CLLNY - Cellnex Telecom: A Juicy Takeover Target For American Tower

Summary

- American Tower and Brookfield are rumored to team up to acquire Cellnex Telecom, Europe's largest cellular tower operator in Europe.

- Cellnex is a company and not a REIT, but it is trading at roughly 10-12 times its anticipated 2025 AFFO-equivalent.

- That makes it a juicy target for American Tower, which is trading at almost twice that multiple.

- If no buyout happens, I would be a buyer of Cellnex at the current share price and in the lower 30 EUR range.

Introduction

Cellnex Telecom ( CLNXF ) has a very simple business model: it operates cell phone towers and rents it out to third parties (mobile carriers). It is a win-win situation: a mobile carrier doesn’t really want to build their own cell phone towers as it is not as efficient as having a third party owner which can lease space and capacity on the same tower to 2-3 operators. This means third party operators will very likely always continue to exist: it is easier for a mobile carrier to just lease them rather than building and operating them. The business model is sound, and all contracts with the carriers are pretty long-term focused.

Thanks to the strong visibility of future earnings and the very strong cash flow profile of these cell phone towers (the sustaining capex is very, very low), there has been a real wave of consolidation in Europe, mainly fueled by cheap debt. It was good practice to borrow at 1.5% to buy 5% yielding assets from any financial engineering point of view.

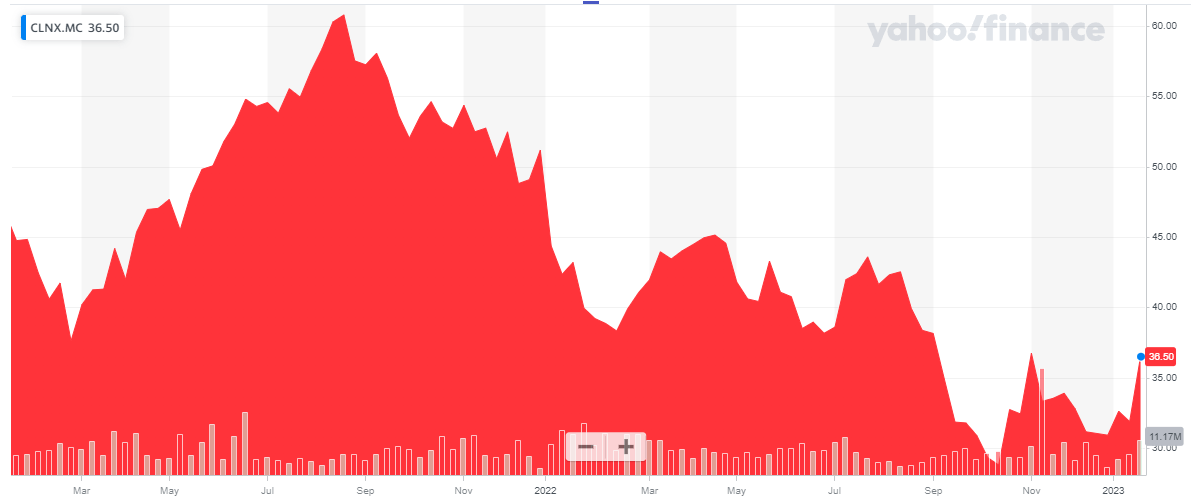

But. Reality is setting in, and the debt that was originally issued at 1 or 1.5 or 2% will have to be refinanced at much higher rates (4-5%), and that will hurt the earnings. In this article I wanted to dig a bit deeper into Cellnex as it is the largest European player, active in several countries. Unfortunately the share price jumped last Friday on (unconfirmed) buyout rumors of Brookfield ( BAM ) ( BN ) and American Tower ( AMT ) kicking the tires of Cellnex.

{kind=link}

Cellnex has its primary listing on the Madrid Stock Exchange where it is trading with CLNX as ticker symbol . The average daily volume in Madrid is approximately 1.9 million shares er day, for a total monetary value of roughly 70M EUR per day. I will use the Euro as base currency throughout this article.

