CPAC - Cementos Pacasmayo: Decent Q3 Results As Cement Demand In Peru Remains High

2023-10-31 12:18:49 ET

Summary

- The company’s revenues went down by 6.7% in Q3 2023 while its EBITDA rose by 3.2% thanks to the completion of a new kiln at the Pacasmayo plant.

- In my view, the EBITDA margin could surpass 26% in 2023 as clinker production from the new facility ramps up.

- Cement demand in Peru remains above pre-pandemic levels and it seems low GDP growth is having a muted effect at the moment.

- With cement demand remaining resilient, I continue to think Cementos Pacasmayo should be trading at above 8x EV/EBITDA.

Introduction

I’ve been following Peruvian cement producer Cementos Pacasmayo ( CPAC ) closely and I’ve written three articles about the company on SA so far. The latest of them was in July 2023 and in it I said that cement demand in Peru has been resilient and that the new kiln at the Pacasmayo plant could boost the EBITDA margin to over 26% by the end of 2023.

Well, Cementos Pacasmayo released its Q3 2023 financial results on October 26, and I think they were strong. Revenues went down by just 6.7% as cement demand in the country remained robust while EBITDA improved by 3.2% year on year largely thanks to the new kiln. I’m keeping my buy rating on the stock. Let's review.

Overview of the Q3 2023 financial results

In case you're not familiar with Cementos Pacasmayo or my earlier coverage, here's a brief description of the business. The company was founded in 1949 and it has a total of three facilities in northern Peru with a combined cement production capacity of 4.9 million MT/year as well as a clinker manufacturing capacity of 3.4 million MT/year. Cementos Pacasmayo is among the three main cement producers in Peru, with the other two being UNACEM, and Cemento Yura. Together, these three firms control over 90% of the local cement market and each of them could be considered a monopoly in a separate region of the country. Cement has a low cost-to-weight ratio, which means it’s economically unfeasible to transport it over long distances, which also makes imports uncompetitive from a cost standpoint.

