weekly Review, where we discuss closed-end fund ("CEF") market activity from both the bottom-up - highlighting individual fund news and events - as well as the top-down - providing an overview of the broader market. We also try to provide some historical context as well as the relevant themes that look to be driving markets or that investors ought to be mindful of.

This update covers the period through the second week of June. Be sure to check out our other weekly updates covering the business development company ("BDC") as well as the preferreds/baby bond markets for perspectives across the broader income space.

Market Action

CEFs enjoyed a good week, in reversal of the weakness we have seen over the previous month. Month-to-date, all but two sectors are up, led by the higher-beta Convertibles and MLPs.

Systematic Income

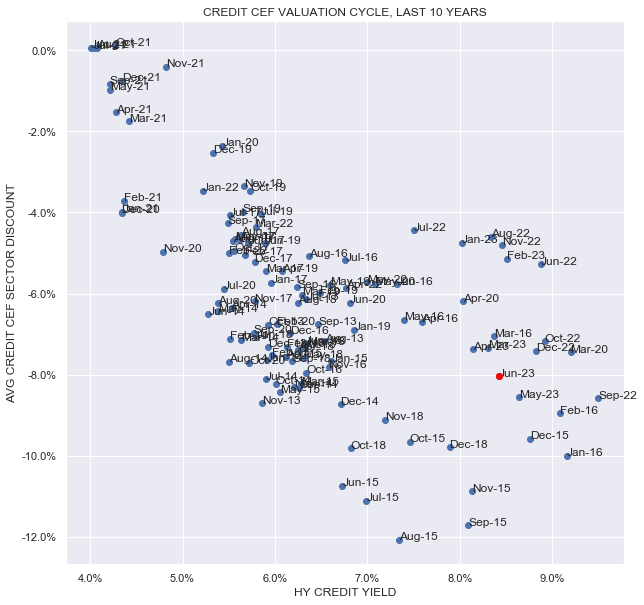

Revisiting our usual discount / yield CEF matrix which uses high-yield corporate bonds as the yield proxy we see that the CEF market remains in the fairly attractive lower-right quadrant of wide discounts and high yields. This is quite a change from the much less attractive upper-left quadrant where CEFs spent most of 2021.

{kind=link}

Market Themes

As investors prepare for the Fed rate hiking cycle to end, a sensible question is whether we should expect net income (and hopefully, distributions) to rise back up after a drop across many CEFs over the past 18 months.

If short-term rates start to move lower, net income for most fixed-rate CEFs should rise. However, we wouldn't expect net income to move back to the same level as it was at the end of 2021.

This is because short-term rates are unlikely to go back to zero which means that leverage costs are likely to remain well above their 2021 levels. And secondly, total borrowings are also unlikely to move back to their 2021 levels. This would require longer-term interest rates to also fall back to their rock bottom levels e.g. AA yields would have to fall from 4.8% to 1.7%. That seems pretty unachievable.

One aspect that will grow net income levels is when funds start to rotate into higher-coupon securities which have been issued since 2022. Although this will result in higher net income, it will not lead to a higher level of portfolio yield which is really what investors ought to pay attention to.

Ultimately, it seems likely that net income for non-floating rate credit CEFs will reverse when the Fed starts to reverse the hikes (some later this year if market consensus is correct) however investors shouldn't expect it to scale the heights of 2021.

Market Commentary

The Delaware Investments National Municipal Income Fund ( VFL ) cut its distribution by around 28%. VFL is one of the few Muni CEFs that haven't cut in this rate hiking cycle. One reason was that the previous distribution wasn't particularly egregious. Another reason could be that the managers were waiting for the end of the rate hiking cycle to get a better gauge of a sensible longer-term distribution.

Some managers choose to update the distribution fairly frequently to reflect current economics (Nuveen, BlackRock) while others do so infrequently and try to manage it through the cycle (PIMCO). There is no right or wrong here however a longer wait can mean a greater overall cut because it likely requires the funds to hold some bonds to finance the distribution which, naturally, leaves fewer income-generating assets. VFL struggled a bit recently, underperforming the median CEF by around 4% over the past year in total NAV terms. The valuation has been tempting for some time however tepid performance means the fund can be mostly ignored.

Two Royce equity CEFs (RVT, RMT) cut their distributions by 6-7%. The funds have a managed distribution policy (i.e. MDP) which pays out 7% of the average of the prior 4 quarter-end NAVs. As it happens, the Sprott Focus Trust ( FUND ) uses the same MDP but with a 6% multiplier and also cut.

Using quarter-end NAVs will make the distribution quite volatile which is why other CEFs use an average of daily NAVs over some time frame (e.g. RiverNorth) or a monthly rather than quarterly average (e.g. Allspring). Over the longer term, the distribution will depend on whether the funds can outperform their multiplier. A figure of 6-7% does not seem out of reach for equity CEFs and the three funds have delivered on these performance levels over the previous decade which suggests that the distribution should be roughly flat if this kind of performance continues in the future.

For further details see:

CEF Weekly Review: Is A Net Income Snap-Back In The Cards For CEFs?