A quick look at the business model and free cash flow

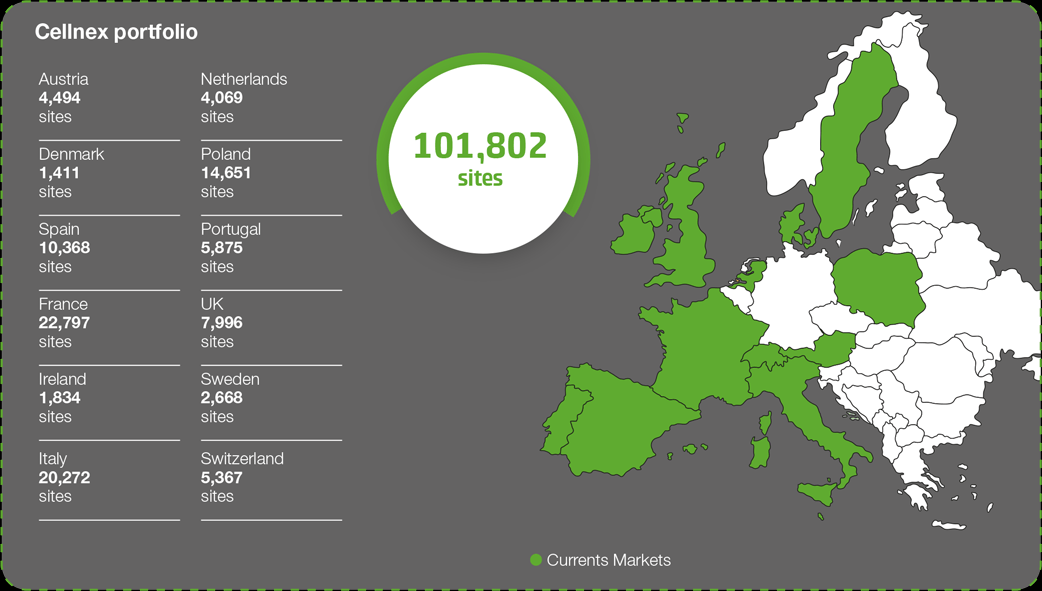

Cellnex has in excess of 100,000 sites all over Europe, with France being the largest contributor, accounting for over 20% of the total site count. Italy is a close second with about 20%. The total number will have increased a little bit after closing the most recent acquisition deal which finally obtained the required antitrust approvals, but the breakdown is still pretty representative.

{kind=link}

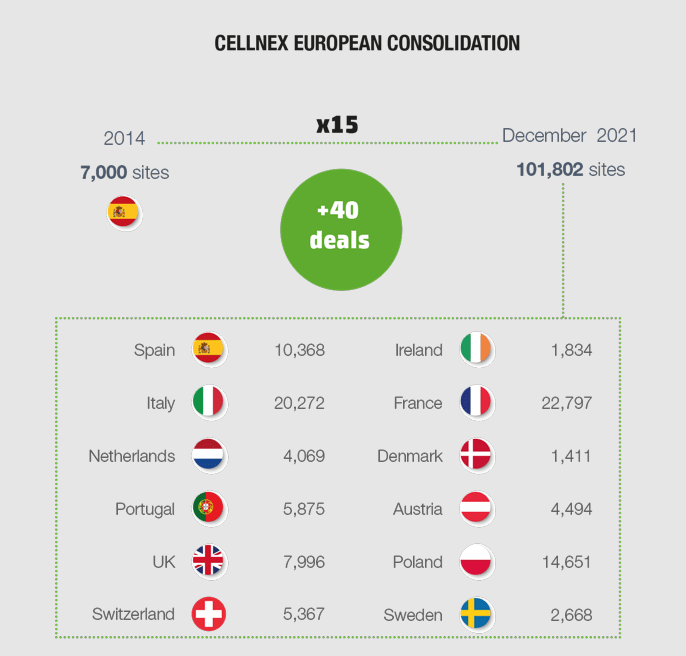

As mentioned in the introduction: the business model is simple. Cellnex owns cell phone towers and leases them out to 1-3 tenants per tower. Cellnex was one of the main consolidators in Europe, as it has grown its total site count by 1,400% thanks to closing 40 deals. The company also distributes radio and TV signals for certain stations.

{kind=link}

Those deals were debt-funded as that just made a lot of financial sense. It also means Cellnex had 16.6B EUR in gross debt and about 2.7B EUR in lease liabilities on its balance sheet as of the end of June. Fortunately there also was about 2.5B EUR in cash, so the net financial debt (excluding leases) was roughly 14.1B EUR. There are currently 705M shares outstanding, resulting in a market cap of 25.7B EUR and an enterprise value (excluding leases) of just under 40B EUR. Way too big a company for ESCI of course.

Before diving into the debt situation, it makes sense to discuss how much free cash flow the company is currently generating, before the increasing interest rates will hit the bottom line. The most recent detailed financial report is the H1 2022 report and that’s a good starting point.