{kind=link}

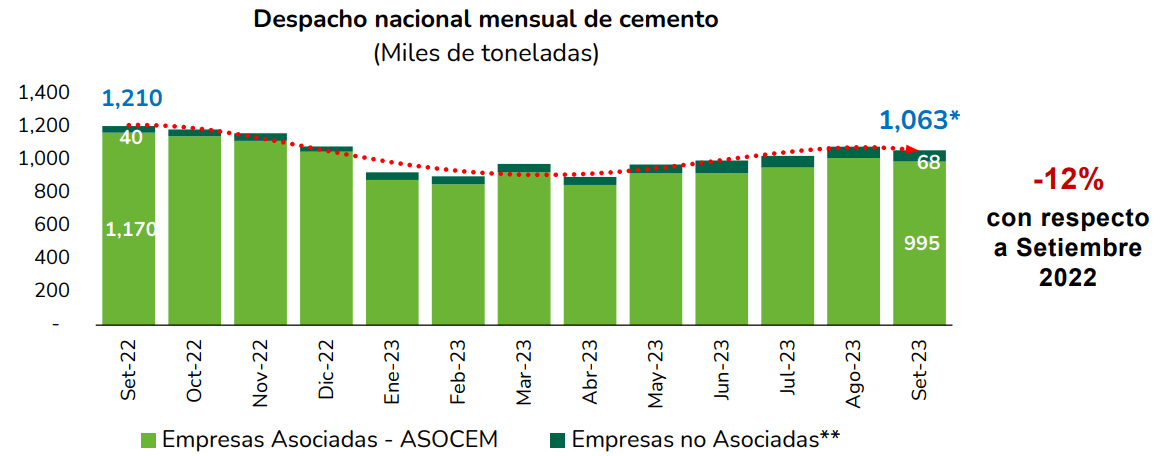

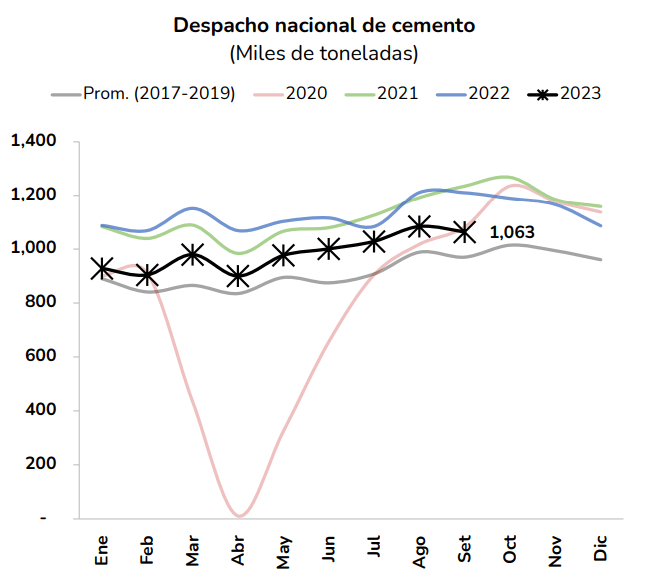

The Peruvian cement market also shares an interesting characteristic with many other countries in Latin America – the majority of demand comes from the so-called self-construction segment, which includes individuals that typically buy bags of cement to build or improve their homes. As a consequence, cement demand in Peru is sensitive to economic growth and it reached record levels in 2022 following the end of COVID-19 restrictions. While cement demand in Peru has been softening over the past several months, monthly shipments are still above the levels for the 2017-2019 period. According to data from the Association of Cement Producers of Peru (ASOCEM), cement deliveries in Peru for September 2023 were around 12% lower compared to September 2022 but about 10% higher compared to the same month for the 2017-2019 period. The figures seem even more impressive after you take into account that data from Peru’s INEI statistics agency showed that GDP contracted by 0.58% over the first eight months of 2023, with the construction sector shrinking by 9.63%.

{kind=link}

{kind=link}

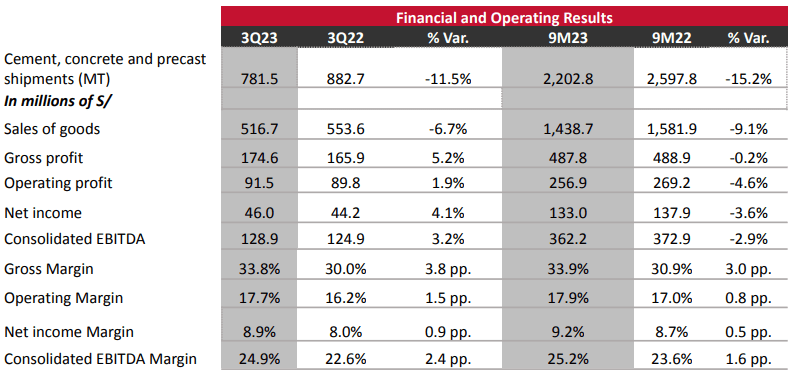

Turning our attention to the Q3 2023 financial results of Cementos Pacasmayo, I think they were decent as revenues went down by 6.7% year on year to 516.7 million Peruvian soles ($131.4 million) compared to a 12.1% annual decrease booked in Q2 2023. The company managed to boost product prices as the sales volume of cement, concrete and precast decreased 11.5%. The gross profit margin thus remained above the 39% level for the second consecutive quarter. The EBITDA margin of the company, in turn, rose by 2.4 percentage points to 24.9% and I’m optimistic it could be above 26% in Q4 2023.

{kind=link}

{kind=link}

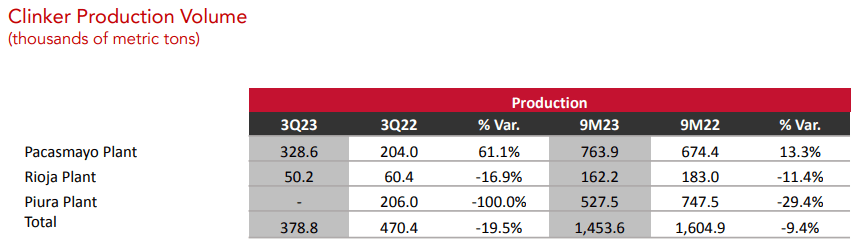

The company’s margins also received a boost from the completion of an $80 million investment in a new kiln at the Pacasmayo plant during Q3 2023, which increased its clinker capacity by 0.58 million MT/year. While Cementos Pacasmayo wasn’t importing any clinker in Q2 2023, the new facility still improved profitability by taking on production from more inefficient plants. As you can see from the table below, the clinker output decreased significantly at the Rioja plant, and it completely stopped at the Piura plant.