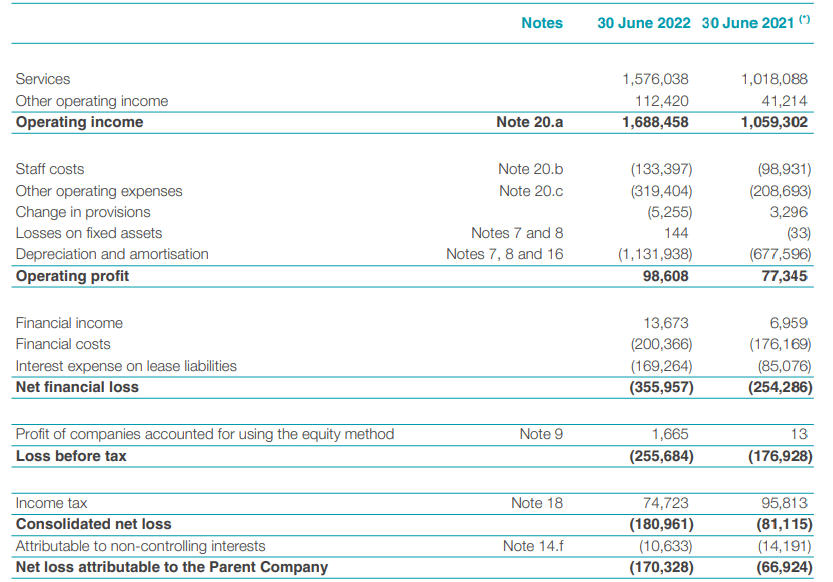

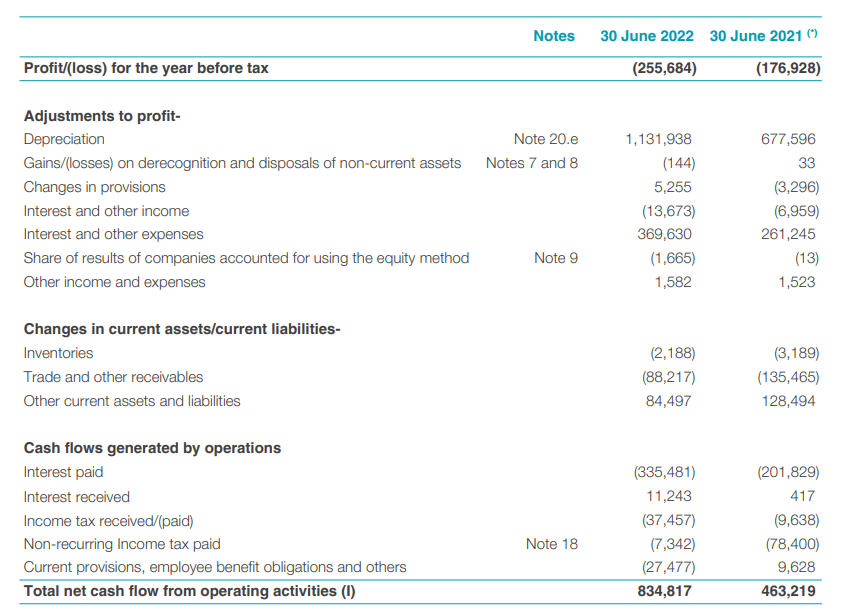

The total revenue in the first half of 2022 was 1.7B EUR , resulting in an operating profit of just under 100M EUR. As you can see below, the depreciation and amortization expenses are high. Not relative to the value of the assets, but relative to the revenue. After deducting the 356M EUR in finance expenses and after taking the tax credit into account, the net loss attributable to the shareholders of Cellnex was 170M EUR or 0.25 EUR per share (note: since the end of H1, the share count has increased, which should result in a lower EPS).

{kind=link}

One thing is clear: the very high depreciation expenses are causing the net loss. But once a tower has been built (or purchased), the sustaining capex falls back to almost nothing. In the first nine months of the year, the total sustaining capex was 57M EUR. That’s 20M EUR per quarter, and 40M EUR for a semester. I will round this up and use 50M EUR in sustaining capex in the first half of 2022.

The reported operating cash flow in the first half of the year was 835M EUR, which includes about 45M EUR in taxes paid. There also was a negative impact of 6M EUR from working capital changes so the adjusted operating cash flow (excluding making adjustments for the timing of tax payments) was 841M EUR.

{kind=link}

From that amount, one should also deduct the 325M EUR in lease payments. This means the underlying operating cash flow was 516M EUR, and the free cash flow would be roughly 466M EUR or just over 60 cents per share.

{kind=link}

Cellnex did complete an acquisition so the H2 results could (and should) be a bit stronger and will for sure exceed 1B EUR for 1.5 EUR per share.

Breaking down the debt: long-term bonds = smart

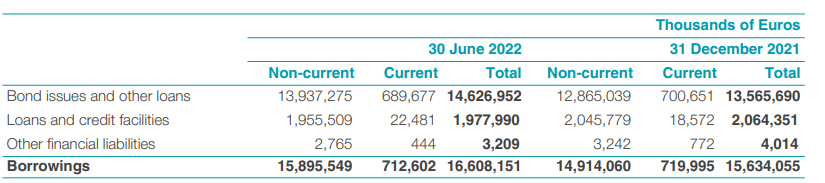

With about 16.6B EUR in debt on the balance sheet, it will become extremely important to keep an eye on interest rates. Fortunately Cellnex played it smart and less than a fifth of its total debt consists of floating rate debt (bank debt). 86% of the total debt has been raised by issuing bonds. Note: the breakdown below only shows 15.6B EUR in gross debt as it excluded the equity component of the convertible bonds. Seeing Cellnex’ price trading where it is, I am just assuming the entire 16.6B EUR in debt will have to be repaid in cash.