{kind=link}

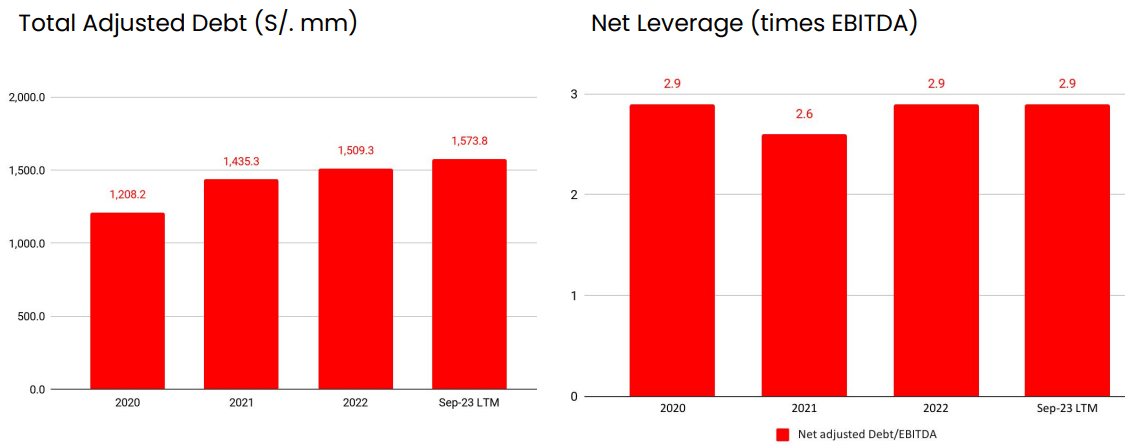

Looking at the balance sheet, total outstanding debt increased to 1.57 billion Peruvian soles ($414.5 million) as of September 2023 due to the investment in the new kiln. The net debt, in turn, came in at 1.39 billion Peruvian soles ($353 million). Yet, the net leverage ratio was at 2.9x, which is the same level as 2020 and 2022 and I think it seems manageable.

{kind=link}

Overall, I think that Q3 2023 was a decent quarter for Cementos Pacasmayo as cement demand in Peru remained above pre-pandemic levels despite macroeconomic headwinds. In my view, cement demand in the country is likely to hover around 1,000 MT per month in Q4 2023, and the company’s EBITDA for the quarter could surpass 130 million soles ($33.1 million).

Turning our attention to the valuation, Cementos Pacasmayo has an enterprise value of $769.7 million at the moment and is trading at EV/EBITDA ratio of 6.3x on a TTM basis. In my view, the company should be trading above 8x EV/EBITDA due to the strong cement demand in Peru as well as the company’s monopoly position in the northern part of the country. This level is equal to around $7.58 per ADR or an upside potential of 51.2%.

Looking at the downside risks, I think the major one is that Peru’s sluggish GDP growth could start negatively affecting cement in a major way over the coming months. This would put pressure on the revenues and EBITDA of Cementos Pacasmayo. In September, the Peruvian Central Bank revised its GDP growth projection for 2023 from 2.2% to 0.9%.

Investor takeaway

Cement demand in Peru continues to be strong despite low GDP growth and I think that Cementos Pacasmayo booked decent revenues in Q3 2023. In addition, the new kiln boosted EBITDA and I think the EBITDA margin could be above 26% in Q4 2023. The company is trading at 6.3x EV/EBITDA and it seems undervalued as cement demand is Peru is showing no signs of returning to pre-pandemic levels anytime soon.

For further details see:

Cementos Pacasmayo: Decent Q3 Results As Cement Demand In Peru Remains High