{kind=link}

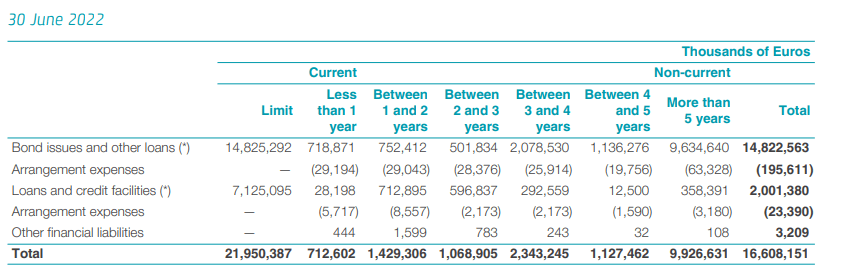

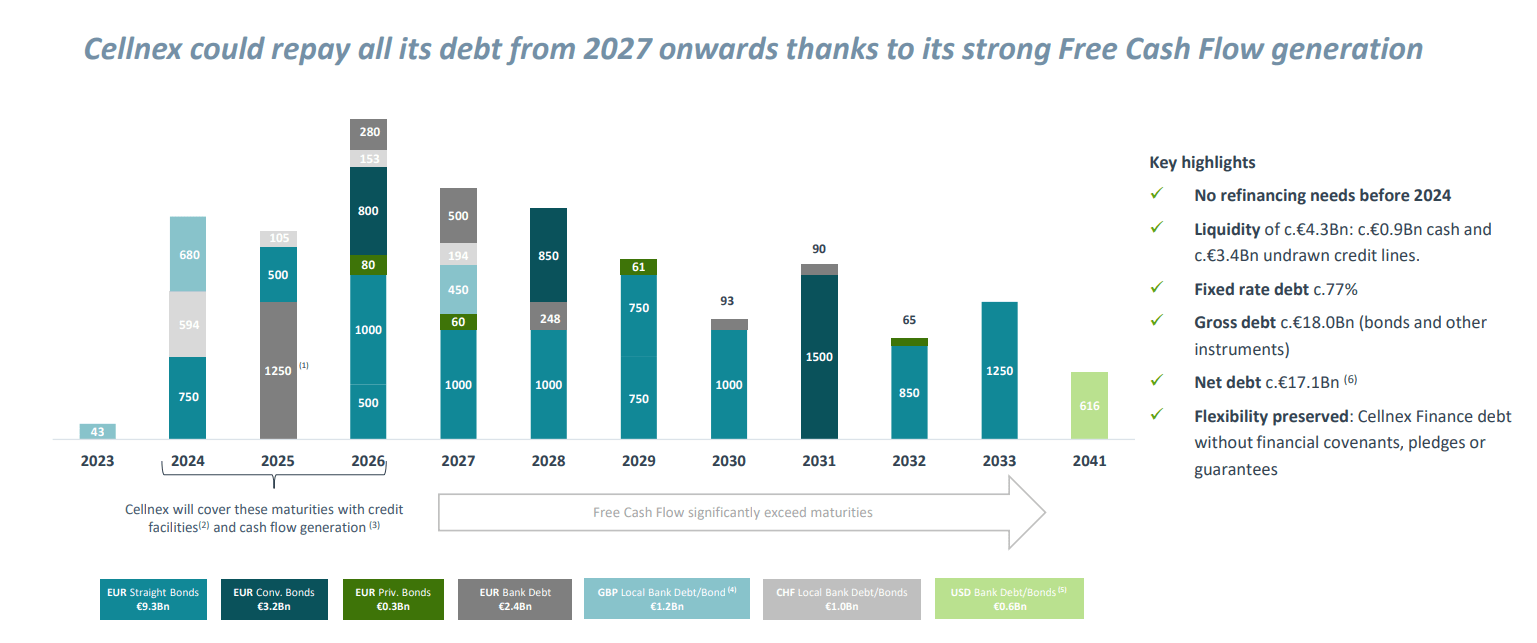

Cellnex has nicely staggered its debt repayments. Only 2.1B EUR has to be repaid before the summer of 2024 and the current cash position could actually easily take care of every single repayment. Additionally, about 60% of the total debt had a term of more than 5 years. That’s good as it provides a runway to increase the revenue and lease income before it gets slapped in the face with higher interest rates.

{kind=link}

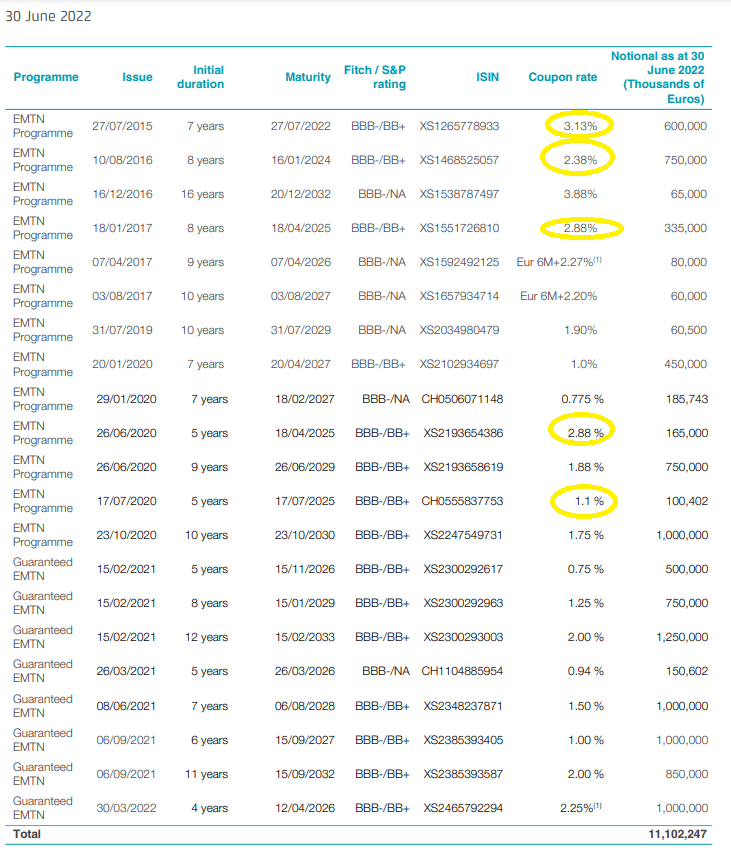

Cellnex also provided a nice breakdown of the size of its loans and the respective maturity dates. I have circled the loans due before the end of 2025.

{kind=link}

Interestingly, the loans that will mature first have the highest coupons, which means that even if the cost of debt increases to 5%, the impact will remain limited to about 50M EUR per year, assuming all loans are 100% refinanced (which I do not anticipate).

{kind=link}

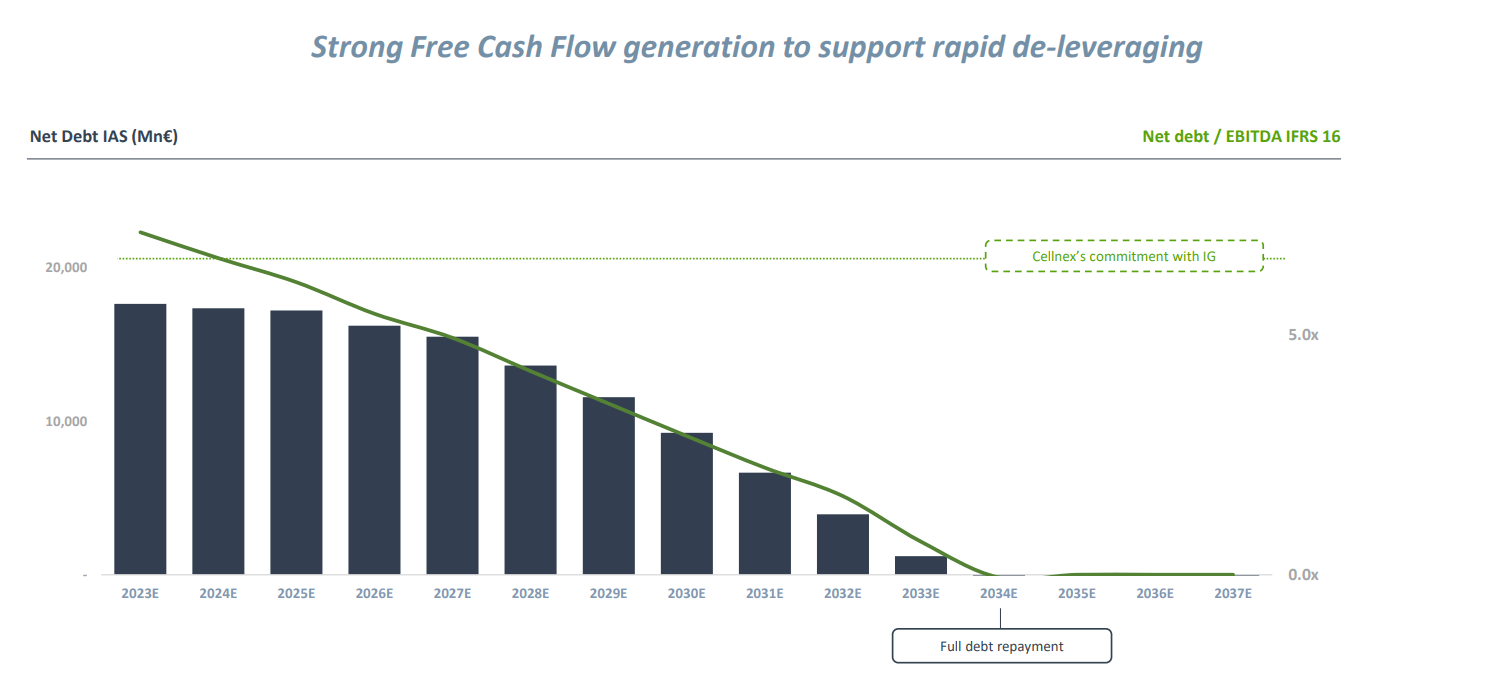

Cellnex for sure has the debt level on the top of its mind as it even provided a chart to show when all debt could be repaid using the free cash flow generated by the company. While I don’t mind some debt, it is good to see the company is mindful of the impact of higher interest rates and is already proactively shifting gears.

{kind=link}

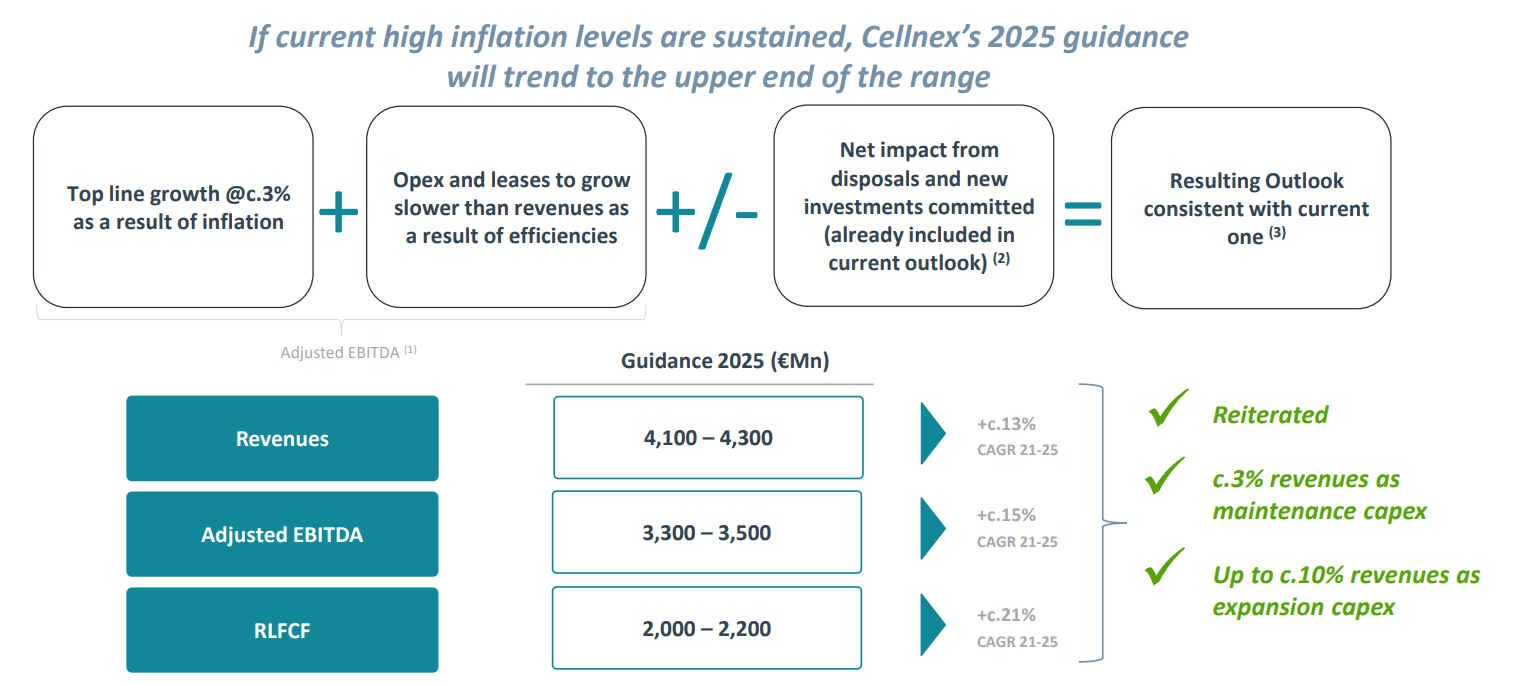

Interestingly, Cellnex is now guiding for the 2025 guidance to reach the upper end of its guidance. As a reminder: CLNX expects 2-2.2B EUR in free cash flow by 2025 due to an EBITDA increase to 3.3-3.5B EUR.

{kind=link}

It’s perhaps not a surprise Cellnex used 2025 because the majority of its cheap loans will only mature after 2025 so the hardest hit will follow in the post-2025 era. But let’s first start with the 2025 guidance.

We know the EBITDA will be around 3.4B EUR (midpoint), and we also know the average depreciation rate will be roughly 2.4B EUR going forward. That results in 1B EUR in EBIT. The interest expenses should remain relatively flat as I expect Cellnex to repay a portion of the debt coming due rather than opting for 100% refinancing. I will use 650M EUR as interest expenses which is similar to the H1 interest expense. I expect debt repayment to cancel out the higher interest rates between now and 2025.

That results in 350M EUR in pre-tax income, for a net income of roughly 250M EUR or 30-35 cents per share.

We also know the sustaining capex will be 3% of the revenue (so 125M EUR), and the lease payments should remain relatively unchanged at 650M EUR per year. If we add back the 2.4B EUR in depreciation and subsequently deduct 800M EUR in sustaining capex and lease payments (775M EUR rounded up to 800M EUR), the free cash flow result would be roughly 1.85B EUR or 2.6 EUR per share. The free cash flow result would be equal to the AFFO for a REIT. AMT is a REIT, Cellnex isn’t so that’s why I have to use the FCF for Cellnex’s result, which is the most comparable metric to American Tower’s AFFO result.

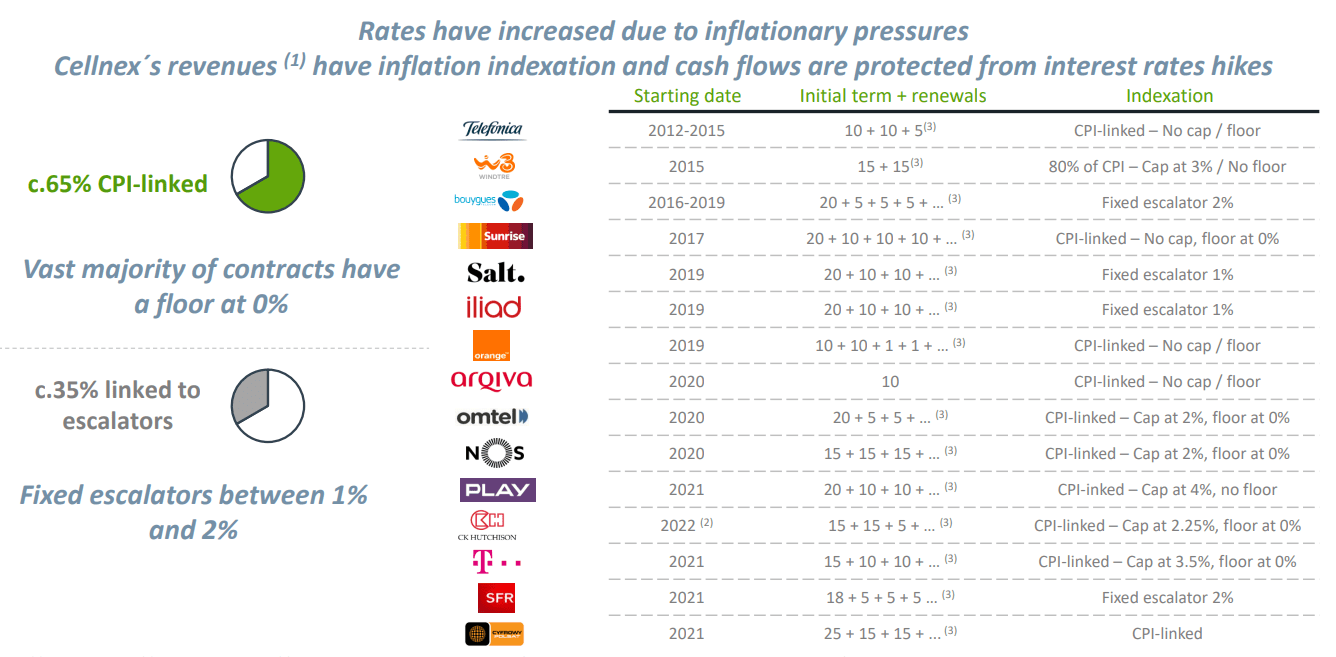

The higher revenue and EBITDA should be caused by the completion of all synergy benefits after all M&A (this is estimated at 100M EUR per year) while Cellnex anticipates to be able to increase its revenue by 3% per year based on the existing lease escalators. While the image below shows 65% of the lease agreements have CPI-linked lease increases, most of them are capped at 2-3%. So unfortunately this means Cellnex’ revenue growth will be capex and we will not see a standard 6-10% revenue increase in 2023.

{kind=link}

Investment thesis

Cellnex is not expensive. The company is clearly benefiting from its wise decision to lock in interest rates for the long haul, and the impact will only be clearly noticeable from 2026 on. And that means the impact could actually be pretty benign. If the total revenue indeed comes in at 4B EUR from 2026 on, standard 2% yearly hikes would add about 50-70M EUR to the EBITDA which would actually be sufficient to entirely cover the impact of a 4% interest rate increase on 1.5B EUR in annual debt refinancings. This means I see the FCF/share stagnate in 2027-2029 before increasing again from 2029 on. Due to the vast majority of debt having fixed interest rates, I think Cellnex is in an excellent position to get through the refinancing cycle without a dent in its performance.

Also kindly notice my own FCF calculation for 2025 is about 7% below the lower end of the company’s guidance so I’m definitely a bit more conservative. Reaching the lower end of the guidance (which would be a disappointment as Cellnex is actually guiding for the higher end of the guidance) would result in a FCFPS of 2.8-2.85 EUR per share. Reaching the higher end of the guidance would result in an FCF/AFFO exceeding 3 EUR per share.

AMT is currently trading at approximately 22.5 times its 2022 AFFO and likely around 20 times its 2024-2025 AFFO. Applying that same multiple would result in a 2025 price target of 55-60 EUR per share for Cellnex. I definitely understand why AMT would be very interested in Cellnex, even if it would have to pay a 40% premium on top of the current share price as even at 50 EUR per share, AMT would still be paying just 15-16 times AFFO, making it an accretive deal even if no synergy benefits would be unlocked.

Bottom line: I hope the M&A rumor will be disproven soon. I would like to pick up stock in the lower-30 EUR range as at 33 EUR per share, the 2025 FCF yield (comparable to the AFFO for American Tower) will be 8-8.5%. An as Cellnex hardly pays a dividend there is just a symbolic dividend of a few cents per year), that entire FCF result could be used to simply repay debt rather than refinancing it. And if there is any truth to the buyout rumor, AMT and Brookfield could be getting a very good deal depending on the ultimate price they will pay.

For further details see:

Cellnex Telecom: A Juicy Takeover Target For American Tower